APU Repair and Overhaul Service Market Size, Share & Industry Analysis, By Service Type (Repair, Overhaul, Inspection & Diagnostics, Testing & Certification, Modifications & Compliance, and Support Services), By Maintenance Level (Line Maintenance (On-wing), Intermediate / Component Shop, and Depot / Heavy Shop Visit), By Aircraft Type (Narrow Body, Wide Body, Regional Jets, and Others), By End User (Airlines, Leasing Companies, Business Aircraft Operators, and Government Operators), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

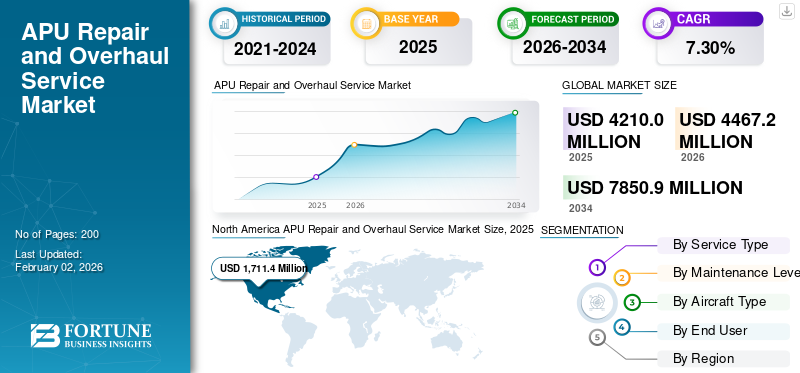

The global APU repair and overhaul service market size was valued at USD 4210.0 million in 2025. The market is projected to grow from USD 4467.2 million in 2026 to USD 7850.9 million by 2034, exhibiting a CAGR of 7.30% during the forecast period. North America dominated the global APU repair and overhaul service market with a market share of 40.65% in 2025.

APU repair and overhaul involves disassembling, inspecting, repairing, or replacing components such as life-limited parts, and testing small gas turbine engines to restore them to OEM standards, often at set intervals based on flight hours or cycles. These units, typically in aircraft tail cones, supply onboard electrical power and air for air conditioning, engine starting, and in-flight backups without ground equipment. They support commercial, military aviation, and business jets for autonomous operations.

Key APU maintenance, repair and overhaul (MRO) players include Lufthansa Technik, Honeywell International Inc., and others, which run global shops offering testing, repairs, and leasing for multiple APU types. The major players also provides long-term APU maintenance service plans and fleet-wide support for airlines such as Air India to improve reliability and reduce cost risk.

Download Free sample to learn more about this report.

APU REPAIR AND OVERHAUL SERVICE MARKET TRENDS

Integration of Digital Twin and AI is the Latest Market Trend

The integration of digital twins and AI represents a key trend in the APU repair and overhaul industry, creating virtual replicas of units that mirror real-time performance using sensor data on vibration, temperature, and fuel flow. These models enable predictive analytics to forecast failures, optimize inspection intervals, and simulate repairs before physical disassembly, reducing downtime for airlines. AI algorithms process historical flight data alongside live inputs to detect anomalies in turbine blades or generators early, supporting condition-based maintenance over fixed schedules.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Air Traffic and Fleet Expansion to Drive Market Growth

The increasing global air traffic intensifies aircraft utilization, accelerating APU wear from frequent engine starts and high-cycle operations, which necessitates more frequent repair and overhaul cycles to maintain reliability. Fleet expansion, fueled by post-pandemic recovery and new aircraft deliveries, introduces additional units requiring scheduled maintenance, initial inspections, and component replacements. Low-cost carriers and cargo operators emphasize APU uptime for Extended-range Twin-engine Operational Performance Standards (ETOPS) compliance and operational efficiency, while aging fleets in secondary markets demand intensive overhauls.

MARKET RESTRAINTS

Stringent Regulatory Compliance to Restraint Market Growth

Stringent regulatory compliance restrains APU repair and overhaul service market growth by imposing rigorous inspection mandates, certification standards, and continuous airworthiness requirements under FAA and EASA rules, which demand extensive documentation and qualified personnel. Operators must adhere to ETOPS protocols monitoring APU performance metrics such as oil consumption and vibration, triggering frequent shop visits that strain resources. Enhanced safety crackdowns post-incidents require advanced training and audits, elevating costs and delaying approvals for repairs.

