Airport Fire and Rescue Vehicles Market Size, Share & Russia-Ukraine War Analysis, By Vehicle Type (ARFF Crash Tenders (4x4, 6x6, 8x8), Rapid Intervention Vehicles (RIVs), and others), By Propulsion Type (Conventional Diesel, Hybrid (Diesel–Electric), and Fully Electric / Zero-Emission), By Water / Foam Capacity (Up to 6,000 L, 6,001 to 10,000 L, and Above 10,000 L), By Airport Size (Mega & Large Hub Airports, Medium Airports, and others), By End User (Large International & Hub Airports, Regional & Domestic Airports, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

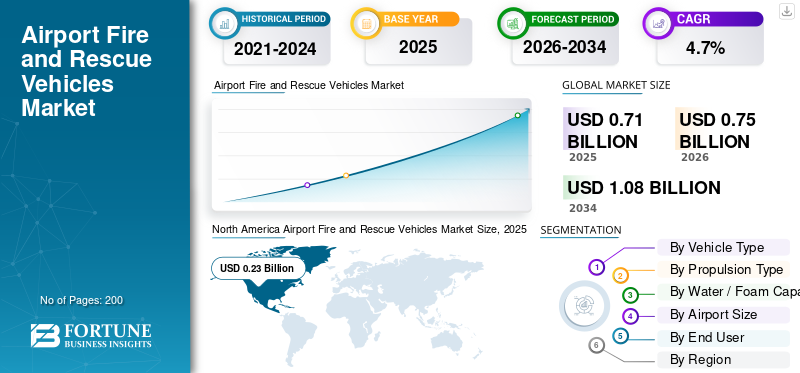

The global airport fire and rescue vehicles market size was valued at USD 0.71 billion in 2025. The market is projected to grow from USD 0.75 billion in 2026 to USD 1.08 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. North America dominated the global airport fire and rescue vehicles market with a market share of 32.39% in 2025.

Airport fire and rescue vehicles are large, specialized trucks at the edge of the runway, ready to respond when an aircraft has an issue or emergencies. They carry large tanks of water and foam, high-reach turrets, dry chemical systems, and rescue gear. These vehicles are designed to reach any point on the airfield within a few minutes, following ICAO and FAA rules. The market is driven by three main factors. These include the stringency of regulatory response and performance standards, expansion of airport networks in Asia Pacific and the Middle East, and the replacement of 20-plus-year-old trucks across airports in Europe and North America with higher-capacity, cleaner, and more digital models.

On the supply side, expansion is driven by a few specialized manufacturers that keep improving state of the art firefighting equipment. Rosenbauer, with its PANTHER line, and Oshkosh, with its Striker family and newer hybrid Striker Volterra models, are leading the market. At the same time, companies such as Magirus, NAFFCO, Morita, E-ONE, and regional manufacturers are expanding the market by customizing ARFF trucks for emerging airports in Asia, the Middle East, Africa, and Latin America.

Download Free sample to learn more about this report.

AIRPORT FIRE AND RESCUE VEHICLES MARKET TRENDS

Electrification and PFAS-Free Foam Shift ARFF Fleets toward Greener Tech

A significant trend in the market is the shift toward greener, smarter fleets. Airports are replacing older diesel ARFF vehicles with hybrid and fully electric models. These cutting edge vehicles maintain advanced firefighting capabilities with being more environmentally friendly. At the same time, regulators are pushing for a move away from PFAS-based foams. Cutting edge aircraft rescue and firefighting vehicles are being created with fluorine-free agents and improved firefighting equipment. Together, these changes are encouraging manufacturers to redesign ARFF vehicles for lower emissions, safer foam systems, and better compliance with changing safety standards during the forecast period.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Aviation Safety Standards to Push the Demand for Airport Fire and Rescue Vehicles

The steady tightening of airport safety rules is one of the main reasons fueling the market expansion. Under the guidance of the International Civil Aviation Organization (ICAO) and national regulations, airports must keep enough aircraft rescue and firefighting vehicles (ARFF vehicles) to meet strict response times, agent volumes, and performance criteria. This pressure leads operators to replace older trucks with state-of-the-art firefighting equipment. These systems have higher capacity, better reliability, and they are increasingly environmentally friendly. This shift directly increases the ARFF market size over the forecast period.

In January 2023, ICAO released the 4th edition of its Airport Services Manual, Part 1, which focuses on Rescue and Firefighting. This edition updated guidance related to Annex 14, addressing airport rescue and firefighting levels of protection, required quantities of extinguishing agents, and response time standards. It reinforces the global expectations for modern rescue and firefighting services at aerodromes.

