Application Performance Management Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (On-premises, Cloud and Hybrid), By Enterprise Type (Large Enterprises and SMEs), By Application (Web APM and Mobile APM), By Industry (BFSI, Retail, Manufacturing, IT & Telecom, Healthcare and Others), and Regional Forecast, 2026 – 2034

APPLICATION PERFORMANCE MANAGEMENT MARKET SIZE AND FUTURE OUTLOOK

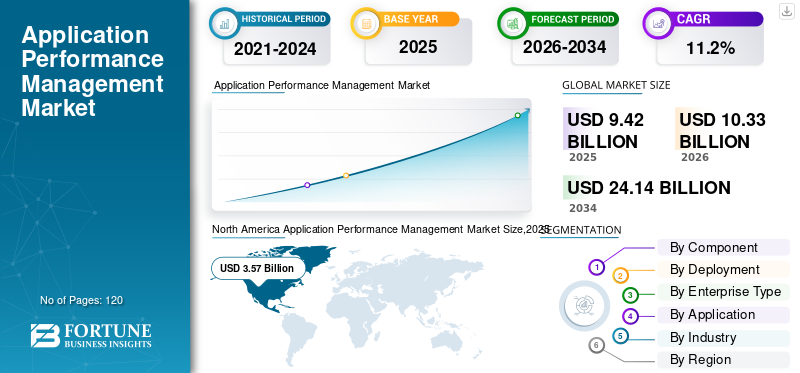

The global application performance management market size was valued at USD 9.42 billion in 2025. The market is projected to grow from USD 10.33 billion in 2026 to USD 24.14 billion by 2034, exhibiting a CAGR of 11.2% during the forecast period. North America dominated the global application performance management market with a market share of 37.9% in 2025.

Application performance management (APM) focuses on tools and systems that monitor, trace, and optimize applications in web, mobile, micro services and cloud native contexts. The market is primarily driven by increasing demand for real-time insight into user experience and revenue-critical digital services as well as quick adoption of cloud and containerized architectures from businesses, thus making traditional application performance monitoring insufficient.

Additionally, monitoring real-time user journeys and business transactions is becoming highly crucial due to growing reliance on digital services for both income and customer experience. Companies are also encouraged to invest in APM technologies that facilitate quicker releases, root cause research, and decreased downtime due to expansion of complex hybrid IT environments, DevOps, and Site Reliability Engineering techniques. These factors fuel market growth, globally.

The market is dominated by established key players, such as Akamai Technologies, Cisco AppDynamics, Broadcom Inc., Datadog Inc. and Dynatrace Inc. These players are focusing on integrating APM with broader observability platforms, combining logs, metrics and traces into a single analytics layer to provide full-stack visibility. Companies are also investing heavily in AI driven analytics that automate anomaly detection, root cause analysis, and performance optimization.

Download Free sample to learn more about this report.

Application Performance Management Market key takeaways

- 2025 Market Size: USD 9.42 billion

- 2026 Market Size: USD 10.33 billion

- 2034 Forecast Market Size: USD 24.14 billion

- CAGR: 11.2% from 2026-2034

- North America dominated the application performance management market with a 37.9% share in 2025.

- The software segment captured the largest market share in 2025, reaching USD 6.42 billion.

- The hybrid deployment segment is projected to grow at the highest CAGR of 13.1% during the forecast period.

North America

North America maintained its leading position in 2025, with the market valued at USD 3.57 billion.

Asia Pacific

Asia Pacific is estimated to reach USD 2.62 billion in 2026 and is projected to grow at the highest CAGR of 13.9% during the forecast period.

Europe

Europe is anticipated to reach USD 2.59 billion in 2026, registering a CAGR of 10.3% during the forecast period.

U.S.

The application performance management market is estimated to reach USD 3.04 billion in 2026.

Japan

Growing cloud adoption and increasing digital transformation initiatives are driving demand for application performance management solutions.

Read More

IMPACT OF GENERATIVE AI

Generative AI is Reshaping Market with Integration of Predictive Monitoring and Intelligent Insights

Generative AI is rapidly influencing the market by turning conventional monitoring into predictive and intelligent solutions. By evaluating telemetry data, it makes automated root cause analysis, anomaly identification and proactive issue forecasting easy. This helps in detecting possible performance issues before they have an impact on end users. The need for observability solutions capable of managing intricate, AI-based workloads is growing as businesses incorporate generative AI into their operations, opening up new growth prospects for the industry. Additionally, generative AI makes observability accessible to a wider range of users, such as product teams and business owners, by automating insights and providing natural-language explanations. For instance,

- In January 2025, Dynatrace highlighted its AI‑powered observability tools, presented at its Perform 2025 conference and aimed at helping clients monitor and optimize deployments of AI systems and LLM‑backed applications.

