Co‑Packaged Optics Market Size, Share & Industry Analysis, By Integration (2.5D CPO, 3D CPO, On-Board Optics, and Others ), By Data Rate (Less than 1.6T, 1.6T, 3.2T, and 6.4T and above), By Component (Optical Engine, Electrical IC, Laser Source, Connector & Packaging, and Other Components) By Application (Hyperscale Cloud Data Centers, Enterprise Data Centers, Telco Central Officers, HPC/AI/ML Clusters, Networking & Defense, and Other Applications), By End-use (Cloud Service Providers, Telecom Operators, Government & Defense, and Other Industries), and Regional Forecast, 2026 – 2034

CO‑PACKAGED OPTICS MARKET SIZE and FUTURE OUTLOOK

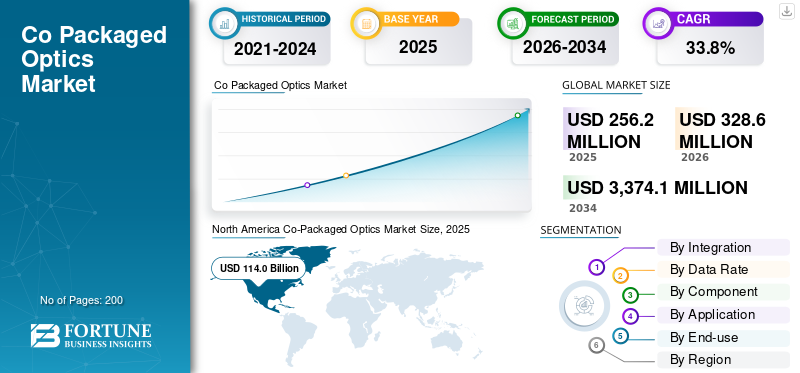

The global co‑packaged optics market size was valued at USD 256.2 million in 2025. The market is projected to grow from USD 328.6 million in 2026 to USD 3,374.1 million by 2034, exhibiting a CAGR of 33.8% during the forecast period. North America dominated the co‑packaged optics market with a market share of 46.25% in 2025.

Co‑packaged optics solutions integrate optical engines directly with switching ASICs or high-performance processors to enable ultra-high bandwidth, low-latency interconnects for hyperscale cloud, AI workloads, HPC clusters, telecom networks, and edge computing environments. Unlike traditional pluggable optics or copper-based interconnects, CPO provides higher data rates, improved energy efficiency, and reduced thermal overhead, while supporting modular Integration, 2.5D or 3D packaging, and scalable deployment across multiple servers, racks, and data centers.

The rapid growth of AI workloads, hyperscale cloud services, multi-terabit data transfers, and energy-conscious data center design is driving demand for co‑packaged optics. Organizations are deploying CPO solutions to reduce power per bit, minimize latency, optimize switch-to-engine integration, and support future-proofed high-speed optical connectivity for next-generation networking and compute environments.

Key players such as Intel Corporation, Broadcom Inc., Cisco Systems, Inc., and NVIDIA Corporation are advancing their CPO offerings through integrated optical engines, silicon photonics, thermal and power-optimized packaging, and high-speed interconnect designs. These vendors focus on delivering solutions that enable multiterabit-per-second links, high-performance optical-electrical co-design, modular 2.5D/3D integration, and deployment-ready systems for hyperscale cloud, AI, and telecom infrastructure. They are also driving ecosystem collaborations and joint ventures to accelerate adoption, improve manufacturability, and reduce time-to-market for high-speed co‑packaged optics solutions. These vendors focus on delivering platforms that support real-time cost visibility, workload optimization, budget control, cost allocation, anomaly detection, and policy-based governance for enterprises managing increasingly complex cloud and AI-driven infrastructure.

Download Free sample to learn more about this report.

