Wired Drill Pipe Market Size, Share & Industry Analysis, By Component (Wired Drill Pipe Body, Telemetry System, Surface Equipment, and Others), By Application (Onshore and Offshore), and Regional Forecast, 2026-2034

Wired Drill Pipe Market Size and Future Outlook

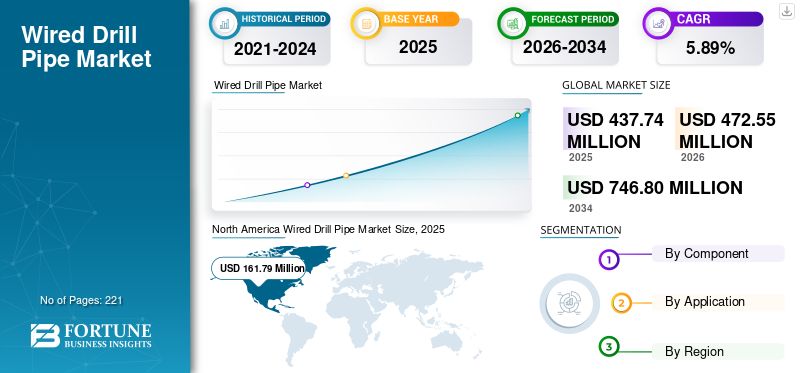

The global wired drill pipe market size was valued at USD 437.74 million in 2025. The market is projected to grow from USD 472.55 million in 2026 to USD 746.80 million by 2034, with a CAGR of 5.89% over the forecast period. North America dominated the wired drill pipe market with a market share of 36.96% in 2025.

Wired Drill Pipe (WDP) is an advanced type of drill pipe equipped with an embedded data transmission system that enables high-speed, real-time communication between downhole tools and surface systems during drilling operations. Unlike conventional mud-pulse telemetry, it uses electrical or inductive connections to transmit large volumes of data instantly. This technology enhances drilling efficiency, improves well placement accuracy, and supports better decision-making in complex wells such as deep-water, HPHT, and extended-reach drilling.

The market growth is primarily driven by the increasing demand for real-time downhole data and digital drilling technologies. As oil and gas operators focus on improving drilling efficiency and reducing non-productive time, WDP enables faster data transmission compared to conventional telemetry systems. Additionally, the rise in deep-water, ultra-deep-water, and complex onshore wells (HPHT and extended-reach drilling) is accelerating adoption, as these environments require high-speed and reliable communication. Growing investments in offshore exploration, particularly in regions such as Latin America and the Middle East, further support market expansion. Moreover, the industry’s shift toward automation, predictive analytics, and intelligent well construction is driving demand for advanced telemetry solutions, such as wired drill pipe.

The leading players in the market, such as NOV Inc., SLB, Baker Hughes Company, Halliburton Company, and Weatherford International plc, are focusing on continuous technological innovation and digital integration to strengthen their market position. Their efforts are centered on developing high-speed telemetry systems, advanced sensors, and real time data transmission capabilities to enhance drilling efficiency and accuracy. Additionally, these companies are investing heavily in automation, data analytics, and remote drilling operations, enabling smarter and more efficient well construction. Strategic initiatives such as partnerships, product launches, and expansion into deep-water and complex well projects further support their growth. Overall, their combined focus on digital drilling ecosystems, performance optimization, and integrated service offerings is driving the evolution of the WDP market.

Download Free sample to learn more about this report.