MARKET DYNAMICS

Market Drivers

Growing Adoption of Hybrid and Multi-Cloud Environments Fuels Demand for Unified APM Solutions

The rapid adoption of hybrid and multi-cloud environments has led to increasingly fragmented IT infrastructures, where applications and workloads are spread across various cloud providers, on-premise systems and edge environments. This results in isolation of application resources, leaving organizations without full insight into their applications or ability to monitor all components of an application from a performance perspective. Monitoring performance across network, API, container and third-party service, presents challenges due to the broad range of potential performance issues that exists at multiple tiers.

Organizations need a solution that monitor every aspect of an application using a single view, combining log files, metrics and traces. Full-stack visibility enables development and operations teams to pinpoint or rule out the root cause of performance issues, limit application downtime and actively support reliable application performance in a mixed environment. Thus, organizations are searching for combining solutions with the goal of enhancing visibility across their systems. For instance,

- November 2025, Palo Alto Networks plans to acquire Chronosphere, a cloud‑native observability platform, for USD 3.35 billion. Through this acquisition, the company aims to combine Chronosphere’s real‑time observability with Palo Alto Networks’ AI‑driven security and monitoring competences to better service modern cloud and AI‑native workloads.

Market Restraints

High Implementation Costs and Complexity Hinders Market Growth

For many small/medium-sized businesses, APM tools present a considerable challenge due to high price tag and level of complexity. For most small and medium-sizedbusinesses, switching to an entirely new APM tool set is not feasible, as it requires a significant amount of time, money and specialized skills to successfully implement it. In addition, companies need customization of their APM solutions due to the company's specific requirements regarding IT environment or unique business processes.

Market Opportunities

Rising Adoption of APM Among SMEs and Digital Native Firms Fuels Market Growth

Smaller businesses that previously relied on simple or manual methods can get advanced performance monitoring due to the trend toward SaaS-based APM products. The rising adoption of cloud applications and API-driven architectures by SMEs and digital native businesses has increased their need for more in-depth performance and user experience monitoring. For smaller teams with limited resources, modern APM technologies provide easy onboarding, reasonable pricing, and automatic insights. This opens up an unexplored market opportunity that may encourage significant demand in the future. Long-term revenue potential for APM vendors increases as these businesses grow and demand more sophisticated observability capabilities. For instance,

- In September 2025, Splunk Observability Cloud launched new features that enhance hybrid-application monitoring and provide richer context for synthetic-transaction alerts and user journeys, underscoring demand for unified monitoring solutions across hybrid and multi-cloud environments.

Application Performance Management Market Trends

Surge in Partnerships within Cloud and DevOps Ecosystem Pushes Market Growth

As APM is widely adopted globally, with vendors forming partnerships and alliances with DevOps tool providers. This aims to connect their solutions seamlessly with the tools that developers and operation team utilize. Vendors benefit from their ability to connect with cloud providers, container orchestration technology, CI/CD, and incident management tools. When these solutions work together, it becomes easier for customers to adopt an APM solution. By creating seamless integration of data between build, deploy, and operate, these integrated tools enable APM platforms to provide higher visibility into application performance and support faster troubleshooting. Additionally, vendors are able to provide a larger distribution channel for their products and services through partnerships and/or collaborations with companies that are leading to the emergence of Cloud Native/Container technology. For instance,

- In November 2025, Microsoft introduced new AI-powered full-stack observability capabilities in Azure Monitor. Through this launch, the company aims to strengthen its offerings.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Growing Demand for Cloud Based Monitoring Strengthens Software Segment Leadership

Based on component, the market is bifurcated into software and services.

Software captured the largest market share and is estimated to reach USD 6.42 billion for 2025. Enterprises are increasingly adopting cloud-based APM platforms that provide automated monitoring and analysis with minimal service dependence. Increasing architectural complexity and introduction of advanced features such as AI-assisted diagnostics are further increasing the dominance of software segment.

Services are anticipated to grow at the highest CAGR of 12.2% during the forecast period, as organizations increasingly rely on expert implementation, configuration, and managed support to optimize complex cloud-native and hybrid application settings.

By Deployment

Rapid Enterprise Shift to Cloud Environments Strengthens Segment Growth

Based on deployment, the market is divided into on-premises, cloud, and hybrid.

Cloud segment secured the largest application performance management market share and reached 3.75 billion for 2025, as many companies have moved to scalable cloud solutions and are looking to implement APM solutions in their own cloud ecosystem that allow faster deployment, cheaper costs, and enhanced monitoring of micro-services and container apps. Suppliers are also focusing on cloud-first features that makes it easier for businesses to utilize and take advantage of cloud solutions.