MARKET OPPORTUNITIES

Expansion of Urban Air Mobility to Offer Market Opportunity

As electric vertical takeoff and landing (eVTOL) aircraft are increasing to alleviate urban congestion, there is a growing need for a reliable power source. These platforms demand lightweight, hybrid-electric APUs or power systems optimized for frequent short flights, creating the need for specialized maintenance, battery-integrated overhauls, and rapid-turnaround MRO. Moreover, APUs supply vital power for systems (such as air conditioning, lights, and avionics), which is necessary for fast turnarounds in crowded urban vertical ports and increases the demand for dependable APU repair and overhaul services.

MARKET CHALLENGES

Skilled Labor Shortages May Hinder the Market Growth

Skilled labor shortages are likely to hinder the market growth by limiting the availability of certified technicians proficient in turbine disassembly, vibration analysis, and hybrid-electric diagnostics. Moreover, specialized training for evolving APU architectures in case of electric aircraft systems demands extended apprenticeships amid competing industries. Owing to this, providers struggle to scale capacity, prompting reliance on outsourced labor or automation pilots which is a challenge for market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service Type

Rising Regulatory Mandates to Drive the Overhaul Segment’s Dominance

On the basis of segmentation by service type, the market is segmented into repair,

overhaul, inspection & diagnostics, testing & certification, modifications & compliance, and support services.

The overhaul segment dominated the global APU repair and overhaul service market share in 2025. The segment growth is primarily driven by regulatory requirements by various aviation regulatory bodies such as FAA, EASA, and among others.

The repair segment is poised to expand at the highest CAGR of 7.44% over the analysis period.

By Maintenance Level

Complex Maintenance Cycles to Fuel Depot / Heavy Shop Visit Segment

In terms of maintenance level, the market is classified into line maintenance (on-wing), intermediate / component shop, and depot / heavy shop visit.

The depot / heavy shop visit segment captured the largest market share in 2025. APU maintenance is complicated, specialized, and heavily regulated, requiring considerable, in-depth work at specialized facilities. This complex nature of maintenance cycles is a key factor influencing segment growth.

The intermediate / component shop segment is anticipated to expand at the highest CAGR of 7.56% over the forecast period.

By Aircraft Type

Narrow Body Segment to Expand Given the Largest Commercial Aircraft Fleet

Based on aircraft type, the market is segmented into narrow body, wide body, regional jets, and others.

The narrow body segment held a dominant share in the global market in 2025. The majority of the world's fleet of commercial aircraft comprise narrow-body models. APU maintenance is one of the MRO services which is in more demand due to the sheer number of these aircraft in service.

The wide body segment is set to flourish at a CAGR of 7.43% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Airlines Segment Dominates the Market Owing to the Need for Maximizing Aircraft Utilization Rate

By end user, the market is categorized into airlines, leasing companies, business aircraft operators, and government operators.

The airlines segment held a dominating market share in 2025. Airlines place a high priority on maximizing aircraft availability and usage. They have direct control over maintenance schedules or have closely linked partnerships with MRO providers, which enables timely APU servicing and less aircraft ground time.

The leasing companies segment will witness the highest growth rate of 7.84% during the forecast period.

APU Repair and Overhaul Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America APU Repair and Overhaul Service Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America held the dominant share in 2024, valuing at USD 1579.5 million, and also took the leading share in 2025, with a value of USD 1711.4 million. The market for APU repair and overhaul services in North America is expanding due to its huge commercial and military fleets, strong production, and significant OEM presence such as Honeywell, Pratt & Whitney, and others. The U.S. market is anticipated to expand, driven by fleet modernization, extended lifespans of mature aircraft, and the increasing demand for efficient MRO. In 2026, the U.S. market is estimated to reach USD 1107.8 million.

Europe and Asia Pacific

Regions such as Europe and Asia Pacific are anticipated to show notable market expansion over the forthcoming years. During the analysis period, the Asia Pacific market is projected to record a CAGR of 7.82% during the forecast period, which is the highest amongst all the regions. The regional market is expanding owing to increased investment in MRO infrastructure, growing fleets (particularly in China and India), rising demand for air travel, and a strategic emphasis on digital/predictive maintenance. Driven by these factors, China is anticipated to record the valuation of USD 527.8 million, Japan to record USD 213.8 million, and India is set to record USD 367.9 million in 2026.

Following Asia Pacific, the Europe market for APU repair and overhaul services is estimated to reach a value of USD 991.8 million in 2026. The regional growth is driven by increased air traffic, fleet growth, stringent EU sustainability regulations (such as Flight Path 2050), and technological advancements toward digital MRO and low-emission solutions. In the region, U.K. and Germany are estimated to reach USD 347.8 million and 274.2 million each in 2026.

Rest of the World

In the rest of the world, the Middle East and Africa and Latin America regions would grow at a moderate rate over the forecast period. In 2026, the Middle East and Africa market for APU repair and overhaul services is set to record USD 181.0 million as its valuation. Latin America is set to depict the value of USD 105.6 million in 2026. The growth is driven by strategic partnerships, expanding fleets, and aircraft modernization programs, among others.

