Aircraft Hydraulic Systems Market Size, Share & Industry Analysis, By Components (Hydraulic Fluid, Reservoir, Pump, Actuator (Motor), Valves, & Others), By Type (Closed-Center & Open-Center), By Solution (Line Fit & Retrofit), By Application (Flight Controls, Landing Gear, Brakes, Thrust Reversers & Other Systems), By Platform (Fixed Wing, Rotary Wing, & Unmanned Aerial Vehicles (UAVs)), By Fixed Wing (Narrow Body, Wide Body, Regional Jet, Military Aircrafts, Business Jet & General Aviation Aircraft) By Rotary Wing (Commercial Helicopters & Military Helicopters), & Regional Forecast, 2026-2034

Aircraft Hydraulic Systems Market Size and Future Outlook

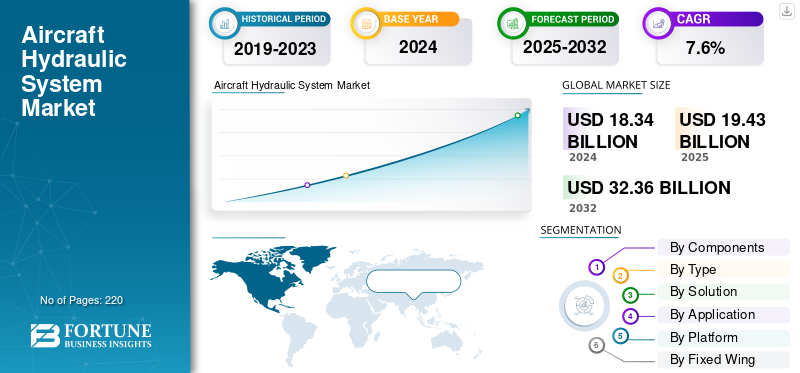

The global aircraft hydraulic systems market size was valued at USD 19.43 billion in 2025. The market is projected to grow from USD 20.14 billion in 2026 to USD 37.09 billion by 2034, exhibiting a CAGR of 7.90% during the forecast period. North America dominated the aircraft hydraulic systems market with a market share of 36.90% in 2025.

Aircraft hydraulic systems are mission-critical power delivery networks that employ pressurized hydraulic fluid to power critical aircraft components. They transfer mechanical power from engines to hydraulic power, allowing sensitive control over heavy aircraft components that would otherwise demand gigantic physical power. Hydraulic systems work according to Pascal's Law principle, where enclosed fluid systems have equal pressure on all sides, thus delivering efficient power with little friction loss.

Hydraulic systems of aircraft drive several flight-critical functions in both commercial and military aviation. Commercial aircraft such as the Boeing 787 have three separate hydraulic systems at 5,000 psi, whereas the Airbus A350 makes use of a low-complexity "2Hydraulic2Electric" (2H2E) architecture with two hydraulic circuits and low maintenance.

International air passenger traffic is expected to expand by 4.1% a year between now and two decades, fueling record aircraft orders. The International Air Transport Association predicts the commercial fleet will top 46,000 aircraft by 2035 aids the demand for new hydraulic systems anticipate the global market growth.

Furthermore, the market encompasses several major market players with a broad portfolio with innovative products, and strong regional presence expansion have supported the dominance of these companies in the market. Major players are such as Parker Hannifin Corporation, RTX Corporation, Safran S.A., Eaton Corporation, Honeywell International, and so on.

Download Free sample to learn more about this report.

Aircraft Hydraulic Systems Market KEY TAKEAWAYS

- 2025 Market Size: USD 19.43 billion

- 2026 Market Size: USD 20.14 billion

- 2034 Forecast Market Size: USD 37.09 billion

- CAGR: 7.90% from 2026–2034

- North America dominated the aircraft hydraulic systems market with a 36.90% share in 2025.

- The actuator (motor) segment is projected to account for the largest market share of 51.20% in 2026.

- The closed-center segment is projected to hold the largest market share of 93.07% in 2026.

North America

North America held a 36.92% market share in 2025, valued at USD 7.17 billion, and is projected to reach USD 7.38 billion in 2026.

Asia Pacific accounted for 35.16% of the global market in 2025, valued at USD 6.83 billion, and is estimated to reach USD 7.12 billion in 2026.

Europe

Europe represented 13.66% of the global market in 2025, valued at USD 2.65 billion, and is projected to reach USD 2.79 billion in 2026.

