White Chocolate Market Size, Share & Industry Analysis, By Form (Bars, Chips & Chunks, and Spreads), By Application (Confectionery, Bakery, Dairy & Frozen Desserts, Beverages, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

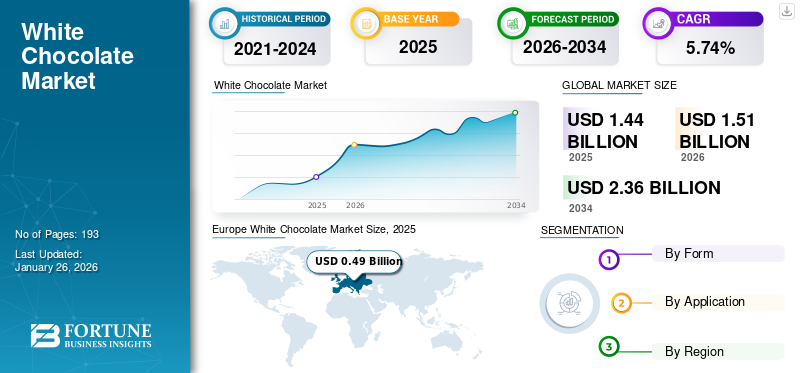

The global white chocolate market size was valued at USD 1.44 billion in 2025. The market is projected to grow from USD 1.51 billion in 2026 to USD 2.36 billion by 2034, exhibiting a CAGR of 5.74% during the forecast period. Europe dominated the white chocolate market with a market share of 33.86% in 2025.

Barry Callebaut, Cargill Inc., Fuji Oil Company Ltd., Mars Inc., and Hershey Company are a few key players in the industry.

White chocolate demand is primarily driven by factors such as the emerging confectionery industry growth, changing consumer purchasing behavior, and the emerging popularity of premium snacks. The surge in the artisanal bakery sector is another factor significantly contributing to product consumption worldwide. White chocolate allows food manufacturers to introduce new products beyond traditional white chocolate confectioneries. Thus, key players from the confectionery, beverages, and frozen desserts manufacturers are utilizing the product. This factor is projected to drive market growth in the upcoming years.

Download Free sample to learn more about this report.

White Chocolate Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 1.44 billion

- 2026 Market Size: USD 1.51 billion

- 2034 Forecast Market Size: USD 2.36 billion

- CAGR: 5.74% from 2026–2034

Market Share:

- Europe dominated the white chocolate market with a 33.86% share in 2025, driven by the region's growing demand for premium confectioneries, innovative product development using caramelized and infused white chocolate variants, and a strong artisanal bakery industry. Germany leads within Europe, where low-sugar white chocolate and white chocolate-based beverages are gaining popularity.

- By form, white chocolate bars held the largest market share in 2024 due to their convenience, portability, and wide usage across multiple food applications. The spreads segment is projected to grow at the fastest rate due to their creamy texture and versatility in bakery and dessert innovations.

Key Country Highlights:

- Germany: A key market in Europe where low-sugar white chocolate and chocolate-based beverages such as hot white chocolate are increasingly popular.

- United States: White chocolate demand is supported by festive gifting culture, rising snack consumption, and major players like Mars and Hershey introducing innovative offerings.

- India: Rising demand for plant-based and dairy-free confections is propelling growth, supported by startups like CARRA launching vegan white chocolate bars.

- Brazil: Urbanization and higher disposable incomes are encouraging white chocolate consumption across confectionery, bakery, and beverage segments.

- United Arab Emirates: Increasing consumption of cookies and baked goods is driving demand for white chocolate chips, slabs, and spreads used in premium bakery applications.

