Canine Stem Cell Therapy Market Size, Share & Industry Analysis, By Therapy Type (Autologous, Allogeneic, and Others), By Disease Indication (Orthopedic & Musculoskeletal, Dermatology & Skin Inflammation, Neurology, Immune & Inflammatory Disorders, Oral/Dental, Ophthalmic, Reproductive & Urogenital, and Others), By End User (Veterinary Specialty Hospitals, Veterinary Clinics, Veterinary Ortho/Rehab Centers, Academic & Research Institutes, Veterinary Regenerative Medicine Centers, and Others), and Regional Forecast, 2026-2034

Canine Stem Cell Therapy Market Size and Future Outlook

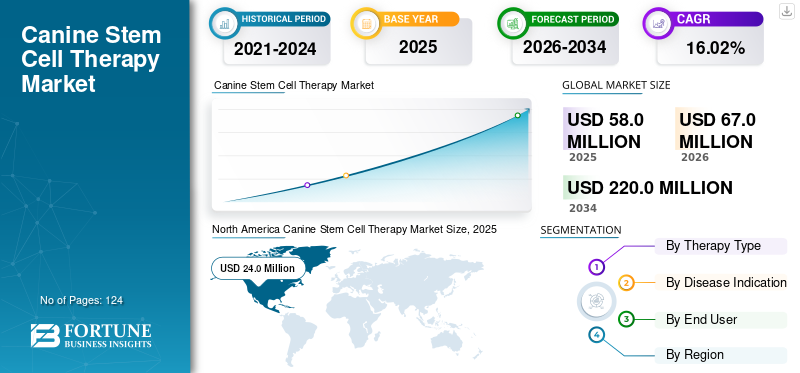

The global canine stem cell therapy market size was valued at USD 58.0 million in 2025. The market is projected to grow from USD 67.0 million in 2026 to USD 220.0 million by 2034, exhibiting a CAGR of 16.02% during the forecast period. North America dominated the canine stem cell therapy market with a market share of 41.37% in 2025.

The global market includes stem cell-based products, processing systems, banking services, and treatment methods tailored for dogs within veterinary care environments. The market is expanding, as it has become a key regenerative treatment method for minimizing inflammation, aiding tissue repair, enhancing mobility, and managing chronic conditions in dogs. The growth of the market is driven by rising pet ownership, the increasing incidence of osteoarthritis and mobility issues in pet dogs, spending on advanced veterinary care, a broader acceptance of regenerative veterinary medicine, and a rising need for advanced treatment solutions among different end users.

Key industry players, including VetStem, Inc., EquiCord, Ardent Animal Health, LLC, and Bioceltix S.A., are actively strengthening their product offerings by increasing investments in research & development.

Download Free sample to learn more about this report.

CANINE STEM CELL THERAPY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 58.0 million

- 2026 Market Size: USD 67.0 million

- 2034 Forecast Market Size: USD 220.0 million

- CAGR: 16.02% from 2026–2034

- North America dominated the canine stem cell therapy market with a 41.37% share in 2025.

- The orthopedic & musculoskeletal segment is projected to hold 72.7% of the market in 2026.

- The veterinary clinics segment is expected to account for 32.3% of the end-user market in 2026.

North America

North America the market reached USD 24.0 million in 2025, driven by high pet ownership, strong veterinary spending, and early adoption of regenerative therapies.

Europe

Europe the market is projected to grow at a 15.59% CAGR, supported by increasing acceptance of regenerative medicine and regulated stem cell products.

Asia Pacific

Asia Pacific the market is expected to reach USD 13.6 million in 2026, fueled by rising pet adoption and growing demand for advanced veterinary care.

U.S.

The market is projected to reach USD 25.6 million in 2026, supported by strong demand for regenerative treatments and advanced veterinary infrastructure.

Japan

The market is estimated to reach USD 3.4 million in 2026, driven by increasing adoption of premium pet healthcare services.