U.S.

U.S. The market is projected to reach USD 5.84 billion by 2026.

Japan

Japan The market is projected to reach USD 0.83 billion by 2026.

Read More

MARKET DYNAMICS

Market Driver

Growing Commercial Aviation Sector and Increasing Fleet Modernization Programs by Emerging Countries Drives Market Growth

The aerospace market witnesses record growth momentum due to worldwide passenger traffic growth and commercial fleet modernization efforts. According to International Air Transport Association estimates, the demand for air travel is expected to grow by more than 40 percent until 2030, with an estimated 43,600 new aircraft deliveries until 2044. This high demand for advanced hydraulic systems enables the continued pressure for sophisticated hydraulic systems to support larger commercial aircraft such as narrow-body and wide-body platforms.

Advanced aircraft such as the Boeing 787 and Airbus A350 need complex hydraulic architectures with high operating pressures of 5,000 psi, well beyond traditional system design specifications. Airlines prefer fuel-efficient platforms with light hydraulic components that provide improved power-to-weight performance with minimal compromise on operation reliability levels. Replacement cycles for older fleets also drive higher hydraulic system demand, as operators require upgraded systems to meet higher performance capability needs and regulatory requirements.

- For instance, in July 2025, Boeing reported production volumes up to 52 aircraft deliveries, adding to combined Boeing-Airbus monthly production of 126 aircraft. This production rebound reflects industry strength in supporting hydraulic system demand growth as manufacturers rebuild pre-pandemic production levels.

Market Restraints

Chances of Hydraulic Fuel Leakage and High Maintenance Cost Hamper Market Growth

Aircraft Hydraulic Systems encounter recurring operational issues of fluid leakage, which causes high maintenance costs and reliability issues. Market research shows that hydraulic fluid leak is the leading cause of system failure, contributing to 80-90 percent of incidents related to hydraulic issues.

Airlines are faced with heavy financial costs in terms of inspection schedules, component overhaul processes, and regulatory compliance processes justified by the contamination of hydraulic fluids. The fire hazard of traditional hydraulic fluids poses safety risks in hot aviation environments, necessitating the use of specialized fire protection systems that add weight and complexity to aircraft.

Maintenance activities incur prolonged turnaround times to deal with hydraulic system repairs, most notably engine-driven pump failure and actuator replacement. Local operators are disproportionately affected by the cost of hydraulic maintenance as they lack specialized technical skills and component supply, which limits operating flexibility. Hydraulic fluid spillage risks of environmental contamination add compliance weight, as the operator must introduce specialized containment and disposal processes in compliance with rigorous aviation environmental regulations.

Market Opportunities

Ongoing Adoption of More-Electric Aircraft Integration and Hybrid System Development Catalyze Growth Opportunity

The aviation industry shift toward electric aircraft architectures is opening up enormous opportunities for new-generation hydraulic system integration. Industry players can leverage hybrid electro-hydraulic solutions by meshing legacy hydraulic reliability with electric system efficiency. Power-hydraulic power generation in localized form using motor-pump packages has greater benefits compared to centralized hydraulic distribution systems as it minimizes weight, complexity, and maintenance needs.

Power-on-demand hydraulic systems facilitate energy savings through the activation of hydraulic power only when needed for particular operations, allowing for aircraft fuel efficiency goals. New materials such as composites and high-strength alloys make lightweight designs of hydraulic components possible while preserving performance and lowering the weight of the aircraft.

Electro-hydraulic actuator technologies open the door for integrated solution development by manufacturers across both traditional and higher-electric aircraft platforms. These technologies provide higher power density than purely electric solutions yet offer fine control functionality needed for flight-critical applications. Modular hydraulic system architecture allows for flexible configuration designs accommodating a wide range of aircraft requirements from regional jets to wide-body commercial and military aircraft.

This move toward distributed actuation systems offers possibilities for tailored hydraulic solutions for certain aircraft zones over centralized distribution networks. Investment in research and development in smart hydraulic technologies with digital control and monitoring features prepares manufacturers to respond to changing industry needs.

- For instance, in March 2025, ZeroAvia has announced that it has been chosen by AFWERX to receive a Small Business Innovation Research (SBIR) grant to pursue a feasibility study to embed hydrogen propulsion into Cessna Caravan aircraft in conjunction with next-generation aircraft automation technology.

