Class 7 Trucks Market Size, Share & Industry Analysis, By Truck Configuration (Rigid Trucks, Tractor Units, and Vocational Trucks), By Application (Freight & Regional Distribution, Construction & Infrastructure, Municipal & Public Services, Towing & Recovery, and Specialized Vocational Applications), By Propulsion (Diesel, Natural Gas (CNG/LNG), Hybrid Electric, Battery Electric (BEV), and Hydrogen Fuel Cell (FCEV)), By Axle Configuration (4×2, 6×2, 6×4, and Others), and Regional Forecast, 2026-2034

Class 7 Trucks Market Size and Future Outlook

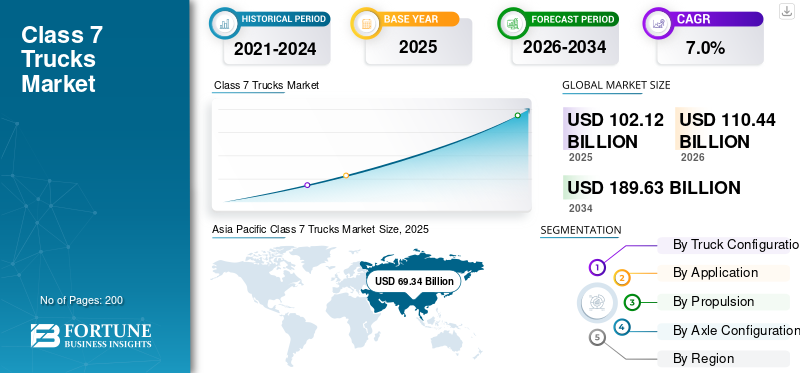

The global class 7 trucks market size was valued at USD 102.12 billion in 2025. The market is projected to grow from USD 110.44 billion in 2026 to USD 189.63 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. Asia Pacific dominated the class 7 trucks market with a market share of 67.9% in 2025.

Class 7 trucks are heavy duty commercial vehicles with a Gross Vehicle Weight Rating (GVWR) of 26,001 to 33,000 pounds, commonly used for urban freight distribution, municipal services, towing, and medium-range vocational applications. Key driving factors are rising market demand, technological advancements, regulatory support, infrastructure development, expanding end-use industries, and increased investments that positively influence overall market performance.

Major players in the market include Daimler Truck, PACCAR, Volvo Group, Navistar, and Isuzu Motors, competing through fuel-efficient powertrains, electrification strategies, fleet telematics integration, safety innovations, and vocational customization capabilities.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

CLASS 7 TRUCKS MARKET TRENDS

Electrification and Alternative Fuel Adoption Reshaping Fleet Procurement

One of the prominent market trends is the gradual shift toward electrification and alternative fuel adoption, including battery electric and hydrogen fuel cell variants. Fleet operators are increasingly evaluating the total cost of ownership, emissions compliance, and sustainability targets when making procurement decisions. Advancements in battery range, charging infrastructure, and government incentives are accelerating pilot deployments. This transition is influencing product development strategies, supply chain investments, and long-term market growth across urban delivery and municipal applications.

- In March 2025, Isuzu launched battery-electric Class 6 and Class 7 F-Series medium duty trucks with Cummins’ Accelera powertrain, featuring next-generation Lithium Iron Phosphate (LFP) batteries and a 14Xe eAxle, with production slated for 2027 in North America.

MARKET DYNAMICS

MARKET DRIVERS

Rising Urban Freight Distribution to Accelerate Market Demand

Growing urbanization and the rapid expansion of e-commerce are significantly increasing medium-duty freight movement within cities. Class 7 trucks are widely used for regional haul, last-mile bulk delivery, and municipal logistics, making them essential to urban supply chains. Expanding retail networks, construction activities, and infrastructure modernization projects are further supporting the market demand. As fleet operators seek higher payload capacity with maneuverability advantages, these factors collectively contribute to sustained market growth during the forecast period.

