Aircraft Seals Market Size, Share & Industry Analysis, By Seal Type (Static Seals and Dynamic Seals), By Static Seal (O-rings & X/quad-rings, Flat gaskets (ring/full-face), D-section seals (doors, windows, and nacelles), Barrier Seals, and Others), By Dynamic Seal (Shaft seals, carbon seals, Spring-energized PTFE seals, Rod/piston seals & wipers, and Others), By Material (Composite, Polymer, and Metal), By Composite (Fabric-reinforced elastomer, Laminated foil–elastomer, fiberglass, Ceramic-fiber, and Others), By Polymer, By Platform, By Application, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

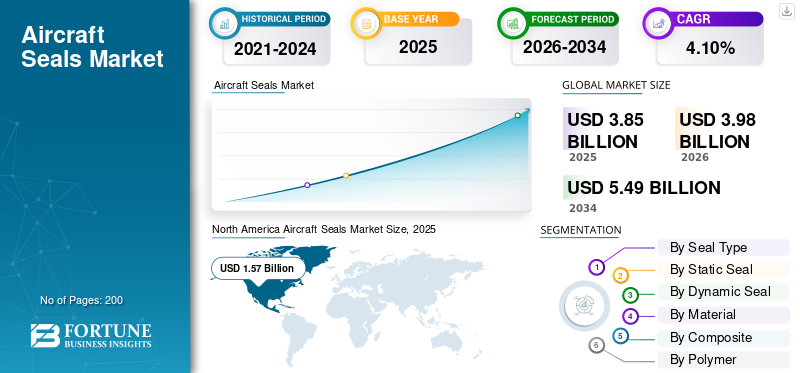

The global aircraft seals market size was valued at USD 3.85 billion in 2025. The market is projected to grow from USD 3.98 billion in 2026 to USD 5.49 billion by 2034, exhibiting a CAGR of 4.10% during the forecast period. North America dominated the aircraft seals market with a market share of 40.78% in 2025.

The aircraft seals market covers the design, qualification, and supply of components that keep fluids, gases, pressure, fire, and contaminants under control across airframe and propulsion systems. It includes O-rings, gaskets, profile/bulb, and fire-barrier seals, along with dynamic solutions such as rod or piston, shaft seals, and spring-energized PTFE assemblies. Materials include elastomers (FKM, HNBR, FFKM, VMQ/FVMQ), engineered polymers (PTFE, PEEK), and composites such as fabric-reinforced or laminated foil-elastomer constructions, with metals reserved for high temperatures and pressures. These seals are used in engines and APUs, hydraulics and landing gear, fuel systems, doors and windows, nacelles, and ECS or bleed-air systems.

Key players include Parker Aerospace (Prädifa), Trelleborg Sealing Solutions, Freudenberg Sealing Technologies, Hutchinson, Saint-Gobain Seals (Omniseal), Technetics Group, Greene Tweed, SKF Aerospace, Bal Seal Engineering, and Kirkhill (TransDigm). These players are driving innovation by using advanced materials to enhance performance.

Download Free sample to learn more about this report.

Aircraft Seals MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.85 billion

- 2026 Market Size: USD 3.98 billion

- 2034 Forecast Market Size: USD 5.49 billion

- CAGR: 4.10% from 2026–2034

- North America dominated the aircraft seals market with a 40.78% share in 2025.

- Composite segment led vessel type demand with a 16.70% share in 2025.

- D-section seals (doors, windows, nacelles) held the largest share within static seal types in 2025.

North American

North America led the market with USD 1.57 billion in 2025, driven by strong aircraft production and MRO demand.

Europe

Europe shows stable growth driven by aerospace engineering capabilities and strict certification standards.

Asia Pacific

Asia Pacific is the fastest-growing region, supported by rising aviation manufacturing and fleet expansion.

U.S.

Market reached USD 1.00 billion in 2026, supported by large fleet size and recurring maintenance demand.