Aircraft Hydraulic Systems Market Trends

Increasing Integration of Advanced Materials and Lightweight Component to Enhance Performance Accelerate Market Trends

The aircraft hydraulic systems market trend illustrates growing use of advanced materials formulated to provide improved performance while minimizing component weight. Industry manufacturers use high-strength titanium alloys and composite materials more and more to build hydraulic components for better strength-to-weight ratios. Uses of carbon fiber reinforced polymers in hydraulic reservoirs and housing components provide substantial weight savings over conventional aluminum construction without loss of structure integrity.

Additive manufacturing processes allow for the production of intricate hydraulic components with cooling channels and optimized internal geometries that enhance efficiency while minimizing assembly needs. Surface treatment processes such as advanced coatings and plating processes improve corrosion resistance and prolong component life in extreme aviation environments.

Nano-material incorporation into hydraulic seals and gaskets yields improved temperature resistance and decreased leakage rates, taking care of major maintenance issues. Smart materials with shape-memory alloy components present potential for self-altering hydraulic components that adapt to optimize performance under changing operating conditions.

Lightweight hydraulic pumps using innovative bearing technologies and optimized impeller shapes provide enhanced efficiency with lower power consumption demands. Bio-based hydraulic fluids using renewable resources promote environmental sustainability goals while preserving performance. Sensor technologies integrated into hydraulic components provide real-time performance monitoring without excess weight penalties.

- For instance, in June 2023, Boom Supersonic revealed significant progress on Overture, its eco-friendly supersonic airplane, including important developments regarding the Symphony engine. The diagrams provided illustrate essential systems within Overture, such as avionics, flight controls, hydraulics, fuel systems, and landing gear, all created for maximum performance, efficiency, and safety. The hydraulic systems are designed with triple redundancy to ensure dependable power for flight controls and mechanical systems, and Overture's landing gear is suitable for international airport runways and taxiways, allowing takeoff and landing across more than 600 routes globally.

Market Challenges

Growing Environmental Regulations and Sustainability Compliance May Hinder Market Growth

Aircraft hydraulic systems are under growing regulatory scrutiny in terms of environmental concern and sustainability requirements. Conventional petroleum-based hydraulic fluids present serious environmental risks through soil contamination, groundwater pollution, and marine ecosystem harm in the event of a leakage or incorrect disposal.

The regulatory bodies adopt stringent standards for biodegradable hydraulic fluids that need to prove full environmental compatibility with sustained standards of performance. Swedish Standard SS 15 54 34 prescribes extensive environmental requirements which demand high degrees of biodegradability, low aquatic toxicity, and low content of carcinogenic substances from hydraulic fluids. Aviation operators incur significant compliance expense when replacing conventional hydraulic fluids with environmentally acceptable hydraulic fluids from system compatibility testing and certification demands.

Global environmental regulations increasingly limit the use of synthetic hydraulic fluids with toxic additives, compelling manufacturers to formulate alternative products that uphold performance standards. Regulations on waste disposal add to the operating pressures as operators are required to adopt specialized protocols for collecting, treating, and environmentally friendly disposal of hydraulic fluid can hinder the market growth.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Components

Growing Superior Power Density and Technological Advancement Drive Segment Dominance

The global market is segmented by components into the hydraulic fluid, reservoir, pump, actuator (motor), valves, and others.

The actuator (motor) segment will accounting for the largest market share in 2026 with a share of 51.20%. In addition, the segment is also estimated to be the fastest growing segment during the forecast period with the highest CAGR of 8.4%. Aircraft actuators produce more than 100,000 pounds of force and preserve compact sizes necessary for space-restricted aerospace uses; abilities not witnessed with other actuation technologies. The segment receives ongoing development in technology, specifically creation of electro-hydraulic actuators (EHA) and electro-hydrostatic actuators that offer hydraulic power density coupled with electronic control accuracy. These next-generation actuator systems dispense with centralized hydraulic systems but preserve high-force output levels, responding to industry needs for weight savings and more efficient energy use in more-electric aircraft designs drives the segmental growth.

- For instance, in January 2023 its win to provide electrohydraulic actuators for COMAC C919, China's indigenously built first large commercial passenger airplane, evidencing the growing international market for sophisticated actuator technologies.

