Limited Slip Differential Market Size, Share & Industry Analysis, By Vehicle Type (SUV & Pickup Trucks and Sedan & Hatchback), By Type (Mechanical and Electronic), By Sales Channel (OEM and Aftermarket), By propulsion Type (ICE and Electric), By Drive Type (ALL-Wheel Drive, Front-Wheel Drive, and Rear-Wheel Drive), and Regional Forecast, 2026-2034

Limited Slip Differential Market Size and Future Outlook

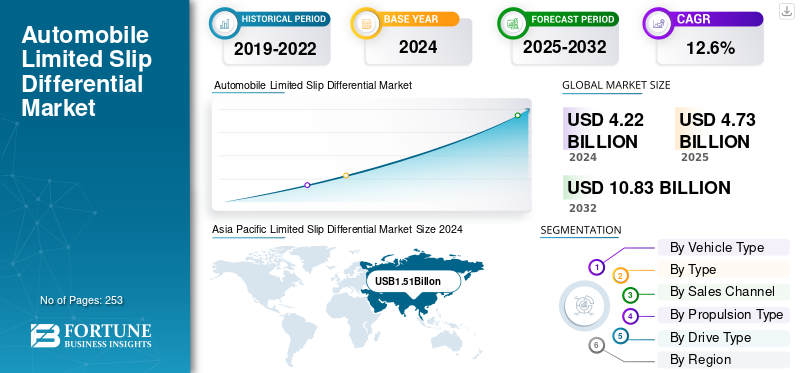

The global limited slip differential market size was valued at USD 4.73 billion in 2025. The market is projected to grow from USD 5.3 billion in 2026 to USD 13.68 billion by 2034, exhibiting a CAGR of 12.58% during the forecast period. Asia Pacific dominated the limited slip differential market with a market share of 36.58% in 2025.

A Limited Slip Differential (LSD) is a mechanical or electronic device integrated into a vehicle’s drivetrain that allows drive wheels to rotate at different speeds while maintaining torque distribution. Unlike an open differential, which can lose traction when one wheel slips, an LSD limits this slip to enhance grip and stability during acceleration, cornering, or on uneven surfaces. It is widely used in high-performance cars, sports vehicles, SUVs, and off-road applications to improve handling, safety, and traction efficiency.

The global market is expanding steadily, driven by increasing demand for high-performance vehicles and the growing integration of advanced traction systems in off-road and sports models. Demand is reinforced by consumer preference for enhanced vehicle stability and control under diverse driving conditions. Key players such as ZF Friedrichshafen AG, Eaton Corporation, JTEKT Corporation, GKN Automotive, BorgWarner Inc., and Dana Incorporated lead innovation through electronically controlled and torque vectoring LSDs. Advancements in sensor technology and integration with all-wheel-drive systems are transforming performance capabilities, supporting market growth across passenger cars and light commercial vehicles globally.

Download Free sample to learn more about this report.

Impact of U.S. Tariffs on Market

U.S. tariff policies have influenced the global limited slip differential market demand by increasing the costs of raw materials and imports for automotive components sourced from Asia and Europe. Tariffs on steel, aluminum, and precision gear assemblies have increased production costs for manufacturers including Eaton and Dana. This has prompted some OEMs to localize sourcing or modify supply contracts. Temporary cost pressures and disrupted import timelines have modestly slowed North American LSD supply chains; however, strong domestic manufacturing bases have helped mitigate the long-term impact on overall production.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Electric Vehicles (EVs) is Driving Growth of LSD Market

The global transition toward electric mobility is emerging as one of the most significant drivers for the limited slip differential market growth, particularly for electronic Limited Slip Differentials (eLSDs). EVs, known for their instant torque delivery, create unique traction and stability challenges that conventional open differentials cannot manage effectively. As a result, eLSDs equipped with electro-hydraulic actuators and electronic control units are increasingly being used to distribute torque dynamically across the driven wheels, ensuring maximum grip, stability, and performance under varying driving conditions.

According to the International Energy Agency (IEA), global electric vehicle sales surpassed 14 million units in 2024, marking a 35% year-on-year increase, with EVs now representing over 18% of total car sales globally. This expanding EV base directly translates into rising demand for advanced drivetrain components, such as eLSDs, that can handle the rapid, high-torque characteristics of electric propulsion systems. Automakers are actively integrating eLSDs into their EV platforms to enhance traction control systems, cornering precision, and driver confidence, particularly in high-performance and all-wheel-drive (AWD) electric models.