COMPETITIVE LANDSCAPE

Leading Players Emphasize Predictive Maintenance and Authorized Repairs to Secure Competitive Edge

The APU repair and overhaul service market features dominant players such as StandardAero, Lufthansa Technik, Honeywell Aerospace, Tag Aero, and Safran. These key players are focusing on authorized repairs, predictive maintenance, and hybrid-electric upgrades to gain competitive edge in the market. Recent strategic partnerships and acquisitions have helped enhance global shop capabilities and digital twin integration. Furthermore, the expansion of military sustainment contracts alongside commercial fleet modernizations bolsters service reliability. Additionally, industry leaders are prioritizing field repairs and supply chain resilience, with strong momentum in North America and Europe driven by fleet growth, defense programs, and regulatory compliance.

LIST OF KEY APU REPAIR AND OVERHAUL SERVICES COMPANIES PROFILED

- Honeywell Aerospace Technologies (U.S.)

- Pratt & Whitney (Canada)

- Safran (France)

- Lufthansa Technik (Germany)

- EPCOR (AFI KLM E&M) (Netherlands)

- TurbineAero (U.S.)

- TAT Technologies (Israel)

- StandardAero (U.S.)

- Delta TechOps (U.S.)

- AMECO (Aircraft Maintenance & Engineering Corporation) (China)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Austrian Airlines and Lufthansa Airlines inked a 14-year maintenance and support contract with Pratt & Whitney Canada. The 41 APS5000 APUs (auxiliary power units) on the two airlines' combined Boeing 787 aircraft fleet are covered by the agreement.

- August 2025: A contract for MRO services for the GTCP331-500 APU (Auxiliary Power Unit) used on the B777 (Boeing 777) platform was signed by TAT Technologies Ltd. with an international commercial carrier. The three-year agreement is worth about USD 12 million in revenue or USD 4 million annually on average.

- June 2025: Honeywell and Vietjet Air signed a five-year contract to maintain Honeywell's 331-350 Auxiliary Power Units (APUs) on Vietjet's fleet of Airbus A330 aircraft.

- February 2025: Lufthansa Technik and Eastern Airlines Technic (EASTEC), a China Eastern Airlines’ subsidiary, inked a 12-year exclusive maintenance services deal. The deal covers technical assistance for all of China Eastern Airlines' Airbus A350 fleet's auxiliary power units (APUs).

- November 2024: Honeywell chose Qatar Airways as the official maintenance, repair, and overhaul (MRO) supplier for the Auxiliary Power Units (APUs) of the Airbus A350.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.30% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Service Type, Maintenance Level, Aircraft Type, End User, and Region |

|

By Service Type |

· Repair · Overhaul · Inspection & Diagnostics · Testing & Certification · Modifications & Compliance · Support Services |

|

By Maintenance Level |

· Line Maintenance (On-Wing) · Intermediate / Component Shop · Depot / Heavy Shop Visit |

|

By Aircraft Type |

· Narrow Body · Wide Body · Regional Jets · Others |

|

By End User |

· Airlines · Leasing Companies · Business Aircraft Operators · Government Operators |

|

By Geography |

· North America (By Service Type, Maintenance Level, Aircraft Type, End User and Country) o U.S. (Aircraft Type) o Canada ( Aircraft Type) · Europe (By Service Type, Maintenance Level, Aircraft Type, End User and Country/Sub-region) o U.K. ( Aircraft Type) o Germany ( Aircraft Type) o France ( Aircraft Type) o Russia ( Aircraft Type) o Rest of the Europe ( Aircraft Type) · Asia Pacific (By Service Type, Maintenance Level, Aircraft Type, End User and Country/Sub-region) o China ( Aircraft Type) o Japan ( Aircraft Type) o India ( Aircraft Type) o South Korea ( Aircraft Type) o Rest of the Asia Pacific ( Aircraft Type) · Rest of the World (By Service Type, Maintenance Level, Aircraft Type, End User and Country/Sub-region) o Middle East and Africa ( Aircraft Type) o Latin America ( Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4210.0 million in 2025 and is projected to reach USD 7850.9 million by 2034.

In 2025, the North America market value stood at USD 1711.4 million.

The market is expected to exhibit a CAGR of 7.30% during the forecast period of 2026-2034.

The overhaul segment dominated the market by service type in 2025.

Rising global air traffic and fleet expansion are key factors driving the market growth.

StandardAero, Lufthansa Technik, Honeywell Aerospace, Tag Aero, and Safran are some of the key players in the market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us