WHITE CHOCOLATE MARKET TRENDS

Caramelized Chocolate Trends is Gaining Popularity in the Industry

In recent years, caramelized white chocolate is gaining more traction in the confectionery industry. In the process of caramelizing, the chocolate receives nutty and slightly crunchy notes. Thus, its unique flavors, textures, and mouthfeel appeal to a wider consumer base. Companies are developing new products with zero-sugar and zero-calorie claims to excel the trend and commercialize the caramelized chocolate trend. It is likely to drive the market in the upcoming years. For instance, in August 2021, Barry Callebaut, one of the leading industrial chocolate manufacturers, introduced a premium caramelized white chocolate solution - Caramel Aura in different forms such as coatings and chips. The newly launched products are available in no-added flavors or colors for customers in North America.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Emerging Fusion Flavor in Food Applications to Drive Product Demand

A shift in consumer food preferences is creating opportunities for innovative and new-flavor food product development. As a result, local food processors and artisanal bakeries are sourcing locally developed ingredients to develop regional-inspired treats. Introducing seasonal menus and seasonal-specific flavors is also partially contributing to developing innovative flavors in food options. Since consumers are craving a sense of surprise in bakery and pastry products, the trend of unexpected flavor combinations by fusing local ingredients with classic ingredients is emerging. For instance, Le Levain Bakery, one of the artisanal bakeries in Singapore, developed matcha and white chocolate croissants with a new texture to offer onigiri croissants. Such instances are projected to contribute to the white chocolate consumption from the bakery industry. Therefore, the global white chocolate market growth is estimated to showcase a steady upward trend during the forecast period.

MARKET RESTRAINTS

Increasing Raw Material Price May Hamper Market Growth

White chocolate is made from cocoa butter, milk, and sugar. Cocoa butter is a vital ingredient in manufacturing the product. Over the past couple of years, the cocoa butter price has been exhibiting a sudden spike in the industry due to the reduced yield and availability of cocoa beans, which creates challenges in the supply chain. Furthermore, milk and sugar prices are also shifting to new heights. Altogether, it is increasing the operational overhead and reducing the profit margins of white chocolate manufacturers, which is anticipated to hamper the market growth during the forecast period.

MARKET OPPORTUNITIES

Increasing Plant-based Chocolate Product Developments to Change Industry Landscape

The vegan chocolate trend has been emerging across the world as a popular alternative to traditional chocolate, catering to consumers with dietary preferences such as veganism, lactose intolerance, or a desire for plant-based options. As dietary preferences evolve and awareness of ethical and environmental considerations grow, there has been a remarkable shift toward plant-based alternatives to traditional chocolate. A compassionate, dairy-free version of this beloved confection that caters to the burgeoning demand for cruelty-free, sustainable, and health-conscious food options. As a result, companies are developing new products without using milk and animal-sourced ingredients to commercialize the vegan trend. This factor is anticipated to drive the global market. In April 2022, CARRA, an Indian plant-based chocolate manufacturing company, launched its first dairy-free white chocolate bar to meet the consumer demand for vegan chocolate in the market.

Segmentation Analysis

By Form

Wide Availability, Convenience, and Portability are Likely to Drive Demand for White Chocolate Bars

Based on form, the market is divided into bars, chips & chunks, and spreads.

The white chocolate bars segment is projected to hold the highest market share in 2024. Key players such as Barry Callebaut, Fuji Oil, and Nestle are offering white chocolate in a bar format, as it offers less cost in processing and shaping the products. It is also used to caramelize white chocolate in different processed foods. Furthermore, the bar form of the chocolate offers more convenience and portability to food processors in storing and utilizing it according to their convenience. This factor is expected to drive the demand for the segment in the upcoming years.

The spreads segment is anticipated to expand with the fastest growth trajectory during the forecast period. White chocolate spreads offer more flexibility in incorporating and developing innovative sweet confectioneries and bakery products. Furthermore, spreads offer a premium, creamy texture to cake and dessert spreads.

By Application

Huge Application of Product Results in Confectionery Segment’s Dominance

Based on application, the market is segmented into confectionery, bakery, dairy & frozen desserts, beverages, and others.

