Aircraft Ejection Seat Market Size, Share & Industry Analysis by Aircraft Type (Fighter Jet, Bomber Aircraft, Trainer Aircraft, Turboprop Trainer, Electronic Warfare Aircraft, Reconnaissance Aircraft, Special Mission Aircraft, VTOL Aircraft, Helicopter, and Others), By Seat Type (Zero-Zero Rocket-Propelled Seat, Rocket-Assisted Ejection Seat, Catapult Only Seats, and Encapsulated Seats), By Fitment (OEM, MRO, and Others), By Seat Arrangement (Single Seat and Twin Seat), By End User (Airforce, Naval, and Others), and Regional Forecast, 2026-2034

Aircraft Ejection Seat Market Size and Future Outlook

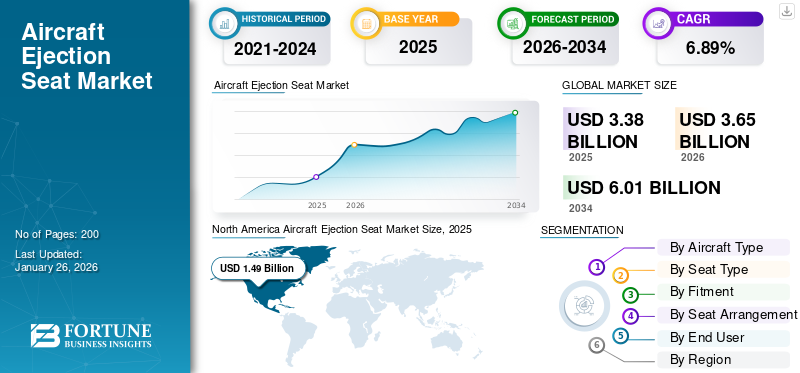

The global aircraft ejection seat market size was valued at USD 3.38 billion in 2025 and is projected to grow from USD 3.65 billion in 2026 to USD 6.01 billion by 2034, exhibiting a CAGR of 6.89% during the forecast period. North America dominated the aircraft ejection seat market with a market share of 44.05% in 2025.

The market revolves around the development and production of emergency escape systems that ensure pilot safety during critical flight situations. These seats are engineered to eject the pilot from an aircraft within seconds, using rocket motors or explosive cartridges, followed by automatic parachute deployment. They are essential components in military fighter jets, trainer aircraft, and some advanced civil aviation prototypes. The market features various seat types, including single-seat and twin-seat configurations, designed according to aircraft structure and mission requirements. Key components typically include rocket motors, ejection handles, seat harnesses, survival packs, and parachute systems. Rising defense spending, modernization of fighter fleets, and a growing emphasis on pilot survivability continue to drive market growth.

Prominent players such as Martin-Baker Aircraft Co. Ltd., Collins Aerospace, and NPP Zvezda dominate the industry with innovations focused on enhanced reliability, lightweight materials, and next-generation smart ejection technologies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Focus on Pilot Safety and Fleet Modernization to Drive Market Expansion

The market is witnessing significant growth due to the increasing emphasis on pilot safety and modernization of defense fleets worldwide. Advanced fighter jet programs such as the F-35 Lightning II, Rafale, and India’s Tejas are fueling the demand for reliable, high-performance ejection seat systems. Governments are prioritizing safety in high-risk missions, leading to investments in ejection technologies that can operate effectively at both high and low altitudes, propelling aircraft ejection seat market growth. Innovations such as smart sensors and lighter composite materials further enhance safety, reliability, and ease of integration solidifying ejection seats as a crucial element of next-generation combat aircraft.

MARKET RESTRAINTS

High Development Cost and Complex Integration May Hinder Wider Adoption

Despite strong demand, the market faces limitations due to high development and customization costs. Each ejection system must be tailored to specific aircraft models, demanding extensive engineering, testing, and certification processes. This customization inflates costs and extends project timelines, making adoption challenging for smaller air forces. Additionally, ongoing maintenance and the replacement of pyrotechnic components require specialized expertise and regulatory compliance. The lack of large-scale commercial applications also restricts market expansion, leaving growth largely dependent on military procurement cycles and defense budgets especially in regions with limited financial resources.

MARKET OPPORTUNITIES:

Emerging Defense Programs and Retrofits to Create Lucrative Growth Opportunities

Expanding defense modernization initiatives in Asia Pacific, the Middle East, and Eastern Europe are opening new avenues for market players. Nations such as South Korea, the UAE, and Poland are launching indigenous fighter jet programs, driving the demand for locally manufactured ejection systems. Retrofitting existing aircraft with advanced ejection seats also presents a promising revenue stream, particularly for aging fleets. Lightweight materials such as carbon-fiber composites and advanced propulsion technologies are enabling performance upgrades. Collaborations between global leaders such as Martin-Baker and Collins Aerospace with regional defense agencies are fostering ejection seat technology transfer, boosting innovation and regional self-reliance in safety systems.

