Adaptive Engines Market Size, Share & Industry Analysis, By Platform (Sixth-generation Fighter Aircraft, Fifth-Generation Fighter Upgrade Pathways, and Others), By Engine Architecture (Adaptive-cycle engines, Variable-Cycle Engines, and Others), By Component (Fan & Compressor System, Combustor & Turbine System, and Others), By Development Stage (Concept Design & Tech Maturation, Prototype Engine Build & Ground Testing, and Others), By Application (Air superiority & penetrating combat, and Others), By End User (Air Forces, Naval Aviation Forces, and Others), and Regional Forecast, 2026-2034

Adaptive Engines Market Size and Future Outlook

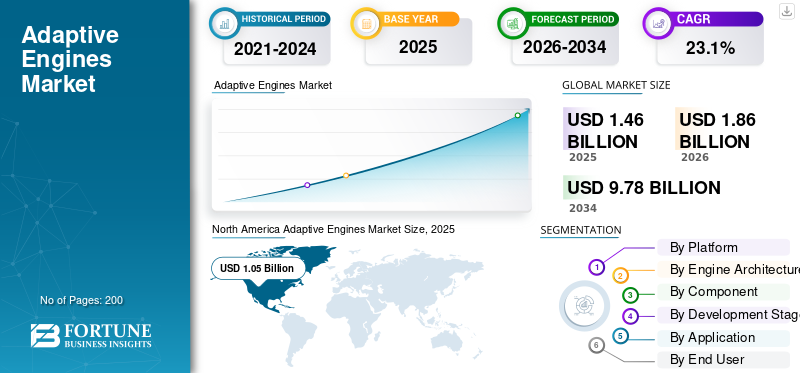

The adaptive engines market size was valued at USD 1.46 billion in 2025. The market is projected to grow from USD 1.86 billion in 2026 to USD 9.78 billion by 2034, exhibiting a CAGR of 23.1% during the forecast period.

Adaptive engines are military aircraft propulsion systems that can dynamically adjust airflow and operating mode during flight to balance thrust, fuel consumption, cooling, and fuel efficiency. The market is driven by increasing air force demand for adaptive engines that can support fighter jets with longer range, stronger thermal management, high performance, and better efficiency in air dominance missions.

Key players include GE Aerospace, Pratt & Whitney, Rolls-Royce Holdings plc., Safran Aircraft Engines SAS, MTU Aero Engines AG, IHI Corporation, and Avio Aero S.r.l. These companies are evolving adaptive cycle and generation adaptive propulsion through demonstrator programs, GCAP, FCAS/SCAF, and pushing engine technologies from test stages toward military aircraft integration.

Download Free sample to learn more about this report.

ADAPTIVE ENGINES MARKET TRENDS

Shift from Traditional Fighter Propulsion to Adaptive-Cycle Architectures Fuels Product Demand

One major trend influencing the global market is the shift from traditional fighter propulsion to adaptive-cycle and three-stream engine architectures. As future fighter jets are required to operate over longer ranges, hotter electronic loads, and perform more demanding air-dominance missions, traditional engine designs face challenges in balancing thrust, cooling, and fuel efficiency. As a result, demand for adaptive engines is rising around next-generation military aviation programs. Their capability to deliver improved fuel economy, enhanced thermal management, and high performance during combat without sacrificing cruise efficiency boosts the adaptive engines market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Inclination toward Sixth-Generation Combat Aircraft to Drive Product Demand

A major driver for the global market is the shift toward sixth-generation combat aircraft and future air-dominance programs. Modern fighter jets need longer operational range, lower fuel consumption, stronger cooling, and greater onboard power for sensors, electronic warfare, and mission computers. These evolving requirements are increasing demand for adaptive engines, which can dynamically shift between thrust-focused and cruise-efficient operating modes. For air forces, these capabilities translate into better fuel efficiency and high performance during the long-range combat missions where traditional engine architectures are approaching their performance limits.