CO‑PACKAGED OPTICS MARKET TRENDS

Telecom and Edge Networks are Accelerating Demand for High-Bandwidth Optical Interconnects

Telecom operators and edge data centers are increasingly exploring high-bandwidth, low-latency optical connectivity to support next-generation mobile networks (5G/6G), enterprise edge services, and distributed AI workloads, positioning co‑packaged optics or dense optical interconnects as part of long-term network evolution. As mobile operators push for more capacity at the network edge and in backhaul links to keep up with explosive data demand, optical technologies are gaining focus since they can deliver much higher throughput and lower energy per bit than copper-based solutions. For instance,

- In June 2026, Dixon Technologies’ joint venture in India with Gemtek Technology to manufacture optical transceivers and telecom optical products, underscoring telecom ecosystem investment in optical hardware to support evolving transport needs.

These investments indicate that operators are preparing their networks not only for higher data rates but also for lower latency, increased reliability, and future-proofing their infrastructure for AI-enabled services and ultra-dense edge deployments.

This trend also highlights an opportunity for CPO suppliers to collaborate with telecom vendors to offer tailored solutions that meet stringent edge and 5G/6G requirements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Explosive Growth of AI and High-Performance Computing Workloads Fueling Co‑Packaged Optics Demand

The rapid expansion of artificial intelligence and high-performance computing (HPC) workloads is a major driver for the co‑packaged optics market growth as these applications place enormous demands on data center network bandwidth and efficiency. As AI models grow larger and HPC tasks scale across many servers and accelerators, data movement between components becomes a critical bottleneck that traditional copper interconnects cannot handle effectively at high speeds or low power. For instance,

- According to ET Telecom, data center interconnects (DCI) bandwidth demand could increase by at least sixfold over the next five years, largely driven by the need to support AI training and inference traffic, with many new facilities expected to be dedicated to AI workloads.

- In addition, real-world connectivity data shows that bandwidth purchases for data center connectivity surged by nearly 330% between 2020 and 2024.

As hyperscale operators expanded optical infrastructure to meet escalating AI-related traffic. These trends underscore why optical solutions, especially co‑packaged optics that bring optical interfaces directly into silicon packages, are becoming essential to provide the multiterabit per second links required for modern AI and HPC environments while improving power efficiency and reducing latency.

MARKET RESTRAINTS

High Integration Costs and Deployment Complexity Limiting Widespread Adoption

High cost of Integration and deployment is a major restraint for the market since embedding optical engines, photonic integrated circuits, and sophisticated cooling directly with ASICs or XPUs drives up both capital expenditure and operational complexity. Unlike traditional pluggable optics, where components are modular and relatively inexpensive, CPO requires precision photonics, advanced assembly, and very tight alignment tolerances, with silicon photonics often representing 40–50% of the total module cost, and the remaining optical components adding another large share of expenses due to lasers, detectors, and high precision optics.

These costs currently make CPO solutions several times more expensive than conventional pluggable alternatives, restricting adoption mainly to hyperscale data centers where performance gains justify the investment. In contrast, cost-sensitive enterprise segments delay deployment.

MARKET OPPORTUNITIES

Energy Efficiency and Power Savings Driving Adoption in Hyperscale and Edge Data Centers

Energy consumption and heat generation are critical challenges for modern data centers as networking speeds and AI workloads scale rapidly, forcing operators to rethink how data moves inside racks and across fabrics. Traditional copper interconnects become increasingly inefficient at high data rates, consuming significant power as long electrical paths and high-power retimers add heat and complexity. For instance,

- Co‑packaged optics can reduce power for optical interconnects to as little as about 5% of equivalent copper-based solutions, significantly lowering the energy required per bit of data transmission and easing thermal management demands.

These energy savings translate into reduced operational expenses and make CPO an attractive option for hyperscale and AI-centric data centers seeking to meet sustainability goals while supporting high-density computing. For instance,

- Integrating optics closer to the ASIC cuts electrical losses and power overhead, helping network designers push toward 800 Gbps and 1.6 Tbps links without proportionally higher energy costs.

Segmentation Analysis

By End-use

Cloud Service Providers Segment Dominated Market, Driven by Extensive Internal Data Traffic and Infrastructure Investment

Based on end-use, the market is segmented into cloud service providers, telecom operators, government & defense, and other industries (financial services, healthcare).