Japan

Market is projected to reach USD 0.20 billion in 2026, driven by aerospace manufacturing and increasing use of advanced sealing materials.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Aging Aircraft Extend Maintenance Tails to Support Market Growth

As aircraft age, components degrade due to environmental exposure, fatigue, and general wear, necessitating more routine and non-routine maintenance. Seals, critical in preventing fluid and gas leaks in engines, hydraulics, fuel, and environmental systems, are sensitive to thermal cycling, chemical attack, and micro-movement at joints. The effect is higher inspection findings, more frequent replacements, and broader work scopes during scheduled checks. Operators increasingly adopt standardized kits and retrofit higher-performance materials (e.g., spring-energized PTFE, FFKM, PEEK) to improve reliability and extend intervals. This combination of rising maintenance activity and value-added upgrades lengthens the maintenance tail and supports notable demand for the demand.

MARKET RESTRAINTS

Strict Certification and Qualification Barriers Slow Adoption in the Aircraft Seals Market

Stringent certification and qualification barriers are a primary restraint in the aircraft seals industry, resulting in extending development timelines, elevating innovation costs, and slowing adoption of new materials and designs. Compliance with rigorous FAA/EASA requirements demands comprehensive testing, certification expenditures, and extensive documentation and traceability. These demands create high capital thresholds for R&D, tooling, and qualification campaigns, which impact smaller manufacturers to compete and limit competitive entrants.

MARKET OPPORTUNITIES

Broader Adoption of Synthetic and Sustainable Aviation Fuels to Unlock Market Opportunities

Engines and gearboxes are running hotter, while the broader use of synthetic and sustainable aviation fuels is reshaping the chemical exposure profiles. This is expanding demand for FFKM, filled-PTFE, and PEEK, along with fabric-reinforced fire seals and laminated barrier designs. The shift opens room for premium sealing materials and systems with longer life, lower friction, and better chemical tolerance. Retrofit kits tailored to known problem interfaces (leak points, abrasion zones, and cold-soak stiffness) can deliver measurable reliability wins and maintenance savings. Digital stocking, on-demand machining for spring-energized geometries, and regional finishing centers shorten lead times. Suppliers that engage early with OEMs/MROs on material qualification, kitting, and configuration support can translate technical wins into program-length revenue streams.

AIRCRAFT SEALS MARKET TRENDS

High Temperature Polymers and Advanced Material Adoption is a Key Market Trend

Adoption of high-temperature polymers and advanced materials has become a defining trend in aircraft sealing. The transition reflects industry demands for components that tolerate extreme thermal and pressure environments, reduce mass, improve fuel efficiency, and comply with stringent safety standards. With newer engines operating at elevated temperatures and tighter clearances, specifications increasingly favor high-performance elastomers (FKM, HNBR, fluorosilicone) together with PEEK and PTFE solutions that retain integrity under combined thermal and mechanical loads. These materials deliver superior resistance to jet fuel, hydraulic fluids, wear, and environmental aging, extending service intervals, lowering leakage risk, and reducing maintenance requirements over the life of the aircraft.

MARKET CHALLENGES

Specialized Material Dependence and Supply Disruptions to Deter Industry Growth

Aircraft seals depend on niche chemistries, engineered polymers, coated fabrics, and precision springs that are available from a limited number of qualified suppliers. Any disruption in regulations, geopolitical trade shifts, or energy costs hampers market growth by extending lead times and raising input prices. Rapid production ramps are difficult to meet as materials and tooling require lengthy qualification cycles. Moreover, supply chain disruptions further elongate lead times for qualified elastomers, PTFE, PEEK, coated fabrics, and precision springs, delaying scheduled maintenance and retrofit programs.

US Tariff Impact

Tariffs on imported components and raw materials such as elastomers, steel, and aluminum raise manufacturing costs for aircraft seals. These higher input costs are often passed through to OEMs and MRO providers, and ultimately to airlines. As replacement parts become more expensive under tariff regimes, operators may evaluate shifting maintenance to MRO facilities in jurisdictions with fewer trade duties to control total cost and reduce turnaround risk.

