Automotive Constant Velocity Joint Market Size, Share & Industry Analysis, By Joint Type (Ball Type and Tripod Type) By Drive Type (Front Wheel Drive (FWD), Rear Wheel Drive (RWD), and All Wheel Drive (AWD)), By Vehicle Type (Passenger Cars, Commercial Vehicles, and Electric Vehicles), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

AUTOMOTIVE CONSTANT VELOCITY JOINT MARKET SIZE AND FUTURE OUTLOOK

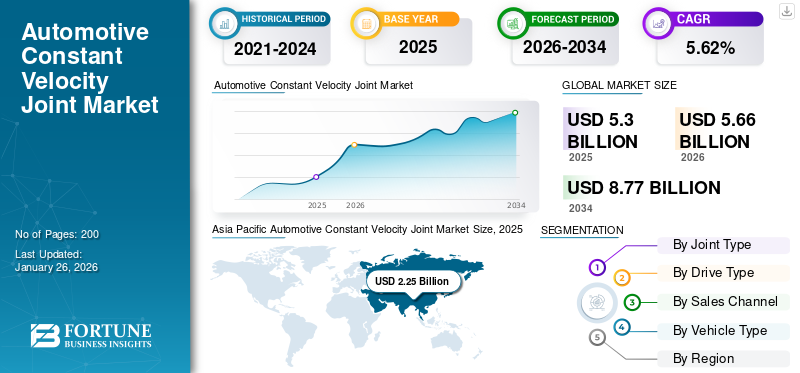

The global automotive constant velocity joint market size was valued at USD 5.30 billion in 2025. The market is projected to grow from USD 5.66 billion in 2026 to USD 8.77 billion in 2034 at a CAGR of 5.62% in the 2026-2034 period. Asia Pacific dominated the global market with a share of 42.44% in 2025.

An automotive Constant Velocity joint (CV joint) is a mechanical component that allows shafts to rotate freely while maintaining a constant velocity, compensating for the angle between them. It is crucial in vehicles, especially those with front-wheel drive, to transmit torque smoothly without friction or vibration. CV joints are typically found at the ends of drive shafts, connecting the transmission to the wheels. They are protected by a rubber boot filled with grease to prevent wear and contamination. Common issues include cracked boots, which can lead to joint failure if not addressed promptly. Regular maintenance is essential to ensure proper function and longevity of these joints.

The global automotive constant velocity joint market is experiencing significant growth due to several factors. The increasing adoption of electric and hybrid vehicles, along with the demand for compact and lightweight CV joints, is driving market expansion. Additionally, the globalization of automotive manufacturing and evolving suspension systems contribute to this growth.

Trends such as the integration of smart sensors for predictive maintenance and the adoption of CV joints in autonomous vehicles are also influential. The market is segmented by joint type, propulsion, application, and end-user, catering to diverse automotive needs. The global automotive constant velocity joint market is led by GKN Automotive, American Axle & Manufacturing, and NTN Corporation, which collectively hold significant market shares. These players specialize in advanced CV joint designs for passenger cars and commercial vehicles, with innovations in lightweight materials and hybrid/electric vehicle compatibility.

The COVID-19 pandemic had a mixed impact on the automotive constant velocity joint market. While supply chain disruptions and reduced vehicle production initially hindered growth, the market has since recovered. Currently, the market is benefiting from increased demand for commercial vehicles and the rising popularity of all-wheel and four-wheel drive systems. Furthermore, advancements in technology, such as the integration of smart sensors, are enhancing market prospects. The focus on environmental sustainability and autonomous vehicle technologies also supports ongoing market growth.

Download Free sample to learn more about this report.

