Autonomous BVLOS Drones Market Size, Share & Industry Analysis, By Platform Type (Fixed-Wing, Rotary-Wing, and Hybrid VTOL), By Range Class (Short-range (< 25 km), Medium-range (25 km to 150 km), and Long-range (>150 km)), By Propulsion type (Battery-electric, Hybrid-electric, Fuel-powered/ICE, & Hydrogen fuel-cell), By Application (Inspection & Monitoring, Surveying & Mapping, Agriculture, Cargo & Medical Delivery, Defense ISR/Reconnaissance, & Others), By End User (Commercial Enterprises, Civil Government & Public Safety Agencies, & Defense & Military Users), & Regional Forecast, 2026-2034

Autonomous BVLOS Drones Market Size and Future Outlook

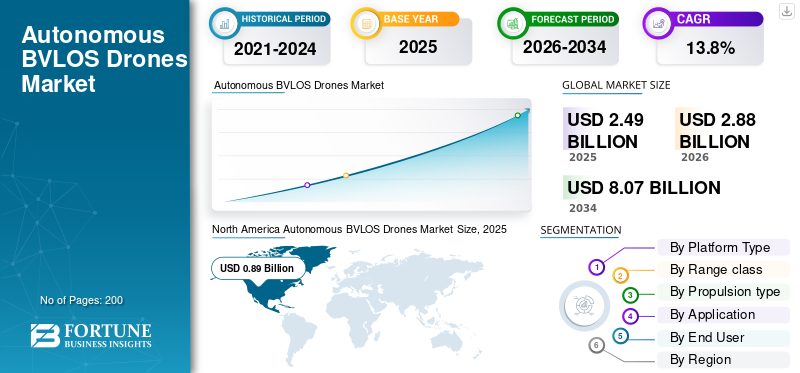

The autonomous BVLOS drones market size was valued at USD 2.49 billion in 2025. The market is projected to grow from USD 2.88 billion in 2026 to USD 8.07 billion by 2034, exhibiting a CAGR of 13.8% during the forecast period. North America dominated the autonomous BVLOS drones market with a market share of 35.74% in 2025.

The global autonomous BVLOS drones market encompasses drones that can conduct Beyond Visual Line of Sight (BVLOS) missions using onboard autonomy for navigation, sensing, route execution, and mission management with limited human input. Compared with visual line-of-sight operations, these systems are built for broader, more efficient BVLOS drone operations across infrastructure inspections, environmental monitoring, crop monitoring, precision agriculture, logistics, public safety, and defense use cases. The market is driven by rising demand for autonomous BVLOS drone systems, improvements in BVLOS capabilities, and regulatory shifts led by the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency.

Key players are moving the market from pilot programs to repeatable operations. Companies such as Wing, Zipline, and Amazon Prime Air are pushing commercial adoption by expanding delivery-focused BVLOS drone operations. At the same time, AeroVironment continues to strengthen the defense and surveillance side of the global autonomous BVLOS drone industry. These companies are driving the market through network expansion, aircraft upgrades, better autonomy, and real-world deployments.

Download Free sample to learn more about this report.

Autonomous BVLOS Drones MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.49 billion

- 2026 Market Size: USD 2.88 billion

- 2034 Forecast Market Size: USD 8.07 billion

- CAGR: 13.8% from 2026–2034

- North America dominated the market with a 35.74% share in 2025.

- The Short-range (<25 km) segment accounted for 44.01% of the market share in 2025.

- Rotary-wing segment led the market in 2025 due to strong suitability for hovering and inspection-based BVLOS operations.

North American

North America led the market in 2025, supported by strong regulatory progress and a mature commercial drone ecosystem.

Europe

Europe accounted for 25.08% of global share in 2025, driven by defense, surveillance, and regulated BVLOS expansion under EASA frameworks.

Asia Pacific

Asia Pacific is emerging as the fastest-growing region, supported by regulatory reforms and rising commercial and defense drone adoption.

U.S.

Market stood at USD 0.82 billion in 2025, driven by large-scale commercial drone operations and expanding BVLOS approvals.

Japan

Market reached USD 0.11 billion in 2025, supported by Level 4 BVLOS regulatory rollout enabling advanced drone operations.

