Automotive Intelligence Battery Sensor Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Sensor Technology (Hall-Effect and Shunt-Based), By Voltage Architecture (12V, 24V, and 48V), By Battery Type (Lead-Acid and Lithium-Ion), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026–2034

Automotive Intelligence Battery Sensor Market Size and Future Outlook

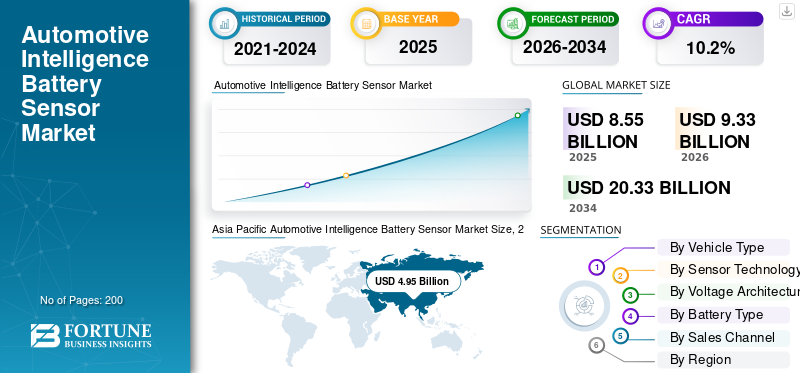

The global automotive intelligence battery sensor market size was valued at USD 8.55 billion in 2025. The market is projected to grow from USD 9.33 billion in 2026 to USD 20.33 billion by 2034, exhibiting a CAGR of 10.2% during the forecast period. Asia Pacific dominated the automotive intelligence battery sensor market with a market share of 57.89% in 2025.

An automotive intelligence battery sensor is an electronic device that monitors battery parameters such as voltage, current, and temperature, enabling efficient energy management, improved performance, and enhanced vehicle reliability. Market growth is driven by increasing vehicle electrification, rising demand for advanced battery management systems, growing adoption of electric vehicles, stricter emission regulations, and the need for improved energy efficiency and reliability.

Major players in the market include Robert Bosch GmbH, Continental AG, DENSO Corporation, HELLA GmbH & Co. KGaA, Valeo SA, and NXP Semiconductors, competing through advanced sensing technologies, battery management integration, real-time monitoring capabilities, and enhanced vehicle electrification solutions.

Download Free sample to learn more about this report.

AUTOMOTIVE INTELLIGENCE BATTERY SENSOR MARKET TRENDS

Rising Vehicle Electrification and Advanced Energy Management Systems to Drive Market Growth

The increasing shift toward vehicle electrification, including electric and hybrid vehicles, is significantly driving the demand for Intelligence battery sensors. These sensors play a crucial role in monitoring vehicle battery health, optimizing energy usage, and ensuring efficient power distribution across vehicle systems. As modern vehicles incorporate more electronic components, the need for precise optimal battery diagnostics becomes essential. This type of market trend is further supported by stringent emission norms and fuel efficiency standards, encouraging automakers to adopt advanced energy management solutions.

- In May 2025, the IEA reported a 35% increase in global EV sales in Q1, with total sales expected to exceed 20 million units. This surge drives automotive intelligence battery sensor market demand to ensure efficient energy management, safety, and performance monitoring.

MARKET DYNAMICS

MARKET DRIVERS

Integration of Smart Diagnostics and IoT-Enabled Monitoring to Shape Market Trends

The growing integration of IoT and smart diagnostic technologies is transforming the automotive battery sensor landscape. Intelligence battery sensors are increasingly equipped with real-time data transmission capabilities, enabling predictive maintenance and remote monitoring. This enhances vehicle reliability and reduces unexpected failures. Automakers and fleet operators are leveraging connected technologies to improve operational efficiency and reduce downtime. As vehicles become more digitally connected, the demand for sensors that support advanced diagnostics and data analytics is expected to rise steadily.

- In October 2025, General Motors announced a centralized computing platform with 1,000× bandwidth and 35× AI performance, integrating propulsion, safety, and diagnostics. Such software-defined architectures increase reliance on Intelligence battery sensors for real-time monitoring, predictive maintenance, and energy optimization.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Initial Costs and Complex Integration to Restrain Market Expansion

The adoption of Intelligence battery sensors is often hindered by high initial costs associated with advanced sensing technologies and system integration. These sensors require compatibility with vehicle electronics and battery management systems, increasing design complexity. For cost-sensitive markets, especially in developing regions, manufacturers may hesitate to adopt such technologies. Additionally, retrofitting these sensors in existing vehicle platforms can be challenging. These factors collectively ac t as restraints, limiting widespread adoption despite the long-term operational benefits offered by intelligent battery monitoring systems.