MARKET RESTRAINTS

High Upfront Costs and Tight Airport Budgets to Restrain Market Growth

A major factor limiting airport fire and rescue vehicles market growth is high procurement cost and tight airport budgets. ARFF vehicles are costly, with a single major tender costing between USD 0.5 million and over USD 1.5 million, depending on size and the firefighting equipment it carries. Smaller and financially struggling airports find it hard to validate these investments. As a result, fleet renewal often takes many years. This situation causes older diesel units to stay in service longer than preferred, which slows the adoption of more environmentally friendly and sustainable solutions. It also limits short-term market expansion, even though the need for safety is clear.

In March 2023, Airports Council International, North America reported that U.S. airports face an estimated USD 151 billion in infrastructure needs over just five years. They noted that the required projects far exceed available funding from Airport Improvement Program grants, passenger facility charges, and airport revenues.

MARKET OPPORTUNITIES

Green ARFF Fleets and Hybrid Tech to Open New Growth Opportunities

Major opportunity in this market is the move toward sustainable and eco-friendly solutions in ARFF fleets. Airports are under pressure to reduce emissions with following strict safety rules. As a result, they are looking at hybrid and fully electric aircraft rescue and firefighting vehicles. This trend benefits companies such as Oshkosh Corporation and Rosenbauer as they are introducing innovative, low-emission ARFF vehicles that maintain full firefighting capabilities and quick response times. As more airports incorporate sustainability into their long-term plans, the demand for these next-generation, environmentally friendly vehicles is expected to grow, boosting the global market.

MARKET CHALLENGES

Foam Transition, Training, and Supply Chains May Create Challenges for ARFF Modernization

Beyond cost, airport fire and rescue teams encounter several practical challenges that slow down the modernization of ARFF fleets. Moving from old PFAS-based foams to fluorine-free agents requires rethinking tactics, retraining crews, and sometimes modifying aircraft rescue and firefighting vehicles as well as fixed systems. At the same time, global supply chain issues and long build times for modern firefighting equipment make it difficult to quickly replace aging trucks. As a result, many operators end up using old diesel fleets longer than they prefer, which slows down technological progress and the adoption of more environmentally friendly solutions over the forecast period.

In May 2023, the U.S. Federal Aviation Administration released its Aircraft Firefighting Foam Transition Plan. This plan outlines how Part 139 airports should shift from PFAS-containing AFFF to fluorine-free foams. It details decontamination processes, equipment changes, and training implications. The plan also notes that important questions about implementation and costs remain.

Impact of Russia Ukraine War

Russia–Ukraine War Disrupts Aviation and Supply Chains, Delaying ARFF Upgrades but Creating Future Rebuild Demand

The Russia-Ukraine war has a mixed, mostly indirect effect on the airport fire and rescue vehicles market. On the negative side, the closure of Ukrainian airspace, sanctions on Russian aviation, and the rerouting of Europe-Asia traffic have hurt airline finances. This has driven up fuel and operating costs, making it harder for airports to find money for new ARFF vehicles in the short term. The war has also added pressure to already weak global supply chains for trucks, chassis, and components. This has lengthened lead times and raised prices for aircraft rescue and firefighting vehicles.

On the positive side, increased defense spending in Europe and NATO countries, along with the future reconstruction of Ukraine’s damaged airports and transport infrastructure, suggests a coming surge in demand for modern firefighting equipment once rebuilding shifts from planning to action over the forecast period.

In February 2022, the European Union responded to Russia’s invasion by banning the sale of aircraft, parts, and aviation equipment to Russian companies. A few days later, they closed EU airspace to all Russian aircraft. Subsequent sanctions packages included bans on exports of aviation and space industry goods and jet fuel. The European Parliament noted that these measures, along with the closure of Ukrainian airspace, significantly impacted air passenger transport and raised transport costs across Europe.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

ARFF Crash Tenders Segment Dominates Due to Performance and Compliance Needs

By vehicle type, the market is categorized into ARFF crash tenders (4x4, 6x6, 8x8), Rapid Intervention Vehicles (RIVs), combined rescue & fire fighting vehicles, and support & auxiliary vehicles.

The ARFF crash tenders (4x4, 6x6, 8x8) dominates the market as they are the main aircraft rescue and firefighting vehicles that airports depend on to meet strict ICAO response times and airport safety rules. They carry the largest water and foam loads, have high-output turrets, and include top firefighting equipment. As a result, most fire and rescue budgets go to these heavy units first. Smaller RIVs and support trucks also play a vital role, but when funds are limited, airports usually focus on renewing the big crash tenders. This helps maintain frontline firefighting capabilities and compliance during the forecast period.

