Waterborne Coatings Market Size, Share & Industry Analysis, By Resin Type (Acrylic, Polyurethane (PU), Epoxy, Alkyd, Polyester, Polytetrafluoroethylene (PTFE), Polyvinylidene Chloride (PVDC), Polyvinylidene Fluoride (PVDF), and Others), By Application (Architectural and Industrial), and Regional Forecast, 2026-2034

Waterborne Coatings Market Size and Future Outlook

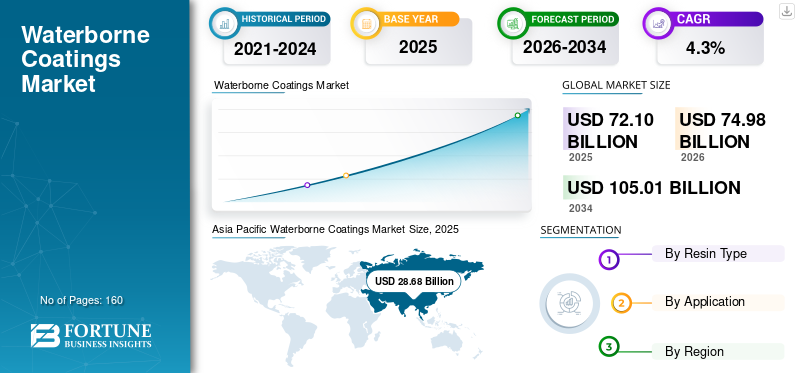

The global waterborne coatings market size was valued at USD 72.10 billion in 2025. The market is projected to grow from USD 74.98 billion in 2026 to USD 105.01 billion by 2034, exhibiting a CAGR of 4.3% during the forecast period. Asia Pacific dominated the waterborne coatings market with a market share of 39.77% in 2025.

Waterborne coatings are coating formulations that use water as the primary carrier for polymer binders and additives, enabling lower Volatile Organic Compound (VOC) emissions than conventional solvent-borne systems. They are supplied as architectural paints (interior/exterior), industrial maintenance and OEM coatings, wood coatings, primers, and specialty systems where performance is driven by film formation, adhesion, durability, corrosion protection, and compliance with application-specific standards.

The market growth is driven by tightening VOC regulations, expanding construction and renovation activities, and ongoing substitution of solvent-borne chemistries in selected industrial applications. Growth is further supported by advances in dispersion chemistry (acrylic, polyurethane dispersions, and waterborne epoxies), which continue to narrow the performance gap in durability and chemical resistance. At the same time, end-user qualification requirements, substrate preparation practices, and ambient cure constraints in some industrial settings continue to shape adoption pathways and product mix.

Furthermore, the market comprises several major players, including AkzoNobel, PPG Industries, Sherwin-Williams, BASF, and DOW, as well as raw-material and binder suppliers such as BASF and Dow. Broad product portfolios, formulation know-how, and manufacturing and distribution footprints support these companies' competitive positioning in the global market.

Download Free sample to learn more about this report.

Waterborne Coatings MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 72.10 billion

- 2026 Market Size: USD 74.98 billion

- 2034 Forecast Market Size: USD 105.01 billion

- CAGR: 4.3% from 2026–2034

- Asia Pacific dominated the waterborne coatings market with a 39.77% share in 2025.

- The acrylic segment held the largest resin type share at 39.8% in 2025.

- The architectural segment accounted for the largest application share of 65.2% in 2025.

North American

North America is expected to reach USD 15.67 billion in 2026, driven by remodeling activity and VOC regulations.

Europe

Europe is projected to reach USD 19.54 billion in 2026, expanding at a 4.4% CAGR during the forecast period.

Asia Pacific

Asia Pacific led the market with USD 28.68 billion in 2025 and is projected to reach USD 30.0 billion in 2026.

U.S.

The market reached USD 13.53 billion in 2025, supported by strong repaint demand and premium architectural coatings.

Japan

Demand is supported by increasing adoption of low-VOC waterborne coatings and sustainable construction practices.

Read More

WATERBORNE COATINGS MARKET TRENDS

VOC Regulations, Green-Building Requirements, and Performance-Driven Reformulation is a Key Market Trend

Waterborne coatings demand is increasingly shaped by VOC and air-quality regulations that encourage low-emission paints and industrial coatings, particularly in densely populated and industrialized regions. Regulatory pathways and procurement standards are driving higher-performance documentation and durability expectations, accelerating the adoption of advanced acrylic dispersions, polyurethane dispersions, and hybrid systems that improve scrub resistance, weatherability, and adhesion. In parallel, manufacturers are reformulating to manage coalescent content, film formation under low-temperature conditions, and label claims linked to indoor air quality and sustainability.