The confectionery segment is expected to hold a major white chocolate market share. Increasing premium confectionery demand among consumers is unlocking a new venture for white chocolate manufacturers. White chocolate is significantly used in molding, coating, and enhancing the visual appeal of confectionery products. Its functional benefits and textural stability offer an advantage for confectionery manufacturers to adopt in developing novel product categories. As a result, the segment is anticipated to expand with a stable growth rate in the upcoming years.

The bakery segment is anticipated to expand at the highest growth rate during the forecast period. White chocolate, especially spreads, is widely utilized as fillings and toppings in bakery products such as cakes, buns, and pastries. It offers a vibrant texture and an appealing look to the bakery products. Therefore, white chocolate is gaining popularity in the segment.

White Chocolate Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe White Chocolate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Europe generated USD 0.49 billion, contributing 33.86% to global market revenue, and is projected to grow to USD 0.51 billion in 2026. The growth of the market is primarily driven by the rising demand for ready-to-eat snacks among consumers, the availability of a wide range of products, and the premiumization of the product offerings. White chocolate is one of the prominent chocolate types that is popular among consumers. New flavor innovations by including new ingredients, help to make the product popular among consumers. Products such as Blonde chocolate, which is made of white chocolate with caramel, help to create a unique taste profile in the chocolate products. Other ingredients, such as lemon, are also used in white chocolate to enhance the flavors. Additionally, increasing white chocolate production capacity across the region is further driving the industry in the region.

Germany is one of the leading markets within the region. The demand for high-quality chocolate products is increasing across the country. Chocolate drinks such as hot chocolate and other chocolate-flavored beverages are popular among consumers. Additionally, white chocolate with low sugar content is preferred over other chocolate products with high sugar content.

North America

North America maintained a strong presence in the global market, reaching USD 0.28 billion in 2025, accounting for 19.28% share, and is expected to reach USD 0.28 billion in 2026. North America is one of the stable markets for white chocolate. Chocolate has emerged as one of the most suitable gifting options in North America, especially in the U.S. and Canada, during festive seasons, which allows white chocolate manufacturers to experiment with their products and present exotic products on retail shelves and impress consumers. The U.S. is one of the key markets, and the growth of the product in the market has been driven by rising snacks and confectioneries popularity paired with the increased demand for ice cream and dairy-based desserts among consumers. Large international chocolate companies such as Mondelez, Barry Callebaut, Puratos, and Mars are constantly adopting strategies in order to tailor their product offerings in the country.

Asia Pacific

The Asia Pacific market accounted for USD 0.29 billion in 2025, representing 20.44% of the global industry, and is expected to reach USD 0.31 billion in 2026. The demand for white chocolate across the region, including China, India, Japan, and Australia, is expanding significantly, and several reasons are driving the growth of the market. The low price of white chocolate, its suitability for a wide range of applications, and the presence of a huge number of chocolate producers in the region are some of the major factors contributing to the amplified market size. Chocolate remains a popular choice for snacking, gifting, and celebrations, thereby fueling its demand in the market. The demand for dairy-free chocolates is increasing rapidly owing to the rising adoption of vegan diets. Therefore, chocolate manufacturers are launching white chocolates that are dairy-free and can be used to manufacture vegan food offerings for consumers. This factor is likely to drive the demand for white chocolate, resulting in the highest CAGR during the forecast period.

South America

In South American countries, the presence of all income-class consumers is prevalent, which is a growth-boosting factor for white chocolate products. Increasing urbanization, purchasing power, and the women working population are likely to drive the demand for chocolate-based confectionery products, including white chocolate. Furthermore, technological advancements, particularly within the chocolate market, have created significant opportunities for growth in the country. Consumers in Brazil and Argentina are becoming more sophisticated in their taste preferences, influencing the application of white chocolate in various food products such as confectionery, beverages, bakery, and others.

