Automotive Wheel Alignment Services Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Service Type (Two-Wheel Alignment and Four-Wheel Alignment), By Service Provider (OEM Authorized Service Centers, Independent Workshops, Tire & Specialty Chains, and Others), By Technology Used (3D Camera-Based Systems, CCD Systems, Laser Systems, and Others), By End User (Individual Vehicle Owners, Fleet Operators, Commercial Transport Companies, and Rental & Leasing Companies), and Regional Forecasts, 2026-2034

Automotive Wheel Alignment Services Market Size and Future Outlook

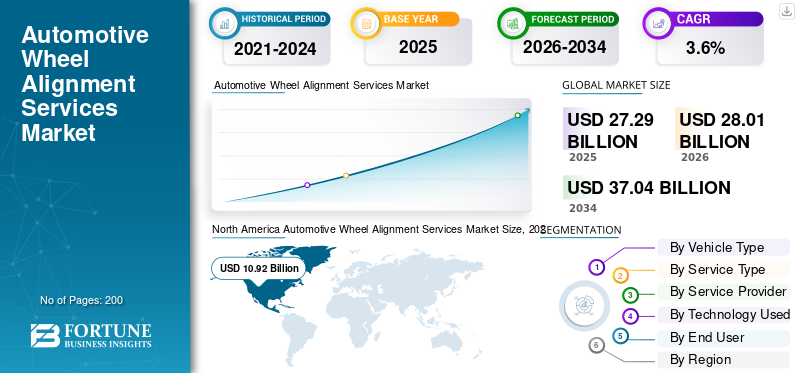

The global automotive wheel alignment services market size was valued at USD 27.29 billion in 2025. The market is projected to grow from USD 28.01 billion in 2026 to USD 37.04 billion by 2034, exhibiting a CAGR of 3.6% during the forecast period. North America dominated the automotive wheel alignment services market with a market share of 40.01% in 2025.

The automotive wheel alignment services market represents the industry dedicated to inspecting, adjusting, and correcting wheel angles to ensure proper vehicle balance, steering accuracy, tire longevity, and fuel efficiency. This industry forms a vital part of routine automotive maintenance and directly supports road safety and operational performance across passenger and commercial vehicle categories. The market analysis includes services performed using modern wheel alignment technology and advanced digital wheel alignment system platforms.

The market is influenced by rising global vehicle sales, expanding vehicle parc, and increasing awareness among vehicle owners regarding preventive maintenance. As vehicle complexity grows, especially with the integration of advanced technologies such as ADAS and electronic stability systems, precise wheel alignment has become increasingly essential. Modern vehicles, categorized by vehicle type, require calibrated alignment to maintain performance standards and regulatory compliance.

Growth is also supported by rising service penetration in emerging regions, including the Asia Pacific and the Middle East & Africa, where motorization rates continue to increase. Additionally, the growing demand for fleet optimization among logistics operators is strengthening alignment service adoption for commercial vehicle applications.

Over the forecast period, digitization of service centers, integration of alignment equipment with diagnostics platforms, and increased equipment modernization will shape future market trends. This market research report reflects structured market sizing, regional expansion, and technology transition.

Leading players are expanding service networks, introducing AI-enabled alignment systems, and forming partnerships to enhance calibration accuracy and digital service tracking, thereby strengthening their global competitive positioning.

Download Free sample to learn more about this report.

AUTOMOTIVE WHEEL ALIGNMENT SERVICES MARKET TRENDS

Shift Toward 3D and Digital Wheel Alignment Technology is a Key Market Trend

A key industry trend is the migration from laser-based systems to 3D camera-based wheel alignment technology. Digital platforms improve accuracy, reduce service time, and integrate with vehicle diagnostics, enhancing customer trust and repeat service. This trend supports premium service positioning across North America and Europe.

For instance, in April 2024, Snap-on introduced upgraded John Bean 3D alignment systems with enhanced imaging capability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Vehicle Parc and Emphasis on Fuel Efficiency Propel Service Demand

Increasing global vehicle ownership and growing focus on fuel efficiency are driving demand in the market. Misaligned wheels reduce fuel economy and accelerate tire wear, prompting regular service adoption among vehicle owners and fleet operators. Rising vehicle sales across developing regions further expand the serviceable base, strengthening overall market sizing and growth potential.

- For instance, in January 2024, the U.S. Department of Energy highlighted that proper tire maintenance and wheel alignment can improve fuel economy by up to 3%.

MARKET RESTRAINTS

High Equipment Costs Limit Small Workshop Adoption

The high upfront cost of advanced wheel alignment system equipment restricts adoption among small and informal workshops, particularly in the Middle East & Africa and parts of the Asia Pacific. Modern 3D alignment platforms require significant capital investment, limiting the penetration of sophisticated wheel alignment technology and thereby slowing the automotive wheel alignment services market growth.

- For instance, in July 2023, a report from the Automotive Service Association noted that rising equipment costs remain a concern for independent repair shops.

