Window Lift Motors Market Size, Share & Industry Analysis, By Mechanism Type (Cable-Type Regulator Systems and Scissor-Type Regulator Systems), By Vehicle Type (Hatchbacks & Sedans, SUVs, LCVs, and HCVs), By Door Position (Front Window Lift Motors and Rear Window Lift Motors), By Sales Channel (OEM and Aftermarket), By Motor Type (Brushed DC Motor and Brushless DC (BLDC) Motor), and Regional Forecast, 2026–2034

Window Lift Motors Market Size and Future Outlook

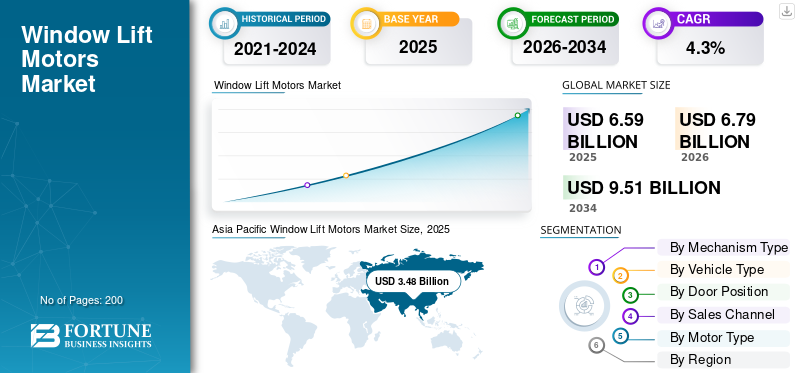

The global window lift motors market size was valued at USD 6.59 billion in 2025. The market is projected to grow from USD 6.79 billion in 2026 to USD 9.51 billion by 2034, exhibiting a CAGR of 4.3% during the forecast period. Asia Pacific dominated the window lift motors market with a market share of 52.81% in 2025.

Window lift motors are compact electric actuators installed inside vehicle doors that control the upward and downward movement of power windows, converting electrical energy into mechanical motion through gear-driven mechanisms. Key factors that stimulate market growth, increase market demand, and influence purchasing behavior include technological advancements, regulatory support, rising consumer income, urbanization, industry investments, and evolving customer preferences.

Major players in the market include Brose Fahrzeugteile, Bosch, Denso Corporation, Valeo, Mitsuba Corporation, and Johnson Electric. These players are competing through lightweight motor designs, enhanced durability, noise reduction technologies, and advanced power window automation solutions.

Download Free sample to learn more about this report.

Window Lift Motors Market Key Takeaways

- 2025 Market Size: USD 6.59 billion

- 2026 Market Size: USD 6.79 billion

- 2034 Forecast Market Size: USD 9.51 billion

- CAGR: 4.30% from 2026–2034

- Asia Pacific dominated the window lift motors market with a 52.81% share in 2025.

- The SUVs segment accounted for the largest market share in 2026.

- The cable-type regulator systems segment dominated the global market in 2026.

North America

North America remained the third-largest regional market in 2025.

Asia Pacific

Asia Pacific held 52.81% share in 2025, valued at USD 3.48 billion.

Europe

Europe market is projected to grow at a CAGR of 3.0% during the forecast period.

U.S.

The market in the U.S. is projected to reach USD 0.93 billion by 2026.

Japan

The market in Japan is projected to reach USD 0.73 billion by 2026.

Read More

WINDOW LIFT MOTORS MARKET TRENDS

Rising Vehicle Electrification and Premium Feature Integration to Accelerate Market Growth

Major market trends are the increasing electrification in passenger vehicles and the growing integration of comfort-focused features. These trends are significantly supporting the global window lift motors market growth. Automakers are standardizing power windows even in entry-level models, while premium vehicles incorporate anti pinch, one-touch, and smart control functionalities. The shift toward electric vehicles further strengthens product demand, as EV platforms rely entirely on electrically operated subsystems. Continuous innovation in compact motor design and improved efficiency is reinforcing long-term market expansion.

- According to IEA, in 2025, the global electric car sales are projected to exceed 20 million units, representing more than 25% of total car sales worldwide. During the first quarter of 2025, electric vehicle sales increased by 35% compared to the same period last year.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Consumer Preference for Comfort and Convenience to Drive Market Demand

Consumers increasingly prioritize comfort, safety, and ease of use in modern vehicles, directly driving the demand for window lift motors. Features such as automatic up/down functions, remote-controlled window operation, and integration with central locking systems are becoming common expectations. Urbanization and rising disposable incomes, particularly in emerging economies, are encouraging higher adoption of power window systems. This evolving consumer behavior is influencing OEM production strategies and contributing positively to overall market growth.