- In June 2024, the District Department of Transportation released its updated District Freight Plan, outlining data-driven freight modeling, curbside management digitization, zero-emission truck transition strategies, and infrastructure upgrades to improve urban goods movement efficiency, safety, and multimodal freight integration across Washington, D.C.

MARKET RESTRAINTS

High Initial Acquisition Costs Limiting Fleet Replacement Cycles

One of the primary restraints in the market is the high upfront cost of vehicle procurement, particularly for advanced diesel and electric class 7 truck models. Small and mid-sized fleet operators often delay replacement cycles due to capital constraints and fluctuating freight rates. Additionally, financing challenges and rising input material costs can impact purchasing decisions. These cost pressures may slow market penetration of technologically advanced vehicles, moderating overall market growth in price-sensitive regions.

MARKET OPPORTUNITIES

Telematics and Fleet Digitalization Creating Aftermarket Revenue Streams

The integration of advanced telematics, predictive maintenance systems, and connected fleet platforms presents significant opportunities for the class 7 trucks market growth. Fleet operators increasingly prioritize reduced operational costs & efficiency, fuel optimization, and real-time vehicle diagnostics. This shift enables OEMs and technology providers to expand service-based revenue models, including subscription platforms and remote monitoring solutions. As digital transformation accelerates across commercial transportation, value-added services are expected to enhance market share positioning and long-term profitability.

- In March 2025, NTEA launched the Commercial Vehicle Data Exchange (CVDE) during Work Truck Week, introducing a standardized digital framework that enables OEMs, up fitters, and body builders to securely share vehicle chassis data, streamline up fitting processes, improve compatibility validation, and reduce engineering lead times.

MARKET CHALLENGES

Supply Chain Volatility and Component Shortages Disrupting Production Stability

Persistent supply chain disruptions, including semiconductor shortages and raw material price volatility, remain a critical challenge for manufacturers. Delays in component sourcing can extend production timelines and impact delivery schedules for fleet customers. Furthermore, geopolitical tensions and trade policy uncertainties may affect cross-border supply networks. These uncertainties complicate production planning and inventory management, potentially influencing market analysis projections and creating short-term fluctuations in vehicle availability across key regions.

Segmentation Analysis

By Truck Configuration

Strong Regional Distribution Networks and Fleet Versatility to Strengthen Rigid Truck Segment Leadership

Based on truck configuration, the market is segmented into rigid trucks, tractor units, and vocational trucks.

The rigid trucks segment dominates the market due to its widespread use in regional freight distribution, urban deliveries, and municipal operations. These trucks offer operational flexibility, lower acquisition costs compared to articulated alternatives, and compatibility with diverse body configurations. High fleet penetration across retail, food distribution, and utility services sustains consistent replacement demand for class 7 trucks. Their adaptability to both diesel and emerging electric platforms further reinforces stability in segmental market share.

- In October 2024, Hitachi Construction Machinery unveiled the EH4000AC-5 rigid dump truck with a 242-ton payload and a max speed of 65 km/h, showcasing metal-fabricated durability, multiple drive modes, and optional battery electric and trolley charging upgrades for future zero-emission mining operations.

The vocational trucks segment is projected to expand at a CAGR of 8.0% during the forecast period. Rising infrastructure development, construction activities, and municipal modernization programs are accelerating demand for specialized configurations, including dump, utility, and service trucks across developing and mature economies.

By Application

Expanding Regional Logistics Networks and Retail Supply Chains to Sustain Freight & Regional Distribution Segment Growth

Based on application, the market is segmented into freight & regional distribution, construction & infrastructure, municipal & public services, towing & recovery, and specialized vocational applications.