Download Free sample to learn more about this report.

Segmentation Analysis

By Seal Type

Rising Utilization and Upgrades Power Accelerate Growth of the Dynamic Seals Segment

On the basis of seal type, the market is bifurcated into static seals and dynamic seals.

The dynamic seals segment accounted for the major market share in 2025. The increasing demand is owing to higher flight cycles and harsher operating conditions that accelerate wear on moving interfaces, along with upgrades to spring-energized PTFE/PEEK designs that boost performance and value per replacement.

The static seals segment is expected to grow at a CAGR of 3.83% over the forecast period.

By Static Seal

Leak Tightness and Refurb Cadence Propel D-Section Seals (Doors, Windows, Nacelles) Segment

In terms of static seal, the market is categorized into O-rings & X/quad-rings, flat gaskets (ring/full-face), D-section seals (doors, windows, and nacelles), barrier seals, and others.

The D-section seals (doors, windows, nacelles) segment captured the largest share of the market in 2025. Demand is expanding owing to long linear runs per aircraft and tighter high-pressure/leak specifications, and due to regular door and nacelle refurbishment cycles that favor low-compression-set, low-friction profiles.

The O-rings & X/quad-rings segment is expected to grow at the highest CAGR of 3.95% over the forecast period.

By Dynamic Seal

Rising Need For Wipers to Block Grit/Water Ingress Drove Rod/Piston Seals & Wipers Segment Growth

Based on dynamic seals, the market is segmented into shaft seals, carbon seals, spring-energized PTFE seals, rod/piston seals & wipers, and others.

The rod/piston seals & wipers segment held the dominating position in 2025. This segment grows owing to heavy reciprocating loads in flight-control actuators and landing-gear struts, and the need for wipers that block grit/water ingress and standardized kits that streamline shop visits.

The segment of carbon seals is set to flourish and is growing at a CAGR of 4.42% growth across the forecast period.

By Material

High-Temp Chemistry Boosted the Polymer Segment Growth

Based on material, the market is segmented into composite, polymer, and metal.

The polymer segment held the dominating position in 2025. Growth in the segment is owing to a mix shift toward high-temperature, chemical-resistant grades (FFKM, filled PTFE, PEEK), and compatibility with evolving fluids without redesign of existing glands.

The segment of composite will witness a growth rate of 3.96% growth across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Composite

Fabric-Reinforced Elastomer Segment Led due to its Durability

Based on composite, the market is segmented into fabric-reinforced elastomer, laminated foil–elastomer, fiberglass, ceramic-fiber, and others.

The fabric-reinforced elastomer segment held the dominating position in 2025. Adoption accelerates owing to fire and thermal requirements in nacelles and firewalls, and reinforced profiles that conform to complex gaps while improving durability and installation speed.

The fiberglass segment is set to flourish with a growth rate of 3.81% during the forecast period.

By Polymer

Broad Approval Across Fuel and Lubrication Systems Encouraged Fluoroelastomers (FKM/FPM) Segment Growth

Based on polymer, the market is segmented into fluoroelastomers (FKM/FPM), Hydrogenated Nitrile (HNBR), Perfluoroelastomer (FFKM), Silicones (VMQ/FVMQ), PTFE & filled PTFE, PEEK / PAEK, and others.

The Fluoroelastomers (FKM/FPM) segment held the dominating position in 2025. Steady growth persists owing to broad approval across fuel and lubrication systems, and reliable sealing with incremental gains in compression set and low-temperature performance.

The hydrogenated Nitrile (HNBR) segment is set to flourish with a growth rate of 4.58% during the forecast period.

By Platform

Narrow-Body Segment Led the Market, Driven by Highest-Cycle Fleet

Based on platform, the market is segmented into narrow body, wide body, regional jet, military aircraft, helicopter, and UAV.