In July 2024, Rosenbauer signed a long-term agreement with the German Armed Forces to supply up to 60 PANTHER 8x8 airport firefighting vehicles. This includes an initial batch of 35 high-capacity crash tenders with 12,500-litre water tanks and advanced turret systems. These will replace older vehicles and improve airfield rescue and firefighting performance at multiple bases.

The combined rescue & fire fighting vehicles segment is expected to show the fastest CAGR of 6.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Proven Reliability and Global Fleet Familiarity to Drive Conventional Diesel Segmental Dominance

On the basis of propulsion type, the market is classified into conventional diesel, hybrid (diesel–electric), and fully electric / zero-emission.

The conventional diesel segment continues to be the main choice for airport fire and rescue vehicles as airports rely on it during times of need. Diesel-powered aircraft rescue and firefighting vehicles provide a predictable range, quick refueling, and reliable performance in extreme heat or cold. Although hybrid and electric ARFF vehicles are on the rise, most operators still stick with diesel for their main fire and rescue fleets. They only add modern low-emission units on the outskirts. These factors are poised to drive the dominance of the conventional diesel segment for most of the forecast period.

The hybrid (diesel–electric) segment is expected to show the fastest growth at a CAGR of 15.1% over the forecast period.

By Water / Foam Capacity

6,001 to 10,000 L Segment Dominates Due to Optimal Capacity and Fleet Standardization

Based on water / foam capacity, the market is segmented into up to 6,000 L, 6,001 to 10,000 L, and above 10,000 L.

The 6,001 to 10,000 L segment is popular as it balances capacity, cost, and maneuverability for most ICAO-category airports. These ARFF vehicles carry enough water and foam to meet safety standards and response-time rules at large regional and many hub airports. They do this without the extra weight and cost of the very largest trucks. As a result, this mid-range specification has become the global standard for front-line aircraft rescue and firefighting vehicles, driving the largest share of the market over the forecast period.

The above 10,000 L segment is the fastest growing segment and is set to expand at a CAGR of 8.0% over the forecast period.

By Airport Size

Medium Airports Dominates the Market Due to Heavy Regional Traffic and Consistent Capital Expenditures

Based on airport size, the market is segmented into mega & large hub airports, medium airports, and small airports & general aviation airfields.

The medium airports segment leads ARFF demand as they have enough traffic and aircraft size to need strong fire and rescue services, but they lack the big budgets of major hubs. They still require full ICAO-compliant aircraft rescue and firefighting vehicles and upgraded stations to maintain quick response times. As a result, a significant amount of ARFF spending occurs on medium airports instead of at a few major hubs. As traffic increases and more secondary cities add new routes, these medium airports are set to play a big role in renewing the global ARFF fleet during the forecast period.

In February 2024, the U.S. Federal Aviation Administration announced USD 110 million in Airport Infrastructure Grants for 71 airports. This funding includes support for new or upgraded aircraft rescue and firefighting facilities and access roads at regional and mid-sized airports such as Jamestown Regional Airport and Ford International Airport. The aim is to improve safety and emergency response capabilities.

The mega & large hub airports segment is expected to show the fastest growth at a CAGR of 5.8% over the forecast period.

By End User

Large International and Hub Airports Segment Leads owing to High Traffic and Large Aircraft Handling

The market is segmented by end user into large international & hub airports, regional & domestic airports, military air bases, and heliports & special-purpose airfields.

The large international and hub airports segment leads in ARFF spending as they handle large aircraft, high traffic, and tough airport safety audits. To meet strict safety standards and ICAO-driven response times, these hubs invest significantly in fleets of high-capacity aircraft rescue and firefighting vehicles equipped with the latest firefighting tools. They often test new, more environmentally friendly ARFF solutions first, leading to new technology deployment across these major hubs. Driven by these factors, the segment is set to dominate the global airport fire and rescue vehicles market share and show the fastest growth at a CAGR of 5.4% during the forecast period.

The heliports & special-purpose airfields segment is anticipated to be the second fastest growing segment, expanding at a CAGR of 5.0% throughout the forecast period.

Airport Fire and Rescue Vehicles Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world (Middle East & Africa and Latin America).

North America

North America Airport Fire and Rescue Vehicles Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valuing at USD 0.22 billion, and also took the leading share in 2025 with a value of USD 0.23 billion. The market is primarily led by the U.S., which alone contributes over 85.46% share of the regional share in 2025. North America, particularly the U.S., leads the global ARFF market due to its wide and busy airport network, along with strong federal funding for airport safety and infrastructure. Many of these fleets are now old enough to be replaced with newer, more effective firefighting equipment. With initiatives such as the Airport Improvement Program and IIJA grants supporting long-term market growth, the U.S. is expected to be the largest regional buyer of ARFF vehicles during the forecast period.