- The hydraulic fluid segment is estimated to be the second fastest growing segment with a CAGR of 8.0% during the forecast period. Fluid chemistry technologies and strict environmental regulations to transform the industry toward greener alternatives. New-generation aircraft hydraulic fluids are required to meet ever more stringent performance demands such as improved thermal stability, lower flammability properties, better anti-wear capabilities, and longer service life intervals without having to be compatible with legacy aircraft systems to anticipate the segmental growth.

- For instance, in 2024, the European Clean Sky 2 program reached Technical Readiness Level 5 for efficient electrical environmental control systems minimizing engine bleed air dependency in favor of industry-wide efforts toward more sustainable hydraulic fluid use and environmental compliance.

To know how our report can help streamline your business, Speak to Analyst

By Type

Variable Displacement Pump Integration Enables Superior Performance Drives Segmental Growth

The market by type is classified into closed-center and open-center.

The closed-center segment will accounting for the largest market share in 2026 with a share of 93.07%. In addition, the segment is also estimated to be the fastest growing segment during the forecast period with the highest CAGR of 7.9%. Closed-center hydraulic systems gain market leadership with integration of variable displacement piston pumps that offer pressure-compensated operation, automatically compensating fluid delivery to meet system demand while keeping pressure availability constant. These pumps have incorporated swashplate mechanisms that change displacement from zero to maximum output depending on system pressure feedback, allowing energy-efficient performance to minimize heat generation and prolong component service life.

- For instance, in September 2025, Embraer has officially contracted with Panama to acquire four A-29 Super Tucano aircraft, which will be utilized by the Panamanian National Air and Naval Service (SENAN) as a new asset for surveillance and security.

The open-center segment expansion is focused in general aviation, regional aircraft, and niche helicopter applications where ease of operation and cost-effectiveness are more important than requirements for rapid response. These systems exhibit particular robustness in light aircraft applications such as business jets, regional turboprops, and military trainer aircraft that appreciate simplified hydraulic designs with lower component complexity.

By Solution

Fleet Modernization Programs and Periodic Maintenance of Current Fleet Creates Sustained Aftermarket Demand and Segment Growth

The market by solution is further segmented into line fit and retrofit.

The retrofit segment will accounting for the largest market share in 2026 with a share of 60.40%. In addition, the segment is also estimated to be the fastest growing segment during the forecast period of 2025-2032 with the highest CAGR of 8.0%. The expansion is fueled by widespread fleet modernization initiatives and mandated regulatory compliance updates in commercial and military aviation. International commercial aircraft fleet age averages around 11.2 years, with airlines embarking on retrofit programs to maximize aircraft service life while enhancing operational efficiency and regulatory compliance. Some of the prominent retrofit programs include hydraulic system upgrades for greater reliability, hydraulic fluid conversion to synthetic hydraulic fluids for environmental compliance, and additions of digital monitoring systems for predictive maintenance capabilities.

- For instance, in June 2023, Lufthansa Technik revealed extensive digital retrofit programs for traditional aircraft hydraulic systems that include IoT sensor integration and predictive analytics features that save 25% on maintenance costs while enhancing system reliability.

The line fit segment is aided by original equipment manufacturer partnerships which create long-term supply contracts covering entire aircraft production life cycles, generally 15-20 years for commercial aircraft. Airlines increasingly seek more fuel-efficient aircraft featuring modern aircraft hydraulic technologies that save on operating expenses by providing better system efficiency and less maintenance needs. Regional aircraft manufacturers such as Embraer, ATR, and Bombardier generate additional line fit demand through business jets, regional airliners, and specialized aircraft production programs that need certified integration of hydraulic systems.

By Application

Critical Role of Flight Control System in Aircraft Maneuverability Drives Largest Market Share

The market by application is further divided into flight controls, landing gear, brakes, thrust reversers, and other systems.

The flight controls segment will accounting for the largest market share in 2026 with a share of 49.36%. In addition, the segment is also estimated to be the fastest growing segment during the forecast period with the highest CAGR of 8.4%. This dominance arises from crucial function hydraulic systems perform in operating primary and secondary flight control surfaces, ailerons, elevators, rudders, flaps, slats, and speed brakes to guarantee aircraft stability, maneuverability, and aerodynamic effectiveness. New commercial aircraft such as the Boeing 787 and Airbus A350 use multiple redundant hydraulic systems with pressures of 5,000 psi to provide uninterrupted control surface actuation at all flight conditions, including take-off, cruise, and landing modes. Military transport aircraft and fighter aircraft add to the demand for flight controls through high-performance demands that require high response rates and accuracy of position for high-G maneuvers and weapon deployment.