AUTOMOTIVE CONSTANT VELOCITY JOINT MARKET TRENDS

Increasing Demand for Lightweight and High-Performance CV Joints is Ongoing Market Trend

One major ongoing market trend in the global automotive constant velocity joint market growth is the increasing demand for lightweight and high-performance CV joints. This trend is driven by the automotive industry's focus on improving fuel efficiency and reducing emissions. Manufacturers are developing CV joints using advanced materials and technologies, such as high-strength steels and advanced composites, to reduce weight while maintaining durability and performance. The integration of smart sensors for predictive maintenance is also becoming more prevalent, enhancing the efficiency and reliability of CV joints in modern vehicles. Additionally, the growing popularity of electric and hybrid vehicles, which require more efficient drivetrain components, further supports this trend. As the industry moves toward sustainable solutions, the demand for lightweight CV joints is expected to continue, driving innovation and investment in this sector.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Advanced Drivetrain Systems in Passenger and Commercial Vehicles is a Major Driver for Market Expansion

The increasing adoption of advanced drivetrain systems in passenger and commercial vehicles is a significant driver for market expansion in the automotive industry. This trend is fueled by several factors, including stringent government regulations aimed at reducing emissions, consumer demand for enhanced safety and performance, and technological advancements in drivetrain technology.

Governments worldwide are implementing stringent regulations to reduce vehicle emissions. For instance, the European Union aims to cut emissions from new cars by 55% by 2030 compared to 2021 levels as part of the European Green Deal. Similarly, the U.S. has set a goal for 50% of all new vehicle sales to be electric by 2030. These regulatory pressures are compelling automakers to accelerate the development and production of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs), which require advanced drivetrain systems. The shift toward EVs is also supported by government incentives such as tax breaks and subsidies for consumers and manufacturers.

Technological advancements in drivetrain systems are another key driver. Companies such as Allison Transmission have introduced electric axle powertrain systems for electric buses, showcasing the integration of advanced drivetrain technologies in commercial vehicles. Additionally, innovations such as in-wheel motors and e-axles are becoming more prevalent, offering improved efficiency and performance. These advancements enhance vehicle performance and contribute to reduced emissions and improved fuel efficiency, aligning with regulatory requirements and consumer preferences.

Consumer demand for vehicles with enhanced safety features and superior performance is also driving the adoption of advanced drivetrain systems. The integration of All-Wheel Drive (AWD) and Four-Wheel Drive (4WD) systems in passenger vehicles, traditionally associated with off-road and high-performance vehicles, is becoming more common due to their benefits in enhancing vehicle stability and traction. This trend is particularly pronounced in markets such as North America and Europe, where SUVs and crossover vehicles, often equipped with AWD or 4WD, are increasingly popular.

The increasing adoption of advanced drivetrain systems presents significant opportunities for market expansion. As the automotive industry shifts toward electrification and more efficient drivetrain technologies, manufacturers are investing heavily in research and development to maintain their market position. This shift supports the growth of the automotive drivetrain market and fosters innovation in related technologies such as battery systems, electric motors, and power electronics. The integration of smart sensors and predictive maintenance technologies further enhances the efficiency and reliability of these systems, contributing to ongoing market growth.

MARKET RESTRAINTS

Complexity and Challenges Associated with Integrating CV Joints into Modern Drive Train Systems May Restrain Market Growth

The complexity and challenges of integrating electric and hybrid powertrains involve varying torque characteristics, necessitating specialized CV joints designed to handle these conditions. The design constraints of electric and hybrid vehicles, such as compact powertrains and unique suspension setups, further complicate the integration process. Manufacturers must develop innovative solutions to ensure that CV joints can meet the specific performance and durability requirements of these advanced powertrain systems, making this a key challenge in the market.

Another significant restraint is the emergence of hub motors in electric vehicles. Hub motors, which integrate the motor directly into the wheel, potentially reduce the need for traditional drivetrain components such as CV joints. This technological shift could impact the demand for CV joints in the electric vehicle sector, as hub motors simplify the drivetrain by eliminating the need for complex power transmission systems.