Read More

Autonomous BVLOS Drones Market Trends

Shift from Pilot Programs to Scalable Commercial BVLOS Operations

A major trend in the global market is the shift from isolated demonstrations toward repeatable, revenue-backed BVLOS drone operations at scale. Earlier market activity was heavily centered on trials, technical validation, and regulatory exceptions. Still, the market is now moving toward structured deployment in delivery, infrastructure inspections, environmental monitoring, and other data-intensive use cases. This changes the BVLOS drone market size conversation from technology potential to operating economics, network density, and service reliability.

- In January 2026, Wing announced that it would expand drone delivery with Walmart to 150 additional stores across major U.S. markets, with access planned for more than 40 million people.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Normalization of BVLOS Operations is Driving Market Growth

One major driver of the autonomous BVLOS drones market growth is the shift from case-by-case approvals toward clearer operating rules for routine BVLOS drone operations. The market cannot scale on technology alone, it needs formal pathways that let operators deploy drones beyond visual line of sight for delivery, infrastructure inspections, precision agriculture, environmental monitoring, and other commercial missions with more predictability. The Federal Aviation Administration (FAA) has already framed its BVLOS proposal around safely normalizing these operations, while the European Union Aviation Safety Agency continues to support BVLOS activity through the specific category, including STS-02 for certain BVLOS operations. As those frameworks mature, they directly improve deployment confidence, reduce regulatory friction, and support broader market growth over the forecast period.

- In August 2025, the FAA unveiled its proposed BVLOS rule to safely normalize drone operations beyond visual line of sight, with requirements covering operations, aircraft manufacturing, separation from other aircraft, operational authorizations, security, and record keeping.

MARKET RESTRAINTS

Regulatory Complexity and Airspace-Integration Requirements Continue to Restrain Market Growth

One major restraint in the market is that scaling BVLOS drone operations still depends on complex approval, risk-assessment, and compliance processes rather than a fully harmonized operating environment. Even when the technology is ready, operators still need to prove safety for flights beyond visual line of sight, including separation from other aircraft, operational control, and mission-specific risk mitigation. That slows deployment across infrastructure inspections, environmental monitoring, precision agriculture, and other commercial applications, especially when companies want to expand at a large scale.

MARKET OPPORTUNITIES

Expansion of Autonomous Delivery and Remote Logistics Networks is Creating a Major Market Opportunity

The expansion of delivery and remote logistics networks that require frequent, repeatable flights beyond visual line of sight is a noticeable opportunity in the market. This shifts the market from one-time drone procurement toward regular BVLOS drone operations in healthcare, retail, industrial supply, and time-sensitive distribution. As operators seek faster turnaround, lower delivery friction, and broader service reach at scale, demand for autonomous BVLOS drone systems is anticipated to rise. This results in a strong growth runway for the global autonomous BVLOS drone industry, especially in areas where last-mile delivery and remote-area access are difficult to serve with conventional transport.

MARKET CHALLENGES

Reliable Detect-and-Avoid and Command-and-Control Performance Hinders Market Growth

A major challenge in the market is proving drone technology can operate beyond visual line of sight with reliable command-and-control links, safe separation logic, and dependable detect-and-avoid performance in real operating environments. Commercial demand may be rising, but BVLOS drone operations cannot scale because aircraft cannot yet consistently identify other airspace users, maintain a safe distance, or respond appropriately in mixed or less-controlled airspace. This challenge directly affects the rollout of drones for infrastructure inspections, environmental monitoring, logistics, and other large-scale missions, as safety performance must be demonstrated. The FAA’s 2025 BVLOS NPRM reflects this by building the future framework around UAS integration, third-party services such as UTM, and operational requirements for safe routine use.

Impact of the Current War

Ongoing Conflicts are Accelerating Defense-led Demand and Strengthening Market Outlook

The ongoing Russia-Ukraine war and instability in the Middle East are having a positive impact on the market, especially on the defense and security side. These conflicts have pushed drones further into frontline ISR, border surveillance, force protection, and tactical logistics, raising demand for systems that can operate beyond visual line of sight with greater autonomy, enhanced sensing, and longer mission endurance. These conflicts are not just increasing the procurement of air vehicles but also boosting demand for payloads, software, communications links, and mission systems tied to BVLOS drone operations. It is also supporting Europe and the Middle East as more strategically important regions in the global autonomous BVLOS drone industry.