The landing gear segment is estimated to be the second fastest growing segment during the forecast period. Market expansion for landing gear hydraulics has a 7.7% CAGR until 2032, driven by the increase in global runway infrastructure and rigorous certification standards calling for gear-down performance in cases of multiple failure modes. Business jets, regional jets, and military transport fleets embark on landing gear upgrade programs to increase service life and enhance reliability, and as such, retrofit demand builds for next-generation hydraulic actuators, accumulators, and brake control valves. OEM collaborations with landing gear producers such as Safran Landing Systems and GE Aviation underscore the strategic value of combined hydraulic solutions minimizing weight, reducing maintenance complexity, and optimizing retraction timing, braking response, and steering accuracy.

- For instance, in February 2023, the European Union Aviation Safety Agency released new regulations in 2023 mandating advanced hydraulic brake control systems with automatic anti-skid capability and enhanced runway braking performance analysis, prompting landing gear hydraulic system upgrade across commercial fleets.

By Platform

Growing Adoption of Unmanned Aerial Vehicles (UAVs) Driven by Defense and Commercial Applications Drives Segmental Growth

The market by platform segment is further sub-segmented into the fixed wing, rotary wing, and unmanned aerial vehicles (UAVs)

The unmanned aerial vehicles (UAVs) segment is estimated to be the fastest growing segment with the highest CAGR of 9.7% during the forecast period. This growth spike is driven by increasing defense acquisition of unmanned combat air vehicles (UCAVs), ISR platforms, and increasing commercial drone uses such as cargo shipping, agricultural spraying, and inspection of infrastructure. Defense spending for UAV projects is over $25 billion annually worldwide in 2024 with 900+ ISR UAVs delivered to military forces around the globe showing increasing onboard hydraulic actuation needs for weapon pylons, winglet control surfaces, and turret stabilizing systems.

- For instance, in July 2025, Northrop Grumman collaborated with the autonomous flight innovator Merlin to incorporate the advanced Merlin Pilot flight control system into its Beacon testbed framework. This will utilize a Scaled Composites Model 437 Vanguard demonstration aircraft to evaluate and showcase autonomous flight solutions for defense purposes.

From a commercial perspective, urban air mobility (UAM) and cargo drone applications require small, light hydraulic systems that provide accurate actuation under electric-hydraulic hybrid architectures. Fixed electric-only actuators do not have adequate power-density in payload levels over 500 kg, so micro-hydraulic actuators are the chosen solution.

The fixed wing segment dominated the market share in 2024 accounting for the market share of 79.20%. This demand is fueled by the large installed base of commercial airliners, military transports, business jets, and regional aircraft that use hydraulic systems for flight controls, landing gear, cargo door operation, and utility operations. Military fixed-wing platforms such as fighter aircraft, transport aircraft, and surveillance platforms are another 13,000+ aircraft, and defense modernization programs fuel demand for hydraulic systems for high-performance actuation and redundancy capabilities.

By Fixed Wing

Growing Need of Commercial Airports by Emerging Countries Simultaneously Increasing Demand for Narrow Body Segment’s Growth

The market by fixed wing segment is further categorized into narrow body, wide body, regional jet, military aircrafts, and business jet.

The narrow body segment accounted for the largest market share of 40.14% in 2024 and valued at USD 5.83 billion. This domination is supported by the world fleet of single–aisle aircraft comprising mainly Boeing 737 and Airbus A320 family aircraft which collectively amount to more than 22,000 in-service aircraft, operated by low-cost airlines, full-service network carriers, and regional airlines. Each narrow-body platform accommodates an average of 2.0 hydraulic systems that support primary flight controls, flap and slat deployment, landing gear extension/retraction, and brake control functions. Narrow-body airliner production rates are above 1,000 per year, underlining strong airline capacity growth and high utilization products that drive ongoing line-fit hydraulic system demand.

- For instance, in October 2024, Airbus certified the A321XLR's new hydraulic system architecture, combining high-pressure pumps and composite hydraulic lines. This design saves 10% in system weight, while increasing range capability to 4,700 nautical miles, showcasing ongoing innovation in narrow-body hydraulic solutions.

