Belt Loader Market Size, Share & Industry Analysis, By Ownership (New Delivery, Resale, and Lease/Rent), By System (Self-Propelled, Electric, Towable, Diesel, and Others), By Weight (0-1000 Kg, 1000 – 5000 Kg, and <5000 Kg), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

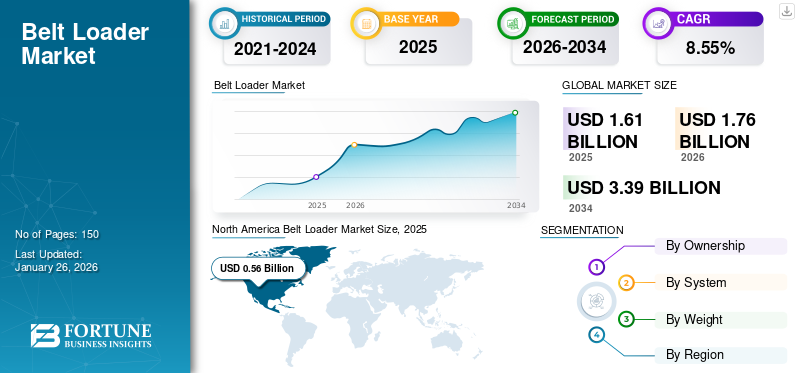

The global belt loader market size was valued at USD 1.61 billion in 2025. The market is projected to grow from USD 1.76 billion in 2026 to USD 3.39 billion by 2034, exhibiting a CAGR of 8.55% during the forecast period. North America dominated the belt loader market with a market share of 34.41% in 2025.

A belt loader is a type of ground support equipment that helps load and unload cargo and luggage in the aircraft. A loader is equipped with mechanical conveyor belts that help ease the loading and unloading of cargo and luggage. The loader is positioned at the entrance of the baggage compartment, the baggage or cargo is loaded on the belt, and it is carried to the opening where it is loaded. Loaders come in various variants, such as self-propelled, electric, towable, diesel, and gas. Textron Inc., Ersel Group, and Sinfonia are some prominent market players that provide technologically advanced, equipped, and sustainable belt loaders and are major growth enablers in the market.

The global market growth has been remarkable in terms of revenue and advancements. The booming commercial aviation market, growing adoption of advanced technology, and growing eGSE components are major factors responsible for the growth. Moreover, the growing procurement and use of military aircraft and transport applications, in turn, add up to the growth in the base year and during the forecast period.

Download Free sample to learn more about this report.

Belt Loader Market Snapshot & Highlights

Market Size & Forecast

- 2025 Market Size: USD 1.61 billion

- 2026 Market Size: USD 1.76 billion

- 2034 Forecast Market Size: USD 3.39 billion

- CAGR: 8.55% from 2026–2034

Market Share

- North America dominated the belt loader market with 34.41% share in 2025, driven by the presence of major market players, robust aviation infrastructure, and strong investments in ground support equipment modernization.

- By system, Self-propelled belt loaders accounted for the largest share in 2024 due to their high efficiency, mobility, and reduced manual labor requirements, making them ideal for modern airport operations.

Key Country Highlights

- United States: Growth driven by rising passenger air traffic post-pandemic and major investments in modernizing ground support equipment, supported by IATA-reported traffic recovery and FAA regulatory initiatives.

- China: Rapid aviation infrastructure development and expansion of air cargo services linked to e-commerce growth boost the demand for high-capacity belt loaders across major airports.

- France (Europe): Presence of leading manufacturers like TLD Group and Charlatte Manutention SA, combined with EU carbon reduction goals, supports adoption of electric and hybrid belt loaders.

- Japan: Increasing demand for advanced, eco-friendly loaders aligns with Japan’s focus on sustainable airport operations and adoption of electric belt loaders to meet emission reduction targets.