In July 2023, the FAA announced USD 1.9 billion in Airport Improvement Program grants, along with an additional USD 269 million in supplemental discretionary funding for 581 airport projects across the U.S. This funding is specifically allocated for runways, taxiways, safety, and sustainability upgrades at over 500 airports.

Europe

Europe is expected to see significant growth in the market in the coming years. The region is projected to depict a CAGR of 3.8% during the forecast period. In 2025, the Europe market touched a value of USD 0.20 billion. In this region, the U.K. and France are expected to reach USD 0.04 billion and USD 0.03 billion, respectively, in 2026. Europe's growth relies on environmental policy as much as on safety. Airports still require aircraft rescue and firefighting vehicles that comply with stringent safety regulations. However, regulators and investors are strongly advocating for sustainable and eco-friendly solutions.

Asia Pacific

Asia Pacific is anticipated to be the fastest growing segment in the global market growing at a CAGR of 6.7% over the forecast period. China, India, Japan, and the rest of the Asia Pacific are building new airports, upgrading smaller airports to higher ICAO categories, and increasing traffic at their current hubs. Each new or upgraded airport needs a baseline ARFF fleet, which usually includes several major crash tenders and support trucks. Even small increases in certified airports result in solid demand for ARFF vehicles and modern firefighting equipment. Based on these factors, China is anticipated to reach a valuation of USD 0.08 billion and India USD 0.04 billion by 2026.

For instance, in April 2025, a separate Vision-2040 view from the Civil Aviation Ministry says India expects around 200 functional airports by 2040, including 50 new airports to be built in the next five years. India has operationalized 88 new airports in the last 11 years, taking the total to 162. The aviation minister has stated that India now aims for “more than 350 airports” in the longer run.

Rest of the World

The rest of the world (Middle East & Africa and Latin America) contributes 9.24% in 2025. The regional segment is comparatively smaller in share but is anticipated to grow at a CAGR of 3.4% over the analysis period. In the Middle East and Africa as well as Latin America, growth is uneven but significant. It is driven by a combination of key cities and targeted improvements. Gulf cities and a few gateways in Africa and Latin America are investing in high-quality aircraft rescue and firefighting vehicles to accommodate larger planes and increased traffic. They often opt for very high-capacity and modern crash tenders.

|

Region |

Indicative new airports (to ~2035) |

Estimated Implied incremental ARFF vehicles (2–4 per airport) |

|

Asia Pacific |

≈ 250–300 |

≈ 500–1,200 |

|

Europe |

≈ 50–60 |

≈ 100–240 |

|

North America |

≈ 5–10 |

≈ 10–40 |

|

Middle East & Africa and Latin America |

≈ 40–60 |

≈ 80–240 |

Sources

- https://stay-grounded.org/planned-airport-projects/

- https://www.airport-technology.com/news/china-new-airports-2035/

COMPETITIVE LANDSCAPE

Key Industry Players

Global ARFF Specialists Focus on Safety, Green Tech, and Lifecycle Support to Gain an Edge over Competitors

The airport fire and rescue vehicles market is quite concentrated, featuring a few global manufacturers and many regional specialists. At the forefront, Rosenbauer from Austria and Oshkosh Corporation, known for Oshkosh Airport Products in the U.S., largely set the technical standards for aircraft rescue and firefighting vehicles. Their PANTHER and Striker models are commonly found in major airports across North America, Europe, and the Middle East. Both companies are advancing technology with features such as hybrid drivetrains, better cab design, enhanced firefighting capabilities, and modern firefighting gear.

Companies such as Magirus, E-ONE, NAFFCO, Morita, Kronenburg, Ziegler, along with several manufacturers from Eastern Europe and Asia, compete based on price, regional presence, and customization. Competition increasingly focuses on three areas instead of just unit sales. The first is meeting compliance and safety standards. This helps airports maintain compliance with stringent safety regulations and ICAO safety requirements through reliable, high-capacity ARFF vehicles with assured response times. Manufacturers are racing to provide more eco-friendly options, including hybrid or electric ARFF vehicles and foam systems that use fluorine-free agents. The third focus is lifecycle support, which includes long-term service contracts, digital diagnostics, and refurbishment programs that prolong fleet life and strengthen customer relationships over the forecast period.

LIST OF KEY AIRPORT FIRE AND RESCUE VEHICLES COMPANIES PROFILED

- Rosenbauer International AG (Austria)

- Oshkosh Corporation : Oshkosh Airport Products (U.S.)

