Automotive Digital Instrument Cluster Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUV, LCV and HCV), By Type (Semi-Digital & Hybrid and Fully Digital), By Display Size (<7 inches, 7-9 inches, 10-12 inches and >12 inches), By Display Technology (TFT-LCD and OLED), By Propulsion (ICE and Electric), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

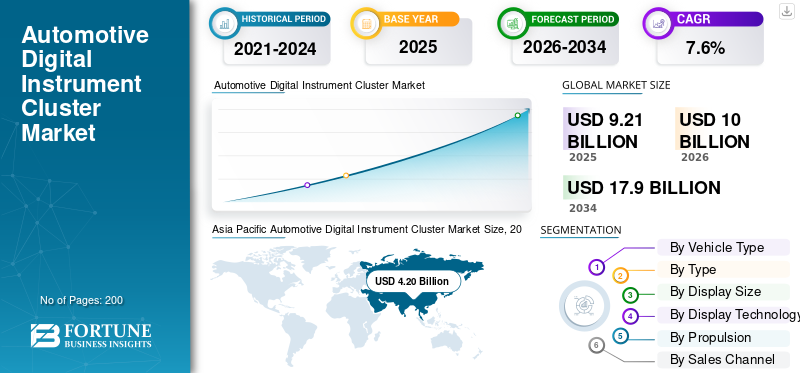

The automotive digital instrument cluster market size was valued at USD 9.21 billion in 2025. The market is projected to grow from USD 10.00 billion in 2026 to USD 17.90 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period. Asia Pacific dominated the global market with a market share of 45.60% in 2025.

The Automotive Digital Instrument Cluster Market represents the systems used to display real-time vehicle information such as speed, fuel level, navigation alerts, warnings, and driver assistance data through digital screens. These clusters replace or complement analog gauges and are now widely integrated across passenger cars and two-wheelers, supporting safer and more intuitive driving experiences.

Market expansion is strongly linked to the shift toward vehicle digitization and the need for an improved vehicle interface. Automakers increasingly deploy digital clusters to integrate navigation, connectivity, and advanced driver assistance systems ADAS alerts within the driver’s direct line of sight. This improves safety while reducing distraction. Growing adoption of electric vehicles EVs further accelerates demand, as EVs require detailed energy-use displays and system diagnostics.

Another key growth parameter is the rising focus on lightweight vehicles and improving fuel efficiency, which is influencing interior and dashboard design choices. Automakers are also exploring the use of lightweight materials, including carbon fiber, alongside digital clusters to reduce dashboard mass and support next-generation lightweight vehicle architectures. As automakers work to lower production costs, scalable display platforms help deliver advanced features at a cost-effective level, especially in mid-segment vehicles.

Over the forecast period, the market is expected to expand steadily, and it is projected to benefit from rising digitalization, ADAS integration, and broader adoption across vehicle segments. Increasing demand for lightweight components, stronger localization of supply chains, and continuous software upgrades will shape long-term adoption. Overall, the market is expected to expand as digital clusters become standard equipment across vehicle categories, supporting connectivity, efficiency, and safety in modern mobility.

Download Free sample to learn more about this report.

Automotive Digital Instrument Cluster Market KEY TAKEAWAYS

- 2025 Market Size: USD 9.21 billion

- 2026 Market Size: USD 10.00 billion

- 2034 Forecast Market Size: USD 17.90 billion

- CAGR: 7.6% from 2026–2034

- Asia Pacific dominated the market with a 45.60% share in 2025.

- HCV segment is projected to grow at a CAGR of 10.0%.

- Fully Digital segment is projected to grow at a CAGR of 11.3%.

Asia Pacific

Asia Pacific USD 3.90 billion in 2024. High vehicle production, rapid tech adoption, and strong electronics manufacturing driving dominance.

Europe

Europe USD 2.11 billion in 2025. Growth driven by strict safety regulations and rising use of digital driver display systems.

North America

North America USD 1.90 billion in 2025. Steady adoption in SUVs and passenger cars supported by OEM presence and ADAS integration.

U.S.

U.S. USD 1.43 billion in 2025. Strong adoption in SUVs and luxury vehicles with increasing ADAS and infotainment integration.