MARKET RESTRAINTS

High Replacement and Maintenance Costs to Restrain Market Penetration

Despite steady demand, high replacement and maintenance costs associated with window lift motor failures act as a restraint in the market. Malfunctioning regulators, worn-out gears, and electrical issues can increase repair expenses, especially in aging vehicles. Price-sensitive consumers in developing regions may delay replacements or opt for low-cost alternatives, affecting premium product adoption. Additionally, fluctuating raw material prices can influence manufacturing costs, limiting profit margins and moderating overall market expansion.

MARKET OPPORTUNITIES

Integration of Smart and Connected Vehicle Technologies to Create New Opportunities

The rapid advancement of connected vehicle ecosystems presents strong opportunities in the market. Integration with vehicle control units, smartphone apps, and advanced driver assistance systems allows intelligent window positioning, remote diagnostics, and enhanced safety monitoring. Automakers are investing in sensor-enabled motors with anti-trap and obstacle detection features. These innovations enhance user safety and also open avenues for higher-value product offerings, strengthening competitive positioning and future revenue potential.

- In October 2025, Porsche filed a patent for a Tunnel Mode that uses onboard cameras and sensors to detect tunnels and automatically lower windows, engage sport mode, open active exhaust valves, and downshift gears to enhance engine acoustics. A secondary mode can keep windows up and activate noise cancellation.

MARKET CHALLENGES

Supply Chain Volatility and Semiconductor Dependency to Challenge Production Stability

The market faces challenges related to supply chain disruptions and semiconductor dependency. Modern motor assemblies increasingly incorporate electronic control modules that rely on microchips and precision components. Global shortages, logistics bottlenecks, and geopolitical uncertainties can delay production cycles and impact OEM supply commitments. Such disruptions may affect timely vehicle deliveries and increase component costs. Managing supply chain resilience and diversifying sourcing strategies remain critical to sustaining consistent market performance.

Segmentation Analysis

By Vehicle Type

Rising Production and Premium Feature Adoption to Strengthen SUVs Segment Growth

Based on vehicle type, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates the global window lift motors market share and is also the fastest growing, supported by the rising global SUV production and increasing consumer preference for premium features. SUVs typically integrate advanced power window systems with one-touch, anti-pinch, and remote-control functionalities across all doors. Higher average selling prices and feature-rich configurations increase motor value per vehicle, strengthening market share. Growing electrification in SUVs further accelerates the demand for efficient, compact window lift motor systems.

- According to IEA, in 2023, SUVs represented 48% of the total global car sales, setting a new record and reinforcing one of the most prominent automotive trends of the 21st century, the growing consumer preference for larger and heavier vehicles.

The hatchbacks & sedans segment accounts for the second-largest share and is projected to grow at a CAGR of 3.3% over the forecast period. Strong global production volumes and widespread adoption of the product across entry and mid-level models sustain steady replacement and OEM demand.

To know how our report can help streamline your business, Speak to Analyst

By Mechanism Type

Lightweight Design and Cost Efficiency to Drive Cable-Type Regulator Systems Segment Growth

Based on mechanism type, the market is sub-divided into cable-type regulator systems and scissor-type regulator systems.

The cable-type regulator systems segment dominates the market and is also the fastest growing, primarily due to its lightweight structure, compact design, and lower manufacturing cost. Automakers increasingly prefer cable-based systems for modern vehicles as they enable smoother operation, reduced noise, and easier integration within tight door architectures. Their compatibility with advanced motor assemblies and anti-pinch technologies further strengthens adoption across passenger cars and SUVs.

The scissor-type regulator systems segment is projected to grow at a CAGR of 2.7% over the forecast period. Although known for durability and structural strength, their heavier design and higher material usage limit widespread adoption in lightweight vehicle platforms.

By Door Position

Higher Functional Complexity and Usage Frequency to Strengthen Front Window Lift Motor Leadership

Based on door position, the market is bifurcated into front window lift motors and rear window lift motors.

The front window lift motors segment dominates the market, as front windows are used more frequently and integrate advanced functionalities such as one-touch operation, anti-pinch safety, and master control integration. These motors are typically more sophisticated and higher in value compared to rear units. Driver-side priority controls and regulatory safety requirements further contribute to stronger OEM installation rates and sustained aftermarket replacement demand.