MARKET RESTRAINTS

High Integration Cost and Qualification Risks to Restrain Market Growth

A major restraint on the market is the high cost and technical complexity associated with integrating the adaptive engine into existing military aircraft platforms. While adaptive propulsion can improve fuel efficiency, cooling, and high performance, its implementation also requires extensive modification to airframe structure, inlet/exhaust layout, software, thermal systems, testing, certification, and sustainment planning. These integration challenges can increase program costs, making adoption less attractive for legacy fighter aircraft. As a result, defense organizations are required to choose between a lower-risk engine upgrade and a full adaptive cycle replacement. Although demand for adaptive engines is strong for future aircraft platforms, near-term retrofit adoption is restrained by cost, schedule, and qualification complexity.

MARKET OPPORTUNITIES

Sixth-Generation Fighter and CCA Programs Create Strong Market Opportunity

A major opportunity for the market lies in the transition from standalone fighter jets to future combat-air ecosystems centered on sixth-generation aircraft and collaborative combat aircraft. These next-gen systems need propulsion technologies capable of reducing fuel consumption, improving fuel efficiency, supporting higher onboard power, and managing heat to support advanced sensors, electronic warfare, and mission computers. As air forces globally pursue longer operational range and air-dominance capabilities, demand for adaptive engine technologies is expected to move beyond experimental programs and into real aircraft integration. This creates a strong opportunity for companies working on adaptive cycle, three-stream cooling, and advanced engine technologies for next-generation military aircraft.

MARKET CHALLENGES

Reductions in R&D Budgets to Limit Market Growth

A major challenge facing the market is its dependence on large-scale, classified, and politically sensitive combat-air programs. Even though demand for adaptive engines is strong, market growth can be affected by delays in fighter aircraft procurement, reductions in R&D budgets, or decisions to extend the service life of existing aircraft rather than invest in new platforms. This is especially important for fighter jets and future military aircraft, where adaptive cycle propulsion requires specialized suppliers, long testing cycles, advanced materials, and deep airframe integration.

For instance, in July 2025, Axios reported that the U.S. administration had paused the U.S. Navy’s F/A-XX next-generation fighter program due to concerns that the defense industry could be stretched by supporting both the Navy’s F/A-XX and the U.S. Air Force’s F-47 programs at the same time.

Impact of Russia-Ukraine and Middle East Conflicts

Russia-Ukraine, Middle East Conflicts, and Wider Security Tensions to Drive Product Demand

The Russia-Ukraine war, Middle East conflicts, Red Sea tensions, and wider Indo-Pacific security concerns are pushing governments to reassess long-range airpower capabilities, fleet survivability, and future air-dominance requirements. For the market, this has an indirect effect, as fighter aircraft and advanced military aircraft require larger combat range, reduced fuel usage, enhanced cooling capabilities, and improved fuel efficiency. This increases the demand for adaptive engines, especially in air force modernization programs, where they can support high performance, thermal management, and improved efficiency across strike, escort, and penetrating combat missions.

For instance, in April 2024, SIPRI reported that global military expenditure reached a record USD 2.44 trillion in 2023, rising 6.8% from 2022, with increases across all regions and strongly driven by the Russia-Ukraine war, Middle East tensions, and broader militarization.

Segmentation Analysis

By Platform

Sixth-Generation Fighter Aircraft Segment Dominated the Market due to its Ability to Provide Superior Performance in Challenging Operational Conditions

In terms of platform, the market is categorized into sixth-generation fighter aircraft, fifth-generation fighter upgrade pathways, unmanned combat aircraft/CCA, advanced demonstrator aircraft, and other military aircraft.

The sixth-generation fighter aircraft led the market in 2025, as future combat aircraft are being developed with long ranges, low fuel consumption, greater power generation, enhanced cooling capacity, and superior performance in challenging operational conditions. Sixth-generation fighters require engines capable of transitioning between cruise operation and combat thrust. This makes adaptive engine adoption more relevant for new-build aircraft than for retrofit programs, where integration costs and certification risks remain higher.