Market Dynamics

Market Drivers

Increased Passenger Air Traffic to Lead to Substantial Market Growth

In the post-pandemic scenario, there has been a rise in the number of passengers globally. Soon after the lockdown ended and the number of COVID-19 cases subsided, there has been a rise in the number of travelers across the globe. Additionally, a report by the International Air Travel Association, IATA, has mentioned that the number of travelers and the aviation industry will grow and return to pre-pandemic conditions by 2024, showcasing a full recovery from the effects of the downfall during the pandemic. Therefore, increased passenger air traffic will subsequently lead to the need for better ground support equipment, including loaders. For instance,

In April 2023, IATA International Air Transport Association unveiled a 55% growth in air traffic in February 2023 compared to February 2022. This growth is attributed to the lowered number of COVID-19 cases and subsequent ease in travel restrictions.

Market Restraints

High Cost of Operations to Restrain Market Growth

Cost is a major factor in ground support equipment operations and maintenance. The maintenance cost of a Loader is extremely high since a modern loader consists of minor components that need to be handled and maintained by professionals, and regular checks are needed. Additionally, there are numerous regulations regarding aircraft operations that need to be taken care of. Therefore, these loaders' production process is time- and cost-consuming. On the other hand, procurement is complex due to the supply backlog and the high cost of the loader. The price is high since a loader has a long life of 10 to 15 years. The procurement and maintenance process is not cost-effective for the airline and aircraft operators, thus hindering the belt loader market growth.

MARKET OPPORTUNITIES

Emergence of Self-propelled Belt Loaders to Act as a Major Market Opportunity

Automated belt loaders are advanced ground support equipment that efficiently unloads luggage and freight on and off planes. They are versatile equipment with a conveyor belt mechanism that is retractable or extensible to adjust for various planes' heights. Powered by diesel, electricity, or hybrid engines, they ensure mobility and convenience in use in conformity with environmental policies. Key design features encompass variable conveyor heights, ergonomically positioned controls, and features ensuring safety to minimize manual handling hazards. Machines, such as the KLS-6, ensure straightforward accommodation of multiple aircraft types. By automating the loading process, self-powered belt loaders play an important role in lowering airport turnaround time, consequently leading to enhanced operational effectiveness and savings for the airlines. Together, these loaders represent a critical component of ground support equipment to ensure the safety and efficiency of airplane operation and efficient airport logistics.

Market Challenges

Stringent Regulations to Challenge Market Development

One of the most considerable challenges facing the belt loader market is that it must meet extremely high-level regulations. These include safety, environmental, and operational efficiency. For instance, airports must meet emission standards and noise reduction, which can be achieved by utilizing electric or hybrid belt loaders. Compliance with such regulations could necessitate heavy investment in new technology or even remodeling current equipment. It could be costly, time-intensive, and affect the profitability of organizations involved in the belt loaders business. Such regulations must be complied with to retain working licenses and avoid legal recourse.

Belt Loader Market Trends

Emergence of Sustainable Ground Support Systems to Act as Major Market Trends

There has been a recent surge in research and development for developing sustainable, eco-friendly ground support equipment, including loaders. Carbon emissions from aviation have caused much harm to the environment, leading to various actions by airport and aviation authorities worldwide to develop initiatives and rules to reduce carbon emissions. Since authorities have initiated work toward reducing carbon emissions, many GSE OEMs have joined hands to develop sustainable and eco-friendly solutions for ground support handling to cater to sustainability regulations and decrease the overall carbon footprint. Additionally, since eco-friendly GSE ensures operator cost savings, demand for sustainable ground support systems has risen.

- North America witnessed belt loader market growth from USD 0.48 Billion in 2023 to USD 0.52 Billion in 2024.

In March 2024, Mallaghan, one of the world's premier airport ground support equipment (GSE) suppliers, engineered, developed, and launched the SkyBelt. This highly proficient, new conventional belt loader leverages decades of experience and focused research and development with major worldwide partners. Featuring a patented lifting system and an extensive range of sophisticated sensor systems, this latest product significantly minimizes the risk of unintentional damage to aircraft throughout ground handling.

