Automotive Data Monetization Platforms Market Size, Share & Industry Analysis, By Platform Type (Vehicle Data Monetization Platforms, Fleet Data Monetization Platforms, and Others), By Application (Usage-Based Insurance (UBI), Traffic & Navigation Services, and Others), By Deployment Model (Cloud-based Platforms and On-premise Platforms), By End User (Automotive OEMs, Fleet Operators & Logistics Companies, Insurance Companies, and Others), By Data Type Monetized (Telematics Data, Driver Behavior Data, Vehicle Health & Diagnostics Data, and Others), and Regional Forecast, 2026–2034

Automotive Data Monetization Platforms Market Size and Future Outlook

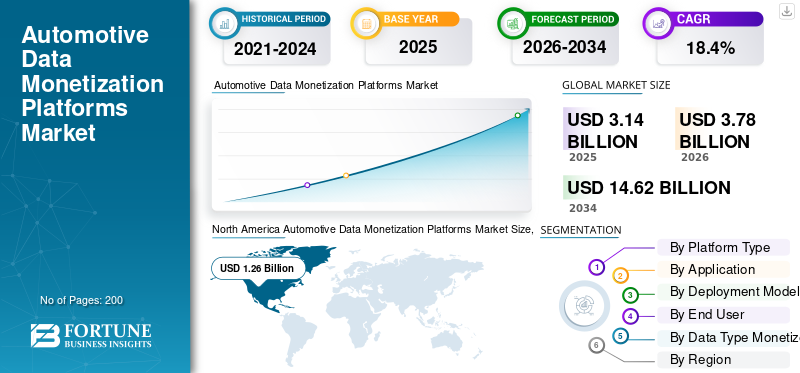

The global automotive data monetization platforms market size was valued at USD 3.14 billion in 2025. The market is projected to grow from USD 3.78 billion in 2026 to USD 14.62 billion by 2034, exhibiting a CAGR of 18.4% during the forecast period. North America dominated the automotive data monetization platforms market with a market share of 40.12% in 2025.

Automotive data monetization platforms are digital systems that collect, process, and analyze vehicle-generated data to create revenue streams through services such as insurance, fleet management, predictive maintenance, and in-vehicle applications. Market growth is driven by rising connected vehicles, increasing demand for data-driven services, advancements in AI and cloud technologies, growing adoption of usage-based insurance, and OEM focus on new digital revenue streams.

Major players in the market include Microsoft Corporation, Amazon Web Services (AWS), IBM Corporation, Bosch Mobility Solutions, and Verizon Communications Inc., competing through cloud platforms, AI-driven analytics, strategic partnerships, and scalable data monetization solutions.

Download Free sample to learn more about this report.

Automotive Data Monetization Platforms Market Key Takeaways

- 2025 Market Size: USD 3.14 billion

- 2026 Market Size: USD 3.78 billion

- 2034 Forecast Market Size: USD 14.62 billion

- CAGR: 18.4% from 2026–2034

- North America dominated the automotive data monetization platforms market with a 40.12% share in 2025.

- Telematics Data segment held the largest market share in 2025.

- Usage-Based Insurance (UBI) segment held the largest market share in 2025.

North America

North America held 40.12% share in 2025, valued at USD 1.26 billion.

Asia Pacific

Asia Pacific is projected to grow at the highest CAGR of 20.4% during the forecast period.

Europe

Europe held the second-largest market share in 2025.

U.S.

Market projected to reach USD 1.26 billion by 2026.

Japan

Market projected to reach USD 0.08 billion by 2026.

Read More

AUTOMOTIVE DATA MONETIZATION PLATFORMS MARKET TRENDS

Rising Connected Vehicle Ecosystem Accelerates Data Monetization Adoption

The rapid expansion of connected vehicles globally is significantly shaping the market trends. Modern vehicles are increasingly equipped with sensors, telematics, and embedded software that continuously generate large volumes of data. This transformation is enabling automakers and technology providers to monetize data through value-added services such as remote diagnostics, driver insights, advanced driver assistance systems, and personalized mobility solutions. As connectivity becomes a standard feature across vehicle segments, the ecosystem for data monetization platforms is expanding, supporting long-term market growth and innovation.