The freight & regional distribution segment holds the largest class 7 trucks market share, driven by increasing intra-city goods movement and expanding retail supply chains. Growth in e-commerce fulfillment centers, food distribution networks, and third-party logistics services sustains consistent fleet deployment. These trucks offer optimal payload capacity and maneuverability for short- to mid-haul routes, ensuring high utilization rates. Stable replacement cycles and fleet management & expansion strategies further reinforce segmental dominance across major transportation corridors.

- In January 2025, Gatik and Loblaw expanded their strategic partnerships to scale AI-powered autonomous Class 6 & 7 trucks across Canada, deploying SAE Level 4 autonomous box trucks equipped with redundant perception systems, drive-by-wire controls, and remote monitoring for middle-mile retail distribution routes.

The towing & recovery segment is projected to grow at a CAGR of 10.9% during the forecast period. Rising vehicle parc, stricter roadside safety enforcement, and expanding highway infrastructure are increasing demand for specialized recovery fleets across urban and intercity transport networks.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

Established Refueling Infrastructure and Proven Performance to Maintain Diesel Segment Dominance

By propulsion, the market is divided into diesel, natural gas (CNG/LNG), hybrid electric, Battery Electric (BEV), and Hydrogen Fuel Cell (FCEV).

The diesel segment dominates the market, supported by its established refueling infrastructure, high torque output, and long haul operational efficiency. Fleet operators continue to prefer diesel powertrains for regional freight and vocational applications due to reliability and lower total cost of ownership in high-utilization cycles. Strong aftermarket support networks and widespread service expertise further sustain diesel’s market share, particularly in regions where alternative fuel infrastructure remains under development.

- In August 2024, Mack Trucks launched the refreshed Mack MD Series medium-duty trucks, featuring Cummins B6.7 diesel engines (up to 325 hp and 750 lb-ft torque), Allison automatic transmissions, enhanced driver-assist systems, and improved interior ergonomics. They expanded wheelbase options for Class 6 & 7 applications.

The Hydrogen Fuel Cell (FCEV) segment is projected to expand at a CAGR of 19.1% during the forecast period. Government decarbonization targets, zero-emission mandates, and investments in hydrogen infrastructure are accelerating pilot deployments in regional logistics and municipal fleet applications.

By Axle Configuration

Operational Efficiency and Urban Maneuverability to Anchor 4x2 Axle Configuration Leadership

By axle configuration, the market is categorized into 4×2, 6×2, 6×4, and others.

The 4×2 segment holds the largest market share, primarily due to its suitability for urban freight and regional distribution routes. These vehicles offer lower acquisition and maintenance costs, improved fuel efficiency, and enhanced maneuverability in dense city environments. Fleet operators favor 4×2 configurations for standardized cargo applications, ensuring high-volume deployment and consistent replacement demand across logistics, retail, and municipal service fleets.

- In March 2023, Mack Trucks introduced the Mack MD Electric, a Class 6-7 medium-duty truck configured with a 4×2 axle setup, powered by three NMC lithium-ion battery packs (up to 260 kWh), offering up to 150-mile range and 150 kW DC fast-charging capability for urban distribution fleets.

The 6×4 axle segment is projected to grow at a CAGR of 8.2% during the forecast period. Increasing demand for higher payload capacity and improved traction in vocational and heavy regional applications is supporting accelerated adoption across construction and utility operations.

Class 7 Trucks Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific dominates the market, supported by rapid urbanization, expanding manufacturing output, and strong growth in regional logistics networks. Rising e-commerce penetration and infrastructure investments across China, India, and Southeast Asia continue to stimulate market demand. Government-backed industrial corridors and fleet modernization programs further strengthen vehicle replacement cycles. Additionally, the presence of major domestic manufacturers and cost-competitive production ecosystems enhances market growth, reinforcing the region’s leading market share during the forecast period.

Asia Pacific Class 7 Trucks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- In January 2025, Tata Motors launched 17 next-generation commercial trucks, introducing Advanced Driver Assistance Systems (ADAS), electronic stability control, collision mitigation systems, and enhanced cabin ergonomics, along with upgraded BS6 Phase II - compliant powertrains and improved telematics integration to enhance safety, fuel efficiency, and fleet productivity.

