CMOS Image Sensor Market Size, Share & Industry Analysis, By Type (Front-illuminated (FI) Image Sensors, Back-illuminated (BI) Image Sensors, and Stacked Image Sensors), By Spectrum (Visible Spectrum, Near-Infrared (NIR), and Short-Wave Infrared (SWIR)), By Resolution (Up to 5 MP, 5 MP to 12 MP, 12 MP to 16 MP, and Above 16 MP), By End-use (Aerospace & Defense, Automotive, Consumer Electronics, Healthcare, Security & Surveillance, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

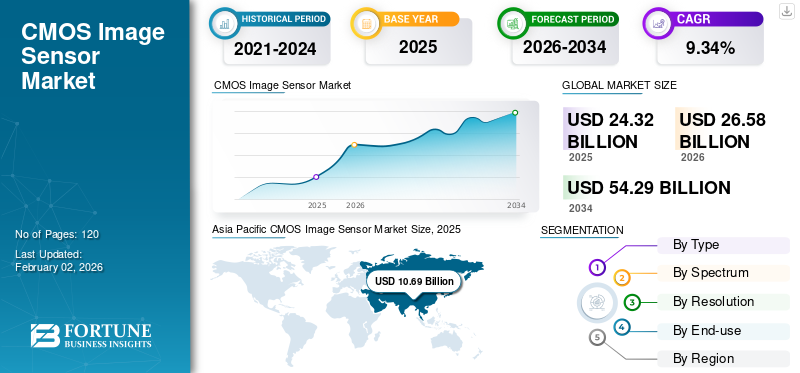

The global CMOS image sensor market size was valued at USD 24.32 billion in 2025 and is projected to grow from USD 26.58 billion in 2026 to USD 54.29 billion by 2034, exhibiting a CAGR of 9.34% during the forecast period. The Asia Pacific region dominated the global market, accounting for a 43.94% share in 2025.

Complementary Metal-Oxide-Semiconductor (CMOS) image sensors are used in smartphones, DSLRs, and other imaging devices as they are a core component of digital cameras. It captures images by converting light into electrical signals. CMOS sensors are cost-effective and energy-efficient devices, making them suitable for battery-powered devices, including smartphones.

CMOS sensors are small in size; owing to this, they are increasingly used in medical imaging applications, such as endoscopic, microscopic, and diagnostic imaging tools. Also, these sensors consume less power and capture high-quality images, making them suitable for medical applications. Thus, this trend is gaining rapid pace to boost market growth.

The market is dominated by established key players, such as Semiconductor Components Industries (Onsemi), Sony Semiconductor Solutions Corporation, Samsung Electronics, Panasonic Corporation, OMNIVISION, and Canon. These players focus on acquiring smaller firms or startups with innovative technologies or unique sensor products to gain a competitive edge. This factor is anticipated to fuel the market growth across the globe.

Download Free sample to learn more about this report.

IMPACT OF RECIPROCAL TARIFFS

The impact of reciprocal tariffs has negatively affected the market growth. The countries involved in reciprocal tariff actions may impose higher tariff rates on raw materials, including silicon wafers and other semiconductor components, or may impose tariff rates on final products such as image sensors. This process would increase production costs for manufacturers, resulting in higher average selling prices for products in consumer electronics, automotive, and security. Thus, it may result in slowing the market growth.

CMOS Image Sensor Market Key Takeaways

- 2025 Market Size: USD 24.32 billion

- 2026 Market Size: USD 26.58 billion

- 2034 Forecast Market Size: USD 54.29 billion

- CAGR: 9.34% from 2026–2034

- Asia Pacific dominated the CMOS image sensor market with a 43.94% share in 2025.

- The back-illuminated (BI) image sensors segment held the largest share at 60.64% in 2026.

- The visible spectrum segment accounted for the highest market share of 66.39% in 2026.

Asia Pacific

Asia Pacific generated USD 10.69 billion in 2025 and accounted for 43.94% of the global market.

North America

North America reached USD 6.66 billion in 2025, representing a 27.37% market share.