Cloud service providers segment held the majority share of the market in 2024 and continued its dominance in 2025 with a 51.9% share, as hyperscale data centers are at the forefront of adopting high-bandwidth, low-latency interconnects to support AI, cloud computing, and large-scale storage workloads. Their enormous internal data movement requirements make traditional copper interconnects inefficient, pushing them toward CPO solutions. Additionally, they have the financial resources and technical expertise to deploy advanced optical engines at scale, and their rapid network expansion for AI and cloud services further accelerates CPO adoption compared with telecom operators or other industries.

Telecom operators segment is expected to witness the highest CAGR of 37.4% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Integration

2.5D CPO Segment Dominated Market Due to Manufacturability and Scalable Deployment

Based on integration, the market is segmented into 2.5D CPO, 3D CPO, on-board optics, and others (photonic integrated circuits, hybrid integration).

2.5D CPO segment held the majority share of the market in 2024 and continued its dominance in 2025 with 45.7% of share, as it offers a balance between performance, manufacturability, and cost. Unlike 3D CPO, which requires full vertical stacking and complex thermal management, 2.5D uses side-by-side integration of the optical engine and ASIC on an interposer, simplifying assembly and improving yield. It also provides high bandwidth and low latency, suitable for hyperscale data centers, while being easier to produce at scale than full 3D solutions. This combination of high performance, lower risk, and relatively lower cost makes 2.5D the preferred choice for early and large-scale deployments.

3D CPO segment is expected to witness the highest CAGR of 37.6% during the forecast period.

By Data Rate

1.6T Segment Held Majority Share Owing to Optimal Performance and Adoption Feasibility

Based on data rate, the market is categorized into less than 1.6T, 1.6T, 3.2T, and 6.4T and above.

1.6T segment held the majority share of the data rate market in 2024 and maintained its dominance with a 41.3% share in 2025 as it meets the performance requirements of current hyperscale and cloud data center applications while remaining feasible for large-scale production. It provides sufficient bandwidth for AI, cloud computing, and high-performance workloads without the higher complexity, cost, and thermal management challenges associated with 3.2T or 6.4T and above. This balance between performance and manufacturability has led to widespread adoption of 1.6T links across data center deployments.

6.4T and above segment is expected to witness the highest CAGR of 44.7% during the forecast period.

By Component

Optical Engine Segment Captured Majority of Share as it is a Core Enabler of High-Speed Optical Transmission

Based on component, the market is categorized into optical engine, electrical IC, laser source, connector & packaging, and other components (controllers, passive elements, etc.).

Optical engine segment held the majority share of the component market in 2024 and maintained its dominance with a 41.5% share in 2025 as it serves as the core subsystem that performs critical optical functions, including light transmission, signal modulation, and wavelength management. Growing deployment of high speed optical transceivers in AI infrastructure, cloud data centers, and next generation networking equipment has significantly increased demand for advanced optical engines. In addition, optical engines account for a substantial portion of the overall transceiver cost due to their complex design, precision manufacturing requirements, and performance impact, which contributes to their dominant market position.

Laser source segment is expected to witness the second-highest CAGR of 39.9% during the forecast period.

By Application

Hyperscale Cloud Data Centers Segment Led Market with High AI and Cloud Workload Demands

Based on application, the market is categorized into hyperscale cloud data centers, enterprise data centers, telco central offices, HPC/AI/ ML clusters, networking & defense, and other applications (edge computing, industrial networking, etc.).

Hyperscale cloud data centers segment held the majority share of the application market in 2024. In 2025, the segment continued its dominance with a 40.0% share as they generate the highest internal data traffic and require ultra-high bandwidth, low-latency interconnects to support AI workloads, large-scale storage, and cloud services. Their extensive deployment of GPUs, TPUs, and high-performance switches creates a critical need for multiterabit-per-second links that traditional pluggable optics or copper interconnects cannot efficiently provide. Additionally, hyperscalers have the financial resources and technical expertise to adopt advanced co‑packaged optics at scale, enabling improved energy efficiency, reduced power per bit, and higher network density, which accelerates adoption relative to enterprise, telecom, or HPC deployments.