The rear window lift motors segment is projected to grow at a CAGR of 4.9% over the forecast period. Increasing rear passenger safety features, rising SUV adoption, and expanding rear-seat comfort enhancements are accelerating installation rates globally.

By Sales Channel

Strong OEM Production Volumes and Feature Standardization to Reinforce OEM Segment Dominance

Based on sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates the market and is also the fastest growing, driven by rising global vehicle production and increasing standardization of power windows across all vehicle categories. Automakers are integrating advanced window lift motor systems during vehicle assembly to ensure quality, safety compliance, and seamless electronic integration. Growing SUV production and vehicle electrification further support OEM installation rates, strengthening global market share during the forecast period.

- In January 2023, Ford filed a patent for an automatic window control system that uses environmental sensors, vehicle speed data, and rain detection to autonomously adjust window positions, improving cabin comfort, aerodynamics, and weather responsiveness.

The aftermarket segment is projected to grow at a CAGR of 3.9% over the forecast period. Replacement demand from aging vehicle fleets and motor wear-related failures sustains steady revenue generation across independent workshops and authorized service centers.

By Motor Type

Cost-Effectiveness and Established Supply Chains to Sustain Brushed DC Motor Demand

Based on motor type, the market is divided into brushed DC motor and brushless DC (BLDC) motor.

The brushed DC motor segment dominates the market due to its cost-effectiveness, simple design, and widespread adoption across mass-market vehicles. Established manufacturing infrastructure and mature supply chains enable large-scale production at competitive prices. These motors provide reliable performance for standard power window applications, making them a preferred choice among OEMs for entry-level and mid-range vehicle models.

The brushless DC (BLDC) motor segment is projected to grow at a CAGR of 5.2% over the forecast period. Higher efficiency, longer lifespan, lower noise levels, and better compatibility with advanced electronic control systems are accelerating adoption, particularly in premium and electric vehicles.

Window Lift Motors Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Window Lift Motors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to register the fastest CAGR during the forecast period. The region benefits from high vehicle production volumes in China, India, Japan, and South Korea, alongside expanding SUV penetration and rising vehicle electrification. Growing middle-class income levels and increasing demand for comfort-oriented features are strengthening OEM installations. Additionally, the presence of major automotive component manufacturers and cost-competitive supply chains supports sustained market growth and regional expansion.

China Window Lift Motors Market

The China market is estimated to touch around USD 2.04 billion in 2026, accounting for roughly 30.0% of global revenues. Strong domestic vehicle production, SUV dominance, EV expansion, and integrated local supply chains sustain leadership and OEM-driven growth.

Japan Window Lift Motors Market

The Japan market is estimated to reach around USD 0.73 billion in 2026, accounting for roughly 10.7% of global revenues. Advanced vehicle engineering, premium feature integration, hybrid production strength, and export-oriented manufacturing support steady technological adoption.

India Window Lift Motors Market

The India market is estimated to touch around USD 0.27 billion in 2026, accounting for roughly 4.0% of global revenues. Rapid passenger vehicle expansion, rising SUV demand, localization initiatives, and improving income levels drive the fastest-growing regional momentum.

Europe

Europe holds the second-largest market share and is projected to grow at a CAGR of 3.0% over the forecast period. Strong production of premium and luxury vehicles across Germany, France, and Italy supports higher-value motor installations. Advanced safety regulations and consumer preference for technologically enhanced vehicles encourage the integration of anti-pinch and smart control systems. Furthermore, the region’s growing electric vehicle production contributes to consistent OEM demand, reinforcing stable market growth despite moderate production expansion rates.

Germany Window Lift Motors Market

The Germany market is estimated to touch around USD 0.39 billion in 2026, accounting for roughly 5.8% of global revenues. Premium vehicle manufacturing, strong EV transition, and advanced safety system integration sustain stable OEM demand.

U.K. Window Lift Motors Market

The U.K. market is estimated to reach around USD 0.08 billion in 2026, accounting for roughly 1.8% of global revenues. Niche vehicle production, luxury segment presence, and steady aftermarket replacements support moderate growth.

North America

North America represents the third-largest market, supported by strong SUV and pickup truck production in the U.S. and Mexico. High penetration of power window systems across vehicle categories sustains OEM demand. Additionally, an aging vehicle parc generates steady aftermarket replacement requirements, particularly for front door motor assemblies. Technological advancements in connected vehicle platforms further support the integration of advanced motor systems, ensuring moderate yet stable market growth across the region.

