Air-to-Air Missiles Market Size, Share & Industry Analysis, By Missile Range Type (Short, Medium, Beyond Visual, Very Long, and Training/Captive Missile), By Range Capacity (10 km to Above 300 km), By Guidance Technology (Infrared Homing, AI/Autonomy-Enabled Guidance, GPS/GNSS-Aided Guidance, & Inertial Guidance), By Seeker Type, By Propulsion System, By Speed, By Airframe (Conventional Tail-Control Missile, Folding-Fin Missile, and Others), By Component, By Procurement Type (New Missile Production, Replacement Stockpile, Development Programs, and Others), & Regional Forecast, 2026-2034

AIR-TO-AIR MISSILES Market Size and Future Outlook

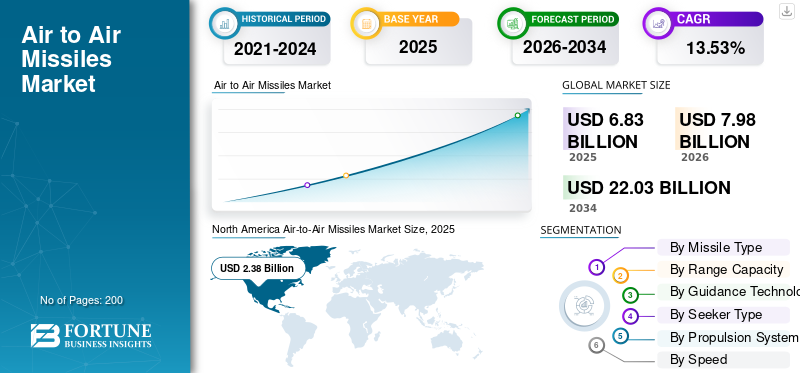

The global air-to-air missiles market size was valued at USD 6.83 billion in 2025. The market is projected to grow from USD 7.98 billion in 2026 to USD 22.03 billion by 2034, exhibiting a CAGR of 13.53% during the forecast period. North America dominated the air to air missiles market with a market share of 34.84% in 2025.

The air-to-air missiles market covers aircraft-launched weapons used to destroy enemy aircraft, helicopters, UAVs, cruise missiles, and other aerial threats across short range, within visual range, and beyond visual range combat scenarios. This is a sovereign-procurement market rather than a normal commercial market, with demand driven by fighter modernization programs, air-superiority competition, NATO and Indo-Pacific stockpile rebuilding efforts, and the shift toward longer-range, network-enabled missiles capable of operating effectively in heavy electronic warfare environments.

A key growth driver is the resurgence of high-end air warfare, as countries increasingly prioritize “first-shot/first-kill” capability to engage hostile aircraft before they can close the operational distance. Global military spending increased in 2025, with particularly strong growth observed across Europe and Asia/Oceania, while IISS has highlighted the rapid expansion of stockpiling munitions programs following the exposure of limited missile inventories during the Russian invasion of Ukraine conflict.

Major players include RTX Corporation, Nammo AS, MBDA Group, Diehl Defence GmbH & Co. KG, Saab AB, and so on. Major companies are focusing on next-generation air-combat weapon development and fighter platforms integration ecosystems to strengthen their competitive positioning and drive growth in the global market.

Download Free sample to learn more about this report.

Air to Air Missiles Market Key Takeaways

- 2025 Market Size: USD 6.83 Billion

- 2026 Market Size: USD 7.98 Billion

- 2034 Forecast Market Size: USD 22.03 Billion

- CAGR: 13.53% from 2026–2034

- North America dominated the air-to-air missiles market with a 34.84% share in 2025.

- The very long-range air-to-air missile segment is projected to grow at the fastest CAGR of 15.82% during the forecast period.

- The above 300 km segment is expected to register the highest CAGR of 16.05% through 2034.

North America

North America led the global market with a value of USD 2.38 billion in 2025 and maintained its leadership position in 2026.