Download Free sample to learn more about this report.

Impact of COVID-19

The COVID-19 pandemic, which started in December 2019 in Wuhan, China, drastically impacted the global economy, subsequently causing a major impact on the global aviation industry. The disruption in the supply chain and shortage of skilled labor amid the pandemic led to delays in aircraft deliveries, thus creating a load of backlogs with OEMs and making the aircraft manufacturing industry the worst hit by the pandemic. The worldwide lockdown has also left the aviation sector with crippled aircraft deliveries. Since airport operations were stopped entirely during the COVID-19 pandemic, it has hugely impacted the overall ground support equipment market, hampering its growth. However, it has been noted that the aviation industry is expected to recover bout 80% to pre-pandemic numbers by 2023.

- For instance, in May 2022, ICAO International Civil Aviation Authority unveiled that air traffic is all set to return to pre-pandemic levels by 80%.

Segmentation Analysis

By Ownership

Growing Global Trade to Propel New Delivery Segment Growth

Based on the ownership, the market has been segmented into new delivery, resale, and lease/rent.

The new delivery segment is expected to hold the dominant market share 54.36% in 2026 over the forecast period owing to a supply backlog created in the aftermath of the pandemic. However, the market is expected to grow exponentially due to the emergence of new airlines and growing passenger air traffic. The increase in new belt loader deliveries is fueled by growing demand for effective material handling. Growing global trade and air traffic volumes necessitate effective systems to handle cargo and baggage; hence, these loaders are crucial to streamline operations. Moreover, technological innovations and automation have increased the popularity of these loaders. Self-propelled versions, for example, enhance efficiency and save labor by automating processes, which makes them appealing to companies looking to upgrade their handling and logistics operations. This blend of automation and efficiency underpins new belt loaders in different industries.

The lease/rental segment is expected to grow at the highest CAGR over the forecast period owing to the growing preference of airport operators and airlines and the high procurement and maintenance cost. Leasing or renting belt loaders has substantial cost advantages. Renting saves money by avoiding a huge initial investment, enabling companies to control cash flow better. This method keeps capital available for other operational requirements. Leasing also provides flexibility and scalability. It allows companies to vary equipment capacity according to shifting operational requirements, such as short-term spikes in baggage handling. This adaptability is especially valuable for seasonal variances or unplanned spikes in activity, providing that companies may effectively handle their operations without getting tied into unused equipment expenses.

By System

Growth of the Aviation Infrastructure Augmented Self-propelled Segment Growth

Based on the system, the market is classified into self-propelled, electric, towable, diesel, and others.

The self-propelled segment is expected to account for the largest market share of 35.43% in 2026. owing to a strong market presence and relevance. Since self-propelled loaders offer remote access and benefits such as automated luggage transfer and efficiency in transfer, they require less manual effort, which airline operators highly demand. The growth of aviation infrastructure contributes primarily to developing self-propelled belt loaders. As airports globally modernize, there is greater demand for effective ground-handling equipment. Self-propelled belt loaders are best suited for such settings as they can work independently and move around congested areas. This makes them most suitable for congested airports where conventional equipment is less effective. The demand for effective baggage handling systems is complemented by the overall objective of improving passenger experience and operational efficiency, which continues to propel the use of high-tech self-propelled belt loaders in contemporary airport environments.

The electric segment is projected to register a higher CAGR during the forecast period owing to the increased integration of electronic vehicles and machinery in regular airport operations. An electric loader enables high performance and lower cost due to low fuel requirements. Additionally, infrastructural developments for Electric Vehicle (EV) charging and maintenance at the airport are going to further boost the belt loader market share over the forecast period.

- The electric segment is expected to hold a 26.12% share in 2024.