MARKET OPPORTUNITIES

Expansion of Advanced Technologies and ADAS Calibration Services Offers Growth Opportunities

Integration of advanced technologies and ADAS systems presents strong growth opportunities. Modern vehicles require precise calibration after suspension repairs or alignment adjustments, which increases service complexity and the value per job. This enhances revenue potential across organized service providers and supports future market trends.

- For instance, in September 2023, Bosch emphasized the growing need for ADAS calibration tools integrated with alignment systems.

MARKET CHALLENGES

Informal Service Sector Creating Pricing Pressure Emerges as a Market Challenge

A significant market challenge is the presence of informal workshops, especially in the Asia Pacific and the Middle East & Africa that offer low-cost manual alignment. This creates pricing pressure on organized players and affects the overall alignment service market analysis accuracy.

- For instance, in November 2023, India’s Automotive Aftermarket Association noted the large share of unorganized workshops in rural regions.

Segmentation Analysis

By Vehicle Type

Hatchbacks/Sedans Segment Dominate the Market Due to Large Global Vehicle Base

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, light commercial vehicles, and heavy commercial vehicles.

Hatchbacks/sedan segment dominates with the largest automotive wheel alignment services market share, due to its massive installed base globally. High ownership among urban vehicle owners, regular commuting usage, and periodic maintenance needs sustain alignment demand.

- For instance, in February 2024, ACEA reported that passenger cars accounted for over 85% of vehicles in use across Europe.

SUVs segment is expected to grow at a CAGR of 4.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Software Leads Because Insight, Workflow, And Value Sit in Analytics

On the basis of service type, the market is segmented into two-wheel alignment and four-wheel alignment.

Four-wheel alignment segment dominates the market, as many modern vehicles use independent rear suspension systems that require full calibration for optimal fuel efficiency and tire performance.

- For instance, in May 2023, Hunter Engineering highlighted increased demand for 4-wheel alignment in independent workshops.

Four-wheel alignment segment is expected to grow at a CAGR of 3.8% over the forecast period.

By Service Provider

Independent Workshops Hold Largest Share Due to Wide Accessibility

On the basis of service provider, the market is segmented into OEM authorized service centers, independent workshops, tire & specialty chains, and others.

Independent workshops segment dominates the market due to its affordability and widespread presence. They capture substantial market shares, particularly outside North America and Western Europe.

- For instance, in August 2023, the Automotive Aftermarket Suppliers Association noted that independent repairers handle most non-warranty services.

Tire & specialty chains segment is expected to grow at a CAGR of 4.6% over the forecast period.

By Technology Used

3D Camera-Based Systems Dominate Through Precision and Efficiency

On the basis of Technology Used, the market is segmented into 3D camera-based systems, CCD systems, laser systems and others.

3D camera-based systems segment dominates the market, as they provide fast, accurate diagnostics and integrate with ADAS calibration platforms, enhancing service reliability.

- For instance, in March 2024, Beissbarth launched an updated 3D alignment system for multi-brand workshops.

3D camera-based systems segment is expected to grow at a CAGR of 4.0% over the forecast period.

By End User

Individual Vehicle Owners Drive Majority Demand

On the basis of end user, the market is segmented into individual vehicle owners, fleet operators, commercial transport companies, and rental & leasing companies.

Individual vehicle owners dominate end-user demand due to routine maintenance and tire replacement cycles. Preventive service awareness supports recurring alignment visits.

- For instance, in January 2024, AAA (the American Automobile Association, Inc.) advised regular alignment checks to maintain tire safety and reduce wear.

Commercial transport companies segment is expected to grow at a CAGR of 5.2% over the forecast period.

Automotive Wheel Alignment Services Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Automotive Wheel Alignment Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 10.92 billion, and also maintained the leading share in 2024, with USD 10.65 billion. The regional growth is driven by high vehicle ownership, advanced workshop infrastructure, and widespread adoption of digital wheel alignment system equipment. The region benefits from a strong preventive maintenance culture and a high penetration of SUVs and light trucks. Increasing integration of advanced technologies supports service value growth.

- For instance, in 2024, FHWA reported over 280 million registered vehicles in the U.S., sustaining alignment service demand.

U.S. Automotive Wheel Alignment Services Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be approximated at around USD 9.07 billion, representing roughly 33.2% of the market.

Europe

Europe is estimated to reach USD 9.40 billion in 2026 and secure the position of the second-largest region in the market. Europe will grow steadily due to aging vehicle fleets, stringent road safety norms, and the rising adoption of advanced diagnostic systems. Structured service networks enhance market sizing visibility. The U.S., however, continues to display higher service penetration and larger alignment equipment modernization.

Germany Automotive Wheel Alignment Services Market

Germany’s market in 2025 was valued at USD 2.26 billion, accounting for roughly 8.3% of global revenues.

U.K. Automotive Wheel Alignment Services Market

U.K. market in 2025 was valued at USD 1.56 billion, accounting for roughly 5.7% of global revenues.