Europe

Europe contributed USD 5.03 billion in 2025, accounting for 20.68% of global revenue.

U.S.

The market is projected to reach USD 5.07 billion by 2026, supported by strong demand in medical imaging applications.

Japan

The CMOS image sensor market is projected to reach USD 2.27 billion by 2026.

Read More

IMPACT OF GENERATIVE AI

Growing Demand for Enhanced Image Quality Fuels Market Growth

Generative AI algorithms, such as GANs (Generative Adversarial Networks), are used to create high-quality images from low-quality images. In this method, the generative AI algorithm works on enhancing the post-capture image to reduce motion blur, enhance image clarity, and improve low-light performance and resolution in real-time. Thus, generative AI technology is increasingly used in CMOS sensors, which are built at a lower cost to offer premium output in terms of image clarity and detail. For instance,

- Smartphone manufacturer Google Pixel uses generative AI technology in its smartphone cameras to enhance high-range zoom photos. Also, this technology helps to resize, remove, or reposition objects in a photo.

MARKET DYNAMICS

Market Drivers

Growing Adoption of Miniature Cameras in Consumer Electronics Drive Market Growth

The growing popularity of miniature cameras and wearable devices among customers is fueling the adoption of CMOS image sensors in the consumer electronics sector. In recent times, demand for smartphones with high-quality cameras is on the rise. Thus, smartphone manufacturers are constantly focusing on improving the camera quality, leading to the adoption of higher-resolution image sensors. Moreover, the growing trend of video conferencing, social media platforms, and selfies is forcing manufacturers to integrate high-quality front and rear cameras in smartphones.

- In January 2023, ams OSRAM launched 0.5 megapixel global shutter CMOS image sensors. These sensors are compact and consume less power, which makes them suitable for wearable and mobile devices.

Further, manufacturing of these sensors is cost-effective compared to CCD (Charge-Coupled Device) sensors, which fuels their integration in mass-market devices. Thus, these factors play an important role in fueling the market growth.

Market Restraints

High Manufacturing Costs May Hinder Market Growth

Manufacturing advanced CMOS image sensors with better sensitivity, higher resolution, and enhanced features such as backside illumination (BSI), stacked sensors, and frontside illumination (FSI) requires complex processes and expensive materials.

Also, the higher cost of raw materials (such as silicon wafers), specialized components, and innovative fabrication technologies increases the overall manufacturing cost of image sensors. Thus, higher manufacturing costs may act as a barrier to market growth.

Market Opportunities

Rising Demand for Advanced Vision Systems in Self-Driving Cars May Create Lucrative Opportunities for Market Growth

The popularity of self-driving cars is increasing among customers globally. These autonomous cars use advanced vision systems to detect and identify objects in their surroundings, such as pedestrians, obstacles, other vehicles, and traffic signs. The use of CMOS sensors is necessary in these systems, as they offer high-quality imaging capabilities in real-time to support lane detection, gesture recognition, object recognition, and collision avoidance.

- According to industry experts, by 2027, fully automated vehicles may require 25 or more onboard image sensors to monitor their surroundings.

The incorporation of cutting-edge technology in autonomous vehicles plays a vital role in enhancing their safety. Owing to this factor, the demand for high-performance sensors also increases across the globe.

CMOS Image Sensor Market Trends

Growing Adoption of 3D Imaging and Depth Sensing in AR/VR Applications

The growing popularity of 3D imaging and depth sensing plays an important role in driving the market growth. The market is driven by the increasing use of augmented reality (AR), virtual reality (VR), autonomous driving, and robotics. These applications require accurate depth perception to enable interactions with digital content or to navigate environments safely. This technology is not limited to gaming and entertainment; it can be useful in industries including healthcare, manufacturing, logistics, retail, and education.

In healthcare, augmented reality assists in surgery, and virtual reality helps in medical training by using depth perception for anatomical accuracy. Moreover, major market players are significantly focusing on investing in 3D imaging and depth-sensing technologies, owing to the growing demand for innovative products. Thus, these factors play a crucial role in fueling the CMOS image sensor market growth during the forecast period.