The wide-body segment is projected to be the fastest growing segment with a highest 8.1% CAGR in hydraulic systems during the forecast period. This growth mirrors intensifying long-haul travel demand and large-scale fleet modernization initiatives swapping out aging four-engine fleets with more efficient twin-engine wide-body configurations. Future-generation wide-body platforms place greater emphasis on more-electric architectures while maintaining hydraulic power for heavy-duty demands. Military strategic airlift modernization and VIP transport programs also contribute to broad-body hydraulic expansion, demanding unique system configurations to accommodate special mission equipment and redundancy enhancement.

- For instance, in June 2025, Boeing began the 777X hydraulic upgrade program, incorporating high-performance closed-center variable displacement pumps and high-efficiency electric motor-driven actuators that provide 25% weight savings and faster response times for the new GE9X-powered configurations.

Rotary Wing

Impact of Rising Defense Budgets, Geopolitical Tensions Driving Modernization Needs Catalyze Segment Growth

The market by rotary wing segment is further categorized into commercial helicopters and military helicopters.

The military helicopters sub-segment is estimated to be the fastest growing during the forecast period with the highest CAGR of 8.0%. The growth is driven by global defense investments and operational demands for reliable actuation in high-stress environments. This segment outpaces others due to the need for advanced hydraulic components that support mission-critical functions such as flight controls and weapon systems in rotorcraft. Key factors include escalating military expenditures, geopolitical influences, and innovations tailored to rotary-wing platforms.

- For instance, in September 2025, the U.S. Department of Defense awarded a USD 1.2 billion contract to Lockheed Martin for CH-53K King Stallion upgrades, incorporating advanced hydraulic actuation for enhanced heavy-lift capabilities.

Commercial helicopters hold over 65.95% market share in aircraft hydraulic systems as of 2024, dominating due to widespread civil applications and steady fleet growth that rely on hydraulic efficiency for versatile operations. This sub-segment benefits from high-volume production and aftermarket services, contrasting with the military's niche focus. Dominance stems from expanding non-defense uses, regulatory support, and economic recovery in aviation sectors.

Aircraft Hydraulic Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Middle East, Africa, and Latin America

North America Aircraft Hydraulic Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed 36.92% to the global market in 2025, with a valuation of USD 7.17 Billion, and is projected to reach USD 7.38 Billion in 2026. This leadership is a result of the region's large aerospace production complex, which is driven by giants such as Boeing, Lockheed Martin, and Northrop Grumman, and which reported over USD 525 billion combined aerospace and defense revenues in 2024.

The area is served by a developed commercial aviation infrastructure backed by 265,400 directly employed aviation staff in Canada alone that produces USD 23 billion in economic output. Highly developed manufacturing capacities, such as investments in artificial intelligence-based manufacturing processes and 3D printing technology, allow North American suppliers to retain technological superiority in hydraulic system development and qualification procedures.

The U.S. market is projected to reach USD 5.84 billion by 2026. The U.S. flies the largest aircraft fleet in the world with more than 44,360 daily flights managed by the Federal Aviation Administration, generating huge demand for hydraulic system parts and maintenance services.

- For instance, in September 2023, the U.S. Air Force's request of USD 5.8 billion to create 1,000 AI-powered unmanned combat aircraft is a revolutionary change in military aviation, generating unprecedented demand for sophisticated hydraulic actuation systems with autonomous operation capability. This program proves North America's dedication to upholding technological leadership through advanced hydraulic technologies serving unmanned aerial vehicle operations.

North American hydraulic system producers' domination is a testament to decades of collective experience in aerospace engineering and regulatory compliance systems. Big defense contractors such as RTX Corporation earned USD 28.28 billion in 2024 revenue, much of which came from hydraulic system integration on military and commercial platforms.

Asia Pacific

The Asia Pacific market was valued at USD 6.83 Billion in 2025, capturing 35.16% of global revenue, and is estimated to reach USD 7.12 Billion in 2026. Strengthened by record commercial aviation growth, passenger traffic is set to double by 2043 and growth rates of 7.9% per annum, the highest of any region.

China's civil aviation sector attained record-breaking performance in 2024, handling 730 million passengers (17.9% year-on-year growth) and overall transportation turnover of 148.52 billion ton-kilometers with 25% yearly growth. India stands to overtake China in air passenger traffic growth by 2026, with estimates pointing to 10.5% growth versus China's 8.9%, as fueled by the low starting point of 0.1 annual trips per capita versus China's 0.5. The Japan market is projected to reach USD 0.83 billion by 2026, the China market is projected to reach USD 1.61 billion by 2026, and the India market is projected to reach USD 1.16 billion by 2026.

