Aluminum Oxide Market Size, Share & Industry Analysis, By Form (Powder, Pellets, and Others), By Application (Aluminum Smelting, Abrasives, Aluminum Chemicals, Refractories, and Others), and Regional Forecast, 2026-2034

ALUMINUM OXIDE MARKET SIZE AND FUTURE OUTLOOK

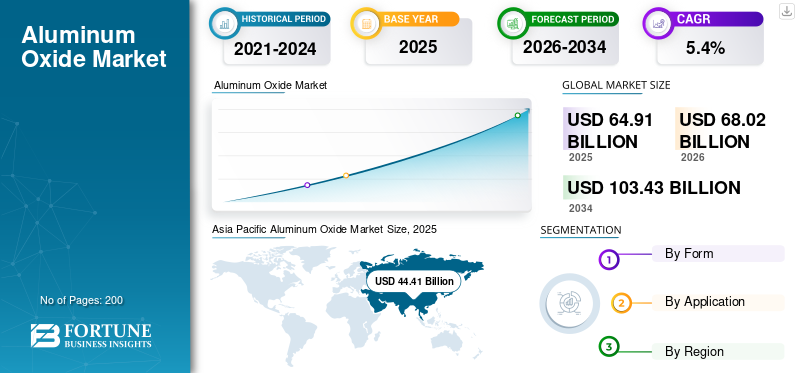

The aluminum oxide market size was valued at USD 64.91 billion in 2025. The market is projected to grow from USD 68.02 billion in 2026 to USD 103.43 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the aluminum oxide market with a market share of 68.41% in 2025.

The aluminum oxide, also known as alumina, is a chemically stable oxide of aluminum widely used as an intermediate material in aluminum smelting and as a functional material in abrasives, refractories, ceramics, electronics, aluminum chemicals, and other specialty industrial applications. The market includes both metallurgical-grade alumina used for primary aluminum production and non-metallurgical alumina used in high-performance industrial and technical applications.

The market growth is associated with its essential role in primary aluminum production, where alumina serves as the direct feedstock for smelting aluminum metal. Demand for aluminum oxide is also supported by its expanding use in abrasives, engineered ceramics, refractories, electronics, and specialty industrial materials, owing to its high hardness, thermal stability, corrosion resistance, and insulating properties. Rising industrialization, infrastructure development, lightweight material demand, and the increasing use of high-purity aluminum oxide in advanced applications further support market growth. Key players operating in the market include Aluminum Corporation of China Limited, Alcoa Corporation, Rio Tinto, Norsk Hydro ASA, and RUSAL.

Download Free sample to learn more about this report.

ALUMINUM OXIDE MARKET TRENDS

Shift Toward Specialty Grades, High-Purity Alumina, and More Value-Added Downstream is Emerging Market Trend

A major trend in the global market is the move away from viewing alumina only as a bulk metallurgical feedstock and toward a more differentiated product portfolio built around purity, soda level, particle characteristics, and downstream suitability. The International Aluminium Institute states that total alumina production includes both metallurgical-grade alumina and chemical-grade alumina, which is significant as it confirms that the market is not limited to smelter demand alone. At the company level, Sumitomo Chemical markets multiple alumina families including aluminum oxide, high-purity alumina, and activated alumina, while its product databook shows distinctions such as normal-soda, low-soda, reactive, and functional-filler grades. This depicts that suppliers are increasingly differentiating on application performance and technical specifications rather than competing only on bulk tonnage.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Primary Aluminum Smelting Demand Drives Market Growth

A major drivers for aluminum oxide market growth is its indispensable role in primary aluminum production. The International Aluminium Institute defines primary aluminium as metal produced through the electrolytic reduction of metallurgical alumina and also reports that total alumina production comprises material used for aluminium production as well as chemical-grade alumina for other uses. This is significant as it shows the market is anchored by a very large and established industrial value chain rather than depending only on fragmented specialty demand. As a result, expansion in aluminum smelting activity, refinery operating rates, and downstream aluminum demand from construction, transportation, packaging, and industrial manufacturing continues to provide the strongest structural support for alumina consumption.