SEGMENTATION ANALYSIS

By Type

Rising Demand for Scalability to Smaller Pixel Sizes Boosted Adoption of Back-illuminated (BI) Image Sensors

Based on type, the market is divided into front-illuminated (FI) image sensors, back-illuminated (BI) image sensors, and stacked image sensors.

Back-illuminated (BI) image sensors accounted for the largest market share 60.64% in 2026. These sensors maintain sensitivity at a smaller pixel size of 1.0 μm. This scalability helps back-illuminated (BI) image sensors to produce high-quality images. Owing to this capability, they are increasingly used in 50MP to 200MP camera sensors while maintaining image quality. Also, it helps electronics product manufacturers to design compact-sized devices along with periscope-style zoom in camera modules.

Stacked image sensors are anticipated to grow at the highest CAGR during the forecast period, as the popularity of these sensors is increasing among customers. These sensors enable real-time HDR video and 4K/8K ultra-fast recording in premium smartphones, including iPhone 15 Pro Max and Sony Alpha 1 among others. Also, stacked image sensors are used for advanced driver assistance systems (ADAS) in vehicles for pedestrian and lane detection in fast motion.

By Spectrum

Mass Adoption of Image Sensors with Visible Spectrum as They Replicate Human Vision

Based on spectrum, the market is segregated into visible spectrum, near-infrared (NIR), and short-wave infrared (SWIR).

The visible spectrum accounted for the largest market share 66.39% in 2026. The majority of consumer devices, such as smartphones, laptops, and tablets, digital cameras, webcams, and drones, use image sensors augmented for the visible spectrum to replicate what the human eye sees. Further, with the rising trend of remote work and video conferencing, manufacturers are designing consumer devices with front-facing visible-spectrum cameras.

Short-wave infrared (SWIR) is expected to grow at the highest CAGR during the forecast period, as these image sensors can see through obscurants, such as fog, smoke, dust, and plastics. Thus, owing to their ability to penetrate through obscurants where visible light fails, SWIR image sensors are considered very important in harsh atmospheric conditions.

By Resolution

Cameras with 16 MP Witness Increased Demand as they Provide Higher Image Details

Based on resolution, the market is classified into up to 5 MP, 5 MP to 12 MP, 12 MP to 16 MP, and above 16 MP.

Above 16 MP segment captured the largest market share 37.07% in 2025, as its higher pixel count offers greater spatial resolution. These cameras capture images with visual detail, especially in zoomed-in images or large prints.

- Smartphones, including Samsung Galaxy S24 Ultra and Xiaomi 14 Ultra, use 50–200 MP main sensors to capture images with more visual details.

5 MP to 12 MP is anticipated to grow at the highest CAGR during the forecast period. These resolution cameras support 1080p to 4K video at real-time frame rates. Also, they consume less power and generate less heat. As these cameras are lower in cost, they help SMEs and startup companies to manufacture the final product at a competitive price.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Continuous Innovation and Feature Differentiation Propelled Adoption of CMOS Sensors in Consumer Electronics

Based on end-use, the market is categorized into aerospace & defense, automotive, consumer electronics, healthcare, security & surveillance, and others (industrial, etc.).

The consumer electronics segment accounted for the largest market share 11.87% in 2026. Consumer devices are in a highly competitive market, owing to increasing innovation in products. Camera performance is a top criterion for buying a device among customers. To attract customers’ attention, manufacturers are mainly focusing on providing cameras with innovative technologies such as AI-enhanced computational photography, 4K/8K video, HDR, slow motion, and night mode.

Automotive is projected to grow at the highest CAGR during the forecast period. Modern cars are equipped with multiple cameras and sensors per car, especially in EVs and premium models. Increasing demand for ADAS-enabled cars requires CMOS image sensors for lane and pedestrian detection.

- According to industry experts, Apple, Baidu, and Google are developing self-driving vehicles, and they are planning to launch their first model in the market by 2027.