U.S. Window Lift Motors Market

The U.S. market is estimated to reach around USD 0.93 billion in 2026, accounting for roughly 14.1% of global revenues. High SUV and pickup production, advanced feature standardization, and robust replacement demand reinforce consistent market expansion.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing gradual expansion. Increasing vehicle ownership, improving economic conditions, and infrastructure development are supporting automotive production and imports. Although the adoption of advanced motor technologies remains comparatively moderate, the rising demand for mid-range vehicles with power window systems is strengthening OEM installations. Growing distributor networks and service infrastructure are further contributing to steady long-term market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Deploy Innovation, Lightweight Engineering, and OEM Partnerships to Outpace Competitors

The market is moderately fragmented, with global Tier-1 suppliers and regional manufacturers competing across OEM and aftermarket channels. Key players in the global market include Brose Fahrzeugteile, Bosch, Denso Corporation, Valeo, Mitsuba Corporation, and Johnson Electric. These companies focus on lightweight assemblies, noise reduction technologies, and enhanced durability. Companies strengthen their competitiveness through long-term OEM contracts, localized production, and integration of anti-pinch and smart control modules. Strategic collaborations and capacity expansions further support market share consolidation across high-growth automotive manufacturing hubs.

LIST OF KEY WINDOW LIFT MOTORS COMPANIES PROFILED

- brose Fahrzeugteile Gmbh Co Kg (Germany)

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- Valeo SA (France)

- Mitsuba Corporation (Japan)

- Johnson Electric Holdings Limited (Hong Kong)

- Aisin Corporation (Japan)

- Magna International Inc. (Canada)

- Inteva Products, LLC (U.S.)

- Hi-Lex Corporation (Japan)

- Nidec Corporation (Japan)

- Shanghai SIIC Transportation Electric Co., Ltd. (SITEC) (China)

- DY Corporation (South Korea)

- IFB Automotive Pvt. Ltd. (India)

- Kongsberg Automotive ASA (Norway)

KEY INDUSTRY DEVELOPMENTS

- December 2025: General Motors revealed plans for enhanced power window switch systems that integrate advanced electronic architecture, enabling improved diagnostic capability, modular control integration, and compatibility with evolving vehicle software platforms.

- October 2025: Nidec announced a USD 19 million investment to expand its Mena, Arkansas, facility. The move aimed at increasing manufacturing capacity for precision electric motors used in automotive applications, enhancing automation capabilities, and strengthening localized production efficiency in North America.

- May 2025: Bosch Japan introduced advanced automotive actuators supporting LIN-based electronic control, enhanced motor efficiency, and compact integration. These features help improving precision control and durability for power window and door module systems.

- April 2025: Brose unveiled next-generation door systems integrating lightweight cable regulators, anti-pinch safety sensors, and energy-optimized motors. The new solutions help reduce door module weight while enhancing NVH performance and system reliability.

- November 2024: Inteva Products expanded its Pune manufacturing facility, increasing production capacity for window regulators and motor assemblies to meet the rising global OEM demand and improve localized supply efficiency.

- January 2024: Winco Window Company introduced an ADA-compliant window system engineered with reduced operating force requirements, accessible hardware positioning, and optimized opening mechanisms to meet Americans with Disabilities Act guidelines while maintaining structural and thermal performance standards.

- May 2022: Aisin expanded its window regulator portfolio, offering vehicle-specific assemblies with improved corrosion resistance, reinforced cable mechanisms, and OEM-grade fitment to strengthen aftermarket replacement coverage.

REPORT COVERAGE

The global window lift motors market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. Furthermore, it includes details on the market dynamics and trends expected to drive the market over the forecast period. It also offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Mechanism Type, By Vehicle Type, By Door Position, By Sales Channel, By Motor Type, and By Region |

| By Mechanism Type |

|

| By Vehicle Type |

|

| By Door Position |

|

| By Sales Channel |

|

| By Motor Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.59 billion in 2025 and is projected to reach USD 9.51 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 3.48 billion.

The market is expected to exhibit a CAGR of 4.3% during the forecast period of 2026-2034.

The SUVs segment leads the market in terms of vehicle type.

The growing consumer preference for comfort and convenience is a key factor driving the market.

Major players in the market include Brose Fahrzeugteile, Bosch, Denso Corporation, Valeo, Mitsuba Corporation, and Johnson Electric.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us