Europe

Europe is projected to register the fastest regional growth and was valued at USD 1.46 billion in 2025.

Asia Pacific

Asia Pacific was valued at USD 2.03 billion in 2025, supported by increasing defense modernization programs.

U.S.

The market was valued at USD 2.28 billion in 2025 and is expected to grow at a CAGR of 12.80%.

Japan

The market was valued at USD 0.45 billion in 2025 and is projected to expand at a CAGR of 15.53% during the forecast period.

Read More

Air-to-Air Missiles Market Trend

Integration of Advanced Propulsion and Seeker Technologies to Fuel Market Development

The main technology trend in the air-to-air missiles market is shifting from a sole focus on missile range toward enhanced survivability, seeker flexibility, datalink performance, and endgame energy retention. Meteor’s ramjet motor gives thrust through the intercept phase and MBDA positions it as having the largest no-escape zone in its class, while its platform list includes Eurofighter Typhoon, F-35, Gripen, and Rafale. MICA NG shows the same technological direction in a smaller missile platform. According to MBDA, the system offers up to 40% greater range versus MICA, a dual-pulse motor, AESA RF seeker, passive imaging IR seeker, and 360-degree launch-envelope capability.

For instance, in December 2025, MBDA, Lockheed Martin Corporation, and the F-35 Joint Program Office completed critical ground-based integration tests for the Meteor Missile on the F-35A Lightning II, including ground vibration testing and fit checks for internal weapons-bay carriage.

Market Dynamics

MARKET DRIVER

Download Free sample to learn more about this report.

Rise in Defense Expenditure to Amplify Product Demand

The strongest growth driver in the market is the return of high-intensity air warfare planning. Air forces are no longer buying fighters alone; they are rebuilding full air-combat packages around BVR missiles, WVR missiles, training rounds, software support, test equipment, and classified sustainment packages.

According to SIPRI’s release published on April 27, 2026, global military spending reached USD 2,887 billion in 2025, with Europe recording growth of 14.00% and Asia/Oceania increasing by 8.10%. This rise in defense expenditure is directly supporting demand for modern fighter weapons and air-superiority inventories. The U.S. Air Force also describes AMRAAM as an all-weather, beyond-visual-range missile procured for U.S. and allied aircraft, underscoring its continued role as a core weapon in allied fighter modernization programs.

For instance, in February 2026, RTX’s Raytheon signed up-to-seven-year framework agreements with the U.S. Department of War to expand critical munition production, including AMRAAM, and stated that annual AMRAAM production would rise to at least 1,900 missiles.

MARKET RESTRAINT

Supply Chain Bottlenecks in Critical Missile Components to Deter Industry Development

The biggest restraint in the market is not demand but the industry’s ability to build, test, certify, and deliver missiles at the required pace. Air-to-air missiles production depend on highly constrained subsystems and components such as solid rocket motors, energetic materials, seekers, datalinks, fuzes, control sections, and mission-critical software.

Even when governments approve large procurements contract, delivery timelines can stretch extended as each missile lot must undergo strict safety, integration, and certification standards. As a result, missile manufacturers are investing heavily in factories, workforce, and supplier network capacity rather than focusing solely on launching new variants.

For instance, in April 2026, L3Harris closed a USD 1 billion Department of War investment in its Missile Solutions business to expand and modernize facilities, accelerate R&D, and increase production capacity for critical missile technologies.

MARKET OPPORTUNITY

Expansion of Advanced Fighter Aircraft Fleets and Missile Integration Programs to Fuel Market Growth

The clearest growth opportunity in the market lies in countries that are procurement or upgrading advanced fighter aircraft including F-35, Typhoon, Rafale, Gripen, F-16, F-15, KF-21. These countries increasingly need missile deeper missile inventories to ensure that their combat aircraft fleets remain operationally credible. The opportunity is especially strong in Europe, where governments are rebuilding air-defense and air-dominance capabilities after years of limited munition inventories. For OEMs, future growth will extend beyond from missile production alone and include integration kits, software updates, test equipment, captive training missiles, spares, and long-term sustainment. MBDA’s Meteor is well placed in this environment as it is already associated with Typhoon, Rafale, Gripen, KF-21, and F-35 integration pathways.