HPC/AI/ML clusters segment is expected to witness the highest CAGR of 38.8% during the forecast period.

Co‑Packaged Optics Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Co‑Packaged Optics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the majority of the co‑packaged optics market share and was valued at USD 114.0 million in 2025. Due to its massive hyperscale data center expansion and advanced optical infrastructure investments, which create strong demand for high-speed optical interconnect technologies. The region is experiencing record data center activity, with ultra-low vacancy rates and rapid increases in supply as AI-driven workloads push operators to build and occupy more capacity across major hubs. For example, North American primary markets have seen accelerated leasing and absorption of new supply, highlighting intense demand for infrastructure that supports high-performance computing and networking. Additionally, major industry players are expanding optical connectivity manufacturing locally. For instance,

- In May 2026, Nvidia and Corning announced a long-term partnership to expand U.S.-based optical connectivity production capacity tenfold and build new facilities in Texas and North Carolina, supporting the optical fiber and connectivity needs of AI data centers.

U.S. Co‑Packaged Optics Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was valued at USD 93.3 million in 2025, accounting for roughly 36.4% of sales.

Europe

Europe is projected to grow at 31.7% over the coming years and reached a valuation of USD 30.9 million in 2025, due to the widespread adoption of AI, cloud computing, and high-performance networking in hyperscale and enterprise data centers. The region has strong regulatory support for digital infrastructure and energy-efficient technologies, which encourages the deployment of power-optimized optical interconnects including CPO.

Additionally, Europe hosts leading semiconductor and optical component manufacturers, along with active research in silicon photonics and photonic Integration, enabling local production and faster adoption.

U.K. Co‑Packaged Optics Market

The U.K. market was valued at around USD 4.9 million in 2025, representing roughly 1.9% of global revenues.

Germany Co‑Packaged Optics Market

Germany’s market reached USD 5.2 million in 2025, equivalent to around 2.0% of global sales.

Asia Pacific

Asia Pacific is expected to grow at the highest CAGR and reached a valuation of USD 91.0 million in 2025, due to the rapid expansion of hyperscale cloud and AI data centers in China, Japan, South Korea, and India, driven by the surge in digital services, AI adoption, and cloud computing. The region is also witnessing substantial investments in next-generation optical networking infrastructure, including local manufacturing of optical components and government-backed initiatives to strengthen data center capabilities. Additionally, telecom operators and edge computing providers in the Asia Pacific are aggressively deploying high-bandwidth networks to support 5G/6G rollouts and AI workloads, which creates significant demand for energy-efficient, high-speed interconnect solutions including co‑packaged optics.

Japan Co‑Packaged Optics Market

The Japanese market was valued at USD 12.2 million in 2025, accounting for roughly 4.8% of global revenues.

China Co‑Packaged Optics Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at USD 33.4 million, representing roughly 13.0% of global sales.

India Co‑Packaged Optics Market

The Indian market was valued at around USD 11.6 million in 2025, accounting for roughly 4.5% of global market share.

South America and Middle East & Africa

The Middle East & Africa are expected to grow at the second-highest CAGR, as the region experiences rapid modernization of its IT and telecom infrastructure. Investments in smart city projects, cloud adoption, and AI-driven services are creating a need for high-bandwidth, energy-efficient interconnect solutions. Telecom operators are upgrading core and edge networks to support 5G rollouts and low-latency connectivity for enterprise and government applications, while hyperscale cloud providers are expanding data center presence in key hubs including the UAE, Saudi Arabia, and South Africa.

South America is expected to grow at a slow and steady CAGR during the forecast period, due to the gradual adoption of hyperscale cloud infrastructure and moderate expansion of AI workloads compared with regions such as North America or Asia Pacific. While Brazil, Argentina, and Chile are investing in data centers and upgrading telecom networks, infrastructure development is slower and more dispersed, and budget constraints often limit large-scale deployment of advanced optical technologies.