- In April 2025, SIPRI reported that world military expenditure reached USD 2.718 trillion in 2024, up 9.4% year over year, with spending in Europe rising 17% and the Middle East rising 15%. SIPRI clearly linked these increases to the Russia-Ukraine war and rising regional tensions, making this a strong market-support point for higher defense-driven demand in the autonomous BVLOS drone space.

Segmentation Analysis

By Platform Type

Rotary-Wing Segment Dominated Market Due to Vertical Take-off Flexibility and Mission Versatility

By platform type, the market is categorized into fixed-wing, rotary-wing, and hybrid VTOL.

Rotary-wing platforms dominated the autonomous BVLOS drones market share in 2025, as they are easier to deploy from confined sites, can hover for detailed data capture, and are well-suited for repeatable BVLOS drone operations such as infrastructure inspections, surveying, public safety, and security monitoring. The FAA’s proposed BVLOS framework is aimed at routine, scalable operations, including package delivery, agriculture, aerial surveying, and civic-interest missions. This operating outline continues to favor rotary-wing systems where controlled take-off, landing, and stationary observation are critical.

- In March 2024, DJI launched DJI Dock 2 with the Matrice 3D/3TD platform and said automated aerial missions could be managed through cloud-based operations for surveying, inspections, asset management, and security.

The hybrid VTOL segment is expected to grow at a CAGR of 19.5% over the forecast period.

By Range Class

Short-Range (< 25 km) Segment Dominates Market Due to High Deployment Flexibility and Strong Fit for Localized Commercial Missions

On the basis of range class, the market is classified into short-range (< 25 km), medium-range (25 km to 150 km), and long-range (>150 km).

The short-range (< 25 km) segment dominated the market in 2025, as most current BVLOS drone operations focus on localized, repeatable missions rather than long-haul flights. This range band is most practical for infrastructure inspections, utility checks, site security, public-safety response, precision agriculture, and short-hop delivery, where operators need frequent maneuvers, controlled takeoffs and landings, and consistent turnaround rather than maximum endurance. It aligns well with regulators' framing of routine operations; for instance, the FAA’s BVLOS proposal is built around scalable low-altitude missions such as package delivery, agriculture, aerial surveying, and civic-interest uses, which naturally support stronger near-term demand for short-range systems.

The long-range (>150 km) is expected to show the fastest growth, registering a CAGR of 16.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion type

Battery-electric Segment Dominates Market Due to Lower Operating Complexity and Strong Fit for High-frequency Commercial Missions

By propulsion type, the market is divided into battery-electric, hybrid-electric, fuel-powered/ICE, and hydrogen fuel-cell.

The battery-electric segment held the largest global market share in 2025, as most current BVLOS drone operations are concentrated in short- to medium-range missions where ease of propulsion system integration, lower maintenance, and easier deployment matter more than maximum endurance. Battery-electric systems are well suited for infrastructure inspections, environmental monitoring, surveying, public safety, and precision agriculture. In these applications, operators need repeatable flights, fast turnaround, and predictable operating costs.

The hydrogen fuel cell segment is the fastest-growing and is expected to grow at a CAGR of 23.4% over the forecast period.

By Application

Inspection & Monitoring Segment Led Market Due to Recurring Enterprise Demand and Strong Suitability for Data-driven Field Operations

Based on application, the market is segmented into inspection & monitoring, surveying & mapping, agriculture, cargo & medical delivery, defense ISR/reconnaissance, and others.

The inspection & monitoring segment dominated the global market in 2025, as it is the most practical and repeatable use case for flights conducted beyond visual line of sight. Utilities, energy operators, transport networks, industrial sites, and critical infrastructure owners increasingly use BVLOS drones to inspect assets across wider areas more frequently, with less manual effort and more consistent data capture. Compared with many other applications, inspection missions solve a clear operational problem such as reducing inspection time, improving worker safety, and enabling continuous asset visibility. As a result, this segment is the strongest near-term revenue contributor across the global market.