Wired Drill Pipe Market Trends

Digitalization and Real-Time Drilling Intelligence is a Key Market Trend

A key market trend is the rapid shift toward wired drill pipe technologies, such as digital drilling and real-time, data-driven decision-making. WDP enables data transmission speeds 10–100 times faster than conventional mud pulse telemetry, allowing operators to access downhole data almost instantaneously. This has led to increased adoption in high-spec wells, particularly in offshore and extended-reach drilling, where even small delays can cost hundreds of thousands of dollars per day. For instance, offshore rig operating costs can exceed USD 200,000–USD 500,000 per day, making real-time optimization highly valuable. Companies are increasingly integrating WDP with advanced analytics and automation platforms, enabling predictive drilling and remote operations. These technological advancements align with the broader oilfield digital transformation, where operators aim to reduce drilling time by 10–20% and improve well placement accuracy, thereby enhancing overall project economics.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Complexity of Wells and Offshore Exploration to Boost the Global Market

The primary driver of the WDP market is the increasing complexity of oil and gas exploration, particularly in deep-water, ultra-deep-water, and High-Pressure High-Temperature (HPHT) environments. These wells require continuous, high-speed data to monitor formation conditions and drilling parameters. Offshore drilling in Oil and Gas Industry is expanding, especially in regions such as Brazil and the Middle East, where complex reservoirs demand advanced technologies. For example, deep-water wells can cost USD 50–100 million each, making efficiency and accuracy critical. WDP systems enable faster formation evaluation and decision-making, reducing Non-Productive Time (NPT) by up to 15–25%. As operators push into more technically challenging reserves to meet global energy demand, the need for reliable, high-bandwidth telemetry solutions continues to grow, directly driving WDP adoption.

Market Restraints

Dependence on Oil Price Cycles and Drilling Activity to Limit the Market Expansion

The WDP market is highly dependent on oil price fluctuations and upstream capital expenditure cycles, which are major restraints. During periods of low oil prices, operators tend to reduce exploration and production spending, directly impacting demand for advanced drilling technologies. For example, during oil price downturns, global rig counts can decline by 20–40%, significantly reducing the need for high-end tools, such as WDP. Since WDP is primarily used in premium drilling environments, it is often among the first technologies to be deferred or scaled back during budget cuts. This cyclical nature creates volatility in market growth and limits long-term investment visibility for suppliers. Consequently, the market’s growth trajectory remains closely tied to global energy prices and upstream investment trends.

Market Opportunities

Expansion into Emerging Markets and Geothermal Drilling to Create New Growth Avenues

A significant opportunity for the WDP market lies in expanding into emerging regions and new applications, such as geothermal drilling. Asia Pacific and the Middle East are witnessing increasing investments in complex drilling projects, with national oil companies gradually adopting advanced technologies. Even a modest increase in WDP penetration by 5–10% in these regions could translate into substantial revenue growth. Additionally, geothermal wells, which often operate at high temperatures and in complex formations, can benefit from real-time data transmission similar to that in oil and gas wells. As global geothermal capacity is expected to grow steadily as part of the energy transition, WDP offers a viable solution to improve drilling efficiency in this sector. This diversification beyond traditional oil and gas applications opens new avenues for wired drill pipe market growth during the forecast period.

Market Challenges

High Capital Cost and Limited Adoption in Conventional Wells to Limit Market Growth

One of the key market challenges is the high capital and operational costs, which limit widespread adoption, especially in conventional and low-complexity wells. Wired drill pipe can cost 3–5 times as much as standard drill pipe, with prices ranging from USD 500–800 per foot, compared to USD 80–150 per foot for conventional pipe. This significant cost premium makes it economically unviable for many onshore or shallow wells where advanced telemetry is not essential. Additionally, the initial investment in supporting infrastructure, training, and maintenance further increases the total cost of ownership. As a result, adoption remains concentrated in high-value wells such as offshore and HPHT environments. This cost barrier slows market penetration and creates a gap between technological capability and actual field deployment.

Segmentation Analysis

By Component

Exploration & Drilling of New Oil Wells to Lead the Segment Growth

Based on component, the market is segmented into wired drill pipe body, telemetry system, surface equipment, and others.