- In May 2024, Hyundai expanded its Bluelink connected car platform across Europe, offering features such as OTA updates, in-car payments, and real-time navigation, enhancing personalized mobility experiences and enabling new data monetization opportunities through digital services.

Integration of AI and Advanced Analytics Enhances Platform Capabilities

The growing integration of artificial intelligence and advanced analytics is redefining the capabilities of automotive data monetization platforms. AI-driven tools enable real-time processing of complex vehicle data, allowing stakeholders to generate actionable insights and predictive models. These technologies support applications such as predictive maintenance, usage-based insurance, usage patterns, and traffic optimization. As machine learning algorithms continue to evolve, platform providers are focusing on improving accuracy, scalability, and automation, making data monetization more efficient and commercially viable across multiple automotive use cases.

- In April 2026, Dataforce launched Ask Dataforce, an AI-powered platform enabling automotive professionals to access real-time vehicle registration data via chat, enhancing data accessibility, analytics efficiency, and supporting advanced automotive data monetization and decision-making processes.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Usage-Based Insurance and Personalized Services Drives Market Growth

The increasing adoption of usage-based insurance (UBI) and personalized mobility services is a major driver for the market. Insurers are leveraging real-time driving data to offer customized premiums based on driver behavior, while automotive companies are using data insights to enhance user experience. This shift toward personalization is encouraging stakeholders to invest in robust data monetization platforms. As consumers demand more tailored services and cost-efficient solutions, the reliance on vehicle data continues to increase, fueling sustained market demand.

- In November 2022, Mobilize Financial Services partnered with Accenture to launch a usage-based insurance platform in Europe, enabling personalized “pay-as-you-drive” models using connected vehicle data, enhancing customer experience, and supporting automotive data monetization strategies.

Automotive OEMs Shift Toward Data-Driven Revenue Models, Boosting Market Growth

Automotive OEMs are increasingly transitioning from traditional vehicle sales and business models to data-driven and service-oriented business strategies. By leveraging vehicle-generated data, OEMs can unlock recurring revenue streams through subscriptions, digital services, and partnerships with third-party providers. This strategic shift is driving investments in data monetization platforms, enabling companies to capitalize on connected vehicle ecosystems. As competition intensifies and margins on vehicle sales narrow, data monetization is becoming a critical growth lever for automakers globally.

- In November 2025, HERE Technologies introduced an industry-first Software-Defined Vehicle maturity framework, enabling automakers to benchmark progress, enhance data monetization strategies, and transition toward software-driven mobility ecosystems with new revenue streams.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Limit Data Utilization Potential

Strict data privacy and protection regulations across regions pose a significant restraint on the automotive data monetization platforms market growth. Regulations such as GDPR and other regional data laws restrict how vehicle and user data can be collected, stored, and monetized. Compliance requirements increase operational complexity and limit the extent of data usage for commercial purposes. Additionally, concerns regarding data ownership and user consent further hinder seamless platform deployment, slowing down the overall pace of market expansion.

MARKET OPPORTUNITIES

Expansion of Smart Cities and Mobility Ecosystems Creates New Revenue Streams

The development of smart cities and integrated mobility ecosystems presents significant opportunities for automotive data monetization platforms. Vehicle data can be leveraged to optimize traffic flow, enhance urban planning, and improve public transportation systems. Collaboration between automotive companies, governments, and technology providers is opening new avenues for data-driven services. As urban mobility becomes increasingly digitized, the demand for platforms that can efficiently manage and monetize transportation data is expected to rise substantially.

- In September 2025, Hyundai Motor Group launched the Next Urban Mobility Alliance (NUMA), a public-private initiative leveraging AI and autonomous technologies to build smart city mobility ecosystems and accelerate data-driven automotive monetization opportunities.

