Biosurgery Devices Market Size, Share & Industry Analysis, By Product Type (Hemostatic Agents, Surgical Sealants & Adhesives, Bone Graft Substitutes, Adhesion Prevention Products, and Others), By Material (Biological and Synthetic), By Application (Orthopedic Surgery, Cardiovascular Surgery, Neurosurgery, Gynecological Surgery, and Others), By End-user (Hospitals & Clinics, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

Biosurgery Devices Market Size and Future Outlook

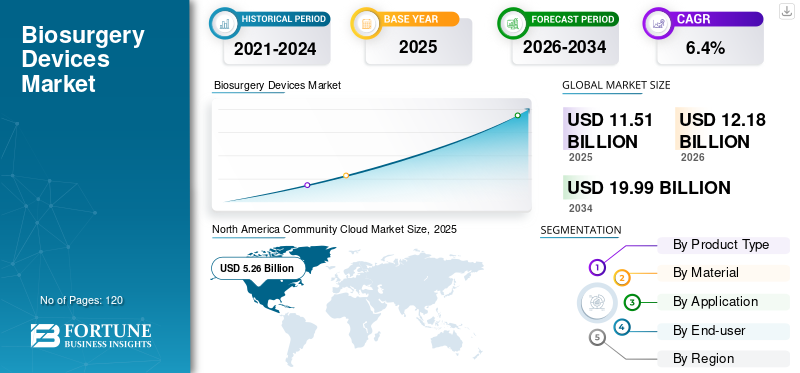

The global biosurgery devices market size was valued at USD 11.51 billion in 2025. The market is projected to grow from USD 12.18 billion in 2026 to USD 19.99 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the global biosurgery devices market with a market share of 45.7% in 2025.

The biosurgery devices include an extensive range of products that are used by healthcare professionals during and after surgical procedures. These devices play a prominent role in controlling bleeding, closing of wounds, and repairing of soft tissues, among others. The market growth is prominently attributed to a substantial rise in the number of surgical procedures per year. In addition, the growing emphasis of healthcare professionals on faster patient recovery is also projected to have a positive impact on the adoption of biosurgery devices. In addition, technological advancements coupled with a rising number of product launches are also estimated to accelerate market growth during the forecast period.

Furthermore, the market is dominated by major players, including Johnson & Johnson Services Inc., Baxter, Medtronic, BD, Integra LifeSciences, and others. These players are involved in innovations and strategic initiatives to expand their market reach.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Number of Surgical Procedures to Impact Positively on Market Growth

The steady rise in surgical procedures globally is projected to drive the global biosurgery devices market growth. A considerable number of patients need operations for cancer, heart disease, trauma, obesity, and joint problems, which increases the use of products that support safer surgery. In addition, biosurgery devices such as sealants, hemostats, and tissue repair tools help surgeons control bleeding, close wounds properly, and lower the risk of leaks or infections. Moreover, hospitals and surgeons are also emphasizing on better surgical outcomes, which also creates a lucrative environment for the adoption of biosurgery devices globally.

- For instance, according to data published by the International Society of Aesthetic Plastic Surgery (ISAPS) in June 2024, during the past 4 years, the number of aesthetic procedures grew by an estimated 40% globally.

MARKET RESTRAINTS:

Strict Regulations to Slow New Product Approvals, thereby Hampering Market Growth

Strict and time-consuming regulatory processes are considerably slowing down the product approvals and introduction. As these products are used inside the body and often interact with blood, tissue, or organs, regulators require detailed safety testing and long clinical studies. This increases development cost and delays market entry for new products. In addition, smaller companies struggle the most, as they may not have the budget or time to meet every requirement quickly. These factors are expected to hamper the market growth.

MARKET OPPORTUNITIES:

Growing Preference for Minimally Invasive Surgeries to Offer Attractive Growth Opportunities

The market is witnessing a considerable rise in minimally invasive and day-care surgeries across the globe. More procedures are now done through minimal incisions or keyholes, and patients are discharged sooner. In such cases, surgeons need products that work quickly, are easy to apply in tight spaces, and give reliable sealing or hemostasis without long operating times. Biosurgery devices that are designed for laparoscopic, robotic, and endoscopic procedures fit this need very well. They can help reduce bleeding, avoid leaks, and support faster discharge, which is important for both hospitals and patients. Moreover, introduction of such products is projected to accelerate market growth during the forecast period.