AIRCRAFT EJECTION SEAT MARKET TRENDS:

Shift toward Smart, Lightweight, and Modular Ejection Seat Technologies

The latest trend in the market is the adoption of smart and adaptive technologies that automatically adjust ejection force and timing. Advanced models are incorporating digital sensors, electronic monitoring, and modular designs for easier maintenance and upgrades. Manufacturers are increasingly using lightweight materials such as titanium and carbon composites to enhance performance without compromising safety. Additionally, partnerships between aircraft ejection seat suppliers and aircraft OEMs are expanding, particularly for next-generation jets such as the F-35 and India’s AMCA. This evolution toward intelligent, weight-optimized, and customizable systems reflects the market’s move toward greater safety and operational efficiency.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Technical Reliability and Certification Challenges to Slow Market Advancement

The aircraft ejection seat industry faces ongoing challenges in ensuring reliability under extreme flight conditions while keeping systems lightweight and compact. Integrating modern ejection seats into legacy platforms often requires structural redesigns, which can delay deployment and raise costs. Moreover, the limited pool of specialized suppliers can create supply chain delays during large-scale defense contracts. Stringent military certification standards add another layer of complexity, lengthening time-to-market for new products. Ensuring pilot safety in zero-altitude or supersonic ejections remains a demanding engineering task posing both technical and regulatory hurdles that manufacturers must overcome to remain competitive.

U.S. Tariff Impact

The imposition of U.S. tariffs on imported aerospace components and raw materials has added notable cost pressures to the aircraft ejection seat industry. Many critical parts, including metals, electronics, and pyrotechnic materials, are sourced globally, making manufacturers vulnerable to price fluctuations and supply delays. These tariffs have particularly impacted companies relying on cross-border partnerships or subcontracted component production. Increased production costs can lead to higher prices for defense procurement programs or delayed deliveries. Additionally, prolonged trade tensions may discourage international collaboration, forcing firms to localize manufacturing, raising short-term expenses but potentially strengthening domestic supply chains long-term.

Segmentation Analysis

By Aircraft Type

Sustained Fighter Deliveries and Upgrade Cycles to Propel Fighter Jet Segment Growth

On the basis of segmentation by aircraft type, the market is classified into fighter jet, bomber aircraft, trainer aircraft, turboprop trainer, electronic warfare aircraft, reconnaissance aircraft, special mission aircraft, VTOL aircraft, helicopter, and others.

The fighter jet segment is anticipated to hold a dominant market share of 6.46% in 2026. The segment growth is driven by ongoing new-build fighter deliveries, mid-life upgrade programs, and high sortie rates that keep CAD/PAD changes, inspections, and depot work consistently funded.

The electronic warfare aircraft segment is expected to grow at the highest CAGR of 7.80% over the forecast period.

By Seat Type

Full-Envelope Safety Mandates to Impel Zero-Zero Rocket-Propelled Seats Segment Growth

In terms of seat type, the market is categorized into zero-zero rocket-propelled seat, rocket-assisted ejection seat, catapult only seats, and encapsulated seats.

The zero-zero rocket-propelled seat segment is anticipated to hold a dominant market share of 14.25% in 2026. In 2025, the segment is anticipated to dominate with 7.21% share. The segment growth is driven by required low-altitude/low-speed protection, wider pilot-fit standards, and the replacement of legacy seats with modern full-envelope designs.

The rocket-assisted ejection seat segment is expected to grow at a CAGR of 6.71% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Fitment

New-Aircraft Programs and Localization Offsets to Drive OEM Segment Growth

Based on fitment, the market is segmented into OEM, MRO, and others.

The OEM segment is anticipated to hold a dominant market share of 17.43% in 2026. The segment growth is driven by active production lines that pull complete seat kits plus integration/qualification work, reinforced by local assembly and offset commitments.

The MRO segment is set to flourish and grow at a CAGR of 7.44% over the forecast period.

By Seat Arrangement

Operational Fleet Mix to Drive Single-Seat Segment Growth

Based on seat arrangement, the aircraft ejection seat market is segmented into single seat and twin seat.

The single seat type segment is projected to dominate the market with a share of 14.78% in 2026. The segment growth is driven by the prevalence of single-seat frontline fighters and steady sustainment per cockpit sequencers, restraints, parachute repacks, and life-limited parts.

The twin seat segment is set to flourish at a growth rate of 6.61% during the forecast period.

By End User

Readiness Targets and Fleet Scale to Drive Air Force Segment Growth

Based on end-user, the market is segmented into airforce, naval, and others.

The airforce segment held a dominating position in 2024. The segment growth is driven by large, highly utilized fleets with strict availability and safety mandates that translate into predictable line-fit, retrofit, and recurring sustainment spend.

The naval segment is set to flourish with a growth rate of 6.44% over the forecast period.

Aircraft Ejection Seat Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America recorded a market size of USD 1.49 billion in 2025, capturing 44.05% of the global market share, and is projected to reach USD 1.61 billion in 2026. North America remains the largest and most technologically advanced ejection-seat market. The U.S. anchors it with deep OEM benches, NASA and DoD test ranges, and a mature depot ecosystem that feeds continuous line-fit and sustainment work. In 2026, the U.S. market is estimated to reach USD 1.11 billion.