Additionally, the evolution of electrically powered belt loaders is driven by no emissions and environmental benefits. Electric loaders are emissions-free and are part of the aviation agenda for sustainability and lower carbon footprint. They also carry with them efficiency in operation and cost savings. Electric loaders are cheaper to operate than fuel-powered models as they provide immediate torque, allowing for the smooth movement of heavy loads. This reduces operating time and costs, therefore being a low-cost choice for airports willing to enhance the equipment for ground handling without degrading the environment.

To know how our report can help streamline your business, Speak to Analyst

By Weight

Growth In Commercial Usage Fueled the 1000-5000 Kg Segment Growth

By weight, the market is classified as 0-1000 kg, 1000-5000 kg, and <5000 kg.

The 1000–5000 kg segment is expected to hold a dominant market share of 46.21% in 2026. The growth is attributed to growing preference and demand for 1000-5000 kg loaders as a golden mean, providing moderate to high weight capacity. The loader can load from minimum to maximum, making it highly efficient and preferable for the operators. The 1000-5000 kg segment is also predicted to grow at the highest CAGR in the forecast period. The boost in air freight shipments supports expanding the 1000 to 5000 kg segment of belt loaders. Boosted international commerce and e-commerce have raised air cargo volumes, requiring effective handling solutions. The medium-sized loads typical in air freight operations suit belt loaders of this weight segment for loading and unloading of cargo. They assist in minimizing aircraft turnaround times and maximizing operational efficiency at airports, thus making them an essential element in the logistics chain for freight operators and airlines that deal with medium-sized volumes of cargo. This efficiency enables the fast delivery of products around the world.

The 0-1000 kg segment is expected to grow significantly in the forecast period, owing to growing numbers of chartered and small-size aircraft. These aircraft have limited passengers, thereby limiting luggage weight. The increasing demand for small aircraft drives the growth of 0-1000 kg belt loaders. A rise in charter flying and private air transport has had more small planes on the road, usually with fewer passengers and less baggage. The planes require lighter and more agile loading and unloading equipment to transfer cargo and baggage effectively. 0-1000 kg capacity belt loaders best fit this purpose, providing the flexibility and effectiveness needed for low-scale operations. This also aligns with the global trend of customized and flexible air travel gaining popularity everywhere.

Belt Loader Market Regional Outlook

In terms of geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

The Presence of Eminent Market Players Boosted Market Growth in North America

North America

North America Belt Loader Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 0.56 billion, accounting for 34.41% of the worldwide market, and is projected to grow to USD 0.6 billion in 2026. The dominance of the North American region is due to the presence of prominent market players. The presence of key market players in the region enables growth opportunities and technological advancements. North America has a well-established infrastructure and ecosystem for efficient avionics research and development and, therefore, is the dominant region. The region is expected to maintain its dominance during the forecast period. The United States market is projected to reach USD 0.48 billion by 2026.

Europe

The Europe market generated USD 0.45 billion in 2025, representing 27.89% of the global market landscape, and is expected to reach USD 0.49 billion in 2026. The European market is forecasted to achieve a higher growth rate in the coming years. Europe is expected to register remarkable growth in the market due to the growing number of air travelers and increased expenditure on aviation from regulatory authorities from major countries in the region. Market players such as BAE Systems, Cobhalm PLC, and SAFRAN are also anticipated to drive the market in the forecast period. The United Kingdom market is projected to reach USD 0.11 billion by 2026, while the Germany market is projected to reach USD 0.10 billion by 2026.

Asia Pacific

Asia Pacific contributed 31.17% to the global market in 2025, with a valuation of USD 0.5 billion, and is projected to reach USD 0.55 billion in 2026. The Asia Pacific market is forecasted to achieve the highest growth rate in the coming years. This rapid growth is due to the high demand for air cargo services due to a rapidly growing e-commerce industry and strengthening regional trade ties. The expanding aviation industry in China and India is another major factor in the region's growth. Developing economies such as India, Japan, and South Korea are big markets with a wide scope of growth. Additionally, renting/ leasing loaders is expected to boost overall market growth over the forecast period, enabling exponential growth with the highest CAGR. The Japan market is projected to reach USD 0.15 billion by 2026, the China market is projected to reach USD 0.17 billion by 2026, and the India market is projected to reach USD 0.10 billion by 2026.