Installation issues with CV joints also pose a challenge. The installation process involves multiple factors, including the angle between the input and output shaft, the type of transmission, and the type of drive of the vehicle. Any mistakes during installation can render the CV joint ineffective and harm the vehicle's transmission. Additionally, CV joints are prone to wear during the initial phase of operation due to inadequate lubrication, leading to overheating issues that require careful management.

The susceptibility of CV joints to wear and tear necessitates frequent maintenance compared to other automotive components. This increases the overall maintenance cost for vehicles and affects the reliability and longevity of CV joints, which can be a deterrent for some consumers and manufacturers. As the automotive industry continues to evolve with more efficient and durable technologies, addressing these challenges will be crucial for the sustained growth of the CV joint market.

MARKET OPPORTUNITIES

Integration With Electric and Hybrid Vehicles Finds Major Opportunity for the Market

The transition to Electric and Hybrid Vehicles (EVs/HEVs) represents a critical opportunity for the global automotive Constant Velocity Joint (CV joint) market. EVs require specialized CV joints to handle higher torque loads from electric motors and ensure efficient power transmission, particularly in multi-motor AWD configurations. This demand is amplified by government mandates for emission reductions, such as the EU's 2035 ban on internal combustion engines and China's NEV policy targeting 40% EV sales by 2030.

Manufacturers such as GKN Automotive are using advanced composites and alloys to reduce CV joint weight by 15–20%, improving EV range and efficiency. NTN Corporation has developed CV joints capable of handling up to 30% more torque, addressing the needs of high-performance EVs. SKF integrates IoT-enabled sensors into CV joints for real-time wear monitoring, reducing maintenance costs and downtime. Strict CO₂ emission limits (95g/km by 2025) drive automakers to adopt EVs, directly increasing CV joint demand.

MARKET CHALLENGES

High Production Costs and Material Complexity Creates Hurdle for Market Development

The global automotive constant velocity joint (CV joint) market faces significant challenges due to high production costs and the complexity of integrating advanced materials and designs required for modern vehicles. Manufacturing CV joints demands precision engineering, specialized alloys, and advanced composites to meet durability and performance standards, particularly for electric and hybrid vehicles (EVs/HEVs) that require higher torque tolerance. These materials, such as titanium composites or high-strength steel, increase production expenses. For instance, lightweight CV joints using carbon fiber-reinforced polymers are critical for EV efficiency but remain costly due to limited scalability in production.

EVs require CV joints capable of handling sudden torque spikes from electric motors, necessitating redesigns that add R&D expenditures. For example, GKN Automotive invested heavily in developing e-drive-compatible CV joints for Hyundai's 2023 EV lineup. Companies such as NTN Corporation are automating production lines to reduce labor costs, while SKF focuses on modular designs to streamline assembly. However, smaller manufacturers struggle to compete, exacerbating the market.

SEGMENTATION ANALYSIS

By Joint Type

Widespread Use of Ball-Type Joints in Passenger Vehicles Dominates Market

The market is segmented by joint type into ball type and tripod type.

The ball type segment is projected to dominate the market with a share of 50.70% in 2026. The ball type segment is traditionally dominant due to its widespread use in passenger vehicles, offering smooth power transmission, reduce vibrations, and accommodating angular variations in front-wheel-drive vehicles. Their lightweight design, cost-effectiveness, and compatibility with modern fuel-efficient vehicles drive adoption. Advances in materials enhance durability, while rising demand for fuel-efficient passenger vehicles solidifies their market leadership

The tripod type is gaining traction due to its high torque capacity and compact design, making it suitable for commercial vehicles and heavy-duty applications. The segment is rising in the market because it provides better stability and efficiency in vehicles with high load-bearing capacities. This growth contributes to the overall market expansion by catering to the increasing demand for commercial vehicles and heavy-duty applications. For instance, the global market for commercial vehicles is expected to drive the demand for tripod-type CV joints, as these vehicles require robust power transmission systems.

By Drive Type

Higher Efficiency and Cost-Effective Property Makes Front Wheel Drive Segment Dominate Market

On the basis of drive type, the market segments are Front Wheel Drive (FWD), Rear Wheel Drive (RWD), and All Wheel Drive (AWD).