North America Aircraft Ejection Seat Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

Other regions such as Europe and Asia Pacific are anticipated to witness notable growth in the coming years. During the forecast period, the Asia Pacific region is projected to record the growth rate of 7.61%, which is the highest amongst all the regions. In 2025, Europe represented USD 0.75 billion, accounting for 22.24% of the worldwide market, and is projected to grow to USD 0.81 billion in 2026. In the region, U.K. and Germany are estimated to reach USD 0.29 billion and 0.21 billion respectively in 2026.

Asia Pacific

Asia Pacific leads in early commercialization, driven by new fighter and trainer lines, indigenous programs, and localization and offset assembly of aircrafts. Backed by these factors, countries including China, Japan, and India are anticipated to record the valuation of USD 0.24 billion, USD 0.12 billion, and USD 0.18 billion respectively in 2026. The Asia Pacific market generated USD 0.63 billion in 2025, representing 18.67% of the global market landscape, and is expected to reach USD 0.69 billion in 2026.

Middle East & Africa and Latin America

Over the forecast period, the Middle East and Africa and Latin America regions would witness moderate growth. The Middle East market, in 2025, is set to record USD 0.35 billion as its valuation. Latin America is set to attain the value of USD 0.16 billion 2025.

Rest of the World

The market in Rest of the World reached USD 0.51 billion in 2025, representing 15.04% of total market revenue, and is projected to reach USD 0 billion in 2026.

COMPETITIVE LANDSCAPE

Extensive R&D and Partnership among Key Players to Define Competitive Landscape

The global market is moderately consolidated, led by life-critical OEMs that pair in-house expertise with joint testing. Core aircraft ejection seat players Martin-Baker, Collins Aerospace (ACES), NPP Zvezda, and AVIC anchor platform supply, supported by specialist tiers such as PacSci EMC and Chemring (CAD/PAD) and Airborne Systems (parachutes). Defense agencies and labs including USAF/NASA, UK MoD, DGA, DRDO, and JAXA contribute range time and co-development. Competition centers on proven zero-zero performance, neck-load mitigation, broad pilot accommodation, digital sequencers, and fast retrofit execution. Offsets, licensed assembly, and robust MRO networks sustain access, while automation and data-driven inspections cut turnaround and cost.

LIST OF KEY AIRCRAFT EJECTION SEATS COMPANIES PROFILED:

- Martin-Baker Aircraft Company (U.K.)

- Collins Aerospace (U.S.)

- NPP Zvezda (Russia)

- AVIC (Aviation Industry Corporation of China) (China)

- PacSci EMC (U.S.)

- Ensign-Bickford Aerospace & Defense (EBAD) (U.S.)

- Chemring Group (U.K.)

- Airborne Systems (U.S.)

- Survival Equipment Services (SES) (U.K.)

- Parker Meggitt (U.K.)

- RUAG MRO International (Switzerland)

- Eaton Mission Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- February 2025: Boeing Defense awarded Collins Aerospace a contract to supply 144 ACES II ejection seats for the F-15EX fleet of the U.S. Air Force.

- December 2024: The Next-Generation Ejection Seat (NGES) program is being updated by the U.S. Air Force to invite more market players to bid for a supply contract comprising F-16 ejection seats, with the possibility of future competition for other aircraft platforms. This will increase competition for some of the five platforms.

- September 2024: WZL2 and Martin Baker Aircraft Company signed a Memorandum of Understanding to provide operational support for Martin Baker's ejection seats aboard Polish Air Force aircraft. The purpose of the Memorandum of Understanding is to forge a long-term strategic partnership in the area of Martin Baker's ejection seat maintenance, repair, and overhaul services for Polish Air Force aircraft.

- August 2024: Martin-Baker Australia has been chosen by Lockheed Martin Australia to provide aircraft ejection seat training, guaranteeing that pilots in the Australian Defence Force possess essential emergency response abilities while flying.

- April 2023: Lockheed Martin and BAE Systems received a new maintenance and support contract by the U.K. for its fleet of F-35 Lightning stealth jets. BAE Systems was assigned to provide groundcrew training, technical support, and a variety of vital services, including ejection seat and canopy maintenance.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.89% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Aircraft Type

By Seat Type

By Fitment

By Seat Arrangement

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.65 billion in 2026 and is projected to reach USD 6.01 billion by 2034.

In 2025, the North America market value stood at USD 1.49 billion.

The market is expected to exhibit a CAGR of 6.89% during the forecast period of 2026-2034.

The fighter jet segment led the market by aircraft type in 2025.

The rising focus on pilot safety and fleet modernization is a key factor driving market expansion.

Martin-Baker Aircraft Company, Collins Aerospace, NPP Zvezda, AVIC (Aviation Industry Corporation of China), and PacSci EMC are some of the prominent players in the market.

North America dominated the aircraft ejection seat market with a market share of 44.05% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us