Emergence of Mobility-as-a-Service (MaaS) Platforms Unlocks Data Monetization Potential

The rapid growth of mobility as a service (MaaS) is creating new opportunities for data monetization in the automotive sector. MaaS platforms rely heavily on real-time vehicle and user data to deliver seamless, on-demand mobility solutions. This generates valuable datasets that can be monetized through route optimization, pricing strategies, and user and driving behavior analysis. As shared mobility gains traction globally, automotive data monetization platforms are becoming essential for enabling efficient and scalable MaaS operations.

- In February 2023, Indra developed a multi-city Mobility-as-a-Service (MaaS) platform across six Spanish cities, integrating real-time transport data into a single application to enhance urban mobility, digitalization, and data-driven transportation monetization strategies.

MARKET CHALLENGES

Interoperability Issues Across Diverse Vehicle and Data Systems Hinder Scalability

A major challenge in the market is the lack of standardization and interoperability across different vehicle platforms and data systems. Automotive data is generated in various formats and structures, making integration across OEMs, service providers, and regions complex. This fragmentation limits seamless data exchange and reduces the efficiency of monetization strategies. Overcoming these technical barriers requires industry-wide collaboration and the development of standardized frameworks, which remains a slow and resource-intensive process.

Segmentation Analysis

By Data Type Monetized

High Volume of Real-Time Vehicle Insights Sustains Telematics Data Segment Demand

Based on data type monetized, the market is segmented into telematics data, driver behavior data, vehicle health & diagnostics data, and location & mobility data.

The telematics data segment dominates the market due to its extensive use in connected cars for real-time data transmission, fleet tracking, and remote diagnostics. OEMs, insurers, and fleet operators rely heavily on telematics for operational efficiency, safety monitoring, and service optimization. Its widespread integration across passenger and commercial vehicles, along with compatibility with cloud and IoT platforms, ensures continuous data generation and monetization opportunities, thereby sustaining strong demand.

- In February 2026, LG Electronics unveiled a next-generation smart telematics solution integrating TCU and antenna modules, enhancing in-vehicle connectivity, real-time data processing, and enabling advanced automotive data monetization and AI-driven mobility ecosystems.

The location & mobility data segment is projected to grow at a CAGR of 20.3% over the forecast period. Increasing adoption of navigation services, smart mobility solutions, and MaaS platforms drives demand for real-time location insights, enabling traffic optimization, route planning, and urban mobility management.

By Application

Widespread Insurance Adoption and Risk-Based Pricing Boost Usage-Based Insurance Segment Demand

By application, the market is segmented into usage-based insurance (UBI), predictive maintenance, traffic & navigation services, in-vehicle advertising, and others.

The usage-based insurance (UBI) segment holds the largest automotive data monetization platforms market share due to increasing demand for personalized and cost-efficient insurance models. Insurers leverage real-time driving data to assess risk accurately and offer customized premiums, improving customer retention and profitability. Growing consumer awareness, regulatory support for telematics-based policies, and integration with connected vehicle platforms are further strengthening adoption, making UBI a key revenue-generating application in automotive data monetization.

- In August 2022, India officially approved usage-based insurance, enabling insurers to offer pay-as-you-drive and behavior-based policies, leveraging vehicle and smartphone data to improve affordability, increase insurance penetration, and promote safer driving practices.

The in-vehicle advertising segment is expected to grow at a CAGR of 20.2% over the forecast period. Rising demand for the data monetization market is segmented into personalized, location-based advertisements, and increasing screen integration within vehicles, which are enabling new revenue streams for OEMs and digital advertisers.

To know how our report can help streamline your business, Speak to Analyst

By Platform Type

Extensive OEM Integration and Continuous Data Generation Strengthen Vehicle Data Monetization Platforms' Dominance

By platform type, the market is segmented into vehicle data monetization platforms, fleet data monetization platforms, and mobility-as-a-service (MaaS) data platforms.

The vehicle data monetization platforms segment dominates the market due to its direct integration with connected vehicles and OEM ecosystems. These platforms enable continuous collection and analysis of real-time vehicle data, supporting multiple revenue streams such as insurance, diagnostics, and in-vehicle services. Strong OEM partnerships, increasing penetration of software defined vehicles, and large-scale deployment across passenger vehicles ensure sustained data flow, reinforcing long-term market demand and platform scalability.