For instance, the Hyundai Ioniq 5 N (2024) employs an eLSD on the rear axle to deliver optimized cornering performance, while BMW’s iX and i4 M50 use electronically controlled differentials to balance torque distribution during high-speed maneuvers. Such systems enhance handling responsiveness while minimizing energy losses from wheel slip, thereby indirectly contributing to improved energy efficiency and range consistency.

Furthermore, as EV adoption grows across regions such as Europe, China, and North America, where stricter safety and vehicle dynamics standards are enforced, the implementation of advanced differential systems is becoming a key design priority. Tier-1 suppliers such as ZF Friedrichshafen AG, BorgWarner Inc., and Eaton Corporation are investing heavily in eLSD technologies designed for electric and hybrid drivetrains, indicating a long-term shift in the market from mechanical LSDs to electronically managed solutions.

MARKET RESTRAINTS

Shift Toward Motor-Based Torque Vectoring in EVs is Restraining LSD Market

The rapid acceleration of electric vehicle (EV) adoption is fundamentally reshaping how torque is managed and distributed across wheels, gradually reducing the need for traditional (LSDs) and even advanced electronic LSDs (eLSDs). In EVs, torque vectoring the ability to control power delivery to each wheel can now be achieved directly through multiple electric motors managed by sophisticated control software. This approach provides faster response, lighter weight, and better system integration, eliminating many of the mechanical components that LSDs rely on.

According to IDTechEx (2024), the average number of motors per battery-electric vehicle increased by 13% between 2015 and 2023, driven by the rise of dual- and tri-motor platforms. These setups enable instant, software-controlled torque distribution between wheels, effectively performing the same role as an (eLSD). For instance, vehicles such as the Tesla Model S Plaid, Lucid Air, and Rivian R1T utilize multiple motors to deliver precise torque vectoring without the need for a mechanical differential. This shift is especially common in high-performance and all-wheel-drive EVs.

Moreover, as automakers push for lighter and more energy-efficient platforms, the elimination of heavy mechanical differential systems aligns with the broader industry goal of improving range and powertrain efficiency. With advances in inverter and control algorithms, software-based torque management now offers automakers greater design flexibility, reduced complexity, and lower long-term maintenance costs. As a result, several leading OEMs are increasingly prioritizing motor-driven torque control over traditional LSD hardware.

Consequently, while the LSD market continues to find applications in performance ICE vehicles and hybrid drivetrains, the growing shift toward electronically managed, motor-based torque vectoring systems presents a clear restraint for LSD manufacturers. Suppliers are being compelled to diversify their portfolios toward hybrid-compatible, electronically assisted, or software-integrated differential systems to maintain relevance in an electrified and software-defined automotive future.

MARKET OPPORTUNITIES

Expanding Integration of LSDs in Hybrid and Autonomous Drivetrains

The rapid evolution of hybrid and autonomous vehicle technologies is creating significant growth potential for LSD & eLSD manufacturers. As automakers strive to deliver improved traction, smoother power transitions, and enhanced control under automated driving, LSDs are being redesigned to function as intelligent torque management systems integrated with hybrid power control units and electronic stability software. In hybrid vehicles, torque often shifts between internal combustion engines and electric motors, requiring highly responsive differentials that can balance power across axles in milliseconds.

According to the U.S. Energy Information Administration (EIA), battery-electric and hybrid vehicles together accounted for over 21% of all new light-duty vehicle sales in the U.S. during Q3 2024, reflecting rapid consumer adoption of hybridized platforms. Likewise, the U.K.’s Zero Emission Vehicle (ZEV) Mandate, introduced in 2024, and requires automakers to ensure that at least 22% of vehicles sold in 2024 are zero-emission, with targets increasing to 80% by 2030. These regulatory trends are encouraging OEMs to expand hybrid offerings and invest in technologies that enhance drivetrain stability, efficiency, and control.

Manufacturers such as Toyota, Honda, and Hyundai have already integrated electronically managed differentials into their hybrid systems. As vehicles approach Level 3 and Level 4 autonomy, the ability to predictively control wheel torque and vehicle dynamics becomes vital. eLSDs equipped with embedded sensors and communication interfaces can exchange data with ADAS (Advanced Driver Assistance Systems) and vehicle control units to maintain traction during autonomous lane changes, sharp turns, or low-traction scenarios.