China

China USD 2.31 billion in 2025. Strong passenger vehicle production, rapid digital cockpit adoption, and robust domestic electronics manufacturing driving market leadership.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Integration of Driver Assistance Features Accelerates Digital Cluster Adoption

The growing deployment of advanced driver assistance systems (ADAS) is a major driver of the automotive digital instrument cluster market growth. Digital instrument clusters provide a central display for warnings, navigation cues, and safety alerts. As vehicles adopt more ADAS features, digital clusters become essential for presenting real-time information clearly, improving driver awareness, and supporting safer driving outcomes.

- For instance, in March 2024, Bosch Mobility stated that increasing integration of ADAS requires digital instrument clusters to display real-time driver alerts clearly.

MARKET RESTRAINTS

High Development and Integration Costs Limit Rapid Adoption

Digital instrument clusters involve complex software, display panels, and electronics, which can increase production costs. Smaller automakers face challenges integrating these systems at scale. Cost pressure becomes more pronounced in entry-level vehicles, limiting faster penetration despite rising demand and slowing overall market growth in price-sensitive regions.

- For instance, in October 2023, Continental AG implied that rising system complexity and electronics costs challenge broader deployment of advanced digital cockpit and cluster solutions.

MARKET OPPORTUNITIES

Expansion of Digital Clusters into Mid-Segment Vehicles Creates New Demand

A strong opportunity lies in expanding digital clusters into mass-market passenger cars. As displays become more cost-effective, automakers can offer digital interfaces in mid-priced models. This supports higher volumes and long-term growth as consumers increasingly expect modern digital dashboards as standard features.

- For instance, in February 2024, Hyundai Motor Company highlighted that digital instrument clusters are expanding into mid-segment models as display technologies become more cost-efficient.

AUTOMOTIVE DIGITAL INSTRUMENT CLUSTER MARKET TRENDS

Shift Toward Larger and High-Resolution Displays Enhances Driver Experience

A key trend is the move toward larger, clearer digital displays that improve readability and interface customization. Enhanced graphics support navigation, vehicle data, and ADAS alerts more effectively. This trend strengthens user experience and supports sustained market growth across vehicle segments.

- For instance, in June 2024, Visteon Corporation implied OEMs increasingly prefer larger, configurable digital clusters to support navigation and integrated driver information displays.

MARKET CHALLENGES

Semiconductor and Display Supply Constraints Affect Production Stability

Supply disruptions in semiconductors and display panels continue to be a major challenge. Inconsistent component availability affects production schedules and raises costs. Managing resilient supply chains is essential, as prolonged disruptions can delay vehicle launches and negatively influence long-term market expansion.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

SUVs Dominate Due to Higher Digital Feature Integration and Display Size Demand

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is divided into Hatchback/Sedan, SUV, LCV, and HCV.

SUVs dominate the automotive digital instrument cluster market share as they typically feature larger dashboards, higher trim levels, and advanced digital interfaces. Automakers integrate bigger, more configurable displays in SUVs to support navigation, vehicle diagnostics, and advanced driver assistance systems ADAS visualization. Strong consumer demand for premium features, combined with higher price tolerance in the SUV segment, accelerates adoption and contributes significantly to overall market growth.

- For instance, in March 2024, Hyundai Motor Company stated that SUVs increasingly feature larger digital instrument clusters to support premium interiors and advanced driver information systems.

The HCV segment is expected to grow at a CAGR of 10.0% over the forecast period.

By Type

Semi-Digital and Hybrid Clusters Leads the Market Owing to Analog Reliability with Digital Flexibility

On the basis of type, the market is segmented into semi-digital & hybrid and fully digital.

Semi-digital and hybrid clusters dominate as they combine analog reliability with digital flexibility. This balance helps automakers manage production costs while offering improved visual features, making them popular in mass-market vehicles.

- For instance, in June 2024, Honda Motor Co. implied semi-digital instrument clusters remain common across mass-market models, offering digital information while retaining familiar analog elements.

The Fully Digital segment is expected to grow at a CAGR of 11.3% over the forecast period.

By Display Size

Sufficient Space for Navigation and ADAS Fuels the 10–12 Inch Display Segment’s Growth

On the basis of display size, the market is segmented into <7 inches, 7-9 inches, 10-12 inches, and >12 inches.

The 10–12 inch segment dominates as it provides sufficient space for navigation and ADAS alerts without excessive dashboard redesign. Automakers favor this size for functionality and cost-effective integration.

- For instance, in May 2024, Visteon highlighted OEM preference for mid-sized digital displays that integrate navigation and driver information without excessive dashboard redesign.