- In November 2025, Toyota filed a patent for a system that compensates drivers for sharing valuable vehicle data, enabling AI training for autonomous driving and enhancing transparency in automotive data monetization practices.

The mobility-as-a-service (MaaS) data platforms segment is projected to grow at a CAGR of 19.9% over the forecast period. Rising adoption of shared mobility, ride-hailing, and integrated transport solutions is driving demand for real-time data platforms that optimize routes, pricing, and user experience.

By Deployment Model

Scalable Infrastructure and Real-Time Data Processing Capabilities Drive Cloud-based Platforms Growth

By deployment model, the market is bifurcated into cloud-based platforms and on-premise platforms.

The cloud-based platforms segment dominates the market of automotive data monetization platforms, and is also the fastest growing due to its scalability, flexibility, and ability to process large volumes of real-time vehicle data. These platforms enable seamless integration with connected vehicles, AI tools, and analytics systems, supporting diverse monetization use cases. Lower upfront costs, faster deployment, and continuous updates make cloud solutions highly attractive for OEMs and service providers, thereby accelerating adoption and sustaining strong market demand.

- In January 2026, Qualcomm and Google introduced Snapdragon vSoC on Google Cloud, enabling automakers to develop, test, and deploy software-defined vehicle applications in the cloud, accelerating innovation and supporting continuous automotive data monetization services.

The on-premise platforms segment is projected to grow at a CAGR of 16.2% over the forecast period. Demand is driven by organizations requiring greater data control, enhanced security, and compliance with strict regulatory frameworks, particularly in sensitive markets and enterprise applications.

By End User

Strong Control Over Vehicle Data and Ecosystem Integration Boost Automotive OEMs' Segment Dominance

By end user, the market is segmented into automotive OEMs, fleet operators & logistics companies, insurance companies, and mobility service providers.

The automotive OEMs segment is estimated to be leading the automotive data monetization market size, as manufacturers increasingly leverage vehicle-generated data to develop new digital revenue streams and enhance customer experience. OEMs have direct access to embedded vehicle systems, enabling seamless data collection, platform integration, and service deployment. Their strong control over connected ecosystems, combined with investments in software-defined vehicles and partnerships with technology firms, supports continuous data monetization and strengthens long-term market positioning.

- In October 2025, Volkswagen partnered with Nuvei to launch a payment solution for connected vehicles in Brazil, enabling subscription-based services and seamless in-car payments, supporting automotive data monetization through integrated digital service ecosystems.

The mobility service providers segment is expected to grow at a CAGR of 21.7% over the forecast period. Rapid expansion of ride-hailing, car-sharing, and MaaS platforms is driving demand for real-time data insights to optimize operations, pricing, and user experience.

Automotive Data Monetization Platforms Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa

Asia Pacific

North America Automotive Data Monetization Platforms Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the fastest-growing region with a CAGR of 20.4% during the forecast period, driven by the rapid expansion of connected vehicles and digital mobility services. Countries such as China, Japan, and India are witnessing strong growth in vehicle production and the adoption of telematics solutions. Increasing investments in smart city projects, 5G infrastructure, and mobility platforms are accelerating demand for data monetization solutions. Additionally, the rise of ride-hailing, fleet data management, and digital ecosystems is creating significant opportunities for platform providers in the region.

- In April 2024, Marelli introduced ProConnect, an integrated cockpit and 5G telematics platform combining infotainment, cluster, and connectivity functions, enabling enhanced in-vehicle data processing, cost efficiency, and supporting advanced automotive data monetization capabilities.

China Automotive Data Monetization Platforms Market

The Chinese market in 2026 is estimated to be USD 0.63 billion, accounting for roughly 16.7% of global revenues. Strong connected vehicle adoption, smart city initiatives, and OEM-tech collaborations drive dominance.

Japan Automotive Data Monetization Platforms Market

The Japanese market in 2026 is estimated to be USD 0.08 billion, accounting for roughly 2.0% of global revenues. Advanced automotive technologies, telematics integration, and a focus on mobility innovation support steady growth.