For instance, in January 2026, MBDA received a new German order for additional Meteor beyond-visual-range air-to-air missiles, following integration progress on F-35 Lightning II and confirmation by Brazil of a successful Meteor firing from Gripen E.

MARKET CHALLENGES

Difficulty in Detecting Targets to Hinder Market Growth

The market’s biggest technical challenge is that modern targets are becoming harder to detect, track, and kill. Fighters, UAVs, cruise missiles, and decoys are increasingly designed with low signatures, electronic attack, datalink disruption, and infrared/radar countermeasures. This is forcing OEMs to upgrade seekers, processors, ECCM logic, data links, and propulsion while keeping missiles compatible with existing launchers and aircraft software architectures. For Example, Rafael’s I-Derby ER, is positioned with a software-defined RF seeker, ECCM features, and two-way datalink for hostile EW environments, while Python-5 is marketed as a fifth-generation IIR missile with full-sphere capability and enhanced resistance to countermeasures.

For instance, in April 2025 Diehl Defence announced a partnership with MDSI to enhance IRIS-T integration into fighter launch platforms through a modular payload integration approach. The announcement is significant as it highlights a real industry challenge, integrating next-generation missile technologies into existing combat platforms without requiring extensive redesign or replacement of legacy systems.

SEGMENTATION ANALYSIS

By Missile Type

Very Long-Range Air-To-Air Missile Segment to Depict Fastest Growth, Driven by Rising Need To Engage Enemy Aircraft

By missile type, the market is divided into short-range air-to-air missile, medium-range air-to-air missile, beyond visual range missile, very long-range air-to-air missile, dual-role air-to-air/ surface-to-air missile, and training/captive missile.

The very long-range air-to-air missile is estimated to be the fastest-growing segment, registering a highest CAGR of 15.82% during the forecast period. Growth in this segment is driven by the increasing need to engage enemy aircraft, AWACS, tankers, and high-value airborne platforms from safer stand-off distances.

The beyond visual range missile segment accounted for the largest global air-to-air missiles market share of 41.90% in 2025 and the is expected to grow at a CAGR of 14.66% during the forecast period.

By Range Capacity

Above 300 Km Segment to Showcase Fastest Growth, Fueled by Growing Interest In Very Long-Range Air Combat Capabilities

By range capacity, the global market is divided into below 10 km, 10–30 km, 30–80 km, 80–160 km, 160–300 km, and above 300 km.

The above 300 km is estimated to be the fastest-growing segment, registering a highest CAGR of 16.05% during the forecast period. This growth reflects rising interest in very long-range air combat capabilities, especially for countering high-value airborne assets and keeping launch aircraft outside enemy engagement zones. Growth is being driven by next-generation air combat concepts in which aircraft are required to launch from safer distances and engage strategic airborne platforms before entering heavily defended zones. Moreover, future air combat operations increasingly rely on long-range kill chains, third-party targeting, and the engagement of enemy support aircraft beyond the reach of traditional fighter weapons.

The 80–160 km segment accounted for the largest global market share of 40.43% in 2025 and the is expected to grow at a CAGR of 13.89% during the forecast period.

By Guidance Technology

AI/Autonomy-Enabled Guidance Segment to Display Fastest Growth, Propelled by Rising Need for Electronic Warfare Resistance

By guidance technology, the global market is divided into infrared homing, active radar homing, semi-active radar homing, passive RF homing, dual-mode guidance, AI/autonomy-enabled guidance, command/datalink guidance, GPS/GNSS-aided guidance, and inertial guidance.