LIMITED SLIP DIFFERENTIAL MARKET TRENDS

Growing Shift Toward Digitally Controlled and Sensor-Integrated LSDs

The automotive industry is steadily moving toward digitally managed and sensor-integrated (LSDs) as part of the wider transition to software-defined vehicles. Unlike traditional mechanical LSDs, modern electronic LSDs (eLSDs) are mechatronic systems that communicate with the vehicle’s control units and sensors to deliver predictive, real-time torque management. These systems monitor parameters such as wheel speed, steering angle, and traction levels to dynamically adjust torque between wheels, enhancing stability, handling, and efficiency across varying road conditions.

Leading suppliers, such as ZF Friedrichshafen AG and BorgWarner Inc., have introduced eLSDs that utilize sensor fusion and control algorithms for adaptive torque vectoring. ZF’s recent driveline systems integrate seamlessly with ADAS and stability control software, enabling proactive traction management that improves both safety and energy utilization. Similarly, BorgWarner’s latest torque vectoring modules utilize embedded microcontrollers to digitally manage wheel torque distribution digitally, replacing traditional mechanical systems.

As connected and autonomous vehicles evolve, LSDs are expected to function as intelligent torque control nodes, capable of integrating with vehicle networks, predictive traction software, and even over-the-air (OTA) updates. The ongoing digitalization of the Limited Slip Differential market trends is transforming LSDs from passive drivetrain components into data-driven, upgradeable systems, redefining their role in next-generation mobility platforms.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

SUV & Pickup Trucks Dominate Owing to Rising Consumer Preference for Versatile, High-Performance Vehicles Capable of Handling Varied Terrains

Based on vehicle type, the market is categorized into SUV & pickup trucks and sedan & hatchback.

SUV & pickup trucks segment is projecteed to dominate the market with a share of 69.68% in 2026 due to the requirement for enhanced traction and off-road capability. LSDs can seamlessly redistribute engine torque from a slipping wheel to one with grip, directly addressing the core performance requirements of these vehicle types. Additionally, there has been a significant, multi-year shift in global consumer preferences toward larger, multi-purpose vehicles, such as SUVs and crossovers. The demand for SUVs and pickup trucks is projected to grow steadily, driven by rising consumer preference for versatile, high-performance vehicles that can handle varied terrains. These vehicle types increasingly integrate advanced driveline systems such as (LSDs) to enhance traction, stability, and towing capability. Expanding off-road, recreational, and utility applications continue to drive the LSD market growth.

By Type

Mechanical Limited Slip Differentials Dominate Due to Reliability, Simpler Design, and Cost-Effectiveness.

In terms of type, the market is bifurcated into mechanical and electronic.

Mechanical LSDs segment is projecteed to dominate the market with a share of 63.94% in 2026 due to their proven reliability, simpler design, and cost-effectiveness. They offer consistent performance in conventional drivetrains, making them a preferred choice for SUVs, pickup trucks, and off-road vehicles. The wide availability of mechanical LSDs in both OEM and aftermarket channels, along with their lower maintenance requirements, continues to sustain their strong market presence and steady adoption across diverse vehicle categories globally.

By Sales Channel

Rising Production of SUVs, Pickups, and Performance-Oriented Models has strengthened the OEM Segment

By sales channel, the market is segmented into OEM and aftermarket.

The OEM (Original Equipment Manufacturer) segment is projecteed to dominate the market with a share of 82.82% in 2026 as automakers increasingly integrate LSDs during vehicle manufacturing to enhance traction, safety, and driving comfort. Rising production of SUVs, pickups, and performance-oriented models has strengthened OEM adoption. Additionally, the shift toward advanced driveline technologies, particularly electronic and torque-vectoring LSDs, has prompted manufacturers to equip new vehicles with these systems as standard or premium options, ensuring steady demand through the forecast period. Major brands such as Toyota, Ford, and BMW continue to equip their vehicles with mechanical or electronic LSDs, reinforcing OEM dominance in the market.

By Propulsion Type

ICE Dominates as ICE Fleet Still Constitutes the Majority of Global on-Road Stock

Based on propulsion type, the market is segregated into ICE and electric.