Cargo & medical delivery is the fastest-growing segment in the market and is expected to grow at a CAGR of 19.6% during the forecast period.

By End User

Commercial Enterprises Segment Dominated Market Due to Recurring Business Use Cases and Clearer Commercial Scaling Potential

Based on end user, the market is segmented into commercial enterprises, civil government & public safety agencies, and defense & military users.

The commercial enterprises segment held the largest global market share in 2025, as private operators have the path to monetizing routine BVLOS drone operations across infrastructure inspections, aerial surveying, asset monitoring, logistics, and precision agriculture. Unlike many public-sector deployments that move slowly through budget and procurement cycles, commercial users adopt BVLOS systems to reduce field time, improve data collection, and run operations at scale with greater cost efficiency. The Federal Aviation Administration (FAA) has also tied future routine BVLOS use directly to applications such as package delivery, agriculture, and aerial surveying, which reinforces that commercial enterprises remain the leading end-user group in the global market.

The defense & military users segment is expected to show the fastest market growth, registering a CAGR of 15.2% over the forecast period.

Autonomous BVLOS Drones Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Autonomous BVLOS Drones Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Dominates Market Due to Advanced Regulatory Momentum and a Large Commercial Deployment Base

North America dominates the market, as it combines strong regulatory progress with a commercially active drone operating environment. The region benefits from a deep U.S. drone industry base, a large registered commercial drone fleet, and an expanding operator ecosystem that already uses drones for infrastructure inspections, delivery, surveying, public safety, and precision agriculture. North America remains the most mature region for scaling BVLOS drone operations, leading the global market.

U.S. Autonomous BVLOS Drones Market

Given the strong contribution of North America to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 0.82 billion in 2025 and is expected to grow at a CAGR of 11.7% over the forecast period.

Europe

Europe held around 25.08% of the global market in 2025, and the region is developing through a more authorization-heavy pathway than North America. The region benefits from strong demand in infrastructure monitoring, border surveillance, public safety, and defense-linked applications. At the same time, the regulatory foundation is being shaped by the European Union Aviation Safety Agency and its specific category framework for operations that fall outside the low-risk open category. The adoption of SORA 2.5 in 2025 improves the operating framework for higher-risk drone missions, and the sharp rise in European military spending in 2024.

France Autonomous BVLOS Drones Market

The French market reached approximately USD 0.09 billion in 2025, equivalent to around 14.97% of global revenues.

Russia Autonomous BVLOS Drones Market

Russia's aggressive positioning and testing program have placed it ahead in the instant regional competition, resulting in Russia's market standing at around USD 0.15 billion in 2025, representing roughly 24.16% of global revenues.

Asia Pacific

Asia Pacific is one of the most important growth regions in the market, and is anticipated to grow at the highest CAGR of 16.2% over the forecast period. Market growth is attributed to a blend of regulatory progress, commercial experimentation, and expanding defense and logistics demand. For instance, in December 2022, Japan’s Level 4 regime, in force since December 5, 2022, opened the door to BVLOS flights over inhabited areas, subject to required approvals. That gives the region a strong platform for scale-up in inspection, delivery, agriculture, and industrial monitoring. At the same time, countries such as China, Japan, India, Australia, and South Korea continue to shape the market in different ways.

China Autonomous BVLOS Drones Market

China is experiencing rapid growth, driven by AI integration for navigation, heavy investments in smart city infrastructure, and, for military applications, with 2025 revenues standing at around USD 0.21 billion, representing roughly 30.74% of global sales.

Japan Autonomous BVLOS Drones Market

The Japanese market in 2025 stood at around USD 0.11 billion, accounting for roughly 15.86% of global revenues.

Rest of the World

The Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share. Still, it is expected to grow at a CAGR of 13.8% during the forecast period. Latin America is supported by formal civilian drone frameworks such as Brazil’s ANAC system, while the Middle East & Africa side is gaining momentum from security demand, government-led drone adoption, and real autonomous logistics deployments such as Rwanda’s expansion with Zipline. This regional block is still fragmented, but it offers a clear growth runway in inspection, mapping, delivery, and defense-linked operations as more countries move from isolated approvals toward structured operating environments.