Alongside VOC pressure, faster project cycles and labor constraints are increasing attention on application efficiency, drying time, and early hardness, especially in architectural repaint and light industrial maintenance. Industrial waterborne systems are also expanding, enabling corrosion protection and appearance with acceptable cure windows and process control, raising demand for 2K waterborne PU and waterborne epoxy primers in select end uses. As sustainability reporting expands, suppliers are increasingly highlighting mass-balance and bio-attributed raw materials, recycled content packaging, and product stewardship documentation to support specification and procurement decisions.

- For instance, policy-driven building renovation and energy-efficiency programs in Europe support multi-year repainting and refurbishment cycles, thereby increasing demand for low-VOC architectural coatings.

MARKET DYNAMICS

MARKET DRIVERS

VOC Compliance, Architectural Repaint Cycles, and Expanding Waterborne Industrial Adoption Drives Market Growth

Architectural coatings remain the largest demand center for waterborne systems, supported by VOC limits and the practical need to reduce odor and improve applicator comfort in occupied spaces. Waterborne acrylic and styrene-acrylic emulsions are widely used in interior and exterior wall paints, primers, and trim coatings where durability, washability, and weather resistance are critical. Renovation and repaint activity provides a steady volume base, while premiumization toward higher-performance paints supports value growth.

In industrial settings, waterborne adoption is expanding in targeted segments such as general industrial, metal furniture, appliances, and selected protective maintenance applications where process control and cure conditions can be managed. Advances in waterborne epoxies, acrylic-epoxy hybrids, and 2K waterborne PU systems are enabling improved corrosion protection and chemical resistance, supporting substitution from solvent-borne systems in regulated or indoor manufacturing environments.

- For instance, industry bodies and regulators increasingly emphasize VOC reduction as a key lever for improving air quality, reinforcing waterborne adoption.

MARKET RESTRAINTS

Performance Trade-offs in Harsh Service Conditions, Cure-Sensitivity, and Line Qualification Costs Restricts Market Expansion

While waterborne technologies have advanced, certain high-performance industrial environments still favor solvent-borne, powder, or high-solids systems due to faster cure, superior chemical resistance, or proven long-term field data. Water sensitivity during application and early film formation can increase defect risk under high humidity, low temperature, or poor substrate preparation, especially for corrosion-protective and exterior industrial applications.

In OEM and regulated industrial lines, qualification timelines, specification lock-in, and production risk can slow substitution even when waterborne products meet laboratory performance requirements. Cost volatility in acrylic monomers, isocyanates, and key additives can also influence pricing and formulation decisions, while meeting multiple regional VOC and labeling requirements may increase compliance and documentation costs for global suppliers.

MARKET OPPORTUNITIES

Green Renovation Programs, Low-Emission Product Premiumization, and Waterborne Expansion Offer Growth Opportunities

Green renovation and energy-efficiency programs can expand demand for architectural coatings tied to refurbishment cycles, including primers, sealers, and high-durability topcoats that extend repaint intervals. Premiumization toward stain resistance, low odor, low-VOC/low-VOC content, and improved indoor air quality claims support higher realized pricing, especially in urban and regulated markets.

In industrial applications, opportunities exist for waterborne systems to meet corrosion and appearance requirements within acceptable process windows, such as appliances, general metal finishing, and selected protective maintenance categories. Product innovation in self-crosslinking acrylics, waterborne epoxy primers, and 2K waterborne PU topcoats, combined with application guidance and training, can expand the addressable market and improve conversion rates. These efforts drive the waterborne coatings market growth.

MARKET CHALLENGES

Multi-Regional Compliance, Application Condition Variability, and Field Performance Assurance Can Hamper Market Growth

A key challenge in waterborne coatings is managing multi-regional VOC frameworks, ecolabel criteria, and chemical disclosure requirements simultaneously, which increases formulation complexity and the cost of maintaining compliant product families across regions. Balancing low-VOC targets with film formation, open time, and early block resistance remains technically challenging for some interior and exterior formulations.

In industrial and protective applications, field performance is sensitive to substrate preparation, humidity/temperature conditions, and coating thickness control. Inconsistent application practices can reduce corrosion protection and aesthetics, increasing warranty risk and slowing conversion from incumbent solvent-borne systems. Manufacturers, therefore, need robust technical support, applicator training, and system-level qualification support to ensure reliable performance.