The dominance of the ICE segment is projecteed to dominate the market with a share of 80.56% in 2026 is supported by the vast number of conventional vehicles in operation and the continued production of high-volume models, such as SUVs and pickup trucks. Mechanical LSDs remain widely used in these vehicles to enhance traction and driving stability, especially under challenging terrain or towing conditions. The strong presence of ICE-based drivetrains, particularly in emerging markets, ensures sustained demand for LSD integration through the forecast period. The enduring global demand for petrol and diesel vehicles ensures the steady prominence of LSDs in this propulsion category.

By Drive Type

Rear-Wheel Drive Dominates Owing to Extensive Use in Performance Cars, Sports Coupes, and Premium Sedans

In terms of drive type, the market is classified into all-wheel drive, front-wheel drive, and rear-wheel drive.

Rear Wheel Drive vehicles currently dominate the market, primarily due to their extensive use in performance cars, sports coupes, and premium sedans. LSDs play a crucial role in improving traction, acceleration, and cornering stability in RWD setups. Automakers such as BMW, Ford (Mustang), and Toyota (GR Supra) continue to equip their RWD models with mechanical or electronic LSDs as standard or optional features, maintaining this segment’s leading market share through 2032. Many high-performance and luxury manufacturers, such as BMW, Lexus, and Chevrolet, equip their RWD models with mechanical or electronic LSDs to ensure superior driving dynamics and control, sustaining the segment’s strong market presence.

To know how our report can help streamline your business, Speak to Analyst

LIMITED SLIP DIFFERENTIAL MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

The market in Asia Pacific reached USD 1.73 Billion in 2025, representing 36.58% of total market revenue, and is projected to reach USD 1.97 Billion in 2026. Asia Pacific dominates LSD demand on sheer vehicle output and fast-rising SUV/UV penetration. China produced 31.28 million vehicles and sold 31.44 million in 2024, with exports at a scale of 5.86 million, which multiplies driveline content opportunities, from mechanical LSDs to eLSDs in performance EVs. India set a new PV record at 4.3 million in 2024, with utility vehicles increasing by 17% to 2.7 million, thereby boosting LSD take-rates for FWD/ AWD SUVs. JAMA reports Japan’s passenger-car production +18.3% (to 7.77 million), supporting continued LSD content in sporty and AWD grades. On the technology front, Asia Pacific OEMs specify Torsen-type LSDs (JTEKT) in halo cars (e.g., the Toyota GR Yaris, featuring front/rear Torsen), and OS Giken continues to proliferate multi-plate LSDs across Japanese sports platforms, keeping enthusiast and motorsport demand vibrant. With China’s output, India’s SUV surge, and Japan/Korea performance lineages, Asia Pacific is both the largest and fastest-growing LSD region. That volume scales suppliers’ mechanical and electronic LSD lines, lowering costs and accelerating global diffusion, especially into EVs and performance SUVs, where torque-vectoring eLSDs are a differentiator. The Japan market is valued at USD 0.40 billion by 2026, the China market is valued at USD 0.76 billion by 2026, and the India market is valued at USD 0.35 billion by 2026.

Asia Pacific Limited Slip Differential Market Size 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market was valued at USD 1.22 Billion in 2025, capturing 25.72% of global revenue, and is estimated to reach USD 1.35 Billion in 2026. Limited-slip differential (LSD/eLSD) demand in North America is pulled by high volumes of trucks/SUVs and by performance-oriented AWD programs. In the U.S., new-vehicle sales climbed to 16 million units in 2024 (highest since 2019), keeping pickup/SUV fitments central to the driveline mix. From the supply side, Eaton (Detroit Truetrac, ELocker) expanded fitments and unveiled an EV-Truetrac tuned for the unique lubrication and high-torque loads of electric axles (2025), directly relevant to e-axle-based eLSD architectures. Meanwhile, AAM’s TracRite portfolio (including electronic variants) underpins OEM pickup/SUV programs, and its earlier collaboration with Drexler foreshadowed high-performance eLSDs for global platforms. As a scale indicator supporting LSD uptake across light trucks and performance cars, OICA records that the U.S. produced 9.13 million commercial vehicles and 1.43 million passenger cars in 2024. The combination of robust pickup/SUV sales (U.S.) and North American truck production sustains high take-rates for mechanical LSDs and growing migration to eLSDs on premium/EV trims, feeding global growth via shared platforms and supplier scale. The U.S. market is valued at USD 0.96 billion by 2026.