The FWD segment is expected to lead the market, contributing 50.70% globally in 2026. The Front Wheel Drive (FWD) segment is expected to maintain its dominant position in the market during the forecast period. This is due to its cost efficiency compared to other drive types. It offers benefits such as reduced mass, efficient space utilization, fuel-efficient vehicles, absence of driveshaft friction, and balanced weight distribution for improved traction. Passenger cars worldwide predominantly use FWD systems, which manufacturers prefer due to their lower manufacturing costs, space efficiency, and sporty performance characteristics. The FWD segment is likely to hold 50.67% of the market share in 2025.

Rear Wheel Drive (RWD) systems are commonly found in vehicles such as school buses, minivans, full-size pickups, truck-based SUVs, high-performance cars, luxury vehicles, sedans, and light commercial vehicles. RWD is favored in sports cars and luxury vehicles as it provides better weight balance. Historically, RWD was preferred in early motoring and is effective in handling rear wheels under adverse weather conditions. The growing sales of luxury vehicles and the expansion of the trucking industry are expected to further boost the demand for RWD drivetrain systems in the future.

The All Wheel Drive (AWD) system offers a significant traction advantage by distributing power to all wheels, enhancing stability in dynamic environments, and improving traction on snow and wet roads. The segment is expected to exhibit a CAGR of 6.40% during the forecast period. AWD is commonly used in SUVs, cars, and minivans. With the increasing adoption of electric vehicles and the preference for AWD systems in upcoming vehicles, there is anticipated strong demand for these systems in the future.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Passenger Car Segment Holds Largest Market Share Due to Increasing Urban Population and Commuting Needs

Based on vehicle type, the market is segmented into passenger cars, commercial vehicles, and electric vehicles.

The passenger car segment will account for 68.02% market share in 2026. The market trend is predominantly led by the passenger car segment, which holds the largest automotive constant velocity joint market share. This dominance is attributed to several factors, including rising industrialization, increasing urban populations, and growing commuting needs. Additionally, the presence of a large number of vehicles, rising disposable incomes, and shifting consumer preferences toward advanced vehicles have collectively contributed to the growing market share of passenger cars. Furthermore, improving economic conditions, increased disposable incomes, rapid urbanization, and the expansion of higher-income population segments are driving consumer spending on luxury items, thereby boosting growth in the passenger car segment. The segment is anticipated to acquire 68% of the market share in 2025.

In terms of product choice and revenue, the commercial vehicle segment is experiencing significant growth. Many drivetrain manufacturers catering to medium and Heavy Commercial Vehicles (MCVs and HCVs) are focusing on All-Wheel Drive (AWD) systems for vehicles with higher power capacities. Consequently, the commercial vehicle segment is projected to rise substantially over the forecast period. The increasing adoption of Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs) worldwide is accelerating developments in related components, such as electric drive systems, transmissions, and powertrain units. For example, the European Union's goal to reduce emissions by 55% by 2030 is driving the demand for electric vehicles, which, in turn, boosts the demand for specialized CV joints. This trend is further propelled by concerns over environmental pollution and the low operating costs associated with electric vehicles, which are expected to drive the growth of EV-based drivetrains in the coming years.

The electric vehicles segment is projected to exhibit a CAGR of 10% during the forecast period.

By Sales Channel

Growth and Share of New Vehicle Sales Makes OEM Dominate Market

The market is segmented by sales channel into OEM (Original Equipment Manufacturer) and aftermarket.

The OEM segment is expected to account for 79.68% of the market in 2026. The OEM segment is dominant due to the high volume of new vehicle production. OEM's dominance stems from their ability to provide superior quality CV joints that meet stringent manufacturing standards. Additionally, the rising production of electric and hybrid vehicles, coupled with the growing demand for lightweight and fuel-efficient components, further strengthens OEMs' market position. The segment is likely to capture 80.27% of the market share in 2025.