- E-ONE (U.S.)

- Morita Group (Japan)

- NAFFCO (UAE)

- Magirus GmbH (Germany)

- Albert Ziegler GmbH (Germany)

- Kronenburg B.V. (Netherlands)

- Volkan Fire Fighting Vehicles (Turkey)

- ITURRI Group (Spain)

- Desautel Fire Trucks (France)

- Angloco Ltd (U.K.)

- WISS Group (Poland)

- Szczęśniak Special Vehicles Sp. z o.o. (Poland)

- Zoomlion Heavy Industry Science & Technology Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Western Sydney International Airport showcased its new Striker Volterra hybrid fire truck The fleet features high-reach extendable turrets, piercing nozzles, and infrared cameras. It highlights how modern ARFF vehicles are being integrated into the airport’s safety plan before opening.

- In November 2025, Oshkosh Airport Products announced that six Striker Volterra electric 6×6 ARFF vehicles officially started service at Dallas Fort Worth International Airport (DFW). This marked one of the first fully electric ARFF fleets at a major international airport and turned a high-profile order into everyday operations.

- In August 2023, Airservices Australia placed an order for four Striker Volterra 6×6 hybrid-electric ARFF vehicles from Oshkosh for the new Western Sydney International Airport. This positions the new airport to open with a fleet of hybrid crash tenders as part of its focus on sustainability.

- In June 2023, Rosenbauer Deutschland signed a long-term agreement with the German Armed Forces to supply up to 60 PANTHER airport firefighting vehicles over 20 years. This includes 35 PANTHER 8×8 units to be delivered by 2029, which will replace the current airfield ARFF fleet in that performance class.

- In May 2023, the U.S. Federal Aviation Administration released its Aircraft Firefighting Foam Transition Plan. This plan outlines how Part 139 airports should move from older PFAS-based AFFF to fluorine-free foams (F3). It signals to ARFF manufacturers and airports that future vehicles and systems must work with new, more sustainable options.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Vehicle Type · ARFF Crash Tenders (4x4, 6x6, 8x8) · Rapid Intervention Vehicles (RIVs) · Combined Rescue & Fire Fighting Vehicles · Support & Auxiliary Vehicles |

|

By Propulsion Type · Conventional Diesel · Hybrid (Diesel–Electric) · Fully Electric / Zero-Emission |

|

|

By Water / Foam Capacity · Up to 6,000 L · 6,001 to 10,000 L · Above 10,000 L |

|

|

By Airport Size · Mega & Large Hub Airports · Medium Airports · Small Airports & General Aviation Airfields |

|

|

By End User · Large International & Hub Airports · Regional & Domestic Airports · Military Air Bases · Heliports & Special-Purpose Airfields |

|

|

By Region |

· North America (By Vehicle Type, By Propulsion Type, By Water / Foam Capacity, By Airport Size, By End User, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) · Europe (By Vehicle Type, By Propulsion Type, By Water / Foam Capacity, By Airport Size, By End User, and By Country) o U.K. (By Vehicle Type) o Germany (By Vehicle Type) o France (By Vehicle Type) o Italy (By Vehicle Type) o Spain (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia-Pacific (By Vehicle Type, By Propulsion Type, By Water / Foam Capacity, By Airport Size, By End User, and By Country) o China (By Vehicle Type) o India (By Vehicle Type) o Japan (By Vehicle Type) o Rest of Asia-Pacific (By Vehicle Type) · Rest of the World (By Vehicle Type, By Propulsion Type, By Water / Foam Capacity, By Airport Size, By End User, and By Country) o Middle East & Africa (By Vehicle Type) o Latin America (By Vehicle Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 0.75 billion in 2026 and is projected to reach USD 1.08 billion by 2034.

In 2025, the North America market value stood at USD 0.23 billion.

The market is expected to exhibit a CAGR of 4.7% during the forecast period of 2026-2034.

The ARFF crash tenders (4x4, 6x6, 8x8) segment leads the market by vehicle type.

Stringent aviation safety standards is a key factor driving the market.

Rosenbauer International AG, Oshkosh Corporation (Oshkosh Airport Products), E-ONE, Morita Group, NAFFCO, Magirus GmbH, Albert Ziegler GmbH, Kronenburg B.V., Volkan Fire Fighting Vehicles, ITURRI Group, Desautel Fire Trucks, Angloco Ltd, WISS Group, Szczęśniak Special Vehicles Sp. z o.o., Zoomlion Heavy Industry Science & Technology Co., Ltd., and among others are the top companies in the airport fire and rescue vehicles market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us