The other military aircraft segment is expected to grow at the highest CAGR of 33.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Engine Architecture

Adaptive-Cycle Engines Segment Dominated the Market, as it Directly Addresses the Core Propulsion Problem

On the basis of engine architecture, the market is classified into adaptive-cycle engines, variable-cycle engines, three-stream engines, and adaptive fan/core upgrades.

The adaptive cycle engines segment held the largest global adaptive engines market share in 2025, as it directly addresses the core propulsion problem facing future fighter jets, the need to deliver high thrust during battles while minimizing fuel usage during cruising and long-range missions. The flexibility of an adaptive cycle enables these engines to achieve enhanced fuel efficiency, effective thermal management, and outstanding performance. Therefore, adaptive engines are more relevant to sixth-generation military aircraft and future air- superiority initiatives than fixed-cycle engines, as customers increasingly seek longer range, reduced reliance on aerial tankers, and efficient performance from next-generation engine systems.

The three-stream engines segment is expected to grow at a CAGR of 32.2% over the forecast period.

By Component

Fan & Compressor System Segment Dominated the Market, Driven by its Critical Role in Thrust Management

By component, the market is divided into fan & compressor system, combustor & turbine system, third-stream & thermal management, engine control & digital system, advanced materials & manufacturing, nozzle, exhaust & integration, and testing & support equipment.

The fan & compressor system segment dominated the market in 2025, as it forms the foundation of how an adaptive engine manages airflow, pressure ratio, thrust response, cooling, and fuel consumption. In adaptive cycle propulsion, the fan and compressor are not passive components; they play a critical role in determining whether airflow is directed toward higher thrust, better fuel efficiency, or enhanced thermal management. This makes the segment particularly important for future fighter jets and military aircraft that need high performance during combat while maintaining fuel efficiency during cruise operations.

The third-stream & thermal management segment is expected to grow at a CAGR of 29.8% over the forecast period.

By Development Stage

Rising Deployment of Next-Generation Military Aircraft Boosted Prototype Engine Build & Ground Testing Segment Growth

On the basis of development stage, the market is classified into concept design & tech maturation, prototype engine build & ground testing, aircraft integration & flight testing, low-rate initial production, and sustainment, spares & support.

The prototype engine build & ground testing segment held the dominant market share in 2025, due to the need for adaptive propulsion to be proven on test stands before aircraft installation. An adaptive engine requires testing of fan performance, compressor stability, adaptive cycle switching, cooling flow, thermal management, controls, fuel consumption, and durability under extreme operating conditions. For future military aircraft and sixth-generation fighter jets, this stage is critical, as air force buyers cannot leap from concept design to flight testing without demonstrating the engine’s ability to provide fuel efficiency, high performance, and reliable efficiency performance across various mission profiles, resulting in segment dominance.

The low-rate initial production segment is expected to grow at a CAGR of 62.6% over the forecast period.

By Application

Need for Improved Fuel Efficiency without Sacrificing Combat Missions Supported Air Superiority & Penetrating Combat Segment Growth

By application, the market is divided into air superiority & penetrating combat, extended-range strike & escort, power & thermal management, fuel efficiency & loiter extension, prototype testing & demonstration, and others.

Air superiority & penetrating combat held the largest market share in 2025, as future fighter jets are being developed to operate within enemy territory without compromising their range, speed, cooling, and survival capabilities. In these missions, adaptive engines play an important role by providing superior combat performance and high thrust while improving efficiency and lowering fuel consumption during cruise or penetrating phases.

The power & thermal management segment is expected to grow at a CAGR of 30.1% over the forecast period.

By End User

Air Forces Dominated the Market, Driven by Increasing Procurement of New Generation Fighter Aircraft

Based on end user, the market is segmented into air forces, naval aviation forces, defense R&D agencies, aircraft OEMs/integrators, and engine OEMs & tier suppliers.