China Class 7 Trucks Market

The China’s market in 2026 is estimated at around USD 47.78 billion, accounting for roughly 43.3% of global revenues. Strong domestic manufacturing, infrastructure expansion, and e-commerce-driven freight demand sustain market growth and fleet modernization.

Japan Class 7 Trucks Market

The Japanese market in 2026 is estimated at around USD 16.35 billion, accounting for roughly 6.2% of global revenues. Advanced fleet efficiency standards, urban logistics optimization, and early alternative fuel adoption support stable market growth.

India Class 7 Trucks Market

The Indian market in 2026 is estimated at around USD 6.83 billion, accounting for roughly 8.7% of global revenues. Rapid urbanization, expanding regional trade corridors, and infrastructure investments accelerate market demand and long-term growth potential.

North America

North America holds the second largest market share and is projected to expand at a CAGR of 8.9% during the forecast period. Strong regional freight movement, well-established distribution networks, and rising investments in zero-emission truck deployments are supporting market growth. Fleet operators increasingly prioritize fuel efficiency, telematics integration, and compliance with regulatory emission standards. Infrastructure spending and vocational fleet upgrades across the municipal and utility sectors further sustain market demand in the region.

- In April 2023, Volta Trucks detailed the upcoming U.S. launch of its Class 7 Volta Zero electric truck, featuring a 150–225 kWh battery pack, a central driving position for enhanced visibility, a 4×2 axle configuration, and an optimized urban range of up to 150 miles for city logistics operations.

U.S. Class 7 Trucks Market

The U.S. market in 2026 is estimated at around USD 13.09 billion, accounting for roughly 11.9% of global revenues. Strong regional freight movement, vocational fleet expansion, and electrification investments drive sustained market growth.

Europe

Europe holds the third-largest market share, driven by stringent emission regulations and progressive decarbonization policies. Fleet renewal initiatives, low-emission zones, and incentives for alternative fuel vehicles are accelerating technology adoption. Mature logistics networks and cross-border freight activity support consistent vehicle utilization. Additionally, the presence of leading OEMs and a structured aftermarket ecosystem contributes to steady market growth, while electrification strategies gradually reshape competitive positioning across Western and Northern Europe.

- In September 2024, Volvo Trucks launched a long-range electric heavy duty truck offering up to 600 km of range, equipped with an advanced battery system exceeding 600 kWh capacity and megawatt charging capability, targeting regional haul operations with reduced downtime and zero tailpipe emissions.

Germany Class 7 Trucks Market

The German market in 2026 is estimated at around USD 4.02 billion, accounting for roughly 3.6% of global revenues. Strong industrial output, cross-border freight activity, and emission-driven fleet upgrades sustain consistent market growth.

U.K. Class 7 Trucks Market

The U.K. market in 2026 is estimated at around USD 3.00 billion, accounting for roughly 2.7% of global revenues. Expanding urban distribution networks and zero-emission transition policies support steady market demand and replacement cycles.

Rest of the World

The rest of the world demonstrates emerging growth potential in the market, supported by infrastructure development, expanding construction activity, and improved trade connectivity. South America, the Middle East, and parts of Africa are witnessing a gradual expansion of fleets for freight and vocational applications. Economic diversification programs and urban development projects are strengthening market demand. Although the adoption of advanced propulsion technologies remains gradual, improving financing access and supporting industrial activity will enhance long-term market growth prospects.