India Automotive Data Monetization Platforms Market

The Indian market in 2026 is estimated to be USD 0.09 billion, accounting for roughly 2.3% of global revenues. Rapid digitalization, growing connected vehicles, and expanding mobility services drive the fastest growth.

North America

North America dominates the market due to the early adoption of connected vehicle technologies and the strong presence of leading technology providers such as AWS, Microsoft, and Verizon. The region benefits from advanced digital infrastructure, high penetration of telematics, and strong collaboration between OEMs and data analytics firms. Additionally, growing demand for usage-based insurance and in-vehicle digital services is accelerating platform adoption. Continuous investments in AI, cloud computing, and smart mobility solutions further strengthen regional market growth.

- In January 2026, AUMOVIO partnered with AWS to accelerate autonomous vehicle development using AI and cloud platforms, enabling faster data processing, improved safety validation, and enhanced automotive data monetization through scalable, data-driven mobility solutions.

U.S. Automotive Data Monetization Platforms Market

The U.S. market in 2026 is estimated to be USD 1.26 billion, accounting for roughly 33.3% of global revenues. Strong tech ecosystem, high connected vehicle penetration, and cloud adoption fuel leadership.

Europe

Europe holds the second largest market share, driven by stringent regulatory frameworks and a strong focus on data privacy and vehicle safety. The region’s well-established automotive industry, led by major OEMs, is actively investing in data monetization strategies and connected vehicle ecosystems. Increasing adoption of telematics-based insurance, predictive maintenance, and smart mobility solutions is supporting market expansion. Furthermore, government initiatives promoting digital transformation and sustainable mobility are encouraging integration of advanced data platforms across automotive value chains.

- In April 2026, BMW Group adopted PTC’s Codebeamer platform to unify requirements management and enable AI-driven digital engineering, enhancing data integration, collaboration, and supporting advanced automotive data monetization and software-defined vehicle development.

Germany Automotive Data Monetization Platforms Market

The Germany market in 2026 is estimated to be USD 0.21 billion, accounting for roughly 5.6% of global revenues. Strong OEM presence, regulatory frameworks, and focus on connected mobility solutions support growth.

U.K. Automotive Data Monetization Platforms Market

The U.K. market in 2026 is estimated to be USD 0.16 billion, accounting for roughly 14.1% of global revenues. Increasing telematics adoption, insurance innovations, and digital mobility ecosystems drive market expansion.

South America

South America is experiencing gradual market growth, supported by increasing adoption of connected vehicle technologies and telematics solutions, particularly in Brazil and Argentina. The expansion of fleet management and logistics sectors is driving demand for data-driven insights and operational efficiency. Although infrastructure challenges and regulatory gaps exist, rising investments in digital platforms and growing awareness of data monetization benefits are encouraging market development. The region is expected to witness steady growth as connectivity and mobility ecosystems continue to evolve.

- In June 2025, Ford South America partnered with RELEX Solutions to implement an AI-driven supply chain platform, enhancing forecasting accuracy, inventory optimization, and operational efficiency across multiple countries, supporting data-driven decision-making in automotive ecosystems.

The Middle East & Africa

The Middle East & Africa represent the fourth largest market, driven by increasing digital transformation initiatives and smart mobility projects in countries such as the UAE and Saudi Arabia. Growing investments in smart cities, connected infrastructure, and advanced transportation systems are supporting the adoption of automotive data platforms. Additionally, the expansion of fleet and logistics operations is creating demand for real-time data analytics. While adoption is still developing, improving connectivity and government-led initiatives are expected to drive sustained market growth.

- In July 2025, AutoData Middle East launched an AI-powered intelligence suite featuring valuation, risk assessment, claims, and dealership tools, enhancing data-driven decision-making, pricing accuracy, and operational efficiency across automotive insurance and used car markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Cloud Integration, AI Analytics, and Ecosystem Partnerships Define Competitive Landscape

The market is moderately consolidated, with major technology and automotive players competing alongside emerging data platform providers. Key companies such as Microsoft, AWS, IBM, Bosch, and Verizon compete through scalable cloud infrastructure, AI-driven analytics, and secure data monetization capabilities. To gain a competitive edge, firms are focusing on platform interoperability, real-time data processing, and strategic partnerships with OEMs, insurers, and mobility providers. Investments in cybersecurity, edge computing, and SaaS-based models further intensify competition.