MARKET OPPORTUNITIES

Growth of Electric Vehicles and Energy Storage Systems to Create Market Opportunities

The rapid expansion of plug-in hybrid electric vehicles, battery electric vehicles, and advancements in energy storage systems present significant opportunities for the Intelligence battery sensor market. As EV adoption accelerates globally, the need for accurate battery monitoring becomes critical for performance, safety, and lifespan optimization. Intelligent sensors enable better thermal management and state of charge-discharge control, enhancing battery efficiency. Additionally, innovations in battery technologies, such as lithium-ion and solid-state batteries, are creating new avenues for sensor integration, supporting the long-term potential for automotive intelligence battery sensor market growth.

- In February 2026, Changan and CATL launched the first mass-production EV with sodium-ion batteries featuring 175 Wh/kg energy density and advanced BMS integration. This innovation increases demand for Intelligence battery sensors to ensure thermal stability, performance monitoring, and safety.

MARKET CHALLENGES

Data Accuracy and Standardization Challenges to Impact Market Development

One of the key challenges in the market is ensuring high data accuracy and standardization across different vehicle platforms and battery types. Variations in battery chemistries and operating conditions can affect sensor performance and reliability. Lack of uniform standards for sensor calibration and data interpretation may lead to inconsistencies in diagnostics. This creates challenges for manufacturers aiming to develop universally compatible solutions. Addressing these issues requires continuous innovation, testing, and collaboration across the automotive and electronics ecosystems.

Segmentation Analysis

By Vehicle Type

Rising SUVs Adoption and Electrification Trends to Propel Segmental Dominance

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates the market due to its increasing global adoption, higher electrical load requirements, and growing integration of advanced electronics. These vehicles demand efficient battery monitoring systems to support features such as ADAS, infotainment, and electrified powertrains. Rising consumer preference for SUVs, coupled with increasing electrification in this segment, significantly boosts the adoption of intelligence battery sensors across both OEM and aftermarket channels.

- In June 2025, Xiaomi launched the YU7 electric SUV, securing over 200,000 orders within one hour, featuring 700 TOPS AI computing, LiDAR, and high-performance battery systems. This surge in EV adoption increases demand for Intelligence battery sensors for efficient energy management, safety monitoring, and performance optimization.

The hatchback & sedans segment is the second-largest and is projected to grow at a CAGR of 8.6% over the forecast period. High vehicle parc, affordability, and widespread usage in urban mobility sustain consistent demand for battery monitoring solutions.

To know how our report can help streamline your business, Speak to Analyst

By Sensor Technology

High Accuracy and Cost Efficiency to Propel Shunt-Based Segment Dominance

Based on sensor technology, the market is segmented into hall-effect and shunt-based sensors.

The shunt-based segment dominates the market due to its cost-effectiveness, high measurement accuracy, and widespread adoption in conventional and entry-level battery management systems. These sensors provide reliable current measurement with a simpler architecture, making them suitable for mass-market vehicles. Their compatibility with existing electrical systems and ease of integration further support large-scale deployment across both ICE and electric vehicles, ensuring consistent demand globally.

The hall-effect segment is projected to grow at a CAGR of 11.6% over the automotive intelligence battery sensor market forecast period. Increasing demand for contactless sensing, enhanced safety, and adoption in electric vehicles drives the rapid growth of this segment.

- In May 2024, LEM introduced coreless current sensors supporting 2kA–42kA measurement, 1 MHz bandwidth, and 85% lower energy consumption. These sensors improve accuracy, reduce power losses, and enable efficient high-current monitoring, supporting advanced electrification applications.

By Voltage Architecture

Widespread Adoption in Conventional Vehicles to Propel 12V Segment Dominance

Based on voltage architecture, the market is segmented into 12V, 24V, and 48V.

The 12V segment dominates the market due to its extensive use in conventional internal combustion engine vehicles and standard automotive electrical systems. These systems support essential vehicle functions such as lighting, infotainment, and engine control, ensuring consistent demand for Intelligence battery sensors. High global vehicle parc and established infrastructure further reinforce the continued dominance of 12V architecture across passenger and commercial vehicles.

- In March 2026, LiTime introduced a 12V 200Ah lithium battery within a Group 31 size, achieving 41% size reduction and double usable energy compared to lead-acid batteries. The battery measures 13.11 × 6.93 × 10.04 inches and delivers improved runtime and space efficiency for compact installations.

The 48V segment is projected to grow at a CAGR of 12.9% over the forecast period. Increasing adoption of mild-hybrid vehicles and demand for improved fuel efficiency are accelerating the shift toward 48V systems.

By Battery Type

Established Usage in Conventional Vehicles to Propel Lead-Acid Segment Dominance

Based on battery type, the market is segmented into lead-acid and lithium-ion.