Middle East & Africa and Latin America

The Middle East & Africa white chocolate market is experiencing steady growth during the forecast period. In 2025, Middle East & Africa represented USD 0.21 billion, accounting for 14.78% of the worldwide market, and is projected to grow to USD 0.22 billion in 2026. The availability, as well as the affordability, of a vast range of cookies, is a critical factor contributing to the growing momentum of the white chocolate market. This ready-to-eat snack has emerged as one of the most consumed snacks, which is available in a variety of flavors such as choco chip, choco nut, and choco crème, among others. White chocolate in the form of chips, slabs, and spreads is also used in the production of cookies and other baked goods. Growing consumption of baked goods such as biscuits, cookies, and others in the region is also projected to boost product usage. Latin America contributed 11.64% to the global market in 2025, with a valuation of USD 0.17 billion, and is projected to reach USD 0.18 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Adopt Strategies such as Merger & Acquisition to Strengthen their Market Share

The global white chocolate market share is concentrated among a few key players and chocolate manufacturers. Barry Callebaut, Cargill Inc., Fuji Oil Company Ltd., Mars Inc., and Hershey Company are a few key players in the industry. They are involved in mergers & acquisitions, new product launches, product innovation, expanding base capacity, and strengthening e-commerce presence to achieve long-term business goals and stay ahead of the competitive curve. The industry landscape is expected to change significantly in the upcoming years. Barry Callebaut is one of the key companies, holding the highest share. The company is emphasizing M&A activities to strengthen its product range and clientele base in the market. In September 2021, the company acquired Europe Chocolate Company (ECC), a Belgian privately-owned B2B manufacturer of chocolate specialties and decorations. The ECC offers chocolate products, including white chocolate in chips, drops, and slab varieties.

LIST OF KEY WHITE CHOCOLATE COMPANY PROFILED

- Barry Callebaut AG (Switzerland)

- Cargill, Incorporated (U.S.)

- CEMOI Group (France)

- Fuji Oil Company Ltd. (Japan)

- Guittard Chocolate Company (U.S.)

- Kerry Group (Ireland)

- Mars Incorporated (U.S.)

- Mondelez International, Inc. (U.S.)

- Nestle S.A. (Switzerland)

- The Hershey Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025 — Cargill Inc., a key food ingredient manufacturing company, launched a new white chocolate product “Bright White” to enhance the visual appearance of bakers, confectioners, and ice cream products.

- March 2025 – Kind LLC., an American snack food company, launched white chocolate snack bars containing almonds and peanuts. The new product is a source of antioxidants, protein, and raspberries.

- January 2025 – Bramble Foods Group, a Leicestershire-based bakery and preservatives manufacturing company, acquired J.H. Whittaker and Sons, Ltd., an emerging confectionery company. Whittaker Chocolate offers white chocolate blocks and slabs.

- February 2024 – Nestle SA, a global food and beverage manufacturing company, launched a new white chocolate bar under its KitKat brand in the U.K.

- January 2024 – Sugar Bowl Bakery, one of the U.S. bakery product manufacturers, launched Cranberry Orange White Chocolate Bites® for developing on-the-go snacks and desserts.

REPORT COVERAGE

The global white chocolate market report analysis provides market share, size, and forecast by all segments included in the report. The report also offers information on market dynamics and trends that are expected to drive the market in the forecast period. It offers information on the prevalence of the product in key regions/countries, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. It covers the global industry analysis, a detailed competitive landscape with information on profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.15% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Form

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.44 billion in 2025 and is projected to record a valuation of USD 2.36 billion by 2034.

The market is expected to grow at a CAGR of 5.74% during the forecast period of 2026-2034.

By form, the bars segment led the market and held the highest share in 2025.

Emerging fusion flavor in food applications is projected to drive market growth.

Barry Callebaut, Cargill Inc., Fuji Oil Company Ltd., Mars Inc., and Hershey Company are a few key players in the industry.

Europe dominated the market in 2025 by holding the largest share.

Increasing plant-based chocolate product developments is the key opportunity in the market.

- 2021-2034

- 2025

- 2021-2024

- 193

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us