MARKET RESTRAINTS

High Energy Intensity, Refining Cost Exposure, and Upstream Supply Dependence Limits Market Growth

A major restraint for the market is the heavy dependence of refining economics on energy, caustic soda, and stable bauxite supply. Alumina production is not a light chemical conversion step as it is a large-scale refining process with substantial energy use, including calcination and other directly connected operations within the plant boundary. The International Aluminium Institute’s statistical framework for alumina and primary aluminium highlights the industrial intensity of these processes, while USGS notes that U.S. bauxite consumption is largely directed into Bayer-process refining for alumina or aluminum hydroxide. This showcases that even where alumina demand is fundamentally strong, producer margins and operating discipline remain highly exposed to raw material and energy cost movements.

This restraint becomes more important when regional refinery disruptions, cost inflation, or feedstock imbalances tighten supply. As the market is still tied to metallurgical-grade alumina, refiners are not always free to pass through cost changes smoothly across the value chain. In practice, producers must balance long-term supply commitments, index-linked pricing, shipping constraints, and local operating costs, which can create volatility in profitability even when product demand remains healthy.

MARKET OPPORTUNITIES

High-Purity Alumina, Battery Materials, and Electronics Uses Create Premium Growth Space

A significant market opportunity is the expansion of high-purity and application-engineered alumina grades for batteries, electronics, semiconductors, coatings, and advanced ceramics. Sumitomo Chemical states that high-purity alumina is used in lithium-ion battery separators, translucent alumina ceramics, LED substrates, and semiconductor thermal materials, while Sasol markets advanced alumina products for battery separators, lighting, abrasives, catalyst carriers, and bioceramic materials. This is commercially important as these uses are not driven only by bulk tonnage, they are also supported by purity requirements, particle control, coating performance, and reliability standards that can support better pricing and more defensible margins than mainstream smelter-grade alumina.

Another opportunity is the continued broadening of non-metallurgical alumina demand across catalysts, refractories, ceramics, adsorbents, and industrial process materials. USGS explicitly identifies abrasives, ceramics, chemicals, and refractories as significant nonmetallurgical alumina outlets, while companies such as Sumitomo’s show active commercial positioning across activated alumina, hydraulic alumina, and functional filler grades. As advanced manufacturing, EV supply chains, electronics packaging, and cleaner industrial process technologies expand, suppliers with strong specialty-alumina capabilities should be well placed to capture higher-value growth beyond the aluminum-smelting core.

MARKET CHALLENGES

Higher demand Concentration in Regions with Large Primary Aluminum Production Challenges Market Expansion

A major challenge for the market is that although the product has multiple downstream applications, global consumption is still influenced by the smelting side of the aluminum chain. This gives the market scale, but it also shows that demand concentration remains high in regions with large primary aluminum production, especially Asia and the Middle East. The International Aluminium Institute’s production data and country coverage stated that global primary aluminum output is heavily concentrated geographically, and that concentration naturally shapes where metallurgical alumina is consumed. This can make the market more regionally imbalanced than specialty-chemical demand patterns alone would suggest.

The market also faces complexity on the specialty side, where purity, particle morphology, soda content, dispersion, and performance standards vary meaningfully by application. Sumitomo’s alumina portfolio alone extents high-purity alumina, advanced alumina, activated alumina, and application-tuned product families, illustrating that specialty growth requires more than simple capacity expansion. Producers need tighter process control, better technical service, and stronger downstream qualification pathways. This supports value creation, but also raises technical and commercial barriers for participants trying to move beyond commodity-grade refining.

IMAPCT OF TRADE PROTECTIONISM AND GEOPOLITICAL

Trade protectionism and geopolitical tensions can affect the market by increasing uncertainty around bauxite access, alumina trade flows, energy costs, and regional refining-to-smelting linkages. The OECD’s 2024 inventory reports export restrictions on industrial raw materials are becoming more prevalent and more prohibitive, with negative spillovers cascading through downstream supply chains. Alumina sits within this broader raw-materials system, which means restrictions on minerals, intermediate materials, or trade routes can influence availability, pricing, and procurement security even when the immediate restriction is not placed directly on alumina itself.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly centered on purity control, particle engineering, specialty grade development, and performance optimization for advanced applications rather than on a radical reinvention of the core refining route. Sumitomo describes its HPA products as uniform fine powders with highly pure and homogeneous crystal structure produced through an aluminum alkoxide hydrolysis process, while its broader databook differentiates low-soda, reactive, easy-sintering, and functional-filler alumina grades. This shows that development work is increasingly focused on tailoring morphology, dispersibility, sintering behavior, and impurity outlines application needs.