Download Free sample to learn more about this report.

Segmentation Analysis

By Resin Type

Widespread Architectural Applications and Performance Advantages Boost Acrylic Segment Growth

Based on resin type, the market is segmented into acrylic, Polyurethane (PU), epoxy, alkyd, polyester, Polytetrafluoroethylene (PTFE), Polyvinylidene Chloride (PVDC), Polyvinylidene Fluoride (PVDF), and others.

The acrylic segment accounted for the largest waterborne coatings market share in 2025. The segment’s growth is driven by broad use in interior and exterior architectural paints, where durability, scrub resistance, and color retention are prioritized. Mature dispersion supply chains, extensive formulation know-how, and strong contractor acceptance support high penetration across price tiers. Furthermore, the segment held a 39.8% share in 2025.

The Polyurethane (PU) segment is expected to grow significantly, driven by performance-oriented demand in wood coatings, floor coatings, and selected industrial applications that require improved abrasion resistance and aesthetics. The Polyurethane (PU) segment is projected to grow at a CAGR of 4.2% during the forecast period.

The epoxy segment is projected to grow significantly over the coming years. The segment’s growth is driven by broader use of waterborne epoxy primers and epoxy-modified systems in industrial maintenance and metal protection, where corrosion resistance is critical.

By Application

To know how our report can help streamline your business, Speak to Analyst

Architectural Segment Dominates the Market Due to the Extensive Use of the Product

By application, the market is categorized into architectural and industrial.

The architectural segment accounted for the largest market share in 2025. The segment's growth is driven by VOC compliance, strong repaint cycles, and preference for low-odor products in occupied buildings. Furthermore, the segment held a 65.2% share in 2025.

The industrial segment is also expected to grow favorably over the forecast period. The segment's demand is driven by gradual conversion in general industrial, appliances, metal furniture, and selected protective applications where waterborne systems meet performance targets. The segment is expected to grow at a CAGR of 4.0% over the forecast period.

Waterborne Coatings Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Waterborne Coatings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 28.68 billion, and is expected to maintain its leading share in 2026, valued at USD 30.0 billion. The region benefits from construction intensity, expanding urban infrastructure, and the rising penetration of waterborne paints across residential and commercial buildings. China remains the largest consumption base, while India and Southeast Asia continue to increase demand linked to housing, industrial growth, and distribution expansion.

China Waterborne Coatings Market

In 2025, the China’s market reached USD 15.32 billion. China’s market demand is supported by large-scale construction activities, continued repaint demand, and the gradual shift toward lower-VOC systems across select industrial value chains.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, estimated to reach USD 15.67 billion by 2026. The market’s growth is driven by repair and remodeling activity, regulatory pressure on VOCs, and continued premiumization in architectural paints. Industrial conversion remains selective, supported by OEM and maintenance use cases where waterborne systems meet performance and productivity requirements.

U.S. Waterborne Coatings Market

In 2025, the U.S. market reached USD 13.53 billion. The U.S. dominates regional consumption due to its large building stock, high repaint activity, and broad availability of premium waterborne architectural paints and coatings.

Europe

Europe is expected to experience significant growth over the coming years. During the forecast period, the region is projected to grow at a 4.4% rate, reaching a valuation of USD 19.54 billion in 2026. The market’s growth is supported by renovation activity, established VOC frameworks, and strong uptake of waterborne architectural coatings. The region benefits from mature manufacturing and distribution networks and an emphasis on sustainability documentation and performance compliance.

U.K. Waterborne Coatings Market

The U.K. market in 2025 was estimated at around USD 2.20 billion, representing approximately 3.6% of global market revenues.

Germany Waterborne Coatings Market

Germany’s market reached approximately USD 3.69 billion in 2025, equivalent to around 4.8% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 5.09 billion. The demand is concentrated in architectural paints, with variability across countries depending on construction cycles, renovation activity, and the pace of waterborne conversion in industrial coatings.

Brazil Waterborne Coatings Market

Brazil’s market reached approximately USD 2.45 billion in 2025, equivalent to around 3.6% of global sales.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-led construction in GCC markets, ongoing urban development, and the steady adoption of waterborne architectural coatings. Hot climates and cooling demand reinforce the need for durable exterior coatings, while industrial conversion remains selective by end use.