- For instance, in August 2024, Olympus Corporation announced the launch of two new jaw designs in the POWERSEAL sealer/divider product portfolio. The product offers minimized tissue sticking, which is beneficial for minimally invasive surgery.

BIOSURGERY DEVICES MARKET TRENDS:

Growing Use of Absorbable and Tissue-Friendly Materials is One of Key Market Trends

The preference and adoption of absorbable and tissue-friendly materials is increasing globally. Hospitals and surgeons are extensively preferring products that break down safely inside the body without leaving long-term residue. This reduces the chance of infections and post-surgical reactions. Moreover, new hemostats, sealants, and patches are being designed with softer, flexible, and more natural materials that blend better with human tissue. Such developments are playing a prominent role in growing emphasis on the utilization of absorbable products.

- For instance, in July 2023, Baxter announced the launch of its new PERCLOT Absorbable hemostatic powder in the U.S. market. The product is especially designed to address mild bleeding.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Storage and Handling Issues Limit Use in Busy Surgical Settings to Pose a Challenge for Market Growth

Storage and handling issues are expected to pose a considerable challenge for the market. Many sealants, patches, and hemostatic agents require controlled temperatures, careful preparation, or specific activation steps before use. Some products must be kept refrigerated, mixed quickly, or applied within a short time window. In busy surgical schedules, staff may avoid products that slow down workflow or need extra setup. If the product is not ready on time, surgeons often fall back on simpler tools they can use immediately.

Segmentation Analysis

By Product Type

Superior Treatment Outcome of Spinal Cord Stimulator to Boost Segment Growth

Based on the product type segmentation, the market is classified into hemostatic agents, surgical sealants & adhesives, bone graft substitutes, adhesion prevention products, and others.

To know how our report can help streamline your business, Speak to Analyst

The hemostatic agents segment accounted for the largest global biosurgery devices market share in 2025. The segment growth is majorly attributed to its significant utilization in all types of surgical procedures. Moreover, surgeons extensively rely on them to control bleeding quickly, whether the procedure is general, orthopedic, cardiac, spine, cancer, or trauma surgery. In addition, increasing number of product approvals and introductions is also estimated to have a positive impact on the segment growth.

- For instance, in November 2023, Johnson & Johnson Services Inc. announced approval of ETHIZIATM, an adjunctive hemostat solution to control bleeding situations.

Additionally, the surgical sealants & adhesives segment is expected to grow at a CAGR of 7.1% during the forecast period.

By Material

Stronger Biocompatibility of Biologic Material to Boost Segment Growth

Based on material, the market is segmented into biological and synthetic.

By material, the biological segment accounted for the largest share in 2025. The segment growth is majorly attributed to the superior biocompatibility offered by the biologic materials. In addition, lower risk of infections and adverse reactions is also responsible for segment growth. Moreover, they are also absorbable, which means they break down safely inside the body without needing removal. The segment is expected to hold a 65.3% share in 2026.

- For instance, in May 2025, the partnership of MTF Biologics and Kolosis BIO announced the launch of its new allograft tissues, especially designed for cardiac complex procedures.

In addition, the synthetic segment is projected to grow at a CAGR of 6.8% during the forecast period.

By Application

Substantial Prevalence of Orthopedic Disorders to Boost Segment Growth

Based on application, the market is segmented into orthopedic surgery, cardiovascular surgery, neurosurgery, gynecological surgery, and others.

In 2025, the global market was dominated by orthopedic surgery in terms of application. Certain factors, such as substantial prevalence of orthopedic conditions, technological advancements in orthopedic devices, and superior treatment outcomes of these devices, are responsible for the high share of the orthopedic surgery application segment. Also, the segment is set to hold 35.8% share in 2026.

- For instance, according to data published by the World Health Organization in July 2022, an estimated 1.71 billion people suffer from musculoskeletal conditions globally,

In addition, the cardiovascular surgery segment is projected to grow at a CAGR of 7.1% during the forecast period.

By End-user

Superior Availability of Resources in Hospitals & Clinics Drives Segment Growth

Based on end-user, the market is segmented into hospitals & clinics, academic & research institutes, and others.