Read More

CANINE STEM CELL THERAPY MARKET TRENDS

Advancements in Cell Processing Technologies are a Significant Trend Observed in the Market

Developments in cell processing technologies are becoming a significant trend in the global market, enhancing the quality, consistency, and scalability of treatments based on stem cells. Previously, numerous canine stem cell treatments relied primarily on clinic-based or small-scale processing, hindering standardization and wider acceptance. Through enhanced cell isolation, expansion, cryopreservation, quality assessment, and GMP-compliant production, businesses can now create more dependable autologous and allogeneic treatments for dogs. This is particularly crucial for osteoarthritis and musculoskeletal issues, as veterinarians require safe, reliable, and readily available treatment choices. Enhanced processing also facilitates ready-to-use stem cell products, decreasing the time needed compared to custom cell preparation for patients. Consequently, improved processing technologies are enabling companies to shift from service-oriented regenerative therapy models to regulated, commercial veterinary biologics. This trend is anticipated to enhance acceptance in veterinary specialty hospitals, clinics, and regenerative medicine facilities, supporting the overall global canine stem cell therapy market growth.

- For instance, in March 2025, VetStem Biopharma announced that it secured strategic funding to advance the final steps toward the U.S. FDA conditional approval of StemStat Ortho, an allogeneic, off-the-shelf stem cell therapy for canine osteoarthritis.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Awareness of Regenerative Medicine for Animals to Boost Market Growth

Increasing awareness of regenerative medicine for pets is a major factor propelling the global canine stem cell therapy market, as a greater number of veterinarians and pet owners are learning about stem cell treatment alternatives beyond traditional pain management and surgical methods. Previously, numerous dog owners had a limited understanding of regenerative therapies, which resulted in their adoption being primarily confined to specialty or referral practices. Nonetheless, increasing education via veterinary hospitals, pet health platforms, clinical research, and company-driven awareness initiatives is aiding in establishing stem cell therapy as a treatment for long-standing canine ailments such as osteoarthritis, hip dysplasia, tendon injuries, and inflammation-related disorders. This heightened awareness is significant as pet owners are more frequently prepared to spend on advanced therapies that enhance mobility, comfort, and life quality in older dogs. As veterinarians gain more assurance in addressing regenerative medicine, it is anticipated that referrals and treatment numbers will rise. The trend is further backed by companies advocating for standardized, ready-to-implement stem cell therapies, which can simplify understanding and integration into regular veterinary practice.

- For instance, in April 2025, VetStem announced that it had processed over 40,000 stem cell treatments for animals across the U.S. and Canada, reflecting growing veterinarian and pet-owner trust in regenerative medicine for companion animals.

MARKET RESTRAINTS

Limited Regulatory Frameworks for Veterinary Regenerative Medicine to Hamper Market Growth

Limited regulatory frameworks for veterinary regenerative medicine act as a major restraint for the global market, as stem cell-based animal products are still regulated differently across countries. In markets such as the U.S., animal cell- and tissue-based products may be treated as new animal drugs, which requires developers to follow specific FDA expectations for safety, manufacturing, donor eligibility, and product quality. This increases development cost, documentation burden, and approval timelines, especially for smaller veterinary regenerative medicine companies. At the same time, differences between autologous clinic-based procedures and commercial allogeneic products can create uncertainty for veterinarians and product developers. Limited harmonization across regions also makes it harder for companies to launch the same canine stem cell therapy globally. As a result, regulatory complexity can slow product commercialization, limit the number of approved therapies, and restrict wider adoption across veterinary clinics and specialty hospitals.