Europe

In 2025, Europe held 23.24% of the global market, reaching a valuation of USD 1.1 Billion, and is projected to grow to USD 1.23 Billion in 2026. Europe’s LSD/eLSD pull is driven by premium SUVs and performance derivatives, as well as the rapid electrification of vehicles, which favors torque-vectoring eLSD solutions. GKN Automotive’s eTwinster torque-vectoring modules are now a core strategy for EV handling, building on applications ranging from the Range Rover Evoque to the Focus RS; this technology pathway is increasingly specified for new e-axles. ZF’s networked eLSD integrates with brake systems and OTA-ready controls, an architecture aligned with Europe software-defined vehicle roadmaps. Market fundamentals support volumes: Europe new car registrations rose by 0.8% in 2024 to around 10.6 million, and SUVs reached a record share of 54% (6.92 million units), both of which lifted AWD/LSD installations on high-torque models. On the commercial side, Europe’s buses/coaches rose 9.2% in 2024, while electrically chargeable bus registrations jumped 26.8%, a proxy for e-axle/eLSD adoption in heavy-duty vehicles. With premium/performance SUVs scaling and EV torque management transitioning to software-controlled eLSDs, Europe emerges as the second-fastest-growing region for LSD content, reinforcing global supplier learning curves and exports. The U.K. market is valued at USD 0.23 billion by 2026, while the Germany market is valued at USD 0.38 billion by 2026.

Rest of the World

In 2025, Rest of the World generated USD 0.68 Billion, contributing 14.46% to global market revenue, and is projected to grow to USD 0.75 Billion in 2026. Rest of the World’s growth is anchored by Latin America and the Middle East, where SUVs dominate consumer preference and off-road use. Brazil rebounded strongly, with 2024 sales reaching a 10-year high (+14% to 2.63 million), according to ANFAVEA. Additionally, 2024 production increased by 9.7%, both of which are supportive of LSD content in pickups and crossovers. In the Gulf, robust 4×4/SUV adoption underpins LSD fitments for desert duty cycles (multiple sources note strong 2024 growth), while local luxury/performance demand sustains premium eLSDs. On the supplier side, aftermarket and OE-service channels (Eaton Detroit Truetrac, AAM TracRite) remain active, ensuring LSD availability for popular truck platforms across LATAM and MENA. ultimately, recovering LATAM volumes and SUV-heavy Gulf demand add steady incremental LSD pull; combined with export-linked Mexico, RoW acts as a positive tail to global LSD growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Trend Toward Adopting Electrified, Adaptive LSD Technologies Optimized for EVs and Hybrids is Driving Key Market Players

The Global Limited Slip Differential (LSD) Market is moderately consolidated, with key manufacturers such as Eaton Corporation, ZF Friedrichshafen AG, JTEKT Corporation, GKN Automotive, Dana Incorporated, BorgWarner Inc., AAM (American Axle & Manufacturing), and Drexler Automotive GmbH dominating both OEM and performance segments. These players compete through advancements in electronic LSD (eLSD) systems, torque-vectoring integration, and electrified driveline compatibility. Eaton remains strong in mechanical and electronic locking differentials, while ZF and GKN lead in eLSD units for premium EVs and AWD platforms. JTEKT and OS Giken maintain their strength in high-performance and motorsport applications, particularly in Japan and Europe. Ongoing partnerships with OEMs for next-generation EV torque-vectoring axles (e.g., ZF’s eLSD integration in software-defined chassis) and increased demand in SUVs and electric performance vehicles are reshaping the competitive landscape toward intelligent, electronically controlled systems.

Major players, including Eaton, ZF, BorgWarner, GKN, Dana, AAM, JTEKT, OS Giken, Drexler, and Quaife, are trending toward electrified, adaptive LSD technologies optimized for EVs and hybrid drivetrains. The market is moving from traditional clutch-based mechanical LSDs to smart eLSDs with real-time torque control and integration with vehicle stability and traction systems. Companies are investing in lightweight, compact differential units, improved thermal management, and software-controlled torque distribution, aligning with global shifts to electrification, performance SUVs, and autonomous-ready driveline platforms.