- In July 2024, JAC Motors launched a new truck range in Brazil, introducing light and medium-duty models equipped with Euro V-compliant diesel engines, manual and automated transmissions, reinforced chassis platforms, and enhanced telematics features to support regional freight and vocational operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Electrification Strategies and Fleet Digitalization Intensify Competitive Positioning

The class 7 trucks market is moderately consolidated, with a few global OEMs commanding significant market share through large-scale manufacturing and established dealer networks. Key players such as Daimler Truck, PACCAR, Volvo Group, Navistar (International), and Isuzu Motors compete through fuel-efficient powertrains, zero-emission vehicle development, and advanced telematics integration. Companies are strengthening competitive advantage through electrification investments, strategic technology partnerships, localized production, and aftermarket service expansion. Increasing focus on connected fleet solutions and vocational customization further intensifies competition across mature and emerging regional markets.

LIST OF KEY CLASS 7 TRUCKS COMPANIES PROFILED

- Daimler Truck AG (Germany)

- PACCAR Inc. (U.S.)

- Volvo Group (Sweden)

- Navistar, Inc. (International Motors) (U.S.)

- Isuzu Motors Limited (Japan)

- Hino Motors, Ltd. (Japan)

- Ford Motor Company (U.S.)

- General Motors (U.S.)

- Traton SE (MAN Truck & Bus) (Germany)

- Scania AB (Sweden)

- Iveco Group N.V. (Italy)

- Dongfeng Motor Corporation (China)

- FAW Group Corporation (China)

- Foton Motor Group (China)

- Ashok Leyland Limited (India)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Volvo Group dominated the Europe’s heavy truck market, supported by strong deliveries of FH, FM, and FMX models, including battery-electric variants with up to 540 kWh capacity, advanced I-Shift transmissions, and fuel-efficient Euro VI diesel powertrains.

- March 2025: Kenworth expanded its zero-emission lineup with new medium-duty battery-electric trucks, offering multiple wheelbase options, integrated PACCAR ePowertrain systems, DC fast-charging, and configurations tailored for pickup and delivery applications.

- September 2024: DTNA delivered Freightliner eM2 electric trucks to Pitt Ohio, featuring 315 kWh batteries, dual-motor propulsion, and up to 230 mile range in certain configurations, supporting fleet electrification in regional freight operations.

- August 2024: 7Gen deployed a Class 7 battery-electric box truck in Canada featuring high-capacity lithium-ion batteries, telematics integration, and optimized payload configuration to support zero-emission urban freight operations and fleet decarbonization initiatives.

- March 2024: Mack Trucks showcased its MD Electric medium-duty truck at Work Truck Week, highlighting a 260 kWh battery system, 4×2 configuration, 150-mile range, and zero-emission capability for pickup, delivery, and vocational fleets.

- February 2024: Freightliner announced production readiness of the eM2 electric truck, offering up to 315 kWh of battery capacity, regenerative braking, and multiple body configurations, targeting vocational and regional distribution customers.

- January 2024: Volvo Trucks launched a new global truck range, introducing upgraded Euro VI-compliant diesel engines, enhanced fuel-efficiency packages, aerodynamic improvements, and digital driver interfaces, alongside battery-electric variants, strengthening its medium- and heavy-duty portfolio for regional haul and vocational applications.

- May 2023: Daimler Truck unveiled the Freightliner eM2, a Class 6-7 battery-electric truck equipped with up to 315 kWh of battery capacity, dual electric motors delivering up to 480 hp peak output, and AC/DC charging flexibility for regional haul operations.

REPORT COVERAGE

The global class 7 trucks market analysis provides an in-depth study of the market size and forecast for all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026-2034 |

| Unit | Value (USD Billion) & Volume (Units) |

| Segmentation | By Truck Configuration, By Application, By Propulsion, By Axle Configuration, and By Region |

| By Truck Configuration |

|

| By Application |

|

| By Propulsion |

|

| By Axle Configuration |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 102.12 billion in 2025 and is projected to reach USD 189.63 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 69.34 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period.

The freight & regional distribution segment leads the market in terms of application.

Rising urban freight distribution is the key factor driving the market.

Key players such as Daimler Truck, PACCAR, Volvo Group, Navistar (International), and Isuzu Motors are the top players, among others.

Asia Pacific held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us