This makes alumina R&D less about changing the identity of the material and more about improving how it performs in batteries, electronics, thermal management, ceramics, catalysis, and coatings. Sasol explicitly positions high-purity alumina for ceramic-coated battery separators and notes its role in improving important LIB performance characteristics such as ionic conductivity and dimensional stability. As customers in semiconductors, EV batteries, LED-related materials, and engineered ceramics demand higher consistency and tighter processing windows, alumina R&D is probable to remain focused on advanced grades, cleaner processing, and more application-specific functionality.

SEGMENTATION ANALYSIS

By Form

Powder Segment Dominates Due to Its Central Role in Bulk Smelter Feed and Broad Utility Across Industrial Applications

Based on form, the market is segmented into powder, pellets, and others.

Among these, powder segment is expected to hold largest market share as mainstream alumina produced for aluminum smelting is handled in powder or granular form, and many non-metallurgical alumina products are also sold as powders tailored to ceramics, refractories, fillers, polishing, and advanced industrial uses. The International Aluminium Institute’s production definition and European Aluminium’s alumina-production description both align with alumina being produced and handled as a white powder material, while company product portfolios such as Sumitomo’s also show extensive commercialization of powder-based alumina grades.

The pellets segment also maintains a significant position. Pellets maintain relevance in selected process and handling applications, but are structurally smaller than powder in the broader market. The growth rate of segment is 4.3% during the study period.

The others segment includes specialty physical formats and processed forms serving narrower downstream requirements. Overall, form-based demand is still heavily shaped due to large-scale metallurgical consumption, even as specialty forms continue to gain importance in higher-value uses.

By Application

To know how our report can help streamline your business, Speak to Analyst

Aluminum Smelting Leads Due to Alumina’s Direct Role as Essential Feedstock for Primary Aluminum Production

Based on application, the market is segmented into aluminum smelting, abrasives, aluminum chemicals, refractories, and others.

Among these, aluminum smelting is expected to hold the leading aluminum oxide market share in 2025. Alumina is the essential intermediate raw material used to produce primary aluminum. In this process, metallurgical-grade alumina is dissolved and then reduced through electrolytic smelting to obtain aluminum metal. Since primary aluminum is widely consumed in construction, transportation, packaging, electrical systems, and machinery, alumina demand remains strongly linked to global smelter activity. This segment dominates the market in volume terms as aluminum production requires very large quantities of alumina compared tp other end uses.

The abrasives segment register significant growth during the forecast period. Alumina is widely used in abrasives due to its high hardness, wear resistance, and mechanical strength. It is used in grinding wheels, coated abrasives, polishing compounds, blasting materials, and cutting tools where durable surface finishing and material removal are required. Calcined and fused alumina grades are especially important in this segment as they provide strong cutting performance and resistance to breakdown under stress. The abrasives segment remains an important non-metallurgical outlet for alumina, supported by demand from metal fabrication, automotive, machinery, electronics finishing, and industrial maintenance applications. The growth rate of this segment is 4.2% during the study period.

The aluminum chemicals segment is also expected to account for a notable share of the market. In the aluminum chemicals segment, alumina is used as a feedstock or functional input in the production of a variety of aluminum-based chemical compounds and specialty materials. It supports the manufacture of products such as aluminum salts, catalysts, adsorbents, and other downstream inorganic compounds used in industrial processing. This segment is commercially relevant as alumina serves not only as a bulk raw material but also as a controlled chemical intermediate in processes that require specific purity and reactivity characteristics. Demand in this segment is also supported by chemical manufacturing, water treatment, catalyst systems, and other industrial processing applications.

The others segment includes a broad range of non-metallurgical and specialty applications where alumina performs technical, functional, or performance-enhancing roles. These uses may include catalyst carriers, activated alumina for adsorption and drying, polishing materials, battery-related applications, electronics-related materials, coatings, fillers, and thermal management systems.

ALUMINUM OXIDE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Aluminum Oxide Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific region holds a dominant share of the global market. The region benefits from overwhelming scale of Chinese aluminum and alumina production, additional refining and smelting activity in India and Australia, and a broad downstream industrial base spanning ceramics, refractories, batteries, electronics, and engineered materials.

China Aluminum Oxide Market

China’s market is one of the largest globally, with 2025 revenue at USD 32.80 billion, representing roughly 50.5% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America register positive growth during the forecast period. The region benefits from a combination of established smelting activity, especially in Canada, and a deeper base of specialty material demand across chemicals, catalysts, ceramics, polishing, and advanced industrial manufacturing.