The air forces segment held the largest market share in 2025, as air forces are the primary customers driving demand for future combat aircraft, new generation fighter aircraft, and air-dominance initiatives. Air forces require propulsion systems capable of increasing the combat range, decreasing fuel use, improving fuel economy, and supporting greater cooling capacity to meet the increased needs of sensors, electronic warfare capabilities, and mission computers.

The naval aviation forces segment is expected to grow at a CAGR of 30.1% over the forecast period.

Adaptive Engines Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Adaptive Engines Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share and is anticipated to grow at a CAGR of 19.7% during the forecast period, driven by the U.S.’s growing investment in next-generation fighter aircraft, adaptive propulsion R&D, established aircraft OEMs, and engine technology leadership. The region’s growth is anchored by the U.S. Air Force’s future air-dominance programs, which require fighter jets with longer range, lower fuel consumption, enhanced cooling capacity, and higher onboard power for sensors, electronic warfare, and mission computers. GE Aerospace and Pratt & Whitney also give North America a clear supplier advantage in adaptive cycle and three-stream engine technologies, making the region the most advanced market for transitioning adaptive engine from demonstrator testing toward future military aircraft integration.

U.S. Adaptive Engines Market

Based on North America’s strong contribution to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 1.02 billion in 2025, growing at a CAGR of 19.5% during the forecast period.

Europe

Europe market is anticipated to grow at a CAGR of 29.1% during the forecast period, supported by GCAP, FCAS/SCAF, Eurofighter, and Rafale replacement planning, and wider NATO airpower modernization initiatives. The region’s demand is linked to future military aircraft that need longer range, lower fuel consumption, enhanced cooling capabilities, and greater onboard power. The U.K. and Italy are advancing through GCAP, while France, Germany, and Spain are tied to FCAS/SCAF. Russia is included in Europe, but sanctions and limited access to Western engine technologies restrict its addressable role.

France Adaptive Engines Market

France market reached approximately USD 0.04 billion in 2025 and is anticipated to grow at a CAGR of 30.1% during the forecast period.

Germany Adaptive Engines Market

Germany market reached approximately USD 0.03 billion in 2025 and is anticipated to grow at a CAGR of 31.2% during the forecast period.

Asia Pacific

Asia Pacific is anticipated to grow at the highest CAGR of 20.6% over the forecast period, driven by China’s next-generation combat-aircraft program, Japan’s participation in GCAP, India’s AMCA program, South Korea’s KF-21 development, and Australia’s MQ-28 Ghost Bat initiatives. The region’s large operating distances and rising air force modernization needs are increasing demand for the product that improves fuel efficiency, reduces dependence on aerial tankers, and supports high-performance fighter jets and collaborative CCA platforms.

China Adaptive Engines Market

The Chinese market stood at around USD 0.06 billion in 2025 and is anticipated to grow at a CAGR of 30.4% during the forecast period.

India Adaptive Engines Market

The Indian market stood at around USD 0.02 billion in 2025, accounting for roughly 32.3% of Asia Pacific revenues.

Rest of the World

The rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a CAGR of 22.4% during the forecast period. The region is gaining development in Türkiye, GCC countries, Israel, Brazil, and selected defense-aerospace ecosystems. The Middle East & Africa leads this region, supported by the KAAN fighter program, Turkish UCAV development, Israeli unmanned systems capabilities, and Gulf air force modernization. Latin America is primarily driven by modernization, with Brazil’s Gripen/Embraer/Saab ecosystem supporting limited opportunities related to military aircraft upgrades, digital controls, fuel consumption improvement, and future unmanned systems.

Latin America Adaptive Engines Market

The market in Latin America reached around USD 0.01 Billion in 2025 and is anticipated to grow at a CAGR of 18.1% during the forecast period.