More than a 12-inch segment is expected to grow at a CAGR of 13.1% over the forecast period.

By Display Technology

Mature Manufacturing Processes and Lower Costs Lead to TFT-LCD Segmental Growth

On the basis of display technology, the market is segmented into TFT-LCD and OLED.

TFT-LCD dominates due to mature manufacturing processes, consistent performance, and lower costs compared to OLED. It meets automotive durability requirements and supports scalable production.

- For instance, in January 2024, Continental confirmed that TFT-LCD remains widely adopted in automotive clusters due to proven reliability and scalable manufacturing processes.

The OLED segment is expected to grow at a CAGR of 24.7% over the forecast period.

By Propulsion

ICE Vehicles Holds the Dominant Position Owing to High Production Volumes

On the basis of propulsion, the market is segmented into ICE and Electric.

Despite EV growth, ICE vehicles dominate due to high production volumes. Digital clusters enhance efficiency monitoring and driver information, supporting the improvement of fuel efficiency goals.

- For instance, in August 2023, Toyota stated that internal combustion vehicles continue to have high global production volumes, sustaining demand for digital clusters across mainstream models.

The electric segment is expected to grow at a CAGR of 14.8% over the forecast period.

By Sales Channel

OEM Channel Leads the Market Owing to Integrated Vehicle Design and Assembly

On the basis of sales channel, the market is segmented into OEM and Aftermarket.

OEMs dominate as digital clusters are integrated during vehicle design and assembly. Direct sourcing ensures compatibility, quality control, and long-term supply stability.

- For instance, in March 2024, Bosch Mobility highlighted that digital instrument clusters are primarily supplied through OEM integration to ensure system compatibility and functional safety.

The aftermarket segment is expected to grow at a CAGR of 12.1% over the forecast period.

Automotive Digital Instrument Cluster Market Regional Outlook

By region, the automotive digital instrument cluster market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive Digital Instrument Cluster Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the automotive digital instrument cluster market, valued at USD 3.90 billion in 2024, and also maintained the leading share in 2025, due to high vehicle production volumes, rapid technology adoption, and strong electronics manufacturing capabilities. Rising adoption of connected features, increasing production of passenger cars, and cost-efficient manufacturing processes support large-scale deployment. Strong local supply chains and rising consumer preference for modern driver interfaces further reinforce the region’s leadership.

Based on Asia Pacific’s strong contribution and China’s dominance within the region, the China market is USD 2.31 billion in 2025, accounting for roughly 25.08% of global automotive digital instrument cluster sales.

China Automotive Digital Instrument Cluster Market

China's automotive digital instrument cluster market is projected to reach approximately USD 2.15 billion in 2025. China represents the largest country-level market due to high passenger vehicle and SUV production volumes and rapid adoption of digital cockpits. Strong domestic electronics manufacturing and widespread integration of advanced driver assistance systems support large-scale deployment of digital instrument clusters across vehicle segments.

India Automotive Digital Instrument Cluster Market

India automotive digital instrument cluster market is projected to reach approximately USD 0.38 Billion in 2025, equivalent to around 4.23% of global automotive digital instrument cluster sales.

North America

North America is estimated to reach USD 1.90 Billion in 2025 and secure the position of the third-largest region in the market. The market shows steady adoption of digital instrument clusters driven by demand for advanced vehicle displays across SUVs and passenger cars. Strong OEM presence, higher feature penetration, and growing integration of advanced driver assistance systems support continued market expansion across the region.

U.S. Automotive Digital Instrument Cluster Market

U.S. automotive digital instrument cluster market is projected to reach approximately USD 1.43 Billion in 2025, equivalent to around 15.5% of global automotive digital instrument cluster sales. The U.S. market shows high adoption of large, customizable digital instrument clusters, particularly in SUVs and luxury vehicles. OEMs focus on advanced driver assistance systems ADAS and infotainment integration, which supports steady growth during the forecast period.

Europe

Europe is projected to record a growth rate of 6.2% in the coming years and reach a valuation of USD 2.11 billion by 2025. The market grows steadily due to strict safety regulations and high penetration of digital displays in mid-to-premium vehicles. Automakers emphasize integrated driver information systems and ADAS visualization, supporting continued adoption of digital instrument clusters across vehicle segments.

