Automotive Carbon Fiber Composites Market Size, Share & Industry Analysis, By Carbon Fiber Type (PAN-based and Pitch-based), By Resin Type (Thermoset and Thermoplastic), By Application (Structural Components, Exterior Parts, Interior Components, Powertrain Components, and Others), By End-use (Passenger Cars, Electric Vehicles, Commercial Vehicles, and Others), and Regional Forecast, 2026-2034

Automotive Carbon Fiber Composites Market Size and Future Outlook

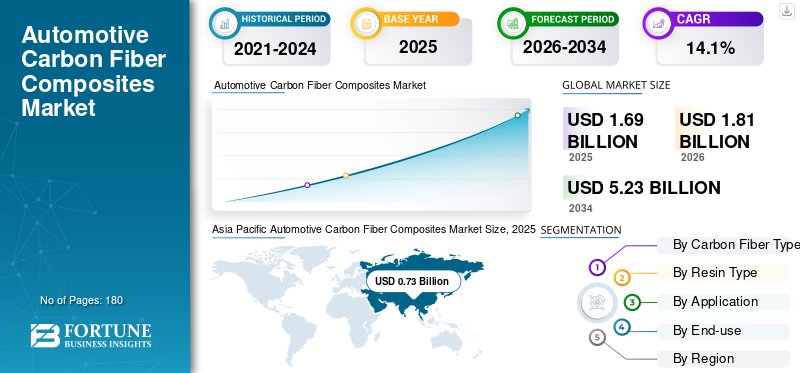

The global automotive carbon fiber composites market size was valued at USD 1.69 billion in 2025. The market is projected to grow from USD 1.81 billion in 2026 to USD 5.23 billion by 2034, exhibiting a CAGR of 14.1% during the forecast period. Asia Pacific dominated the automotive carbon fiber composites market with a market share of 43.19% in 2025.

The market comprises materials such as carbon fiber reinforced polymer (CFRP) materials used in passenger cars, electric vehicles, and commercial vehicles for structural, exterior, interior, and powertrain applications. These composites combine carbon fibers with thermoset or thermoplastic resins to deliver high strength-to-weight ratio, corrosion resistance, and superior crash performance. The market includes PAN-based and pitch-based carbon fibers integrated through processes such as resin transfer molding (RTM) and automated fiber placement.

A key global driver shaping the future outlook is the accelerating electrification of the automotive industry. EV platform development and tightening emission norms are pushing OEMs to integrate lightweight composite materials to enhance energy efficiency and structural performance. Key players in the market include Toray Industries, Teijin Limited, SGL Carbon, Mitsubishi Chemical Group, and Hexcel Corporation.

Download Free sample to learn more about this report.

Automotive Carbon Fiber Composites Market Trends

Rising EV Production to Increase the Demand for Lightweight Battery Enclosures and Structural Components

The rapid expansion of electric vehicle production globally is significantly increasing the demand for carbon composite battery enclosures and structural components. Battery packs add substantial weight to EV platforms, requiring lightweight materials to offset mass and extend driving range. Carbon composites offer superior stiffness, crash resistance, and thermal stability, making them suitable for battery protection systems. OEMs are increasingly integrating composite cross-members, underbody shields, and structural reinforcements in EV platforms.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Focus on Vehicle Safety and Crash Performance Optimization to Drive Industry Expansion

Stringent crash safety regulations across North America, Europe, and Asia are encouraging the use of high-performance composite materials, driving automotive carbon fiber composites market growth. Carbon composites provide enhanced energy absorption during impact while reducing vehicle mass. Automakers are leveraging structural CFRP components to improve passenger protection and meet evolving safety ratings. This focus on crash optimization is expanding composite usage beyond cosmetic applications into structural domains.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Limited Large-Scale Production Infrastructure in Emerging Markets to Hamper Product Adoption

The adoption of automotive carbon composites in emerging markets is constrained by limited manufacturing infrastructure. High capital investment requirements for composite processing equipment restrict local production capabilities. The dependence on imported carbon fiber and resins further increases costs. These limitations slow penetration rates in cost-sensitive automotive segments.

MARKET OPPORTUNITIES

Advancements in Resin Transfer Molding (RTM) and Automated Fiber Placement Technologies to Offer New Opportunities

Technological advancements in resin transfer molding and automated fiber placement are reducing production cycle times and improving cost efficiency. These innovations enable higher throughput suitable for mass automotive manufacturing. Automation enhances consistency and material utilization, lowering scrap rates. Such advancements are expected to drive broader composite adoption across mid-segment vehicles.