Middle East & Africa Adaptive Engines Market

The Middle East & Africa market stood at around USD 0.02 Billion in 2025 and is expected to reach USD 0.17 billion by 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Certified Military Aircraft Programs to Strengthen Their Market Position

The global adaptive engine market is led by a small group of advanced propulsion companies with deep capability in adaptive cycle design, fan and compressor systems, hot-section materials, digital controls, and thermal management. GE Aerospace and Pratt & Whitney lead development efforts in the U.S., and Rolls-Royce, Safran Aircraft Engines, MTU Aero Engines, Avio Aero, and IHI are positioned through GCAP and FCAS/SCAF-linked propulsion programs.

Competition is shifting from engine demonstrator development toward aircraft-level integration for sixth-generation fighter jets. Key players are focusing on lower fuel consumption, better fuel efficiency, higher cooling capacity, and high performance for air-dominance missions. Companies that successfully transition adaptive engine technologies from ground testing to certified military aircraft programs are likely to hold the strongest position in the market.

LIST OF KEY ADAPTIVE ENGINES COMPANIES PROFILED

- GE Aerospace (U.S.)

- Pratt & Whitney, an RTX business (U.S.)

- Rolls-Royce Holdings plc. (U.K.)

- Safran S.A. (France)

- MTU Aero Engines AG (Germany)

- Avio Aero S.r.l. (Italy)

- IHI Corporation (Japan)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Aero Engine Corporation of China (AECC) (China)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Boeing was selected to build the U.S. Air Force’s future F-47 fighter under the Next Generation Air Dominance program. The initial contract was valued at around USD 20 billion, supporting the development of a sixth-generation platform that would integrate with autonomous drones and require advanced adaptive propulsion systems.

- December 2024: BAE Systems, Leonardo, and Japan Aircraft Industrial Enhancement Co. (JAIEC) announced a joint venture to develop and deliver the Global Combat Air Programme (GCAP) next-generation fighter aircraft.

- July 2024: The GCAP engine demonstrator consortium moved into the design phase for the U.K.-Italy-Japan global combat air programme fighter aircraft. Under this program, Rolls-Royce Holdings plc, Avio Aero S.r.l., and IHI Corporation are collaborating on the next-generation power and propulsion system.

- May 2024: GE Aerospace’s XA102 next-generation adaptive-cycle fighter engine reportedly completed another round of ground testing. The XA102 is positioned as GE Aerospace’s adaptive engine solution for the U.S. NGAD/F-47 propulsion requirement.

- February 2024: Pratt & Whitney completed a key design review for its XA103 Next-Generation Adaptive Propulsion engine offering. The development supports next-generation fighter propulsion focused on adaptive cycle operation, cooling, thrust, and fuel efficiency.

- March 2023: The U.S. Air Force decided to proceed with the F135 Engine Core Upgrade for the F-35 program instead of adopting a full adaptive-cycle replacement engine.

- August 2022: The U.S. Air Force awarded Next Generation Adaptive Propulsion (NGAP) prototype-engine development contracts to multiple contractors, including GE Aviation and Pratt & Whitney. The contract is worth up to USD 975 million, supporting adaptive-cycle engine work for future sixth-generation combat aircraft.

REPORT COVERAGE

The global adaptive engines market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry experts’ developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By Engine Architecture

|

|

|

By Component

|

|

|

By Development Stage

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.46 billion in 2025 and is projected to reach USD 9.78 billion by 2034.

In 2025, the North American market value stood at USD 1.05 billion.

The market is expected to exhibit a CAGR of 23.1% during the forecast period.

By platform, the sixth-generation fighter aircraft segment led the market.

Rising inclination toward sixth-generation combat aircraft is the key factor driving market growth.

Key players in the market include GE Aerospace, Pratt & Whitney, Rolls-Royce Holdings plc., Safran S.A., MTU Aero Engines AG, Avio Aero S.r.l., IHI Corporation, Mitsubishi Heavy Industries, Ltd., Hanwha Aerospace Co., Ltd., and Aero Engine Corporation of China.

North America dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us