U.K Automotive Digital Instrument Cluster Market

The U.K. Automotive Digital Instrument Cluster Market in 2025 is estimated at around USD 0.27 Billion, representing roughly 2.9% of global automotive digital instrument cluster revenues.

Germany Automotive Digital Instrument Cluster Market

Germany’s Automotive Digital Instrument Cluster Market is projected to reach approximately USD 0.52 Billion in 2025, equivalent to around 5.7% of global automotive digital instrument cluster sales.

Rest of the World

The rest of the world markets experience gradual growth as digital instrument clusters expand into mid-priced vehicles. Increasing vehicle production, improving affordability, and rising safety awareness are expected to support long-term adoption across Latin America, the Middle East, and Africa.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Innovation and Platform Scalability Drive Market Competition

The competitive landscape of the Automotive Digital Instrument Cluster Market is shaped by global electronics suppliers and Tier-1 automotive system integrators. Key players compete by delivering visually advanced, software-rich clusters that balance performance, reliability, and cost. Competitive advantage increasingly depends on design flexibility and seamless integration with vehicle electronics.

Leading suppliers invest in research and development to enhance display clarity, processing speed, and system reliability. Companies are developing modular architectures that allow automakers to scale features across multiple vehicle platforms, helping control production costs while maintaining differentiation. Compatibility with electric vehicles EVs and advanced driver assistance systems ADAS is now a baseline requirement rather than a premium feature.

Another core strategy is strengthening supply chains and regional manufacturing footprints. Suppliers localize production to support OEM just-in-time delivery and reduce logistics risk. Software capability is also becoming a differentiator, with clusters increasingly supporting over-the-air updates and configurable interfaces.

Partnerships with automakers during early vehicle development cycles help suppliers embed their systems into long-term vehicle programs. Those offering durable, visually appealing, and cost-effective solutions gain preference as OEMs push digital features into mid-range models.

- In 2024, Bosch Mobility showcased its latest digital cockpit platform, combining instrument clusters with ADAS visualization for scalable use across passenger vehicle segments.

LIST OF KEY AUTOMOTIVE DIGITAL INSTRUMENT CLUSTER COMPANIES PROFILED

- Bosch (Germany)

- Continental AG (Germany)

- Visteon Corporation (U.S.)

- Denso Corporation (Japan)

- Marelli (Japan)

- Aptiv PLC (Ireland)

- Panasonic Automotive (Japan)

- Harman International (U.S.)

- LG Electronics Vehicle Solutions (South Korea)

- Hyundai Mobis (South Korea)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Bosch stated its TFT Connect instrument cluster improves brightness and contrast, enhancing semi-digital and hybrid display performance for two-wheelers.

- May 2024: Toyota Motor Europe stated the Yaris Cross SUV offers a customizable 12.3-inch digital driver display across higher trims.

- April 2024: Marelli stated that ProConnect integrates instrument cluster, infotainment, and telematics into a unified cockpit platform for entry and mid-segment vehicles.

- March 2024: Volkswagen stated the new Passat features Digital Cockpit Pro with next-generation infotainment and driver information integration.

- January 2024: HARMAN stated its CES 2024 portfolio enables OEMs to accelerate deployment of advanced in-cabin digital display experiences.

REPORT COVERAGE

The automotive digital instrument cluster market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Type, Display Size, Display Technology, Propulsion, Sales Channel, and Region |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Type |

· Semi-Digital & Hybrid · Fully Digital |

|

By Display Size |

· <7 inches · 7-9 inches · 10-12 inches · >12 inches |

|

By Display Technology |

· TFT-LCD · OLED |

|

By Propulsion |

· ICE · Electric |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Region |

· North America (By Vehicle Type, Type, Display Size, Display Technology, Propulsion, Sales Channel, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Type, Display Size, Display Technology, Propulsion, Sales Channel, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Type, Display Size, Display Technology, Propulsion, Sales Channel, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, Type, Display Size, Display Technology, Propulsion, Sales Channel and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.21 Billion in 2025 and is projected to reach USD 17.90 Billion by 2034.

In 2025, the market value stood at USD 4.20 Billion.

The market is expected to exhibit a CAGR of 7.6% during the forecast period of 2026-2034.

The SUV segment led the market in terms of vehicle type.

The rising integration of driver assistance features accelerates the adoption of digital clusters, driving the automotive digital instrument cluster market.

Bosch, Continental AG, Visteon, and Valeo are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us