Circuit Breaker for Data Centers Market Size, Share & Industry Analysis, By Type (Low Voltage Circuit Breakers and Medium Voltage Circuit Breakers), By Data Center Type (Hyperscale, Colocation, and Enterprise), Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

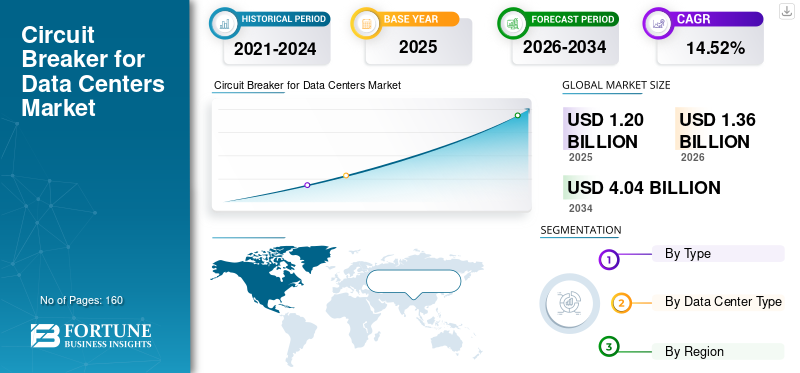

The global circuit breaker for data centers market size was valued at USD 1.20 billion in 2025. The market is projected to grow from USD 1.36 billion in 2026 to USD 4.04 billion by 2034, exhibiting a CAGR of 14.52% during the forecast period. North America dominated the global circuit breaker for data centers market with a share of 40.83% in 2025.

The global transition toward high-performance computing, AI training clusters, liquid-cooled server architectures, and electrical systems is creating a new wave of electrical complexity inside data centers, directly leading to increased demand for advanced circuit breakers. AI racks consuming 30–120 kW each and in some hyperscale deployments surpassing 150 kW, require stronger protection systems capable of handling higher currents, faster fault-clearing, and tighter selective coordination.

Liquid-cooled environments add further electrical protection needs, including enhanced insulation, moisture-resistant components, and breakers with higher endurance against rapid load fluctuations.

- For instance, in March 2025, NVIDIA revealed its upcoming “Kyber” NVL576 rack design, each rack expected to draw up to 600 kW of power, roughly five times the current generation’s ~120 kW. This dramatic increase in rack power density forces data-centre operators to deploy circuit breakers capable of handling higher currents, faster fault interruption, and enhanced monitoring. The shift to megawatt-scale server racks underscores why traditional breaker systems fall short, and why the data-centre segment is specifying premium, digitally-enabled, high-capacity protection hardware rather than generic equipment.

Schneider Electric leads the data center circuit breaker market with highly reliable, energy-efficient protection systems. Eaton follows closely with scalable, robust solutions suited for modular and high-load environments. Siemens offers digitally connected, industrial-grade breakers that enhance monitoring and automation, while ABB provides compact, high-performance circuit breakers designed to minimize downtime in mission-critical data center operations.

Download Free sample to learn more about this report.

CIRCUIT BREAKER FOR DATA CENTERS MARKET TRENDS

Shift to High Capacity and Smart LV and MV Circuit Breakers are Key Market Trends

Circuit breakers used in data centers are evolving rapidly as facilities adapt to extreme power densities, AI workloads, and increasingly complex electrical architectures. One major trend is the shift toward high-capacity LV and MV breakers that can withstand higher fault currents driven by large power blocks, higher-rated UPS systems, and megawatt-scale AI clusters.