GCC Co‑Packaged Optics Market

The GCC market reached USD 4.3 million in 2025, representing roughly 1.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players are Focusing on Innovation and Strategic Expansion to Strengthen Market Share

Key players in the co‑packaged optics market are advancing their solutions to meet the growing demand for high-bandwidth, low-latency optical interconnects in hyperscale data centers, AI workloads, telecom networks, and edge computing environments. Leading companies are focusing on the integration of optical engines with high-speed ASICs, silicon photonics innovation, thermal and power optimization, and modular interposer design to improve performance, energy efficiency, and scalability. Vendors are also expanding their product portfolios to support multi-terabit data rates, 2.5D and 3D integration architectures, and deployment across hyperscale cloud, enterprise data centers, HPC clusters, and telecom infrastructure.

LIST OF KEY CO‑PACKAGED OPTICS COMPANIES PROFILED IN REPORT

- Intel Corporation (U.S.)

- Broadcom Inc. (U.S.)

- Cisco Systems, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Marvell Technology, Inc. (U.S.)

- Ayar Labs Inc. (U.S.)

- Ranovus Inc. (Canada)

- TE Connectivity Ltd. (U.S.)

- Coherent Corp. (U.S.)

- Lumentum Holdings Inc. (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Fujitsu Limited (Japan)

- Ciena Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2026: Nvidia announced it is working with TSMC to scale production of its next‑generation Spectrum‑X co‑packaged optics (CPO) switches later this year, targeting significant improvements in power efficiency and bandwidth for AI data centers. The partnership aims to accelerate optical switch deployments across hyperscale infrastructure.

- June 2026: Ayar Labs formally joined Nvidia’s NVLink Fusion ecosystem, integrating its CPO optical connectivity into the platform to help customers build heterogeneous AI infrastructure with scalable bandwidth and optical interconnect options. The move highlights ecosystem cooperation for rack‑scale AI optical networks.

- June 2026: Amazon signed a multibillion‑dollar agreement with Corning to scale optical fiber and connectivity manufacturing in North Carolina, creating 1,000 jobs and strengthening supply for AI‑oriented data center infrastructure. This expansion underscores the broader demand for optical components driven by AI network buildouts.

- June 2026: Photonic computing company Lightmatter joined the Nvidia NVLink Fusion ecosystem to accelerate high‑performance optical connectivity deployment for AI systems. The strategic alignment is expected to reduce cabling complexity and enhance optical link scalability in dense AI clusters.

- May 2026: GlobalFoundries introduced its SCALE™ optical module, an OCI MSA-compliant co-packaged optics solution for AI data center interconnects. The platform uses coarse and dense wavelength division multiplexing to enhance bandwidth density and scalability versus traditional electrical links.

- March 2026: NVIDIA and Coherent Corp. entered a multiyear strategic agreement to advance optics technologies for next‑generation AI data center architecture. The deal includes NVIDIA’s multibillion‑dollar purchase commitments and expanded access to Coherent’s advanced laser and optical networking products, supporting ultrahigh‑bandwidth, energy‑efficient connectivity.

REPORT COVERAGE

The co-packaged optics market report provides a comprehensive analysis of the industry, focusing on key market players and the overall competitive landscape. It offers valuable insights into current market trends, technological advancements, and significant industry developments. The report further examines key growth drivers, restraints, opportunities, and challenges influencing market expansion.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 33.8% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Integration, Data Rate, Component, Application, End-use, and Region |

| By Integration |

|

| By Data Rate |

|

| By Component |

|

| By Application |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 256.2 million in 2025 and is projected to reach USD 3,374.1 million by 2034.

In 2025, the North Americas market value stood at USD 114.0 million.

The market is expected to grow at a CAGR of 33.8% over the forecast period.

By end-use, cloud service providers segment led the market.

Explosive growth of AI and high-performance computing workloads fueling co‑packaged optics demand.

Intel Corporation, Broadcom Inc., Cisco Systems, Inc., and NVIDIA Corporation are the top players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us