The wired drill pipe body segment accounted for approximately 64.73% of the market share. The wired drill pipe body forms the structural backbone of the WDP system and remains the most fundamental component in drilling operations. Its demand is closely tied to overall drilling activity, rig deployment, and replacement cycles. While the segment is relatively mature, it continues to benefit from ongoing drilling in offshore and high-complexity wells. Innovation in this space focuses on improving durability, fatigue resistance, and performance under extreme conditions, such as high pressure and temperature.

Telemetry system segment is expected to grow at a CAGR of 6.76% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

High Existence and Expansion of Onshore Wells to Propel Segment Growth

Based on application, the market is segmented into onshore and offshore.

The onshore segment held the largest wired drill pipe market share of 69.21% in 2025. The onshore segment represents the largest and most established application area for wired drill pipe, primarily due to the high number of active rigs and continuous drilling activity, especially in shale and unconventional resources. Operators on land have increasingly adopted WDP to improve drilling efficiency, optimize well placement, and reduce non-productive time. The technology is particularly valuable in long horizontal wells, where precise geosteering is critical for maximizing hydrocarbon recovery.

The offshore segment is expected to grow at a CAGR of 6.28% during the forecast period.

Wired Drill Pipe Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Wired Drill Pipe Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in the market valued at USD 161.79 million in 2025, accounting for approximately 36.96% of the global market. North America is the most technologically advanced market for wired drill pipe, driven by high strength shale development and widespread horizontal drilling. The U.S. alone operates 700–800 active rigs and drills over 12,000–15,000 horizontal wells annually, many of which require precise geosteering and real-time downhole data. In basins such as the Permian, where lateral lengths often exceed 10,000–15,000 feet, WDP plays a key role in optimizing well placement and reducing drilling time. Offshore activity in the Gulf of Mexico also supports demand, with deepwater wells reaching water depths beyond 1,500 meters and requiring advanced telemetry for pressure and safety management. The strong presence of leading oilfield service companies and early adoption of digital drilling technologies make North America the most mature and innovation-driven market.

U.S. Wired Drill Pipe Market

The U.S. market was estimated at USD 128.91 million in 2025 and is set to reach USD 138.62 million in 2026. The U.S. is the most advanced market for wired drill pipe, driven by large-scale shale drilling and long horizontal wells often exceeding 10,000 feet. Operators prioritize real-time data to optimize geosteering and reduce drilling time across high-activity basins such as the Permian. Offshore projects in the Gulf of Mexico further support demand due to the complexity of deepwater operations and high operational costs.

Asia Pacific

The Asia Pacific market is valued at USD 116.65 million in 2025, accounting for approximately 26.65% of global market revenues. Asia Pacific is a high-volume but relatively underpenetrated market for wired drill pipe, with strong growth potential. Countries such as China and India collectively drill tens of thousands of wells annually, including deep and high-pressure wells exceeding 5,000–7,000 meters in depth. Offshore exploration is expanding in regions such as Southeast Asia and offshore India, where water depths typically range from 1,000 to 2,500 meters. While adoption of WDP is still developing compared to North America, operators are increasingly recognizing its value in improving drilling efficiency and reducing uncertainty in complex reservoirs. The region’s growing energy demand and shift toward deeper and more technically challenging wells are expected to drive gradual adoption of advanced telemetry technologies.

China Wired Drill Pipe Market

China remains the dominant contributor in the Asia Pacific, estimated at USD 38.20 million in 2025 and set to reach USD 41.84 million in 2026. China is a high-volume drilling market with thousands of wells drilled annually, including deep and ultra-deep wells exceeding 6,000 meters. The increasing complexity of unconventional and tight reservoirs is driving the gradual adoption of advanced telemetry technologies. While penetration of wired drill pipe is still developing, the scale of drilling activity creates strong long-term potential.

India Wired Drill Pipe Market

India was estimated at USD 20.50 million in 2025 and is expected to reach USD 22.47 million in 2026. India’s market is expanding with increasing exploration in both onshore and offshore regions, including deepwater fields in the Krishna-Godavari Basin. Wells often involve high-pressure conditions, requiring improved monitoring and control systems. Adoption of the product is growing as operators focus on enhancing drilling efficiency and reducing uncertainties.