The aftermarket segment is growing rapidly as consumers seek durable and affordable replacement parts for older vehicles. The growth of the aftermarket segment is driven by the increasing average age of vehicles, particularly in regions such as North America and Europe. This growth contributes to the overall market by providing additional revenue streams for manufacturers and suppliers. For example, the demand for aftermarket CV joints market is expected to rise as the global SUV market expands, leading to more vehicles requiring maintenance and replacement parts. The segment is expected to record a CAGR of 9.10% of the market share in 2025.

AUTOMOTIVE CONSTANT VELOCITY MARKET REGIONAL OUTLOOK

Based on geography, the market is studied across Asia Pacific, Europe, North America, and the rest of the world.

Asia Pacific Automotive Constant Velocity Joint Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific region is poised to emerge as the fastest-growing and dominant region in the global market. In 2025, the Asia Pacific market stood at USD 2.25 billion, representing 42.44% of global demand, and is projected to grow to USD 2.41 billion in 2026. Key factors driving this growth include the presence of major automotive manufacturers, a robust supply chain, and supportive government policies. The region's high population and economically strong countries, such as China and India, which account for over 45% of the global population, are expected to boost market expansion further.

Additionally, favorable government measures aimed at reviving the auto industry post-COVID-19 have enhanced growth prospects. The rising sales of All-Wheel Drive (AWD) vehicles, along with anticipated growth in Electric Vehicles (EVs) and Internal Combustion Engine (ICE) vehicle sales in South Asia, are also driving market expansion. High urbanization and the development of smart cities are anticipated to propel the automotive market growth in this region. The market value in China is expected to be USD 1.31 billion in 2026.

On the other hand, Japan is projecting to hit USD 0.29 billion and India is likely to hold USD 0.23 billion in 2026.

Europe

Europe contributed approximately USD 1.48 billion to the global market in 2025, accounting for 27.87% share, and is expected to reach USD 1.58 billion in 2026. Europe holds the second-highest position in the market, with Germany serving as a primary hub for major auto manufacturers. Europe is anticipated to account for the second-highest market size of USD 1.48 billion in 2025, exhibiting the second-fastest growing CAGR of 6% during the forecast period. The region is known for being an early adopter of new trends and technologies, with Germany ranking as the second-largest manufacturing hub for auto parts globally. The rapid adoption of electric vehicles in Norway, Germany, the U.K., and the Netherlands is contributing to market growth in Europe. The market value in U.K. is expected to be USD 0.25 billion in 2026.

On the other hand, Germany is projecting to hit USD 0.45 billion in 2026. and France is likely to hold USD 0.19 billion in 2025.

North America

The market in North America reached USD 1.22 billion in 2025, representing 23.09% of total market revenue, and is projected to reach USD 1.3 billion in 2026. driven by rising vehicle sales and increasing consumer preference for comfortable driving experiences and pollution-free commuting. Regional government initiatives focused on developing automotive components are expected to support and promote manufacturing capabilities, contributing to market growth.

The U.S. automotive constant velocity (CV) joint market is experiencing steady growth, driven by rising demand for All-Wheel-Drive (AWD) and Four-Wheel-Drive (4WD) vehicles, especially SUVs and trucks, which require robust CV joints for optimal power transmission and handling. The market is also benefiting from increased sales of commercial vehicles, with U.S. truck sales rising by 3.8% in 2022. Innovations such as lightweight materials, advanced lubrication, and smart sensors for predictive maintenance are further enhancing product performance and longevity. The U.S. market size is estimated to be USD 0.81 billion in 2026.