The region's aviation infrastructure expansion is led by large airport expansion projects, with Singapore's Changi Airport Terminal 5 and Taiwan's Taoyuan International Airport new terminal due to become operational in the mid-2030s. The strategic location of the region that makes it easier to connect Asia, the Middle East, and Europe drives increasing demand for wide-body jets with superior hydraulic systems. Key airlines such as Air Arabia, Garuda Indonesia, and Singapore Airlines have announced large fleet expansion plans, with Vietnam Airlines eyeing massive aircraft deliveries as part of modernization efforts.

- For instance, in July 2025, the International Civil Aviation Organization obtained commitments of Asia Pacific Member States for end-to-end air travel transformation, reaching 12.4 billion passengers by 2050 with more robust digital infrastructure and harmonized border management systems that will need sophisticated aircraft hydraulic technologies

Europe

Europe accounted for USD 2.65 Billion in 2025, representing 13.66% of the global market share, and is projected to reach USD 2.79 Billion in 2026. European aviation leadership in the environment stimulates innovation in green hydraulic technologies, where airlines emit 133 million tons of CO2 in 2023, reducing by 10% from 2019 levels due to efficiency gains. The commitment of the region to environmental sustainability is reflected by ReFuelEU Aviation supply obligations for sustainable aviation fuels, with a possible reduction in net CO2 emissions of 65 million tons (47%) by 2050.

The UK market is projected to reach USD 0.14 billion by 2026, and the Germany market is projected to reach USD 0.13 billion by 2026.

European manufacturers such as Airbus supplied 766 commercial aircraft in 2024, which necessitated advanced hydraulic systems underpinning the A320 family, A350, and A330 platforms. The area has heritage aerospace clusters established in France, Germany, and U.K., backed by extensive research and development capabilities that drive hydraulic system technologies.

- For instance, in June 2025, the European Aviation Safety Agency's ReFuelEU Aviation initiative sets binding sustainable aviation fuel supply obligations that would cut CO2 emissions from the aviation sector by 47% by 2050, fueling demand for suitable hydraulic system parts and biofuel-resistant materials.

Middle East

The Middle East forms the seventh-largest aviation market to rival South Asia in terms of total capacity. The market in Middle East & Africa reached USD 1.42 Billion in 2025, representing 7.33% of total market revenue, and is projected to reach USD 1.48 Billion in 2026. United Arab Emirates and Saudi Arabia together represent 61% of regional airline capacity, with key structural variations such as Saudi Arabia's 45% domestic operations versus UAE's wholly international orientation. Large airlines such as Emirates, Qatar Airways, and Etihad Airways have large aircraft orders, with Qatar Airways having around 198 aircraft orders worth USD 72 billion as of January 2024 alone.

Latin America

The aviation industry of Latin America’s region exhibits robustness with incremental fleet growth and route network expansion, complemented by economic recovery initiatives and tourism sector reanimation. In 2025, the Latin America market stood at USD 0.78 Billion, representing 4.01% of global demand, and is projected to grow to USD 0.79 Billion in 2026. Brazil accounts for the largest market in the region, underpinned by domestic air travel demand and Embraer's ongoing aircraft manufacturing activities, which produced 206 aircraft in 2024, corresponding to 14% growth over 2023.

Africa

Africa continent's aviation industry has vast growth prospects with 2023 Aviation Infrastructure Gap Analysis covering 42 African countries and determining key investment needs for airports, air navigation facilities, and fleet expansion of aircraft to accommodate anticipated traffic expansion.

COMPETATIVE LANDSCAPE

Key Market Players

The global market is moderately concentrated with high market share among major key players in aerospace suppliers and high rivalry influenced by technological developments and strategic placement. The industry has high entry barriers involving high certification standards, high capital investment requirements, and experience requirements for specialized engineering expertise to maximize incumbent advantages over newcomers to the aerospace market.

Leading competitors seek end-to-end systems integration strategies that offer full hydraulics technology solutions instead of discrete components. This strategy allows for optimized system-level performance, minimized interface complexity, and single-source responsibility aircraft manufacturers desire for risk reduction and program management effectiveness. Organizations such as Parker Hannifin and Collins Aerospace utilize systems integration capabilities to gain higher value content per aircraft while creating long-term customer relationships.