Indonesia Wired Drill Pipe Market

Indonesia was valued at USD 14.10 million in 2025 and is likely to reach USD 15.42 million in 2026. Indonesia’s market is driven by offshore exploration and redevelopment of mature fields, with water depths often exceeding 1,000 meters. Complex geological formations and declining reservoirs require better real-time data for efficient drilling. Product adoption is gradually increasing as operators aim to improve recovery and reduce operational risks.

Europe

Europe accounted for USD 95.65 million in 2025, representing approximately 13.93% of global revenues. Europe’s market is largely offshore-focused, with activity concentrated in the North Sea. Countries such as Norway and the U.K. operate in challenging environments where wells often exceed 4,000–6,000 meters in depth and involve complex geological formations. Offshore drilling costs in this region can exceed USD 200,000 per day per rig, making real-time data transmission critical for minimizing non-productive time and improving operational efficiency. The region also emphasizes safety and environmental performance, which drives adoption of technologies that enhance well control and monitoring. In addition to oil and gas, Europe is gradually exploring geothermal drilling projects, where deep and high-temperature wells benefit from high-speed telemetry systems similar to those used in hydrocarbon exploration.

Germany Wired Drill Pipe Market

Germany was estimated at USD 9.55 million in 2025 and is expected to reach USD 10.26 million in 2026. Germany represents a niche market with limited oil and gas drilling activity but growing interest in geothermal projects. Deep geothermal wells require high-temperature and high-pressure monitoring, where wired drill pipe can provide operational advantages. The market is small but offers potential through energy transition initiatives.

U.K. Wired Drill Pipe Market

The U.K. market was valued at USD 15.79 million in 2025 and is projected to reach USD 16.89 million in 2026. The U.K. market is centered around the North Sea, where offshore wells are technically complex and require precise monitoring. High operating costs per rig enable real time telemetry, essential for minimizing non-productive time. Product adoption is supported by the need for efficiency and safe operations in mature offshore fields.

Latin America

Latin America accounted for USD 28.94 million in 2025, or approximately 6.61% of global revenues. Latin America’s market is strongly influenced by deepwater and ultra-deepwater exploration, particularly in Brazil’s pre-salt basins. Wells in this region are often drilled to depths exceeding 2,000 meters, with total well depths reaching 6,000–7,000 meters, making real-time data transmission essential for safe and efficient operations. Offshore wells in Latin America are among the most expensive globally, often costing USD 80–120 million per well, which increases the importance of technologies that can reduce risk and optimize drilling performance. Mexico is also expanding offshore exploration, further supporting demand. As operators focus on maximizing recovery from complex reservoirs, the adoption of wired drill pipe continues to grow in high-value offshore projects.

Middle East & Africa

The Middle East & Africa were valued at USD 34.71 million in 2025. The region is characterized by large-scale drilling activity and increasingly complex reservoir conditions. The Middle East alone drills thousands of wells annually, many of which involve extended-reach and high-pressure formations exceeding 15,000–20,000 psi. Countries such as Saudi Arabia and the UAE are focusing on maximizing recovery from mature fields through advanced drilling techniques, including long horizontal wells that benefit from real-time data transmission. In Africa, offshore drilling in countries such as Nigeria and Angola involves water depths of 1,500–2,000 meters or more, where WDP enhances well control and operational efficiency. Although adoption is still evolving, national oil companies are gradually investing in digital drilling technologies, creating a steady pathway for WDP integration across the region.

GCC Wired Drill Pipe Market

The GCC market was estimated at USD 21.94 million in 2025 and is set to reach USD 24.12 million in 2026. The GCC region is characterized by large-scale drilling programs and long horizontal wells in mature oil fields. High-pressure reservoirs and extended-reach drilling create strong demand for advanced telemetry solutions. National oil companies are increasingly investing in digital drilling technologies, supporting the gradual adoption of wired drill pipe systems.