Data centers are also adopting smart and connected breakers equipped with digital trip units, thermal monitoring, and event-logging to support predictive maintenance and faster fault isolation, critical for maintaining uptime in 24/7 environments. Another clear trend is the rise of arc-flash mitigation technologies, including zone-selective interlocking, fast-acting relays, and solid-state switching elements, which help operators meet stricter safety requirements while keeping equipment energized. Circuit breakers for data centers are vital as they support reliable power distribution while enabling advanced energy management across high-density digital infrastructures.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Increase in Data Centre Power Demand Fuels Market Expansion

The rapid growth of digital infrastructure and artificial intelligence (AI) workloads is rapidly transforming the scale of data-centre power demand, placing unprecedented strain on power-distribution systems and driving higher specification requirements for circuit breakers. In the U.S., data-centre electricity usage climbed from approximately 58 TWh in 2014 to 176 TWh in 2023, more than tripling over the decade. These factors are driving the circuit breakers for data centers market share.

As rack densities surge (often 20-50 kW per rack or higher) and redundancy architectures evolve toward N+1 and 2N, data-centre operators must deploy a far greater number of medium- and low-voltage circuit breakers including higher breaking-capacity models, with digital monitoring capabilities.

In addition, the explosive growth of AI, cloud services, and digitalisation is pushing global data-centre power demand into unprecedented territory, with the International Energy Agency projecting consumption to more than double to ~945 terawatt-hours (TWh) by 2030, up from about 415 TWh in 2024.

MARKET RESTRAINTS

Grid Connection Bottlenecks and Electrical Infrastructure Delays Hinder Market Expansion

A major restraint in the circuit breakers for data centers market growth is the growing difficulty in securing timely grid connections and upgrading surrounding electrical infrastructure. Across major data-center hubs, including Northern Virginia, Dublin, Frankfurt, Singapore, and parts of Japan, utilities are experiencing multi-year backlogs for high-capacity power delivery.

These delays slow down new data-center construction, reduce the pace of electrical fit-outs, and directly limit procurement cycles for medium-voltage and low-voltage circuit breakers. In several U.S. regions, utilities have warned that new data-centre connections may take 4–6 years due to substation saturation and the need for extensive transmission upgrades.

MARKET OPPORTUNITIES

Transition to High-Efficiency, AI-Optimized Electrical Architectures, and Smart Circuit Breakers Drive Growth Opportunities

A major opportunity for circuit breakers in data centers lies in the industry’s accelerating shift toward next-generation electrical architectures designed to support AI workloads, higher rack densities, and improved energy efficiency. As hyperscale operators deploy 800V–1,500V power distribution, liquid-cooled GPU clusters, and modular power blocks, demand is rising for advanced circuit breakers with higher breaking capacity, arc-flash mitigation, and integrated digital intelligence.

These new architectures require breakers capable of handling rapid load fluctuations, higher fault currents, and tighter selective coordination, conditions under which traditional mechanical breakers are no longer sufficient. The move toward modular, prefabricated power systems presents another opportunity. Many hyperscale campuses now deploy prefabricated MV/LV power skids, each integrating switchgear, UPS units, busways, and high-performance circuit breakers. This model significantly increases volume demand for standardized, factory-assembled breaker systems.

MARKET CHALLENGES

Managing Extremely High Fault Currents Presents Significant Challenges for Market Growth

Circuit breakers for data centers face several emerging technical and operational challenges as facilities scale toward multi-megawatt power blocks and AI-driven densities. One of the primary issues is managing extremely high fault currents generated by large UPS systems, short conductor runs, and dense transformer arrangements.

Traditional LV breakers often struggle to provide selective coordination under these conditions, creating risks of nuisance tripping or cascading outages. Integrating breakers into hybrid electrical architectures, including AC-DC mixed distribution, 800-V power systems, and high-frequency converter-based setups, adds complexity, as many designs push beyond the tested limits of conventional protection equipment.

Segmentation Analysis

By Type

Low Voltage Circuit Breakers Dominate as they are Majorly Used Across Data Centers

On the basis of type, the market is classified into low voltage circuit breakers and medium voltage circuit breakers. In 2025, the low voltage circuit breakers segment dominated the market share. Low voltage segment dominated as many existing data-center electrical architectures still rely heavily on 480/415V AC distribution, with thousands of MCCBs and ACBs deployed across PDUs, RPPs, UPS output panels, and busway feeders. A typical 30–60 MW hyperscale campus contains 5,000–12,000 LV breakers, compared with only 40–120 medium-voltage (MV) breakers at the substation and main distribution level.