MARKET CHALLENGES

Recycling and End-of-Life Management Challenges to Impact Industry Progress

Recycling carbon fiber composites remains a significant challenge due to cross-linked resin systems and fiber recovery limitations. End-of-life vehicle regulations are increasing pressure on OEMs to develop circular economy solutions. Mechanical and chemical recycling technologies are still evolving and can be cost-intensive. Addressing sustainability concerns will be critical for long-term market expansion.

Segmentation Analysis

By Carbon Fiber Type

PAN-Based Carbon Fiber Led the Market Due to Balance of Tensile Strength, Modulus, and Cost Efficiency

Based on carbon fiber type, the market is segmented into PAN-based and pitch-based.

The PAN-based carbon fiber segment accounted for the largest share in 2025 and is expected to witness the fastest growth over the forecast period. It offers an optimal balance between tensile strength, modulus, and cost efficiency, making it suitable for structural automotive applications. Increasing EV platform integration further supports its dominance. The expansion of PAN precursor production capacity in Asia is also driving supply scalability.

The pitch-based carbon fiber segment is projected to grow at a moderate pace with a CAGR of 10.6% over the analysis period. It offers very high modulus and thermal conductivity, making it suitable for niche high-performance applications. However, higher costs and brittleness limit widespread automotive adoption.

By Resin Type

Thermoset Segment Dominated in 2025 due to Strong Mechanical Properties

Based on resin type, the market is segmented into thermoset and thermoplastics.

The thermoset segment accounted for the largest share in 2025 due to its strong mechanical properties and established use in structural components. Epoxy-based systems dominate this segment owing to superior bonding characteristics and heat resistance. Automotive OEMs widely use thermosets in RTM and prepreg applications.

The thermoplastics segment represents the fastest growing segment and is set to grow at a CAGR of 20.0% over the forecast period. Their recyclability, faster processing times, and weldability make them suitable for high-volume automotive manufacturing. Growing EV structural integration is accelerating thermoplastic composite adoption.

By Application

Increasing Demand for Lightweight Crash Structures to Bolster Structural Components Segment Growth

By application, the market is segmented into structural components, exterior parts, interior components, powertrain components, and others.

The structural components segment accounted for the largest automotive carbon fiber composites market share in 2025 and is projected to grow at the fastest pace during the forecast period. The increasing demand for lightweight crash structures, battery enclosures, and chassis components drives this segment. Structural integration significantly increases composite volume per vehicle.

The interior components segment is expected to grow modestly with a CAGR of 11.4% over the analysis period, driven by premium aesthetics and lightweight dashboards and seat structures.

The powertrain segment is projected to grow moderately, supported by composite drive shafts and engine covers in performance vehicles.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Passenger Cars Segment Led the Market in 2025 Owing to High Production Volumes

In terms of end-use, the market is categorized into passenger cars, electric vehicles, commercial vehicles, and others.

The passenger cars segment accounted for the largest share in 2025 due to high production volumes globally. Increasing lightweighting requirements and integration in mid-segment vehicles support sustained growth. Premium passenger vehicles remain key adopters of composite structures.

The electric vehicles segment is expected to witness the fastest growth at a CAGR of 19.4% over the analysis period. Battery weight compensation and structural redesign of EV platforms are driving higher composite content per vehicle.

Automotive Carbon Fiber Composites Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive Carbon Fiber Composites Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in 2025 with a valued of USD 0.73 billion. The dominance is driven by China’s dominant EV production and strong automotive manufacturing base. Government support for new energy vehicles and expanding carbon fiber capacity enhance regional growth prospects. Japan and South Korea also contribute through advanced lightweighting technologies.

China Automotive Carbon Fiber Composites Market

The China market is estimated to reach a value of USD 0.47 billion in 2026, accounting for approximately 28.0% of global revenues. China leads regional growth due to its dominant position in global electric vehicle production, accounting for the majority of EV output worldwide. Large-scale battery manufacturing ecosystems and vertically integrated supply chains enable the rapid adoption of carbon composite battery enclosures and structural reinforcements. Additionally, strong government support for new energy vehicles accelerates lightweight material integration across domestic OEM platforms.

To know how our report can help streamline your business, Speak to Analyst

India Automotive Carbon Fiber Composites Market

The India market is estimated to touch a value of around USD 0.07 billion in 2026. India is witnessing gradual adoption driven by supportive government initiatives such as FAME incentives and localization policies promoting EV manufacturing. Rising domestic vehicle production and investments in lightweighting technologies are further encouraging selective integration of carbon composites in structural and semi-structural applications.

North America

North America remains a significant regional market and reached a value of USD 0.28 billion in 2025. North America is expected to grow steadily due to increasing EV pickup development and regulatory standards focused on fuel efficiency improvement. Strong OEM investments in lightweight battery enclosures and structural components are supporting composite integration. The region also benefits from established carbon fiber manufacturing capacity.