The AI/autonomy-enabled guidance is estimated to be the fastest-growing segment, registering the highest CAGR of 17.04% during the forecast period. Growth in this segment is driven by increasing demand for enhanced target discrimination, electronic warfare resistance, adaptive routing, and future air combat where missiles must operate in cluttered and contested environments. Future missiles systems will need better onboard decision-making, target prioritization, countermeasure resistance, and performance in GPS-denied and electronically contested battlespaces.

The active radar homing segment accounted for the largest global market share of 40.86% in 2025 and is expected to grow at a CAGR of 15.04% during the forecast period.

By Seeker Type

Multispectral Seeker Segment to Reflect the Fastest Growth due to Increasing Need To Counter Stealth Technology

By seeker type, the global market is divided into infrared seeker, radar seeker, electro-optical seeker, multispectral seeker, anti-jam seeker, lock-on mode, and seeker cooling.

The multispectral seeker is estimated to be the fastest-growing segment, holding a highest CAGR of 15.96% during the forecast period. Growth is driven by the increasing need to counter stealth technology, decoys, jamming, and infrared/radar countermeasures through the integration of multiple sensing modes within a single seeker architecture. In addition, air targets use stealth shaping, electronic warfare, decoys, and low-signature profiles that require missiles to combine radar, infrared, imaging, and signal-processing inputs for more reliable kills.

The radar seeker segment captured the largest market share of 41.34% in 2025 and is expected to grow at a CAGR of 14.67% during the forecast period.

By Propulsion System

Scramjet/Hypersonic Concept Segment to Lead due to Rising Interest In Next-Generation Missile Systems

By propulsion system, the market is divided into single-pulse solid rocket motor, dual-pulse solid rocket motor, boost-sustain rocket motor, ramjet propulsion, scramjet/hypersonic concept, thrust vector control, and low-smoke propulsion.

The scramjet/hypersonic concept is likely to be the fastest-growing segment, recording a highest CAGR of 17.72% during the forecast period. Growth is driven by rising interest in next-generation missile defense systems capable of achieving higher speed, longer engagement ranges, and better endgame energy retention. Although still at an emerging stage with a relatively smaller installed base, defense OEMs and militaries explore faster interceptors that reduce enemy reaction time and improve survivability against advanced air defenses and electronic countermeasures.

The single-pulse solid rocket motor segment accounted for the largest market share of 35.14% in 2025 and is expected to grow at a CAGR of 10.35% during the forecast period.

By Speed

High Hypersonic Segment to Dominate due to Growing Need to Reduce Enemy Reaction Time

By speed, the global market is divided into subsonic/training class, supersonic, high supersonic, hypersonic/near-hypersonic, high-G maneuver class, and energy-retention class.

The high supersonic is estimated to be the fastest-growing segment, registering a highest CAGR of 16.36% during the forecast period. Growth is being pushed by the growing need to reduce enemy reaction time, improve survivability against countermeasures, and support next-generation air dominance missions. The future air combat will demand missiles that can close distance faster, defeat evasive targets, and compress the enemy’s decision-making window.

The supersonic segment held the largest market share of 40.62% in 2025 and is likely to grow at a CAGR of 14.28% during the forecast period.

By Airframe

Low-Observable Compatible Missile Segment to Dominate due to Future Stealth Aircraft Requirements

By airframe, the global market is divided into conventional tail-control missile, canard-control missile, thrust-vectoring missile, strake/lifting-body missile, folding-fin missile, and low-observable compatible missile.

The low-observable compatible missile is poised to be the fastest-growing segment, registering a highest CAGR of 16.52% during the forecast period. Its growth is tied to F-35 and future stealth aircraft requirements, where missiles must fit within internal weapon bays, reduce radar signature, and preserve aircraft survivability. Fifth-generation fighter aircrafts increasingly need missiles that can fit internal weapons bays, maintain stealth profiles, and still deliver long-range engagement performance.

The conventional tail-control missile segment accounted for the largest global market share of 34.23% in 2025 and is expected to grow at a CAGR of 10.58% during the forecast period.