The medium voltage circuit breakers segment is experiencing significant growth and is expected to grow at a CAGR of 11.42%.

To know how our report can help streamline your business, Speak to Analyst

By Data Center Type

Hyperscale Data Centers Leads as they Deliver Massive, Scalable, and Highly Efficient Computing Power

On the basis of data center type, the market is categorized into hyperscale, colocation, and enterprise. In 2025, the hyperscale segment dominated the global market as cloud and AI providers now operate facilities that range from 50 MW to 200+ MW per campus, far larger than traditional data centers. A single hyperscale campus can contain numerous servers, requiring massive electrical infrastructure, including thousands of LV breakers and dozens of MV breakers per block. U.S. regions such as Northern Virginia alone host over 2.5 GW of hyperscale capacity, exceeding the entire data-center capacity of several countries.

The colocation segment is expected to grow at a CAGR of 14.08% over the analysis period.

Circuit Breaker for Data Centers Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America held the dominant share in 2025, valued at USD 0.49 billion, and also took the leading share in 2026 with USD 0.56 billion. North America, especially the U.S., is undergoing a structural shift in data-center electrical design, reshaping demand for advanced circuit breakers. A defining trend is the rise of AI and GPU-dense campuses, where individual buildings now reach 80–150 MW, and entire campuses exceed 300–600 MW.

These facilities produce extremely high fault-current levels, pushing operators to adopt high-interrupting-capacity LV ACBs, MCCBs above 65–100 kA, and MV vacuum breakers designed for rapid clearing and arc-flash mitigation. Data-center clusters in Northern Virginia, Columbus, Phoenix, and Dallas are also requiring more MV switchgear per megawatt because utilities are delivering power at higher voltages (13.8 kV, 24 kV, and 35 kV) to handle load growth.

U.S. Circuit Breaker for Data Centers Market

Based on North America’s strong contribution and the dominance of the U.S. within the region, the U.S. market can be analytically approximated at around USD 0.41 billion in 2025, accounting for roughly 34.11% of the global market size.

Europe

Europe is projected to record a growth rate of 12.60% in the coming years, which is the third highest among all regions, and reached USD 0.29 billion by 2025. Circuit breaker demand in European data centers is being reshaped by a combination of grid-stress conditions, environmental regulations, and space-constrained facility designs. Major hubs such as Frankfurt, Amsterdam, and Dublin are operating under tight power-availability constraints, which require breakers with exceptionally high interrupting capacity and fast isolation capability to manage rising fault-current levels within dense transmission corridors.

U.K. Circuit Breaker for Data Centers Market

The U.K. market size in 2025 was at USD 0.079 billion 2025 and is estimated at USD 0.26 billion for 2034, representing roughly 6.53% of the global revenue.

Asia Pacific

Asia Pacific’s market size was USD 0.35 billion in 2025 and secured the second position in the market. India and China’s market values for 2025 are USD 0.073 billion and USD 0.12 billion respectively. The circuit breaker demand in Asia Pacific data centers is being reshaped by the region’s distinct electrical environments, rapid hyperscale expansion, and diverse grid characteristics.

Japan Circuit Breaker for Data Centers Market

Japan’s market in 2025 was USD 0.06 billion, accounting for roughly 4.59% of global circuit breaker for data centers revenues. Demand for circuit breakers in Japan is high due to rapid digital infrastructure expansion, strict reliability standards, and increasing power loads driven by cloud computing and AI adoption.

China Circuit Breaker for Data Centers Market

In 2025, China’s market revenues were estimated around USD 0.12 billion, representing roughly 9.61% of the global market.

India Circuit Breaker for Data Centers Market

India’s market in 2025 was at USD 0.072 billion, accounting for roughly 6.02% of global revenues.