U.S. Automotive Carbon Fiber Composites Market

The U.S. market is estimated to reach USD 0.26 billion in 2026, representing approximately 16.0% of global revenues. The U.S. dominates regional demand with large-scale EV platform investments and growing integration of lightweight structural composites in SUVs and pickup trucks.

Europe

The Europe market reached a valuation of USD 0.56 billion in 2025 and is projected to record the modest growth over the forecast period. This expansion is driven by stringent CO₂ emission regulations and strong regulatory pressure for lightweight vehicles. The region benefits from a high concentration of premium automotive manufacturers integrating structural carbon composites into next-generation platforms. Continued innovation in advanced materials further supports steady demand expansion.

Germany Automotive Carbon Fiber Composites Market

The Germany market is projected to reach approximately USD 0.19 billion by 2026, equivalent to around 11.5% of the global market. The country drives regional demand through premium OEM lightweighting initiatives and early adoption of structural CFRP in high-performance and EV platforms.

U.K. Automotive Carbon Fiber Composites Market

The U.K. market is estimated to reach USD 0.07 billion in 2026, accounting for roughly 4.5% of global revenues. The U.K. market supports growth through advanced composite research capabilities and expanding EV production investments.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa markets reached USD 0.07 billion and USD 0.04 billion respectively in 2025. These markets are projected to register moderate growth following Asia Pacific. Improving automotive production, gradual EV adoption, and increasing awareness of lightweight materials are supporting incremental demand. However, limited local composite manufacturing infrastructure moderates growth pace.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansions and Strategic Partnerships to Promote the Growth of Key Market Players

Key players include Toray Industries, Teijin Limited, SGL Carbon, Mitsubishi Chemical Group, and Hexcel Corporation. Companies are focusing on capacity expansion, strategic partnerships with automotive OEMs, and development of cost-efficient thermoplastic composites. Investments in recycling technologies and localized production facilities are strengthening competitive positioning. Collaborations for EV platform integration are emerging as a key strategy.

LIST OF KEY AUTOMOTIVE CARBON COMPOSITE COMPANIES PROFILED

- Toray Industries (Japan)

- Solvay (Belgium)

- Teijin Limited (Japan)

- SGL Carbon (Germany)

- Formosa Plastics Corporation (Taiwan)

- Hexcel Corporation (U.S.)

- Mitsubishi Chemical Group (Japan)

- Hyosung Advanced Materials (South Korea)

- Gurit Holding (Switzerland)

- Jiangsu Hengshen Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Hexcel Corporation announced the expansion of its advanced composite manufacturing facilities in North America to support the growing demand from automotive and electric vehicle sectors. The expansion focuses on increasing carbon fiber and prepreg production capacity, enhancing supply chain resilience, and enabling large-scale delivery of lightweight structural composite solutions. This move strengthens Hexcel’s regional footprint and supports OEMs transitioning toward next-generation EV platforms.

- October 2024: Teijin Limited introduced next-generation thermoplastic carbon fiber composites designed for high-volume automotive production. The development focuses on faster cycle times, improved weldability, and enhanced recyclability, making the material suitable for structural and semi-structural EV components such as battery enclosures and cross-members. The innovation aims to reduce overall production costs while enabling OEMs to scale composite integration across mass-market vehicle platforms.

- January 2024: SGL Carbon partnered with leading European automotive OEMs to supply lightweight structural battery enclosure solutions for next-generation electric vehicle platforms. The collaboration focuses on integrating high-performance carbon composite materials to enhance crash safety, reduce vehicle weight, and improve overall battery protection efficiency.

- July 2023: Toray Industries expanded its carbon fiber production capacity in Asia to address the rising demand from the automotive sector, particularly electric vehicle applications. The expansion aims to strengthen regional supply security and support growing requirements for lightweight structural components and battery enclosure systems.

REPORT COVERAGE

The global automotive carbon fiber composites market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.1% from 2026-2034 |

| Unit | Value (Kilo Tons); Value (USD Billion) |

| Segmentation | By Carbon Fiber Type, Resin Type, Application, End-use, and Region |

| By Carbon Fiber Type |

|

| By Resin Type |

|

| By Application |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.69 billion in 2025 and is projected to reach USD 5.23 billion by 2034.

The market is slated to exhibit a CAGR of 14.1% during the forecast period of 2026-2034.

Based on carbon fiber type, the PAN-based segment led the market in 2025.

By end-use, the electric vehicles segment is expected to experience the fastest growth during the forecast period.

Asia Pacific held the highest market share in 2025.

Increasing focus on vehicle safety and crash performance optimization is a key factor driving the market growth.

Advancements in Resin Transfer Molding (RTM) and automated fiber placement technologies are key opportunities in the market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us