The narrow body segment held the dominating position in 2025. This growth is owing to the highest-cycle fleet that concentrates sealing needs in hydraulics, doors, and engine peripherals, and sustained production and frequent shop-visit cadence that pulls replacement demand.

The wind body segment is set to flourish with a growth rate of 4.22% during the forecast period.

By Application

High Flight-Cycle Intensity Propelled Hydraulics & Flight Actuation Segment Growth

Based on application, the market is segmented into hydraulics & flight actuation, landing gear, engines & APU, fuel systems, cabin interior, avionics, and others.

The hydraulics & flight actuation segment held the dominant position in 2025. Growth is increasing owing to high flight-cycle intensity that drives rod/piston wear in primary and secondary actuators, and stricter contamination control and leak-prevention programs that pull forward seal replacements and wiper upgrades.

The segment of landing gear is set to flourish with a growth rate of 3.95% across the forecast period.

Aircraft Seals Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America Aircraft Seals Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.51 billion, and maintained the leading share in 2025 with USD 1.57 billion. The market is expanding as a result of rising aircraft production, the need for sophisticated sealing materials, and the emphasis on safety, fuel economy, and emissions control in commercial and military aircraft. Moreover, the U.S. has a robust domestic market with a large passenger base, which increases demand for seals in both new aircraft and recurring maintenance cycles. In 2026, the market in the U.S. is estimated to reach USD 1.00 billion.

Other regions such as Europe and Asia Pacific are anticipated to witness a notable aircraft seals Market growth in the coming years. During the forecast period, the aircraft seals market in Asia Pacific is projected to record a growth rate of 4.84%, the highest amongst all regions. Asia Pacific is the fastest-growing region, driven by significant investments in domestic defense and commercial aviation programs, a thriving MRO industry, and the growing use of cutting-edge, lightweight sealing materials for improved sustainability and fuel efficiency. Backed by these factors, countries including China are anticipated to record the valuation of USD 0.32 billion, Japan to record USD 0.20 billion, and India to record USD 0.28 billion in 2026. After Asia Pacific, the market in Europe is estimated to reach USD 0.73 billion in 2026. In the region, the U.K. and Germany are each estimated to reach USD 0.28 billion and 0.18 billion, respectively, in 2026.

The Middle East and Africa, and Latin America regions would witness a moderate growth during the study period in the market. The Middle East and Africa market in 2026 is set to record USD 0.37 billion as its valuation. Latin America is set to attain the value of USD 0.23 billion by 2026.

COMPETITIVE LANDSCAPE

Strategic Co-Development and Expanding R&D Activities Define the Competitive Landscape

The aircraft seals market is moderately consolidated, led by a limited set of global specialists with deep qualification footprints. Key players such as Parker Hannifin, Trelleborg Sealing Solutions, Freudenberg Sealing Technologies, Hutchinson, Saint-Gobain Seals (Omniseal), Technetics Group, Greene Tweed, SKF, Bal Seal Engineering, and Kirkhill compete on engineering support, on-time delivery, and certification. Recently, leading suppliers have prioritized strategies that strengthen competitive advantage by expanding R&D in high-temperature polymers and spring-energized PTFE solutions, while deepening co-development partnerships with OEMs and Tier-1 integrators.

LIST OF KEY AIRCRAFT SEALS COMPANIES PROFILED

- Parker Hannifin (U.S.)

- Trelleborg Sealing Solutions (Germany)

- Freudenberg Sealing Technologies (Germany)

- Hutchinson (France)

- Saint Gobain Seals (France)

- Technetics Group (U.S.)

- Greene Tweed (U.S.)

- Bal Seal Engineering (U.S.)

- SKF (Sweden)

- Kirkhill (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2024: Trelleborg had made the decision to invest in a new production facility in Morocco with an emphasis on sealing systems for the aerospace sector. The new facility would expand capacity to accommodate the industry's robust worldwide growth while establishing a local presence for a number of customers in the nation.