Hybrid deployment is expected to grow at the highest CAGR of 13.1% during the forecast period, as enterprises need APM solutions that balance on-premises systems and cloud as well as provide end-to-end visibility into both environments.

By Enterprise Type

Complex IT Ecosystems in Large Enterprises Drive Strong Adoption of Advanced APM Solutions

Based on enterprise type, the market is classified into large enterprises and SMEs.

Large enterprises captured the largest market share and secured USD 6.35 billion of revenue for 2025. Large enterprises operate complex and distributed application ecosystems, which require advanced APM for real-time visibility and performance assurance. Their huge IT budgets and faster adoption of cloud native, microservices-based architectures further supports higher investment in comprehensive APM platforms.

SMEs are expected to grow at a highest CAGR of 13.5% during the forecast period, driven by SaaS-based APM tools that are available at affordable prices for SMEs, enabling them to take advantage of more sophisticated monitoring solutions without higher investment in infrastructure or staffing of a specialized APM team.

By Application

High Dependence on Web Applications Sustains Dominance of Web APM Solutions

Based on application, the market is divided into web APM and mobile APM.

Web APM captured the largest market share reached USD 6.54 billion in 2025. This is due to a strong demand for web APM solutions among companies, as majority of business-critical applications currently operate on web-based interfaces. In addition, as companies open up to the full potential of online interactions, the need for comprehensive performance monitoring tools has increased.

Mobile APM is expected to grow at the highest CAGR of 13.6% during the forecast period. This is owing to a significant increase in the number of mobile-first companies, as well as the growing consumer demand for access to content from their mobile devices. There is also an increasing expectation that mobile apps perform better than traditional desktop applications.

By Industry

Critical Need for Uptime and Security Drives BFSI Sector’s Dominance in APM Adoption

Based on industry, the market is categorized into BFSI, retail, manufacturing, IT & telecom, healthcare, and others.

BFSI segment accounted for the largest market share and reached USD 2.23 billion in 2025. Increasing use of digital technologies in BFSI sector for financial transactions and customer service has a massive influence on this growth. Many companies investing large amounts of money into developing APM solutions to support their APM requirements, including uptime, security and compliance.

Healthcare is projected to grow at the highest CAGR of 14.1% during the forecast period. The growth of digital health applications, telehealth using online services, and patient management systems has positioned APM solutions as a critical part of building, operating, and maintaining digital health systems to ensure reliable performance and data security.

To know how our report can help streamline your business, Speak to Analyst

APPLICATION PERFORMANCE MANAGEMENT MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America held the largest market share in 2024, valued at USD 3.30 billion, and also maintained the leading share in 2025, with USD 3.57 billion. This is due to the advanced technological infrastructure and high adoption rates of digital transformation initiatives within the region, which provide significant support for continued growth in this marketplace. In addition to the presence of numerous leading APM vendors, increased demand for APM solutions from large companies and cloud service providers has also contributed to the continued growth of APM solutions in this region. For instance,

- In May 2024, Cisco launched a new virtual appliance for its on-site AppDynamics observability tool. It has new AI features for spotting unusual things and figuring out what's causing problems in SAP and other business apps.

North America Application Performance Management Market Size,2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2026, the U.S. market is estimated to reach USD 3.04 billion. The market is growing rapidly, due to an increased focus on digital transformation through continued shift of businesses toward cloud services, micro services and hybrid IT architectures requiring advanced-level APM tools. In addition, the presence of many of the leading APM vendors, along with innovative solutions using artificial intelligence (AI) for real-time APM, has led to an increased demand the service across industries.

Europe

Europe is anticipated to witness a moderate growth in the coming years. During the forecast period, the European region is anticipated to record a growth rate of 10.3%, which is the fourth highest amongst all the regions, and reach the valuation of USD 2.59 billion in 2026. This is primarily due to focus of European businesses on investing money to digitally transform their businesses through cloud technology. Additionally, strict regulations regarding data privacy, security, and compliance, has led to an increase in the need for strong APM solutions. The shift toward hybrid and multi‑cloud deployments have created massive demand for advanced APM solutions in European IT environments. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 0.48 billion, Germany to record USD 0.51 billion, and France to record USD 0.41 billion in 2026.