The rest of the world is projected to be fourth-largest region with a size of USD 0.35 billion in 2025. The rest of the world, comprising Latin America and the Middle East & Africa, is also expected to contribute significantly to market growth. The Middle East, in particular, is projected to drive growth due to rising imports and increasing luxury vehicle sales in the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Investing in Advanced Technologies to Create Comprehensive Product Portfolio Makes GKN Automotive Limited Leading Player

GKN Automotive Limited is the leading player in the global automotive constant velocity joint market. GKN's dominance is attributed to its extensive product portfolio, which includes a wide range of constant velocity joints tailored for various vehicle types and applications. The company's expertise in designing and manufacturing high-performance CV joints for both passenger and commercial vehicles has earned it a significant market share. GKN's products are known for their durability and efficiency, making them a preferred choice among major automotive manufacturers. Additionally, GKN's strong global presence and strategic partnerships with key automotive companies further solidify its position as a market leader.

NTN Corporation is the second leading player in the global market. NTN's success is driven by its innovative product offerings and strong manufacturing capabilities. The company specializes in producing high-quality CV joints that meet the evolving demands of the automotive industry, particularly in the areas of fuel efficiency and vehicle performance. NTN's global reach and strategic partnerships with automotive manufacturers also contribute to its market position. NTN holds a significant market share, with key players such as GKN and American Axle & Manufacturing also holding substantial shares. NTN's commitment to technological advancements and customer satisfaction has helped maintain its position as a key player in the market. SKF AB, and IFA Group are among the players in the market.

LIST OF KEY AUTOMOTIVE CONSTANT VELOCITY JOINT COMPANIES:

- GKN Automotive (U.K.)

- American Axle & Manufacturing, Inc. (U.S.)

- NTN Corporation (Japan)

- Hyundai WIA Corporation (South Korea)

- SKF AB (Sweden)

- Neapco Holdings LLC (U.S.)

- Nexteer Automotive Group Limited (U.S.)

- Dana Incorporated (U.S.)

- IFA Group (Germany)

- JTEKT Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

September 2024: SKF launched a new master kit and in-house CV joints. It will manufacture CV joints and driveshafts, the critical components that connect the wheel bearing to the power transmission, in-house at SKF's Italian OE Airasca facility.

September 2024: NTN Corporation introduced an advanced constant velocity joint that improves both durability and noise reduction in automotive drivetrains.

April 2024: Hyundai WIA gets a grant for a constant velocity joint for a vehicle with an improved sealing mechanism. The joint includes a hub housing, bearing assembly, power transmission member, and boot with a unique design to prevent foreign substances from entering the bearing assembly.

December 2023: Hyundai and Kia unveiled an integrated wheel drive system for EVs. The new concept moves drive components inside the wheel hub to optimize interior space in electric vehicles. Uni Wheel is a functionally integrated wheel drive system that improves available space inside an Electric Vehicle (EV) by moving the main drive system components to the vacant space within the wheel hub.

February 2023: Borg & Beck launched an extensive range of premium-quality Constant Velocity (CV) joints and driveshafts. With more than 420 CV joints and over 530 driveshafts available as part, it created access to distributors and created a comprehensive solution. All Borg & Beck CV Joints and Driveshafts are manufactured and optimized for robust application. Using premium quality materials, they are precision machined and balanced to ensure a smooth, vibration-free performance.

REPORT COVERAGE

The global market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, types, and leading product applications. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, it encompasses several factors that have contributed to the market's growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.62% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Joint Type

|

|

By Drive Type

|

|

|

By Vehicle Type

|

|

|

By Sales Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.30 billion in 2025. The market is projected to record a valuation of USD 8.77 billion by 2034.

In 2025, Asia Pacific stood at USD 2.25 billion.

The market is projected to grow at a CAGR of 5.62% and will exhibit steady growth during the forecast period of 2026-2034.

Passenger car is the leading segment in the global market.

The increase in automotive sales, growing urbanization, and rising demand for safety & comfort, along with high-powered engines, have propelled the demand for new vehicles, which drives the market growth.

GKN Automotive is a major player in the global market.

Asia Pacific is likely to dominate the market share in 2025.

Increasing adoption of advanced drivetrain systems in passenger & commercial vehicles is a major driver for market expansion.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us