The lead-acid segment dominates the market due to its widespread use in conventional vehicles, cost-effectiveness, and established supply chain. These batteries are extensively utilized in starting, lighting, and ignition (SLI) applications, ensuring consistent demand for intelligence battery sensors. Their reliability, recyclability, and compatibility with existing vehicle architectures further support their continued dominance across both passenger and commercial vehicle segments globally.

The lithium-ion segment is projected to grow at a CAGR of 12.2% over the forecast period. Increasing adoption of electric vehicles and demand for high-energy-density solutions are driving the rapid growth of this segment.

- In December 2024, Stellantis and Zeta Energy announced development of lithium-sulfur EV batteries offering up to 50% faster charging, significantly lighter weight, and less than half the cost per kWh compared to lithium-ion. The technology also enables higher energy density using sulfur-based materials.

By Sales Channel

Strong Integration with Advanced Vehicle Electronics to Propel OEM Segment Dominance

Based on the sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates the market and is also the fastest growing due to increasing integration of Intelligence battery sensors in new vehicles. Automakers are embedding advanced battery management systems to enhance vehicle efficiency, support electrification, and meet regulatory requirements. Rising production of electric and connected vehicles further strengthens OEM demand, as sensors become a standard component in modern vehicle architectures globally.

The aftermarket segment is projected to grow at a CAGR of 9.7% over the forecast period. Growing vehicle parc, replacement needs, and rising awareness of battery health monitoring are driving steady demand in the aftermarket.

Automotive Intelligence Battery Sensor Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Intelligence Battery Sensor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is also the fastest-growing region due to strong automotive production, rising electric vehicle adoption, and increasing demand for advanced battery management systems. Countries such as China, Japan, and South Korea lead in technological advancements and EV manufacturing. Government incentives, expanding vehicle parc, and growing focus on energy efficiency further accelerate demand for Intelligence battery sensors, making the region a key growth hub during the forecast period.

- In 2024, according to IEA, global electric car production reached 17.3 million units, with China producing 12.4 million units, accounting for over 70% of total output. Chinese OEMs contributed more than 80% of domestic production, highlighting strong local manufacturing expansion.

China Automotive Intelligence Battery Sensor Market

The China market in 2026 is estimated at around USD 3.20 billion, accounting for roughly 34.3% of global revenues. Strong EV production, government incentives, and a large vehicle parc drive sustained demand growth in China.

Japan Automotive Intelligence Battery Sensor Market

The Japan market in 2026 is estimated at around USD 0.81 billion, accounting for roughly 8.7% of global revenues. Advanced automotive technologies and hybrid vehicle leadership support steady sensor adoption in the country.

India Automotive Intelligence Battery Sensor Market

The India market in 2026 is estimated at around USD 0.61 billion, accounting for roughly 6.5% of global revenues. Rapid electrification, growing vehicle sales, and policy support accelerate the fastest growth in the Indian market.

Europe

Europe holds the second-largest automotive intelligence battery sensor market share and is projected to grow at a CAGR of 9.8% over the forecast period. Stringent emission regulations and aggressive electrification targets are driving the adoption of advanced battery monitoring systems. The presence of leading automotive OEMs and strong R&D capabilities supports innovation in sensor technologies. Additionally, increasing hybrid and electric vehicle penetration across countries such as Germany and France further fuels consistent demand for Intelligence battery sensors.

- In September 2025, Stellantis introduced its Intelligent Battery Integrated System prototype, integrating inverter and charger functions, achieving 10% higher efficiency, 15% faster charging, and 40 kg weight reduction, while optimizing space and supporting future EV deployment.

Germany Automotive Intelligence Battery Sensor Market

The Germany market in 2026 is estimated at around USD 0.42 billion, accounting for roughly 4.5% of global revenues. Strong OEM presence and electrification targets drive consistent demand growth in Germany.

U.K. Automotive Intelligence Battery Sensor Market

The U.K. market in 2026 is estimated at around USD 0.09 billion, accounting for roughly 1.0% of global revenues. Increasing EV adoption and regulatory push support gradual market expansion in the U.K.

North America

North America represents the third-largest market, driven by the growing adoption of connected and electric vehicles. The region benefits from strong technological infrastructure and early adoption of advanced automotive electronics. Increasing focus on vehicle safety, performance optimization, and battery efficiency is boosting the demand for Intelligence battery sensors. Additionally, the presence of key automotive and semiconductor companies supports innovation and integration of advanced sensing solutions across vehicle platforms.

- In September 2025, WEG and Aderis Energy launched a U.S.-developed battery management system supporting over 4 GW of assets, featuring N+1 redundancy, cloud-based monitoring, and black start capability, enabling resilient and secure energy storage for critical infrastructure.

U.S. Automotive Intelligence Battery Sensor Market

The U.S. market in 2026 is estimated at around USD 1.05 billion, accounting for roughly 11.3% of global revenues. Strong technology adoption and EV investments drive steady market growth in the country.