Asia Pacific

Asia Pacific is projected to record a growth rate of 4.9% in the coming years, and reach a valuation of USD 5.98 billion by 2026. Asia Pacific will witness strong expansion driven by rising motorization, expanding middle-class ownership, and increasing vehicle sales. Growth of organized service chains supports structured alignment services across developing economies.

China Automotive Wheel Alignment Services Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 2.12 billion, representing roughly 7.8% of global market.

India Automotive Wheel Alignment Services Market

Indian market in 2025 was valued at USD 0.86 billion, accounting for roughly 3.2% of global revenues.

Rest of the World

The rest of the world, including Latin America and the Middle East, is expected to witness moderate growth in market. Expanding vehicle fleets, increasing vehicle maintenance awareness, and improving automotive service infrastructure are supporting market development. Growing commercial transport activities and urban vehicle density will further drive alignment service demand in these regions. In the Middle East & Africa, improving infrastructure and growing fleet operations will stimulate service adoption. Market growth remains gradual, supported by increasing commercial transport demand and urban vehicle concentration.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansion and Technology Integration Drive Competition

The competitive landscape of the automotive wheel alignment services market is moderately consolidated, with global equipment manufacturers and organized service chains competing on service accuracy, digital integration, and network expansion. Companies focus on upgrading wheel alignment technology to incorporate 3D camera systems, ADAS compatibility, and data-driven calibration platforms.

Key strategies adopted by market participants include geographic expansion across North America, Asia Pacific, and the Middle East & Africa, strategic acquisitions of regional service providers, and investment in next-generation wheel alignment system platforms. Firms also differentiate through pricing strategies, service bundling, and technician training programs to strengthen market shares.

Technology innovation plays a central role. Manufacturers are integrating cloud-based diagnostics, automated target positioning, and software analytics to enhance efficiency. Partnerships with OEMs help companies align equipment with evolving vehicle and product specifications by vehicle type and product type.

Companies also leverage digital marketing and franchise expansion to capture independent workshops. Over the forecast period, consolidation among service chains and equipment suppliers is expected to intensify competition.

- For instance, in March 2023, Hunter Engineering introduced its Hawkeye Elite alignment platform upgrade to improve ADAS calibration accuracy and digital workflow integration.

LIST OF KEY AUTOMOTIVE WHEEL ALIGNMENT SERVICES COMPANIES PROFILED

- Hunter Engineering (U.S.)

- Snap-on Incorporated (U.S.)

- John Bean (U.S.)

- Bosch Automotive Service Solutions (Germany)

- Beissbarth GmbH (Germany)

- Continental Automotive Service (Germany)

- Corghi S.p.A. (Italy)

- Ravaglioli S.p.A. (Italy)

- Hofmann Megaplan (Italy)

- MAHA Maschinenbau (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Autel demonstrated its IA1000 automated wheel alignment and ADAS calibration system at the NADA Show, presenting robotic target placement and tablet-controlled calibration workflows designed for dealership environments. The system integrates alignment and ADAS procedures to reduce service time while improving measurement consistency and operational efficiency.

- December 2025: LAUNCH showcased its advanced alignment and calibration portfolio at Automechanika Shanghai 2025, highlighting the X-613 3D wheel aligner alongside its integrated ADAS & wheel-aligner robotic solution (X-939). The company emphasized automation, faster target positioning, and improved measurement precision to enhance workshop productivity and digital workflow efficiency.

- October 2025: Beissbarth announced worldwide Mercedes-Benz OE approval of the MB Q.Lign wheel alignment system, enabling OE-compliant deployments with VIN-based workflows and specified equipment scope.

- September 2025: Snap-on published a new Specs Release for wheel alignment systems, adding 550+ new models to its alignment database and further expanding service coverage.

- May 2025: Hunter Engineering issued its semi-annual ‘final 2025’ coverage update, adding hundreds of new alignment records and updates to its WinAlign vehicle information database.

- April 2025: Ravaglioli (Vehicle Service Group) confirmed its presence at Autopromotec 2025, using the event to showcase workshop diagnostics and wheel-alignment solutions to global visitors and partners.

- December 2024: Snap-on introduced the John Bean V4400 Commander, an advanced wheel aligner featuring dual-tower camera technology to enhance productivity and accuracy.

REPORT COVERAGE

The global automotive wheel alignment services market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Service Type, Service Provider, Technology Used, End User, and Region |

| By Vehicle Type |

|

| By Service Type |

|

| By Service Provider |

|

| By Technology Used |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 27.29 billion in 2025 and is projected to reach USD 37.04 billion by 2034.

In 2025, the North Americas market value stood at USD 10.92 billion.

The market is expected to exhibit a CAGR of 3.6% during the forecast period.

Hatchback/sedan segment is leading the market by vehicle type.

Rising vehicle parc and emphasis on fuel efficiency are the key factors driving the market.

Hunter Engineering, Snap-on, Bosch and Beissbarth are some of the top players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us