Competitive Landscape

KEY INDUSTRY PLAYERS

Increasing Investment in High Technologies and Solutions Boosts Market Share of Companies

Key Players such as NOV Inc., SLB, Baker Hughes Company, Halliburton Company, and Weatherford International plc maintain their leadership in the wired drill pipe market through a shared focus on integrated technology development, digital drilling solutions, and high-performance telemetry systems. Collectively, they invest heavily in advancing real-time downhole data transmission, automation, and analytics-driven drilling optimization, enabling faster and more accurate decision-making in complex wells. Their efforts also include end-to-end service integration, combining hardware (drill pipe), telemetry, and surface systems into unified offerings that enhance operational efficiency for clients. Additionally, these players actively pursue strategic collaborations, field deployments in deepwater and HPHT environments, and continuous product innovation, ensuring reliability and performance in harsh conditions. This combined emphasis on technology leadership, global operational scale, and digital transformation is what positions them as dominant players in the industry.

List of Key Wired Drill Pipe Companies Profiled

- NOV Inc. (U.S.)

- SLB (U.S.)

- Baker Hughes Company (U.S.)

- Halliburton Company (U.S.)

- Weatherford International plc (U.S.)

- IntelliServ (U.S.)

- Reelwell AS (Norway)

- APS Technology (U.S.)

- Tenaris S.A. (Luxembourg)

- Vallourec S.A. (France)

- TMK Group (Russia)

- Jindal Saw Ltd. (India)

- Forum Energy Technologies (U.S.)

- Dril-Quip Inc. (U.S.)

- Hunting PLC (U.K.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: NOV Inc. has been supporting Aker BP since 2019 by deploying its DBS wired drill pipe technology to deliver real-time downhole data, improving drilling efficiency, well placement, and risk management. Under a new agreement, Aker BP plans to expand the use of this technology across additional rigs starting in 2025 to further enhance operational performance.

- January 2025: Reelwell AS secured a contract with Vår Energi, in partnership with Odfjell Technology, to deploy its DualLink powered wired drill pipe offshore on the Norwegian Continental Shelf for the first time. The solution combines real-time data transmission with continuous downhole power supply, improving drilling efficiency, tool performance, and overall operational control.

- March 2024: Parker Wellbore and TDE Group formed an exclusive alliance to deploy and commercialize TDE’s powerline™ technology globally. This solution enables continuous downhole power and high-speed data transmission, improving drilling efficiency, reducing non-productive time, and enhancing safety. It also supports more sustainable operations by lowering emissions and eliminating the need for conventional components such as pulsers, turbines, and batteries.

- July 2023: Optime Subsea successfully tested a high-speed wireless communication system for subsea well completion at the Nova field offshore Norway. The system enabled full wireless installation of a tubing hanger without using wired drill pipe, marking a significant advancement in subsea operations and reducing reliance on conventional wired technologies.

- March 2023: Equinor awarded new drilling contracts for the rigs Transocean Encourage and Transocean Enabler, along with a strategic collaboration agreement. The program includes nine wells in the Norwegian Sea and North Sea, with potential expansion to additional wells, and is valued at around USD 191 million. The campaign is set to begin in December and supports continued development across multiple offshore fields.

REPORT COVERAGE

The wired drill pipe market report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.89% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 437.74 million in 2025 and is projected to reach USD 746.80 million by 2034.

In 2025, the North America market value stood at USD 161.79 million.

The market is expected to grow at a CAGR of 5.89% over the forecast period.

By component, the wired drill pipe body segment led the market.

Rising complexity of wells and offshore exploration are the key factors driving the market.

NOV Inc., SLB, Baker Hughes Company, Halliburton Company, and Weatherford International plc are the major players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 221

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us