Competitive advantage increasingly emanates from technological innovation in such fields as electro-hydraulic integration, intelligent system monitoring, and weight-reducing materials. Liebherr's innovation to design high-efficiency electric motor-powered pumps embodies innovation influence, realizing outstanding efficiency gains that immediately translate into aircraft fuel savings and operation cost reduction. Digital integration features such as predictive maintenance repair and overhaul (MRO) services, health monitoring, and remote diagnostics are new competitive differentiators.

Moreover, strategic consolidation through acquisitions allows businesses to broaden technological strength, geographic presence, and customer relations while realizing cost synergies. Safran's acquisition of Collins Aerospace flight control business is a good example of strategic consolidation producing integrated product portfolios and improved competitive stature in commercial, military, and helicopter markets. It further drives the global aircraft hydraulic systems market growth among all industry suppliers such as tier 1, tier 2, and tier 3.

List of Key Aircraft Hydraulic Systems Companies Profiled:-

- Arkwin Industries, Inc. (U.S.)

- Aviation Industry Corp. of China (China)

- CIRCOR International (U.S.)

- Crane Aerospace & Electronics (U.S.)

- Eaton Corporation plc (Ireland)

- Héroux-Devtek Inc. (Canada)

- Honeywell International (U.S.)

- HYDAC Technology GmbH (Germany)

- Liebherr-International Deutschland GmbH (Germany)

- Meggitt PLC (U.K.)

- Moog Inc. (U.S.)

- Nabtesco Corporation (Japan)

- Parker Hannifin Corporation (U.S.)

- RTX Corporation (U.S.)

- Safran S.A. (Paris)

- Senior plc (U.K.)

- Sumitomo Precision Products Co., Ltd. (Japan)

- TransDigm Group Inc. (U.S.)

- Triumph Group, Inc.

- Woodward, Inc. (U.S.)

KEY DEVELOPMENTS

- September 2025: Private charter flight company AirX has secured USD 136 million in funding to grow its fleet, which presently includes 20 large-cabin jets, with three being managed on behalf of third-party owners. The business plans to acquire an additional 20 to 50 aircraft for its fleet, focusing on heavy jets and VIP-configured airliners, including models such as the Bombardier Challenger 850, the Embraer Lineage 1000, and an Airbus A340.

- September 2025: The Guardia di Finanza police in Italy is expanding its fleet with a third Piaggio Aerospace P.180 Avanti Evo twin pusher propeller plane. As part of the agreement, the buyer has options for additional aircraft and will also obtain product support and supplies.

- September 2025: Western Australia has enhanced its emergency response capacity with the introduction of three Leonardo AW139 helicopters. CHC Helicopter is managing the aircraft for the state government. Alongside support from the Royal Automobile Club, the operation has secured USD 17.4 million in funding from the state government.

- June 2025: The S-97 Raider compound helicopter from Sikorsky is being showcased internationally for the first time. The S-97 served as the foundation for Sikorsky's S-102 Raider X, which was submitted for the U.S. Army's Future Armed Reconnaissance Aircraft (FARA) initiative.

- June 2025: Boeing is actively advancing its two main military helicopters currently in production of the AH-64 Apache and CH-47 Chinook. Autonomous features are also being integrated into the CH-47F Block II, the newest variant of the Chinook, initially aimed at enhancing safety and lessening pilot workload. The active parallel actuator subsystem (APAS) connects with the flight control system and performs several functions, including alerting operators if they are nearing potentially hazardous areas of the flight envelope.

REPORT COVERAGE

The global aircraft hydraulic systems market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE |

DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year |

2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.9% from 2026-2034 |

| Unit | USD Billion |

| Segmentation |

By Components

By Type

By Solution

By Application

By Platform

By Fixed Wing

By Rotary Wing

|

| By Region |

North America (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

Europe (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

Asia Pacific (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

Middle East (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

Africa (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

Latin America (By Components, By Type, By Solution, By Application, By Platform, By Fixed Wing, By Rotary Wing, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 19.43 billion in 2025 and is projected to reach USD 37.09 billion by 2034.

In 2025, the market value stood at USD 7.17 billion

The market is expected to exhibit a CAGR of 7.9% during the forecast period.

The flight controls segment is expected to hold the highest CAGR over the forecast period.

Growing commercial aviation sector and increasing fleet modernization programs by emerging countries drives the market growth.

Raytheon Technologies, Lockheed Martin, ThyssenKrupp Marine Systems, Thales Group, and General Atomics, among others are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us