Rest of the World

The rest of the world market is forecasted to achieve a higher growth rate in the coming years. The Rest of the World is set to experience significant growth during the forecast period. This growth is attributed to the growing airline industry in Latin America. Moreover, the growing procurement of business jets and commercial aircraft in the Middle East & Africa boosts market growth.

Competitive Landscape

Key Industry Players

Emerging Partnerships, Collaborations, and Acquisitions by Key Players is Propelling the Market Growth

The upcoming trends in the market are the emergence of new players and existing players indulging in collaborations, partnerships, and acquisitions. For instance, in July 2022, TLD Group partnered with BH Airport and Real Aviation to develop an all-natural turnaround that will be 100% carbon neutralized by 2050. Numerous market players have started green initiatives toward making the loaders electric and eco-friendly for sustainable operations, which is also cost-effective for the operators. These factors are expected to play a major role in boosting market growth.

List of Key Belt Loader Companies Profiled

- Aero Specialties Inc. (U.S.)

- Charlatte Manutention SA (France)

- Darmec Technologies Srl (Italy)

- ERSEL TECHNOLOGY (Turkey)

- FAST Global Solutions (WASP Inc.) (U.S.)

- JIANGSU TIANYI AVIATION INDUSTRY CORPORATION LIMITED (China)

- Sinfonia Technology Co. Ltd. (Japan)

- Textron Ground Support Equipment Inc. (U.S.)

- TLD Group (France)

- Weihai Guangtai Airport Equipment Co. Ltd. (China)

Key Industry Developments

- September 2024- Wollard International, a GSE manufacturer, unveiled their new M100e belt loader at the Europe GSE Expo. With a drawbar rating of 8,000 to 12,000 pounds, the belt loader is designed to function for two shifts without requiring a charge and is, therefore, termed of proven excellence.

- September 2024 – Power Stow, an OEM for belt loaders, unveiled a new belt loader- the tail loader. The tail loader bridges the gap between the baggage cart and the belt loader, improving operational efficiency. The tail loader helps with heavy lifting and different kinds of turning and twisting movements, improving the efficiency of baggage handling operations.

- July 2024- CVC DIF, a subsidiary of CVC Capital Partners, announced the acquisition of the leading Germany-based aviation ground support equipment leasing company- HiSERV. HiSERV is employed in GSE leasing, maintenance, and repair services through its network of workshops across European airports.

- March 2024 – Mallaghan, a pioneer belt loaders manufacturer, partnered with Delta Airlines, a prominent airline from the U.S., to provide the airlines with Mallaghan’s SkyBelt, a new-age belt loader with higher efficiency.

- April 2023 – Delta Airlines unveiled that all ground support equipment- tugs, belt loaders, and tractors at their major Delta Hub in Boston- is nearly electric, with 100% of their GSE fleet powered by electricity. This showcases a massive step toward net-zero ground operation around the world.

Report Coverage

The global market report covers an in-depth technical analysis of the market and majorly focuses on key aspects such as leading market players, COVID-19 effect on the market, , leading technological trends, and research ideology of the product. The report offers insights into the market trends and highlights, drivers, restraints, key industry developments & trends. In addition to the factors above, the report provides numerous factors that will contribute to the market's overall growth during the forecast period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.55% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Ownership

By System

By Weight

|

|

By Region

|

Frequently Asked Questions

The market was valued at USD 1.61 billion in 2025 and is projected to reach USD 3.39 billion by 2034.

The market is projected to record a CAGR of 8.55% during the 2026-2034 forecast period.

The 1000-5000 Kg weight segment accounted for a majority of the market share in 2026.

Increased passenger air traffic boosts market growth.

Textron Ground Support Equipment Inc. and TLD Group are some of the leading players in the market.

The U.S. dominated the global market in 2026.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us