By Component

Air-Breathing Inlet Segment to Lead owing to Ramjet and Scramjet-Powered Missile Concepts

By component, the global market is divided into motor casing, nozzle system, thrust vector control, ignition, thermal protection, propellant grain, air-breathing inlet, combustion system, and fuel system.

The air-breathing inlet is poised to be the fastest-growing segment, registering the highest CAGR of 19.51% during the forecast period. Rapid growth in this segment is driven by ramjet and scramjet-powered missile concepts, where air-breathing propulsion systems enable longer operational range, sustained high-speed performance, and stronger endgame energy retention. In addition, ramjet and future air-breathing propulsion systems require more complex inlet structures to manage airflow, sustain thrust, and improve endgame energy retention over longer distances.

The propellant grain segment led the market, holding a highest share of 33.28% in 2025 and is expected to grow at a CAGR of 13.27% during forecast period.

By Procurement Type

To know how our report can help streamline your business, Speak to Analyst

Development Programs Segment to Lead, Driven by Rising Governments And OEMs Investments

By procurement type, the global market is divided into new missile production, replacement stockpile, development programs, export programs, and joint ventures.

The development programs is estimated to be the fastest-growing segment, registering a highest CAGR of 14.74% during the forecast period. Growth is being driven by next-generation BVR missiles, AI-enabled guidance, hypersonic concepts, improved seekers, and missiles designed for contested electronic warfare environments. Moreover, governments and OEMs are investing in long-range BVR missiles, hypersonic concepts, AI-enabled guidance, multispectral seekers, and low-observable compatible designs to support future air combat requirements.

The new missile production segment secured the largest market share of 34.18% in 2025 and is expected to grow at a CAGR of 13.75% during the forecast period.

Air-to-Air Missiles Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Air-to-Air Missiles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 2.38 billion, and also maintains its leading share in 2026, with USD 2.77 billion. Regional air-to-air missiles market growth is driven by rising geopolitical tensions, rapid modernization of fighter fleets, and increasing demand for advanced missile beyond-visual-range (BVR) capabilities. High defense budgets, investments in hypersonic technology, and the need to counter unmanned aerial threats are further fueling market expansion.

U.S. Air-to-Air Missiles Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 2.28 billion in 2025 and is estimated to grow at a CAGR of 12.80% during the forecast period.

Europe

Europe is projected to register the fastest regional growth, expanding at a CAGR of 15.21% during the forecast period. In 2025, the market value stood at USD 1.46 billion, driven by heightened geopolitical tensions, surging defense spend, and the need to modernize air combat capabilities against advanced aerial threats. Key growth reasons include increasing stockpiles of Beyond-Visual-Range (BVR) missiles, significant investments in R&D, and increasing integration of AI and stealth technologies into next-generation air combat platforms.

U.K. Air-to-Air Missiles Market

The U.K.’s market was valued at USD 0.22 billion in 2025 and is estimated to grow at a CAGR of 13.22% during the forecast period.

Nordic Countries Air-to-Air Missiles Market

The market was valued at USD 0.26 billion in 2025 and is estimated to grow at a rate of 17.36% during the forecast period.

Germany Air-to-Air Missiles Market

The market was valued at USD 0.24 billion in 2025 and is estimated to grow at a rate of 16.54% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 2.03 billion in 2025, securing the position of the second-largest region in the market. The market is projected to grow rapidly, driven by intense regional geopolitical tensions (South China Sea, Taiwan Strait, and Korean Peninsula), rising defense budgets, and modernization efforts. Key growth reasons include increasing territorial disputes prompting procurement of advanced missiles, significant investments in indigenous development (e.g., India's Astra Mk-II, South Korea's KF-21 integration), and the need to counter advanced threats such as hypersonic weapons.

China Air-to-Air Missiles Market

The Chinese market was valued at USD 0.56 billion in 2025 and is estimated to grow at a rate of 12.74% during the forecast period.