MARKET OPPORTUNITIES

Increasing Expenditure on Veterinary Healthcare to Offer Market Growth Opportunities

Rising spending on veterinary healthcare is generating a significant market opportunity for the global market, as pet owners are investing more in advanced treatments that enhance long-term health and quality of life. Dogs are increasingly being treated as family members, prompting owners to invest more in premium therapies, specialized care, rehabilitation, and regenerative medicine. This trend is significant for canine stem cell therapy, as such treatments are often more expensive than standard medications, making adoption highly dependent on pet owners’ affordability and readiness to pay. Increasing veterinary expenditures also enables clinics and specialized hospitals to expand the availability of stem cell treatments for conditions such as osteoarthritis, hip dysplasia, ligament injuries, and chronic persistent inflammatory disorders. Increased expenditure also facilitates improved diagnostic evaluations, ongoing care, and additional treatments when necessary. Consequently, increasing spending in veterinary healthcare is helping canine stem cell therapy evolve from a niche offering into a wider specialty treatment option.

- For instance, in March 2026, the American Pet Products Association (APPA) reported that the U.S. pet industry reached USD 158 billion in 2025, showing continued growth in pet-related spending and supporting the opportunity for advanced veterinary treatments.

MARKET CHALLENGES

High Treatment Costs Pose a Major Challenge to Market Growth

Elevated treatment expenses continue to pose a significant obstacle for the worldwide canine stem cell therapy market, as these procedures are viewed as high-end veterinary services. Stem cell therapy typically includes consultation, diagnostics, anesthesia, fat or tissue harvesting, lab processing, cell injection, follow-up care, and occasionally rehabilitation, raising overall expenses for pet owners. In addition, many pet insurance providers offer limited or conditional coverage for regenerative therapies, increasing out-of-pocket costs and restricting adoption, particularly in price-sensitive markets. This challenge is more pronounced in chronic conditions such as osteoarthritis, where dogs might require long-term care and repeated treatments. Elevated expenses can restrict access primarily to specialized hospitals, referral facilities, and pet owners with greater financial means. Consequently, despite growing clinical interest, elevated costs continue to hinder broader adoption across general veterinary practices. Lowering processing expenses, expanding insurance coverage, and developing ready-to-use treatment solutions will therefore be crucial to improve affordability and support wider market acceptance.

- For instance, in August 2025, Elita Genetics launched Australia’s first commercial pet stem cell banking service and highlighted that Australian dog owners spend about USD 2,500 per year on arthritis management, with some claims reaching up to USD 40,000. This shows the substantial long-term cost burden associated with advanced veterinary care while also demonstrating growing interest in alternative regenerative treatments.

Segmentation Analysis

By Therapy Type

Greater Acceptance Among Veterinarians Boosted Autologous Segment Growth

In terms of therapy type, the market is divided into autologous, allogeneic, and others.

The autologous segment held the dominant global canine stem cell therapy market share in 2025. This dominance is primarily attributed to the widespread commercial use of stem cells derived from the same dog, commonly from adipose/fat tissue. This approach is widely preferred as it reduces concerns related to donor-cell rejection, immune reaction, and disease transmission. Additionally, autologous therapy has gained stronger acceptance among veterinarians as it has been used for years in dogs with arthritis, tendon injuries, ligament injuries, and other orthopedic conditions. The availability of established sample collection, processing, cryopreservation, and reinjection workflows has also supported its higher adoption in veterinary clinics and specialty hospitals. Moreover, as canine osteoarthritis and mobility-related disorders remain among the most common treatment areas, patient-specific autologous stem cell therapies continue to capture a major share of the market.

- For instance, in February 2024, VetStem announced that it had processed over 16,000 patient samples and offered more than 38,000 stem cell treatments for animals across the U.S. and Canada. The company’s adipose-derived regenerative cell therapy model supports the strong commercial use of autologous stem cell therapy in veterinary regenerative medicine.

The allogeneic segment is anticipated to grow at a CAGR of 20.72% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

High Burden of Joint Disorders Supported the Orthopedic & Musculoskeletal Segment Growth

On the basis of disease indication, the market is divided into orthopedic & musculoskeletal, dermatology & skin inflammation, neurology, immune & inflammatory disorders, oral/dental, ophthalmic, reproductive & urogenital, and others.