Rest of the World

The rest of the world region is expected to witness moderate growth during the forecast period and its market size in 2025 was valued at USD 0.076 billion. The demand for circuit breakers in data centers is increasing because modern facilities are shifting toward high-density electrical architectures that place significant stress on protection systems at both low-voltage (LV) and medium-voltage (MV) levels.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors are Actively Expanding Their Market Share Via Partnership, Business Expansion, And Technological Advancements

The global circuit breaker for data centers market holds a semi-consolidated structure, constituting prominent players such as Eaton, Schneider Electric, ABB, Siemens AG, GE Vernova, and others. Companies operating are adopting targeted growth strategies focused on strengthening technical capability, expanding manufacturing presence, and improving access to high-demand sectors.

- In October 2025, ABB launched AI-ready power solutions (MNS with SACE Emax 3 ACBs) aimed specifically at large data centers, and is collaborating with Nvidia on 800 VDC power architectures for gigawatt-scale AI data centers.

Other notable players include Mitsubishi Electric Corporation, Toshiba, Larsen & Toubro, and Atom Power Inc. These companies are expected to prioritize new product launches and collaborations to increase their market share.

LIST OF KEY CIRCUIT BREAKER FOR DATA CENTERS COMPANIES PROFILED:

- ABB (Switzerland)

- GE Vernova (U.S.)

- Schneider Electric (France)

- Eaton (Ireland)

- Siemens AG (Germany)

- Mitsubishi Electric Corporation (Japan)

- Toshiba (Japan)

- Larsen & Toubro (India)

- Atom Power Inc. (U.S.)

- CHINT Group (China)

KEY INDUSTRY DEVELOPMENTS

- July 2025: ABB launched its latest SACE Emax 3, which is intended to address growing concerns about grid stability, cybersecurity, and the soaring power demands of Artificial Intelligence (AI) in data centers. It is designed specifically for large facilities with high power demands, such as data centers, advanced manufacturing sites, hospitals, and airports.

- July 2025: Schneider partnered with NVIDIA to design energy/power infrastructure for AI data centers, circuit breakers implied in power distribution systems.

- April 2025: GE Vernova’s Charleroi, PA plant is ramping production of high-voltage circuit breakers tailored to data centres and grid infrastructure, reflecting growing demand from AI/data-centre builds.

- March 2025: GE Vernova signed an agreement with Amazon Web Services to supply power equipment (including HV equipment, likely circuit breakers + substations) for AWS’s global data-centres.

- March 2024: Schneider announced significant U.S. investment, including increased production of circuit breakers, switchboards, etc, driven by data-centre demand.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.52% from 2026-2034 |

|

Unit |

Value (USD Billion), Volume (Thousand Units) |

|

Segmentation |

By Type, Data Center Type, and Region |

|

By Type |

· Low Voltage Circuit Breakers · Medium Voltage Circuit Breakers |

|

By Data Center Type |

· Hyperscale · Colocation · Enterprise |

|

By Geography |

· North America (By Type, Data Center Type, and Country) o U.S. o Canada · Europe (By Type, Data Center Type, and Country) o U.K. o Germany o France o Spain o Italy o Rest of Europe · Asia Pacific (By Type, Data Center Type, and Country) o China o India o Japan o Australia o Southeast Asia o Rest of Asia Pacific · Rest of the World (By Type, Data Center Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.20 billion in 2025 and is projected to reach USD 4.04 billion by 2034.

In 2025, North Americas market value stood at USD 0.49 billion.

The market is expected to exhibit a CAGR of 14.52% during the forecast period of 2026-2034.

The low voltage circuit breakers segment led the market by type.

Rapid increase in data center power demand drives market growth.

ABB, GE Vernova, Schneider Electric, Eaton, and others are some of the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

High power densities, rising AI workloads, grid-capacity upgrades, and the need for reliable, scalable, and intelligent power protection systems favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us