CMOS IMAGE SENSOR MARKET REGIONAL OUTLOOK

Among regions, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific CMOS Image Sensor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 10.69 billion in 2025, representing 43.94% of the global industry, and is expected to reach USD 11.58 billion in 2026. and is the largest manufacturer of smartphones, laptops, wearables, and tablets enabled with CMOS sensors. The region has a prominent presence of OEMs such as Samsung Electronics, Sony, Panasonic, Canon, Xiaomi, and others. Furthermore, China, India, Southeast Asia, and South Korea, have a fast-growing population of tech-savvy and mobile-first consumers, which play a pivotal role in driving market growth in the region. Also, the market is heavily reliant on Asian suppliers for wafers and assembly.

- According to industry experts, in 2024, over 70% of the world’s smartphones were manufactured in China, Vietnam, India, and South Korea.

Download Free sample to learn more about this report.

China is a major producer and consumer of smart home devices, smartphones, tablets, and laptops equipped with CMOS image sensors. As per industry experts, in China, over 350 million smartphones were shipped domestically in 2024. Also, the country has a prominent network of CMOS sensor packaging and camera module assembly companies, which play a vital role in reducing the packaging cost and speeding up time-to-market. These factors play an important role in fueling market growth across China.The Japan market is projected to reach USD 2.27 billion by 2026, the China market is projected to reach USD 2.33 billion by 2026, and the India market is projected to reach USD 1.65 billion by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 6.66 billion in 2025, accounting for 27.37% share, and is expected to reach USD 7.25 billion in 2026. North America is expected to grow at a prominent pace. The region invests heavily in video surveillance, border monitoring, and critical infrastructure protection, which requires high-performance CMOS sensors. In security and surveillance applications, demand for low-light performance, NIR sensitivity, and night vision devices is high, which plays a vital role in fueling the market growth in the region.The U.S. market is projected to reach USD 5.07 billion by 2026.

In the U.S., CMOS sensors are mainly used in medical imaging applications, such as dental imaging, endoscopy, ophthalmology, and other applications, owing to their high-resolution image quality, compact size, and cost-effectiveness. This factor plays a vital role in fueling the market growth across the country.

Europe

In 2025, Europe generated USD 5.03 billion, contributing 20.68% to global market revenue, and is projected to grow to USD 5.55 billion in 2026. In Europe, the market is expected to showcase noteworthy growth during the forecast period driven by the rising adoption of CMOS sensors in the automotive and industrial automation sectors. Germany, Switzerland, Austria, and the Nordics lead in industrial robotics and factory automation for defect detection, optical inspection, 3D scanning, and stereo vision. These factors fuel demand for the adoption of CMOS image sensors in the automotive industry. For instance,The UK market is projected to reach USD 1.05 billion by 2026, while the Germany market is projected to reach USD 1.03 billion by 2026.

- In October 2024, OmniVision released 3 MP HDR sensors and other imaging solutions at AutoSens Europe 2024. The company designed this sensor specifically for surround- and rear-view automotive cameras.

South America

The adoption of CMOS sensors is growing significantly in South America, owing to the rising adoption of smartphones in Brazil, Argentina, and Chile. Further, customers in the region prefer the adoption of mid-range smartphones, laptops, tablets, and other electronic devices equipped with 2-4 CMOS sensor units per device, which drives the demand for 5-12 MP CMOS sensors. Further, the growing popularity of social media apps increases camera usage among customers.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.77 billion, accounting for 3.18% of the worldwide market, and is projected to grow to USD 0.88 billion in 2026. The Middle East & Africa are expected to grow at the highest CAGR during the forecast period. Multiple governments in the Gulf Cooperation Council (GCC) countries are investing heavily in smart infrastructure, which includes public safety systems, traffic monitoring, and video surveillance systems equipped with CMOS sensors. For instance,

- NEOM city in Saudi Arabia invested approximately USD 500 billion in the development of a mega-city with integrated surveillance, traffic analytics, and AI vision systems.