U.S. Aluminum Oxide Market

In 2025, the U.S. market reached at USD 3.76 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 5.8% of global market sales. The market remains commercially important as it combines limited but real metallurgical demand with a comparatively stronger base in non-metallurgical alumina applications.

Europe

Europe register significant growth during the forecast period. The growth is due to its established aluminum value chain, technical ceramics and refractory demand, catalyst and chemicals consumption, and advanced industrial manufacturing base. European Aluminium describes alumina as the essential precursor to primary aluminium and represents refiners and smelters across the regional value chain, ensuring the continued strategic relevance of alumina within Europe. Similarly, Europe’s importance is not only tied to refining and smelting, but also to higher-value downstream uses in specialty manufacturing and process industries.

Germany Aluminum Oxide Market

The Germany market in 2025 was valued at around USD 2.70 billion, representing roughly 4.2% of global market revenues.

U.K. Aluminum Oxide Market

The U.K. market in 2025 was valued at around USD 1.31 billion, representing roughly 2.0% of global market revenues.

Latin America

Latin America is a smaller but relevant market, supported by Brazil’s role in the aluminum and alumina chain and by downstream industrial demand across the broader region. The region is less dominant than Asia Pacific in total consumption, but it remains commercially meaningful due to its role in both refining and linked industrial uses.

Brazil Aluminum Oxide Market

Brazil market in 2025 was valued at around USD 1.26 billion, representing roughly 1.9% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains highly relevant as the region includes major smelting hubs, particularly in the GCC, even though it is not the largest global alumina refining center overall. The GCC is the leading subregional market within Middle East & Africa as its large-scale primary aluminum production directly drives metallurgical alumina demand. Smelting-scale demand in Bahrain, the UAE, Saudi Arabia, Qatar, and Oman makes the GCC the core regional consumption center, while the rest of the region remains more fragmented and comparatively smaller.

GCC Aluminum Oxide Market

GCC market in 2025 was valued at around USD 3.36 billion, representing roughly 5.2% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key players are Competing Through Bauxite Access and Higher-Value Specialty Alumina Positioning

The global aluminum oxide market is concentrated around a mix of large integrated aluminium producers and alumina refiners with strong upstream control over bauxite mining, alumina refining, and in many cases aluminium smelting. Competition is shaped less by consumer branding and more by refinery scale, energy efficiency, reliability of bauxite supply, exposure to index-linked alumina pricing, and the ability to supply differentiated products such as calcined alumina, alumina hydrate, specialty alumina, tabular alumina, low-soda alumina, and high-purity alumina. Chalco states that it is the world’s largest producer and supplier of alumina, Alcoa says the acquisition of Alumina Limited strengthened its position as one of the world’s largest bauxite and alumina producers, Hydro describes Alunorte as the world’s largest single-plant alumina refinery, and Hindalco highlights its presence in specialty alumina and hydrates.

LIST OF KEY ALUMINUM OXIDE COMPANIES PROFILED IN REPORT

- Aluminum Corporation of China Limited (Chalco) (China)

- Alcoa Corporation (U.S.)

- Rio Tinto (U.K.)

- Norsk Hydro ASA (Norway)

- RUSAL (Russia)

- National Aluminium Company Limited (NALCO) (India)

- Vedanta Limited (India)

- Hindalco Industries Limited (India)

- Emirates Global Aluminium (EGA) (UAE)

- Sasol Limited (South Africa)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Hindalco announced the acquisition of AluChem Companies, Inc. for USD 125 Billion, expanding its position in specialty alumina and adding low-soda tabular alumina and other high-tech alumina grades to its portfolio.

- May 2025: Rio Tinto and Indium Corporation announced successful extraction of the first primary gallium from Rio Tinto’s Vaudreuil alumina refinery in Quebec, highlighting a value-added byproduct opportunity tied directly to alumina refining.

- January 2025: Alcoa reported that it had extended a long-term agreement to supply smelter-grade alumina to Aluminium Bahrain (Alba), reinforcing its commercial position in third-party alumina supply.

REPORT COVERAGE

The aluminum oxide market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, form, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 5.4% from 2026 to 2034 |

| Segmentation | By Form, By Application, By Region |

| By Form |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 64.91 billion in 2025 and is projected to reach USD 103.43 billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The aluminum smelting application segment is expected to lead market during the forecast period.

Asia Pacific held the highest market share in 2025.

Primary aluminum smelting demand drives market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us