In 2025, the orthopedic & musculoskeletal segment led the market. This is owing to the fact that most canine stem cell therapy procedures are used for joint pain, osteoarthritis, hip dysplasia, elbow dysplasia, tendon injuries, and ligament injuries. These conditions are very common in aging dogs and large breeds, creating a larger treatment pool than many other indications. Stem cell therapy is gaining adoption in these cases as it can help reduce inflammation, support tissue repair, and improve mobility when conventional medicines or surgery are not enough. Veterinary clinics and specialty hospitals also have more established treatment protocols for orthopedic use compared with newer areas such as neurology or ophthalmology. Additionally, pet owners are more likely to choose advanced therapy when mobility loss directly affects the dog’s daily activity and quality of life. Thus, the high disease burden and stronger clinical use in joint-related conditions continue to support the dominance of this segment. Furthermore, the segment is set to hold 72.7% share by 2026.

- For instance, in June 2025, Fitzpatrick Referrals highlighted stem cell therapy as a treatment option for dogs suffering from moderate to severe osteoarthritis, especially for patients that are not suitable candidates for surgery or do not respond effectively to conventional medicines.

The dermatology & skin inflammation segment is anticipated to rise with a CAGR of 24.44% over the forecast period.

By End User

Veterinary Clinics Segment Led due to Easier Treatment Coordination

Based on end user, the market is segmented into veterinary specialty hospitals, veterinary clinics, veterinary ortho/rehab centers, academic & research institutes, veterinary regenerative medicine centers, and others.

The veterinary clinics segment dominated the market in 2025. These clinics have a wider reach compared with specialty hospitals, making them the most accessible point for diagnosis, referral, sample collection, and treatment follow-up. Many stem cell therapy workflows, especially autologous fat-derived therapies, can be coordinated through clinics with support from external processing laboratories. This makes it easier for veterinarians to offer regenerative treatment without building full in-house cell processing facilities. In addition, growing awareness among pet owners is encouraging clinics to add advanced therapies alongside pain management, rehabilitation, and surgery support. Thus, broad clinic availability, regular patient flow, and easier treatment coordination continue to support the dominance of this segment. Furthermore, the segment is set to hold 32.3% share by 2026.

- For instance, in March 2026, Gallant announced a partnership with MWI Animal Health to deliver its anticipated FDA conditionally approved, off-the-shelf stem cell therapy to veterinary clinics through a clinic-friendly fulfillment model.

The veterinary ortho/rehab centers segment is projected to grow at a CAGR of 17.68% during the forecast period.

Canine Stem Cell Therapy Market Regional Outlook

By geography, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Canine Stem Cell Therapy Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America region dominated the global market at USD 20.9 million in 2024 and maintained its dominance at USD 24.0 million in 2025. Factors such as high pet ownership, strong spending on companion animal healthcare, and early adoption of regenerative veterinary treatments are boosting the growth of the market.

U.S. Canine Stem Cell Therapy Market

The U.S. market led the North American region and is projected to be approximately USD 25.6 million by 2026, representing about 38.2% of the global market sales.

Europe

Europe market is expected to be growing at a CAGR of 15.59% during the forecast period. The region is growing steadily due to increasing acceptance of regenerative medicine in veterinary care and the presence of regulated stem cell products for canine osteoarthritis. The region also benefits from rising awareness among veterinarians about cell-based therapies for orthopedic and inflammatory conditions.

U.K. Canine Stem Cell Therapy Market

The U.K. market is estimated to reach around USD 3.8 million by 2026, representing roughly 5.6% of global revenues.

Germany Canine Stem Cell Therapy Market

Germany’s market size is projected to reach approximately USD 4.3 million by 2026, equivalent to around 6.4% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach USD 13.6 million by 2026. The region is expected to show strong growth due to rising pet adoption, increasing disposable income, and growing spending on premium veterinary care. Additionally, markets such as Japan, China, South Korea, Australia, and India are witnessing higher demand for advanced pet healthcare services, in turn driving market growth.

Japan Canine Stem Cell Therapy Market

The Japanese market is estimated to reach around USD 3.4 million by 2026, accounting for roughly 5.0% of global revenues.