Asia Pacific

The market in the Asia Pacific is estimated to reach USD 2.62 billion in 2026, and grow at a highest CAGR of 13.9% during the forecast period. Organizations in the region are increasingly looking for advanced APM tools to provide the necessary capabilities to monitor performance and reliability within their distributed and complex infrastructures. In the region, India and China both are estimated to reach USD 0.35 billion and USD 0.56 billion, respectively, in 2026. For instance,

- In October 2024, according to an industry expert’s survey, 90% of Asia Pacific enterprise respondents reported using either multi-cloud or hybrid cloud-based workloads. As a result there is a considerable demand for performance monitoring tools to manage workload performance across heterogeneous clouds.

South America

South America is expected to witness significant growth in this market. The South American market in 2026 is set to record USD 0.68 billion. The market growth is owing to increased adoption of cloud infrastructure and digital services by enterprises, which creates demand for APM solutions that deliver application performance and user experience.

Middle East & Africa

The Middle East & Africa region is estimated to reach USD 0.56 billion in 2026 and grow at a prominent growth rate in the coming years. The market is driven by large investment made into cloud technology and digital transformations across the region. Thus, there is a rise in demand for sophisticated monitoring solutions employed within multi-cloud and hybrid environments. Additionally, increased data center investment and cloud adoption in the region, particularly in the GCC countries, also increased the need for robust APM solutions that provide optimal performance and reliability. In the region, GCC is set to attain the value of USD 0.18 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Are Expanding APM Capabilities and Integrating Observability Solutions to Strengthen Their Market Position

Leading companies in the market are shifting from traditional monitoring tools to advanced observability platforms that provide in-depth visibility of hybrid and multi-cloud environments. Vendors are focusing on offering easy-to-use integration of AI-based analytics, real-time user monitoring, and advanced root cause analysis to support cloud-native application architectures. In addition, different vendors also provide integration of APM tools with CI/CD pipelines, microservice frameworks, and DevOps toolchains, as a way to improve the efficiency of performance management, maintaining system uptime, and quickening the ability to troubleshoot issues. To meet these goals, these vendors have added automation and AI optimization tools to their offerings to simplify operational processes and enhance application reliability.

Long List of Application Performance Management Companies Studied

- Akamxai Technologies (U.S.)

- Cisco AppDynamics (U.S.)

- Broadcom Inc. (U.S.)

- Datadog Inc. (U.S.)

- Dynatrace Inc. (U.S.)

- IBM Corporation (U.S.)

- Open Text Corporation (Canada)

- Microsoft Corporation (U.S.)

- Oracle Corporation (U.S.)

- New Relic Inc. (U.S.)

- BMC Software (U.S.)

- Riverbed Technology (U.S.)

- LogicMonitor (U.S.)

- Splunk (U.S.)

- SolarWinds (U.S.)

- Elastic (U.S.)

- Grafana Labs (France)

- Sumo Logic (U.S.)

- Google Cloud (U.S.)

- Honeycomb.io (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Cisco and Splunk announced a unified full‑stack observability experience by integrating AppDynamics with Splunk log analytics and IT‑service intelligence, enabling joint customers to monitor applications, infrastructure and business metrics seamlessly.

- July 2025: Akamai launched the Akamai App Platform, now in General Availability (GA), offering developers a ready to use Kubernetes based Platform for deploying and monitoring their cloud-native applications and performance.

- June 2025: AppSignal has secured USD 22 million in Series A funding to expand its products and services to North America and target smaller engineering teams and mid-size businesses as a growth area.

- May 2025: During Microsoft’s Build 2025 event, Azure Monitor launched a series of new AI-based troubleshooting options and expanded its observability capabilities by providing health-based models and code suggestions for more efficient monitoring and performance management for both cloud-based and hybrid applications.

- March 2025: Dynatrace acquired Metis Technologies company, which uses AI to keep track of databases. The idea is to make Dynatrace even better at watching everything in your tech stack, from the hardware up to the data itself, and making sure it all runs smoothly.

- June 2024: Akamai Technologies acquired the U.S.-based API security provider, Noname Security. Through this acquisition, the company aims to use Noname Security's expertise in Akamai’s solutions and strengthen its portfolio.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the application performance management market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component

By Deployment

By Enterprise Type

By Application

By Industry

By Region

|

| Companies Profiled in the Report |

|

Frequently Asked Questions

The market is expected to reach USD 24.14 billion by 2034.

In 2025, the market was valued at USD 9.42 billion.

The market is expected to grow at a CAGR of 11.2% during the forecast period.

By industry, BFSI sector led the market.

Growing adoption of hybrid and multi-cloud environments fuels demand for unified APM solutions.

Akamai Technologies, Cisco AppDynamics, Broadcom Inc., Datadog Inc., Dynatrace Inc., IBM Corporation, Open Text Corporation, Microsoft Corporation, Oracle Corporation, and New Relic Inc. are the top players in the market.

North America held the highest market share.

By industry, healthcare sector is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us