- In May 2025, Sigma partnered with Snowflake to deliver AI-powered automotive data cloud solutions, enabling real-time analytics, unified data integration, and new revenue opportunities through advanced automotive data monetization platforms.

LIST OF KEY AUTOMOTIVE DATA MONETIZATION PLATFORMS COMPANIES PROFILED

- Microsoft Corporation (U.S.)

- Amazon Web Services (AWS) (U.S.)

- IBM Corporation (U.S.)

- Bosch Mobility Solutions (Germany)

- Verizon Communications Inc. (U.S.)

- Google LLC (U.S.)

- SAP SE (Germany)

- Oracle Corporation (U.S.)

- Continental AG (Germany)

- Harman International (Samsung Electronics) (U.S.)

- T-Systems International GmbH (Germany)

- Geotab Inc. (Canada)

- Otonomo Technologies Ltd. (Israel)

- Wejo Group Limited (U.K)

- HERE Technologies (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Nissan launched Nissan Deals in Europe, an in-car app delivering real-time, location-based offers using vehicle data insights, enhancing personalized driver experiences and enabling new automotive data monetization opportunities through connected services.

- March 2026: LiveRamp introduced agentic AI upgrades enabling automated data collaboration, audience targeting, and performance measurement, enhancing data-driven decision-making and supporting scalable automotive data monetization and marketing ecosystem optimization.

- December 2025: AWS introduced advanced AI, cloud, and data solutions for automotive applications, enabling large-scale vehicle data processing, software-defined vehicle development, and enhanced data monetization through connected mobility and autonomous driving innovations.

- October 2025: BillingPlatform launched an AI Monetization solution enabling real-time usage-based billing, dynamic pricing, and scalable revenue models, helping companies efficiently monetize AI-driven services and manage high-volume data transactions across global markets.

- October 2025: Oracle launched its AI Data Platform, enabling unified data integration, real-time analytics, and AI-driven automation, helping automotive and enterprise users accelerate innovation and unlock new data monetization opportunities.

- August 2025: Izmo Ltd. launched its Automotive AI Factory to develop AI-driven solutions for dealerships and OEMs, enabling data integration, predictive analytics, and new recurring revenue streams through advanced automotive data monetization platforms.

- July 2025: Bosch Ventures invested in 4screen’s driver interaction platform, enabling real-time, data-driven in-car advertising and engagement, helping automakers unlock new revenue streams through scalable automotive data monetization solutions.

- June 2023: Sonatus introduced Automator, enabling OEMs to deploy vehicle functions, diagnostics, and personalized features without full software cycles, supporting lifecycle innovation and expanding automotive data monetization through software-defined vehicle capabilities.

REPORT COVERAGE

The global automotive data monetization platforms market analysis provides an in-depth study of the market size & forecast by all the market segments included in the automotive data monetization platforms market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.4% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Data Type Monetized, By Application, By Platform Type, By Deployment Model, By End User, and By Region |

| By Data Type Monetized |

|

| By Application |

|

| By Platform Type |

|

| By Deployment Model |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights에 따르면 글로벌 시장 가치는 2025년에 31억 4천만 달러였으며 2034년에는 146억 2천만 달러에 이를 것으로 예상됩니다.

2025년 북미 시장 가치는 12억 6천만 달러에 이르렀습니다.

시장은 예측 기간 동안 18.4%의 CAGR을 보일 것으로 예상됩니다.

텔레매틱스 데이터 부문은 수익화되는 데이터 유형별로 시장을 선도하고 있습니다.

사용량 기반 보험 및 맞춤형 서비스에 대한 수요가 증가함에 따라 도입이 촉진되고 있습니다.

Microsoft, AWS, IBM, Bosch, Verizon 등 주요 기업이 시장을 선도하고 있습니다.

북미는 시장에서 가장 큰 점유율을 차지하고 있습니다.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us