China Canine Stem Cell Therapy Market

China’s market is projected to reach around USD 4.3 million by 2026, representing roughly 6.5% of global sales.

India Canine Stem Cell Therapy Market

The Indian market is estimated to touch around USD 1.4 million, accounting for roughly 2.1% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are anticipated to witness moderate growth in the coming years. The growth of the market is driven by rising companion animal ownership, rising premium veterinary care demand, and gradual improvement in veterinary healthcare infrastructure. The Latin American market is estimated to reach around USD 3.8 million by 2026.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 1.2 million by 2026, representing about 1.8% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Ready-To-Use Allogeneic Therapies to Boost Their Product Portfolios

The global canine stem cell therapy market is moderately consolidated, with a limited number of specialized players holding strong positions in stem cell processing services, regenerative therapy platforms, and allogeneic product development. Some of the leading players include VetStem, Inc., EquiCord, Ardent Animal Health, LLC, and Bioceltix S.A. These companies are focusing on autologous stem cell processing, cell banking, ready-to-use allogeneic therapies, and clinical research for osteoarthritis, tendon injuries, skin inflammation, and other canine conditions.

- For instance, in October 2023, Athersys licensed its animal health assets, including MAPC technology for canine, feline, and equine health applications, to Ardent Animal Health, LLC, to accelerate the development of regenerative medicine solutions for joint disease and other unmet needs in animal health.

Other notable industry participants include StemcellX, Cell Therapy Sciences Ltd., Animacel, Enovis (Companion Animal Health), and JangoPet, LLC. These firms are expected to strengthen their market presence as demand rises for advanced, non-surgical, and clinic-accessible stem cell therapies for dogs.

LIST OF KEY CANINE STEM CELL THERAPY COMPANIES PROFILED

- VetStem, Inc. (U.S.)

- EquiCord (Spain)

- Ardent Animal Health, LLC (U.S.)

- Bioceltix S.A. (Poland)

- Gallant (U.S.)

- StemcellX (U.K.)

- Cell Therapy Sciences Ltd. (U.K.)

- Animacel (Slovenia)

- Enovis (Companion Animal Health) (U.S.)

- JangoPet, LLC. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Bioceltix reported long-term follow-up results for BCX-CM-AD, its stem cell-based therapy for canine atopic dermatitis, showing that the therapeutic effect was maintained for at least 6 months in nearly half of treated dogs.

- February 2026: Bioceltix received environmental approval for a new large-scale stem cell manufacturing facility in Wrocław. The facility is planned to support commercial production of its ALLO-BCLX-based veterinary biologics, including therapies for canine osteoarthritis and canine atopic dermatitis.

- October 2025: Gallant highlighted its ongoing investigation of uterine-derived mesenchymal stromal cells for canine osteoarthritis, with pilot studies evaluating the safety and effectiveness of intravenous allogeneic stem cells for dogs with OA.

- August 2025: Bioceltix announced successful final clinical trial results for BCX-CM-AD in dogs with atopic dermatitis. The study confirmed the therapy’s safety and efficacy across short, medium, and long-term evaluation periods. The company also stated that it was preparing to submit BCX-CM-AD to the EMA for regulatory approval.

- June 2025: Gallant closed USD 18 million Series B financing to advance ready-to-use stem cell therapies for pets.

REPORT COVERAGE

The global canine stem cell therapy market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, and key developments in the industry. The global report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.02% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Therapy Type, Disease Indication, End User, and Region |

| By Therapy Type |

|

| By Disease Indication |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 58.0 million in 2025 and is projected to reach USD 220.0 million by 2034.

In 2025, the market value stood at USD 24.0 million.

The market is expected to exhibit a CAGR of 16.02% during the forecast period.

By therapy type, the autologous segment led the market.

Growing awareness of regenerative medicine for animals is a key factor driving market expansion.

VetStem, Inc., EquiCord, Ardent Animal Health, LLC, Bioceltix S.A., and Gallant are the top players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 124

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us