ZF Friedrichshafen is the global leader in driveline and chassis technologies, holding the top position in the LSD market due to its extensive experience, technical diversity, and strong OEM penetration. Its LSD portfolio includes mechanical clutch-type, multi-plate, and advanced eLSDs integrated into torque-vectoring systems. ZF’s Active Kinematics Control and Torque Vectoring Differentials enhance traction and dynamic stability in high-performance and luxury vehicles. The company supplies leading OEMs, such as BMW, Audi, and Porsche, and has been instrumental in developing LSDs that are adaptable to hybrid and electric platforms. Its strong R&D capabilities, precision manufacturing, and integration of electronic control with mechanical reliability position ZF as the most comprehensive and innovative player in the global LSD market.

JTEKT Corporation ranks second globally due to its ownership and continuous advancement of TORSEN (Torque Sensing) differential technology, a benchmark in helical gear-based LSD systems. JTEKT’s LSDs are widely adopted by major automakers, including Toyota, Lexus, Audi, and Subaru, for both front and rear axles. The TORSEN systems deliver instantaneous torque biasing without the need for clutches, ensuring durability and consistent performance. Additionally, JTEKT has expanded into electronically controlled differentials (eLSDs) and hybrid-compatible drivetrains to align with EV and AWD trends.

LIST OF KEY LIMITED SLIP DIFFERENTIAL COMPANIES PROFILED

- Drexler Automotive GmbH (Germany)

- JTEKT Corporation (Japan)

- Eaton Corporation (Ireland)

- BorgWarner Inc. (U.S.)

- ZF Friedrichshafen AG (Germany)

- Linamar Corporation (Canada)

- GKN Automotive (U.K.)

- Dana Limited (U.S.)

- American Axle & Manufacturing Inc. (U.S.)

- CUSCO Japan Co., Ltd. (Japan)

- RT Quaife Engineering Ltd. (U.K.)

- Xtrac Ltd. (U.K.)

- OS Giken (Japan)

- Carraro SpA (Italy)

- Yukon Gear & Axle (U.S.)

- Auburn Gear LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, BorgWarner Inc. secured a new eXD (electric cross differential) contract with a leading Chinese OEM, where the system dynamically controls slip and torque distribution between wheels in EV architectures, essentially a next-generation electronic LSD/torque-vectoring platform.

- In May 2025, Eaton expanded its electronically controlled Limited Slip Differential portfolio (InfiniTrac/eLSD), offering a fully variable torque distribution device (from open differential to full lock) with response time under 100 ms, integrating vehicle sensors, and scalable across multiple platforms, including EVs.

- In January 2025, JTEKT established its “Solution Co-Creation Center,” which leverages its “Core Competence Platform” to bring together gear, bearing, and machine-tool technologies under one roof. This initiative supports JTEKT’s 2030 Vision of becoming a solution provider that creates the future of the mobility society.

- In June 2024, BorgWarner introduced its modular eLSD and AWD cross-axle systems, which combine electronic clutch actuation with intelligent control algorithms for optimal torque distribution. These systems integrate traditional LSD functionality with software-based dynamics management, providing enhanced traction, performance, and stability for hybrid and electric drivetrains. This innovation highlights BorgWarner’s continuous modernization of drivetrain technology.

- In October 2023, the company unveiled its eCrate modular electric drive unit, a plug-and-play solution derived from its 20-year eDrive and LSD heritage, enabling niche OEMs and retrofit startups to access integrated motor, transmission, and inverter modules. The launch underscores GKN’s move from mechanical LSDs into full electrified torque-management systems.

REPORT COVERAGE

The global limited slip differential market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market forecast offers a comprehensive competitive landscape, including market share, growth prospects, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.58% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Type, By Distribution Channel, By Fuel Type, By Material, and By Region. |

| By Vehicle Type |

|

| By Type |

|

| By Sales Channel |

|

| By Propulsion Type |

|

| By Drive Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.3 Billion in 2026 and is projected to reach USD 13.68 Billion by 2034.

In 2025, the market value stood at USD 1.73 billion.

The Limited Slip Differential market growth is expected to expand at a CAGR of 12.58% during the forecast period of 2026-2034.

SUV & Pickup Trucks segment accounted for the largest contribution in the limited slip differential market share with 69.2% in 2024.

The rising adoption of electric vehicles (EVs) is driving the growth of the LSD market

Top players in the market include ZF Friedrichshafen AG, American Axle Manufacturing, Eaton Corporation, JTEKT Corporation, and GKN Automotive.

Asia Pacific dominated the market in 2025.

North America, Europe, Asia Pacific, and the Rest of the World.

- 2021-2034

- 2025

- 2021-2024

- 253

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us