- May 2025: Hutchinson declared that its O-Rings production facility in Château-Gontier-sur-Mayenne achieved the AeroExcellence Bronze level, the industry standard for operational excellence recognized by the defense and aerospace sectors.

- July 2025- Greene Tweed, a world pioneer in high-performance solutions and sophisticated materials, published study results verifying that its fluorine-based elastomer seals are compatible with Sustainable Aviation Fuels (SAF). The findings provide aircraft executives with important information as they move to low-emission, sustainable fuels while maintaining dependability and safety.

- November 2025: Freudenberg-NOK Alto Products Corp., a global manufacturer of automatic transmission parts, was acquired by Sealing Technologies and its aftermarket company Corteco. This acquisition strengthens the company’s position in the North American and international aftermarket by expanding the range of goods and services it can provide to clients globally.

- June 2025- Omniseal Solutions created and improved spring-energized sealing systems based on polymers. These high-performance seals offer consistent, dependable contact against sealing surfaces by combining internally powered springs, which come in a range of configurations, including V-springs, canted coils, and helical coils, with low-friction materials such as PTFE. The seals can adjust to the pressure variations and dimensional instability that are typical in launch settings due to their designs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.10% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Seal Type, Static Seal, Dynamic Seal, Material , Composite, Polymer, Platform, Application, and Region |

|

By Seal Type |

· Static Seals · Dynamic Seals |

|

By Static Seal |

· O-rings & X/quad-rings · Flat gaskets (ring/full-face) · D-section seals (doors, windows, and nacelles) · Barrier Seals · Others |

|

By Dynamic Seal |

· Shaft seals · carbon seals · Spring-energized PTFE seals · Rod/piston seals & wipers · Others |

|

By Material |

· Composite · Polymer · Metal |

|

By Composite |

· Fabric-reinforced elastomer · Laminated foil–elastomer · fiberglass · Ceramic-fiber · Others |

|

By Polymer |

· Fluoroelastomers (FKM/FPM) · Hydrogenated Nitrile (HNBR) · Perfluoroelastomer (FFKM) · Silicones (VMQ/FVMQ) · PTFE & filled PTFE · PEEK / PAEK · Others |

|

By Platform |

· Narrow Body · Wide Body · Regional jet · Military aircraft · Helicopter · UAV |

|

By Application |

· Hydraulics & Flight Actuation · Landing Gear · Engines & APU · Fuel Systems · Cabin Interior · Avionics · Others |

|

By Geography |

· North America (By Seal Type, Static Seal, Dynamic Seal, Material, Composite, Polymer, Platform, Application and Country) o U.S. o Canada · Europe (By Seal Type, Static Seal, Dynamic Seal, Material, Composite, Polymer, Platform, Application and Country/Sub-region) o U.K. o Germany o France o Russia o Rest of the Europe · Asia Pacific (By Seal Type, Static Seal, Dynamic Seal, Material, Composite, Polymer, Platform, Application, and Country/Sub-region) o China o Japan o India o South Korea o Rest of the Asia Pacific · Rest of the World (By Seal Type, Static Seal, Dynamic Seal, Material, Composite, Polymer, Platform, Application and Country/Sub-region) o Middle East and Africa o Latin America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.85 billion in 2025 and is projected to reach USD 5.49 billion by 2034.

In 2024, the market value stood at USD 1.57 billion.

The market is expected to exhibit a CAGR of 4.10% during the forecast period (2026-2034).

The rod/piston seals & wipers segment led the market by product type.

Broader adoption of synthetic and sustainable aviation is the key factor driving market growth.

Parker Hannifin (US), Trelleborg Sealing Solutions (Germany), Freudenberg Sealing Technologies (Germany), Hutchinson (France), Saint Gobain Seals (France)are some of the prominent players in the market.

North America dominated the aircraft seals market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us