In 2025, the global market was dominated by hospitals & clinics in terms of end-user. Hospitals and clinics lead the biosurgery devices market as most surgical procedures take place in these settings. Complex surgeries such as orthopedic, cardiovascular, gastrointestinal, and trauma cases need controlled bleeding, tissue repair, and wound sealing, which makes biosurgery products essential. These centers have the equipment, trained teams, and sterile environments needed to use advanced hemostats, sealants, patches, and graft materials safely. Furthermore, the segment is set to hold 64.2% share in 2026.

In addition, the academic & research institutes segment is projected to grow at a CAGR of 6.5% during the forecast period.

Biosurgery Devices Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America Community Cloud Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

NORTH AMERICA

North America held the dominant share in 2024, valuing at USD 4.97 billion, and also maintained the leading share in 2025, with USD 5.26 billion. The growth is attributed to an increasing number of surgical procedures, an aging population, and the introduction of advanced technologies. In 2026, the U.S. market is estimated to reach USD 5.24 billion.

- For instance, in August 2024, Cresilon Inc. received approval for its new product, TRAUMAGEL, for controlling moderate to severe bleeding.

EUROPE & ASIA PACIFIC

Other regions, such as Europe and the Asia Pacific, are projected to experience notable growth during the forecast period. Europe is projected to record a growth rate of 5.4%, the second-highest among all regions, and reach a valuation of USD 3.40 billion by 2026. This growth is attributed to the presence of major players in countries including Germany, the U.K., and France. Due to these factors, the U.K. is expected to record a valuation of USD 0.55 billion, Germany USD 0.76 billion, and France USD 0.45 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 2.36 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.52 billion and USD 0.78 billion, respectively, in 2026.

LATIN AMERICA and MIDDLE EAST & AFRICA

Over the forecast period, the Latin America and Middle East & Africa regions are expected to showcase moderate growth in the market. The Latin America market in 2026 is set to reach a valuation of USD 0.50 billion. The growth is attributed to increasing awareness of surgical care in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.13 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Focus on Product Launches and Approval to Strengthen Position of Key Players

In 2025, major players such as Johnson & Johnson Services Inc., Baxter, Medtronic, BD, and Integra LifeSciences accounted for the largest global biosurgery devices market share. The share is attributed to the focus of these players on innovations and other strategic initiatives, including partnerships, acquisitions, and collaborations.

Other prominent companies, such as Zimmer Biomet, Stryker, CSL Behring, B. Braun Melsungen AG, and 3M, are focused on increasing product supply to emerging countries, which is expected to help them gain a significant market share.

LIST OF KEY BIOSURGERY DEVICES MARKET COMPANIES PROFILED:

- Johnson & Johnson Services Inc. (U.S.)

- Baxter International (U.S.)

- Medtronic (Ireland)

- BD (U.S.)

- Integra LifeSciences (U.S.)

- Zimmer Biomet (U.S.)

- Stryker (U.S.)

- CSL Behring (Australia)

- B. Braun Melsungen AG (Germany)

- 3M (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: Cerapedics Inc. received FDA approval for its PearlMatrix P-15 Peptide enhanced bone graft.

- June 2024: Axogen, Inc. announced the launch of its new tissue matrix, Avive+. The newly launched product is a resorbable, multi-layer amniotic membrane allograft.

- April 2023: Olympus Corporation announced the launch of its new EndoClot hemostatic agents in Europe. The new product is especially developed for gastrointestinal procedures.

- December 2021: BD announced the acquisition of Tissuemed, Ltd. to consolidate its position in the surgical solutions market.

- January 2020: Terumo Corporation announced the launch of its new surgical sealant AQUABRID in the EMEA market. The new product is launched to prevent surgical bleeding.

REPORT COVERAGE

The global biosurgery devices market encompasses a detailed analysis of the market, including all segments. It encompasses market dynamics, including market drivers, trends, opportunities, challenges, and restraints. The report also provides key insights, including new product launches and significant industry developments, such as partnerships, mergers, and acquisitions. Additionally, the report provides a detailed profile of key players operating in the market, along with an analysis of their market share.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Product Type

By Material

By Application

By End-user

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.51 billion in 2025 and is projected to reach USD 19.99 billion by 2034.

In 2025, the market value stood at USD 5.26 billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period of 2026-2034.

The hemostatic agents segment led the market by product type.

The key factors driving the market are the increasing number of surgical procedures and technological advancements.

Johnson & Johnson Services Inc., Baxter, Medtronic, BD, and Integra LifeSciences are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us