Rest of the World

The rest of the world region is witnessing steady growth due to expanding automotive markets in South America and the Middle East & Africa. Increasing urbanization, improving economic conditions, and the gradual adoption of electric vehicles are contributing to market expansion. Although infrastructure challenges persist, growing awareness of vehicle efficiency and battery performance is supporting the adoption of Intelligence battery sensors. Government initiatives and investments in automotive development further create growth opportunities in these emerging regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Electrification Trends Define Competitive Intensity

The market is moderately consolidated, with key players focusing on advanced sensing technologies and integration capabilities. Companies such as Robert Bosch GmbH, Continental AG, DENSO Corporation, HELLA GmbH & Co. KGaA, Valeo SA, and NXP Semiconductors compete through innovation in battery monitoring, real-time diagnostics, and vehicle electrification solutions. To strengthen their position, firms are investing in semiconductor advancements, software integration, and EV-focused sensor technologies. Strategic collaborations with OEMs, product miniaturization, and expansion into emerging EV markets are key approaches to enhance competitiveness and global presence.

- In May 2023, HELLA secured series orders for high-voltage battery management systems and Intelligence battery sensors, supporting lithium-ion battery safety and performance. With over 130 million sensors delivered, production expansion in the U.S. and Europe highlights increasing demand for advanced battery monitoring solutions.

LIST OF KEY AUTOMOTIVE INTELLIGENCE BATTERY SENSOR COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- DENSO Corporation (Japan)

- HELLA GmbH & Co. KGaA (Germany)

- Valeo SA (France)

- NXP Semiconductors N.V. (Netherlands)

- TE Connectivity Ltd. (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Infineon Technologies AG (Germany)

- Sensata Technologies Holding plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: FORVIA HELLA announced its next-generation Intelligence battery sensor will enter mass production in China by mid-2026, featuring real-time monitoring, predictive maintenance, and localized development to enhance battery performance, safety, and cost efficiency.

- September 2025: Stellantis and Saft introduced IBIS technology, integrating the inverter and charger into the battery, achieving 10% energy efficiency improvement, 15% power gain, 15% faster charging, and 40 kg weight reduction. This advancement increases the need for Intelligence battery sensors to manage integrated systems, ensure real-time performance monitoring, optimize energy flow, and support advanced electrified powertrain architectures.

- June 2025: LEM introduced a Hybrid Supervising Unit combining shunt and Hall-effect technologies, supporting ±2,000 A measurement, 25 µΩ resistance, and ASIL-D compliance. This innovation enhances accuracy, safety, and integration efficiency, driving demand for advanced Intelligence battery sensors.

- November 2024: NXP introduced an ultra-wideband (UWB) wireless BMS enabling robust voltage and temperature data transfer without wiring, improving energy density and reducing assembly complexity. This innovation enhances system flexibility, lowers lifecycle costs, and accelerates EV development timelines.

- October 2024: Honeywell introduced an electrolyte gas detection sensor using Li-ion Tamer technology, capable of detecting “first vent” events and providing warnings 5–20 minutes before potential battery fire. This enables early intervention, improves EV battery safety, enhances real-time monitoring capabilities, and supports compliance with Global Technical Regulation No. 20 and other evolving EV safety standards.

- October 2024: FORVIA HELLA introduced Intelligence battery sensors for 24V systems, enabling monitoring of SoC, SoH, and SoF with cloud connectivity. These sensors improve energy management, extend battery life, support start-stop systems, and enable predictive maintenance across fleets.

- August 2024: University of Arizona researchers developed a machine learning-based framework using multiphysics models and thermal sensors to predict lithium-ion battery thermal runaway, enabling early hotspot detection, improved safety, and integration into EV battery management systems.

- May 2022: Continental launched new battery protection sensors, including a high-voltage current sensor module and battery impact detection system, featuring ±1% shunt accuracy, temperature sensing from -40°C to 125°C, CAN interface integration, and impact detection enabling lightweight underfloor protection and enhanced EV battery safety.

REPORT COVERAGE

The global automotive intelligence battery sensor market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.2% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Sensor Technology, Vehicle Type, Voltage Architecture, Battery Type, Sales Channel, and Region |

| By Sensor Technology |

|

| By Vehicle Type |

|

| By Voltage Architecture |

|

| By Battery Type |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.55 billion in 2025 and is projected to reach USD 20.33 billion by 2034.

In 2025, the market value stood at USD 4.95 billion.

The market is expected to exhibit a CAGR of 10.2% during the forecast period.

The SUVs segment leads the market in terms of vehicle type.

Integration of smart diagnostics and IoT-enabled monitoring to shape market trends.

Major players in the market include Robert Bosch GmbH, Continental AG, DENSO Corporation, HELLA GmbH & Co. KGaA, Valeo SA, and NXP Semiconductors.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us