India Air-to-Air Missiles Market

The Indian market was valued at USD 0.34 billion in 2025 and is estimated to grow at a rate of 16.27% during the forecast period.

Japan Air-to-Air Missiles Market

The Japanese market in 2025 was valued at USD 0.45 billion and is estimated to grow at a rate of 15.53% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market was valued at USD 0.12 billion in 2025, while the Middle East & Africa market reached USD 0.81 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players are Investing in Automated Factories to Gain Competitive Edge

The air-to-air missiles market is becoming more competitive as governments prioritize larger stockpiles, faster delivery timelines, and interoperability across multiple fighter aircraft platforms. OEMs are responding by expanding production capacity, securing rocket-motor supply, and investing in automated factories and test infrastructure.

Technology competition is moving toward longer-range BVR engagement, improved no-escape zones, software-defined seekers, two-way datalinks, ECCM, and easier aircraft integration. Overall, the industry is growing through munition replenishment programs, fighter aircraft modernization initiatives, multinational integration programs, and technology upgrades aimed at improving survivability in contested airspace environments.

LIST OF KEY AIR-TO-AIR MISSILES COMPANIES PROFILED

- RTX Corporation (U.S.)

- Nammo AS (Norway)

- MBDA Group (France)

- Diehl Defence GmbH & Co. KG (Germany)

- Saab AB (Sweden)

- Roxel Group (U.K.)

- Thales S.A. (France)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Bharat Dynamics Limited (India)

- TÜBİTAK SAGE (Turkey)

- Denel Dynamics (South Africa)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Aviation Industry Corporation of China, Ltd. (China)

- JSC GosMKB Vympel (Russia)

- Artem State Joint Stock Holding Company (Ukraine)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Raytheon received a USD 760.00 million U.S. contract to support AMRAAM production, sustainment, development, and obsolescence mitigation for multiple U.S. and allied FMS customers. The contract shows that AMRAAM demand is moving beyond fresh missile orders into long-term lifecycle support and electronics refresh work.

- September 2025: Raytheon received a USD 41.68 million contract modification covering AMRAAM variants, production, and sustainment activities, bringing the cumulative value of the related contract to more than USD 2.51 billion. The customer base included several NATO and allied air forces, showing continued reliance on AMRAAM as the standard BVR missile across Western fighter fleets.

- September 2025: The U.S. State Department approved a possible USD 570.00 million FMS package to the Netherlands for AIM-120C-8 AMRAAM missiles and related equipment, reflecting growing European demand for beyond-visual-range missile depth as NATO countries strengthen air-defense and air-superiority readiness.

- September 2025: The U.S. State Department approved a possible USD 567.80 million FMS package to Belgium for AIM-9X Sidewinder missiles and related equipment. This supports Belgium’s short-range air-combat capability and strengthens NATO fighter interoperability, especially as European air forces modernize around fifth-generation and upgraded fourth-generation aircraft.

- July 2025: Raytheon was awarded a contract valued at up to USD 3.50 billion for AMRAAM Production Lots 39 and 40.

REPORT COVERAGE

The global air-to-air missiles market report analysis provides a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends that are expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key defense industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.53% from 2026-2034 |

| Unit | USD Billion |

|

Segmentation |

By Missile Type

By Range Capacity

By Guidance Technology

By Seeker Type

By Propulsion System

By Speed

By Airframe

By Component

By Procurement Type

By Geographic

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.83 billion in 2025 and is projected to reach USD 22.03 billion by 2034.

In 2025, the European market value stood at USD 1.46 billion.

The market is expected to exhibit a CAGR of 13.53% during the forecast period.

The scramjet/hypersonic concept segment is expected to hold the highest CAGR over the forecast period.

Rise in defense expenditure is the key factor driving the market.

RTX/Raytheon, MBDA, Diehl Defence, Rafael Advanced Defense Systems, and Lockheed Martin Corporation are the top key players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us