- Doha and Abu Dhabi governments invested heavily in the widespread deployment of IP cameras for traffic and security.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Players are Focusing on Partnership and Acquisition Strategies to Expand Their Customer Base

Notable players are directed toward expanding their global geographical footprint by offering industry-specific services. Market players are concentrating on strategic acquisitions and partnerships with regional market participants to uphold dominance. Leading market players are introducing novel solutions to grow their consumer base. A rise in continuous R&D investments for product advances is augmenting market expansion. Therefore, top players are promptly employing these strategic initiatives to withstand their competitiveness.

Long List of Companies Studied

- Semiconductor Components Industries, LLC (Onsemi) (U.S.)

- ANSYS, Inc. (U.S.)

- Sony Semiconductor Solutions Corporation (Japan)

- Tower Semiconductor (Israel)

- Hamamatsu Photonics K.K. (Japan)

- OMNIVISION (U.S.)

- STMicroelectronics (Switzerland)

- Samsung Electronics (South Korea)

- Panasonic Corporation (Japan)

- Canon Inc. (Japan)

- SK Hynix (South Korea)

- CMOS Sensor Inc. (U.S.)

- Teledyne Technologies (U.S.)

- GalaxyCore Shanghai Limited Corporation (China)

- SmartSens (China)

- Toshiba Corporation (Japan)

- ams-OSRAM AG (Austria)

- Himax Technologies, Inc. (Taiwan)

- PixArt Imaging Inc. (Taiwan)

- Nextchip (China)

….and more

KEY INDUSTRY DEVELOPMENTS

- June 2025: CSEM, the Swiss Center for Electronics and Microtechnology, in collaboration with QDI Systems, a Dutch deep-tech startup, developed an image sensor. This image sensor is capable of converting X-rays into electronic signals using quantum dots on a CMOS chip. It is a compact, affordable, and scalable imaging device suitable for industrial inspections and medical imaging applications.

- May 2025: Eyeo raises approximately USD 17 million in funding to develop a new image sensor architecture. This architecture effectively captures all incoming light and increases sensitivity compared to existing technologies to produce a high-quality image.

- January 2025: Canon developed a CMOS sensor with 410 megapixels. The company developed this sensor for use in surveillance, medicine, and industry applications.

- November 2024: Sony Semiconductor Solutions unveiled the IMX925 stacked CMOS image sensor. This sensor is equipped with a back-illuminated pixel structure and offers high processing speed with a 25-megapixel*1 camera resolution for industrial equipment imaging.

- September 2024: Sony Semiconductor Solutions launched the LYT-818, equipped with a 50-megapixel*1 CMOS image sensor for mobile devices. This product captures a high-quality image in low-light conditions by reducing noise.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Key players operating in the market, such as Semiconductor Components Industries (Onsemi), Sony Semiconductor Solutions Corporation, Samsung Electronics, Panasonic Corporation, OMNIVISION, and Canon, are increasingly investing in high-resolution sensors (e.g., 12 MP, 48 MP, 108 MP, and beyond) to meet the increasing demand for smartphones and advanced imaging devices. By manufacturing sensors enabled with high dynamic range (HDR) and faster readout speeds, companies can differentiate their products in the market. For instance,

- Sony’s Exmor RS series of sensors offers high resolution and high-speed image processing, making them popular in smartphones, cameras, and even automotive applications.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.34% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Spectrum

By Resolution

By End-use

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is expected to reach USD 54.29 billion by 2034.

In 2025, the market was valued at USD 24.32 billion.

The market is projected to grow at a CAGR of 9.34% during the forecast period.

By resolution, above 16 MP led the market.

The growing adoption of miniature cameras in consumer electronics devices drives market growth.

Semiconductor Components Industries (Onsemi), Sony Semiconductor Solutions Corporation, Samsung Electronics, Panasonic Corporation, OMNIVISION, ANSYS, Inc., Tower Semiconductor, Hamamatsu Photonics K.K., STMicroelectronics, and Canon Inc. are the top players.

Asia Pacific held the largest market share in 2025.

By end-use, the automotive sector is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us