Latin America Autonomous BVLOS Drones Market

The market in Latin America reached around USD 0.14 billion in 2025, accounting for roughly 51.64% of global revenues.

Middle East & Africa Autonomous BVLOS Drones Market

Driven by defense, oil & gas, and infrastructure inspection needs, the Middle East & Africa market stood at around USD 0.13 billion in 2025 and is expected to reach USD 0.47 billion by 2034, representing roughly 48.36% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Industry Players Emphasize Repeatable & Scaled Operations to Maintain Their Dominance

The global autonomous BVLOS drones market is led by a mix of enterprise drone companies, delivery-network operators, and defense-focused unmanned systems players. DJI remains important for inspection and survey missions through its Dock 2 and Matrice 3D/3TD platforms, while Wing, Zipline, and Amazon Prime Air are helping commercialize BVLOS delivery through real-world network expansion rather than limited pilots. These companies are pushing the market toward repeatable, scaled operations across logistics, inspections, and monitoring.

On the defense platform side, AeroVironment, Red Cat, and Draganfly are key names. AeroVironment stands out for its strong 2025 revenue and bookings, while Red Cat and Draganfly are expanding with longer-endurance, hybrid platforms suited for surveillance, mapping, and industrial missions. Overall, competition in this market is no longer based only on aircraft supply, it increasingly depends on autonomy, software, regulatory execution, and real operating scale.

LIST OF KEY AUTONOMOUS BVLOS DRONE COMPANIES PROFILED

- Northrop Grumman Corporation (U.S.)

- AeroVironment, Inc. (U.S.)

- Wing Aviation LLC (U.S.)

- Zipline International Inc. (U.S.)

- Amazon Prime Air / Amazon.com, Inc. (U.S.)

- Red Cat Holdings, Inc. (U.S.)

- Skydio, Inc. (U.S.)

- DJI (China)

- Parrot Drones SAS (France)

- Draganfly Inc. (Canada)

- ideaForge Technology Limited (India)

- Terra Drone Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The Government of Rwanda signed an expansion agreement with Zipline as the first milestone under Zipline’s USD 150 million pay-for-performance award from the U.S. Department of State, targeting nationwide autonomous logistics coverage.

- January 2026: Zipline announced it had surpassed 2 million commercial deliveries, raised more than USD 600 million, and would expand operations to Houston and Phoenix.

- August 2025: The FAA unveiled its proposed rule to normalize routine BVLOS drone operations, covering operating requirements, aircraft manufacturing, separation from other aircraft, operational authorizations, security, and record-keeping.

- June 2025: Wing and Walmart announced the world’s largest drone delivery expansion, with plans to add 100 more Walmart stores across major U.S. metros.

- June 2025: Ondas subsidiary Airobotics secured a USD 14.30 million purchase order from a major defense customer for multiple units of its Optimus autonomous drone platform.

- May 2024: Amazon said the FAA had granted Prime Air additional permissions to fly beyond visual line of sight, allowing the company to expand drone deliveries and serve more customers in the U.S.

- March 2024: DJI launched DJI Dock 2 globally with the Matrice 3D/3TD platform, positioning it as a lower-cost automated “drone in a box” solution for surveying, inspections, asset management, and security operations.

- March 2024: Red Cat announced USD 2.50 million in new contract awards from two NATO allied countries for Teal 2 drone systems, training, and accessories.

REPORT COVERAGE

The global autonomous BVLOS drones market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advances, new product launches, key industry developments, and details on strategic partnerships and mergers & acquisitions. The research report also includes a detailed competitive landscape, with information on market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.8% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform Type

|

|

By Range Class

|

|

|

By Propulsion Type

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.49 billion in 2025 and is projected to reach USD 8.07 billion by 2034.

In 2025, the market value in North America stood at USD 0.89 billion.

The market is expected to exhibit a CAGR of 13.8% during the forecast period.

The rotary-wing segment led the market by platform type.

Regulatory normalization of BVLOS operations is driving market growth.

Key players in the market include DJI, AeroVironment, Wing Aviation LLC, Zipline International Inc., Northrop Grumman Corporation, and Red Cat Holdings, Inc.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us