GCC Waterborne Coatings Market

GCC reached USD 1.92 billion by 2025, accounting for approximately 2.8% of global revenues. Commercial construction, infrastructure projects, and increased preference for low-odor, low-emission paint systems in indoor applications support GCC demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Expanding Deposits, Processing Footprints, and Specialty Grades to Maintain Their Market Positions

The market includes a mix of global paint and coating manufacturers and raw material suppliers that provide binders, additives, and formulation platforms. Competition is shaped by product performance, compliance and labeling, supply reliability, application support, and the ability to provide complete system solutions across architectural and industrial categories. Leading companies differentiate through dispersion chemistry, premium architectural brands, industrial qualification capability, and technical services that support specification and application quality. Some key market players include AkzoNobel, PPG Industries, Sherwin-Williams, BASF, and Dow.

LIST OF KEY WATERBORNE COATINGS COMPANIES PROFILED

- AkzoNobel (Netherlands)

- PPG Industries (U.S.)

- Sherwin-Williams (U.S.)

- BASF SE (Germany)

- Dow (U.S.)

- Jotun (Norway)

- Hempel (Denmark)

- Covestro AG (Germany)

- Arkema(France)

- DIC CORPORATION (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2026: PPG launched PPG AQUACRON Waterborne Shop Primers (WSP) for structural steel, featuring rapid curing and low VOCs, signalling performance-driven waterborne primer innovation aimed at throughput gains for fabricators and jobsite corrosion protection.

- February 2026: PPG launched PPG STEELGUARD 652, a water-based intumescent fire protection coating for interior structural steel (UL 263 certified), signalling continued expansion of certified waterborne protective coating platforms in construction/steel applications.

- October 2025: BASF Coatings expanded collaboration with Xiaomi and highlighted the supply of ColorBrite waterborne basecoat within full-layer coating systems for Xiaomi vehicle programs, signalling deeper OEM partnering and continued use/positioning of waterborne basecoat technology in automotive color programs.

- September 2024: Evonik launched TEGO Wet 570 Terra and TEGO Wet 580 Terra biosurfactants for waterborne coatings and inks (EU Ecolabel-compliant), signalling additive innovation aimed at higher bio-based content and more efficient pigment/filler wetting for sustainable waterborne formulations.

- February 2024: Covestro launched its Waterborne Coating Solutions initiative, developing waterborne and waterborne UV resin families for industrial coatings (wood furniture/cabinetry/building products), signalling a targeted push to raise performance and line efficiency while meeting water-based regulatory and customer pressure.

- October 2023: BASF launched ACRONAL MB (biomass-balance) acrylic binders for architectural coatings in North America, signalling product carbon-footprint reduction pathways for waterborne binder portfolios without requiring paint reformulation.

- March 2022: Allnex announced a multi-million-dollar upgrade at its Langley, South Carolina site to expand waterborne resin capacity (incl. acrylics, epoxy, and polyurethane dispersions), signalling investment to support North America’s shift toward greener waterborne industrial and decorative coatings.

- February 2022: PPG launched PPG ENVIROBASE ECP35 high-build primer surfacer for use with its Envirobase High Performance waterborne refinish system, signalling continued product-line expansion around waterborne automotive refinish productivity and lower-VOC performance.

- February 2021: Covestro announced plans for new Polyurethane Dispersion (PUD) and polyester resin plants at its Shanghai integrated site, aimed at meeting rising demand for waterborne coatings and adhesives and accelerating the replacement of solvent-based systems in Asia.

- May 2021: Axalta completed an expansion of its Jiading, Shanghai, waterborne coatings plant, adding waterborne basecoat/primer and small-batch capacity, and more than doubling site capacity, signalling a stronger local supply of eco-responsible OEM and industrial waterborne coatings in China/APAC.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of c% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Resin Type, Application, and Region |

| By Resin Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 72.10 billion in 2025 and is projected to reach USD 105.01 billion by 2034.

Recording a CAGR of 4.3%, the market is slated to exhibit steady growth during the forecast period.

The architectural application segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

AkzoNobel, PPG Industries, Sherwin-Williams, BASF, and Dow are among the prominent players in the market.

VOC compliance, architectural repaint cycles, and expanding waterborne industrial adoption is the key factor driving the market growth.

The major factors expected to favor product adoption in the market are comparable or improved performance with lower VOC/odor levels, safer handling, and the growing availability of advanced waterborne binders that meet compliance and OEM specification requirements.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us