Collaborative Combat Aircraft Market Size, Share & Industry Analysis, By Platform Type (Attritable/Reusable Loyal Wingman CCAs, High-End Survivable CCAs, and Others), By System Offering (Air Vehicle/Aircraft Platform, Mission Autonomy & AI Software, Mission Payload & Sensors, and Others), By Mission Role (Air Superiority/Fighter Escort, ISR, Targeting & Sensor Extension, and Others), By End User (Air Force, Navy /Naval Aviation, Defense R&D/Test Agencies, Marine/Expeditionary Forces, and Joint Commands/Special Mission Users) and Regional Forecast, 2026-2034

Collaborative Combat Aircraft Market Size and Future Outlook

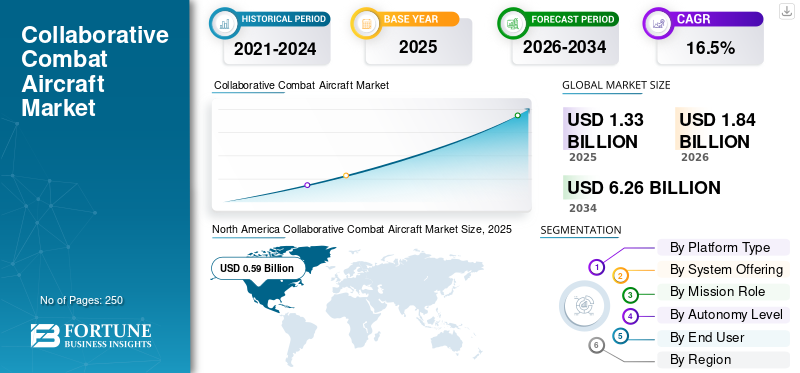

The global collaborative combat aircraft market size was valued at USD 1.33 billion in 2025. The market is projected to grow from USD 1.84 billion in 2026 to USD 6.26 billion by 2034, exhibiting a CAGR of 16.5% during the forecast period. North America dominated the collaborative combat aircraft market with a market share of 44.36% in 2025.

Collaborative combat aircraft (CCA) represent a transformative layer in modern air combat, leveraging networked autonomy, secure datalinks, and advanced sensor fusion to multiply combat effectiveness while reducing risk to manned platforms. The global push for CCAs is accelerating, driven by demand for distributed sensing and strike capability, the need to operate in contested and GPS-denied environments, and the strategic imperative to maintain air superiority.

Major aerospace and defense firms such as Boeing, General Atomics Aeronautical Systems, Inc., Anduril Industries, Inc. are pioneering systems that deliver resilient teaming between crewed fighter aircraft and unmanned wingmen. Key technical advances include open-architecture mission systems that support rapid software upgrades, robust multi-band low-latency datalinks for cooperative engagement, onboard AI for adaptive tasking and intent inference, and modular payload bays capable of accommodating interchangeable sensor and effects packages.

Download Free sample to learn more about this report.

Collaborative Combat Aircraft Market Key Takeaways

- 2025 Market Size: USD 1.33 billion

- 2026 Market Size: USD 1.84 billion

- 2034 Forecast Market Size: USD 6.26 billion

- CAGR: 16.5% (2026–2034)

- North America dominated the market with a 44.36% share in 2025.

- The mission autonomy & AI software segment is projected to register the fastest growth at a 19.7% CAGR during the forecast period.

- The air superiority/fighter escort segment is expected to witness the highest growth, expanding at a 20.2% CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to witness significant growth, driven by rising airpower modernization and evolving Indo-Pacific security requirements.

North America

North America generated USD 0.59 billion in 2025 and is projected to reach USD 0.82 billion in 2026.

Europe

Europe is projected to register a 15.2% CAGR during the forecast period.

U.S.

U.S. market reached USD 0.55 billion in 2025.

Japan

Japan market reached USD 0.04 billion in 2025.

Read More

COLLABORATIVE COMBAT AIRCRAFT MARKET TRENDS

Shift Toward Modular and Software-Defined Combat-Air Systems is Emerging as a Key Market Trend

The market is increasingly being shaped by the transition from platform-centric unmanned aircraft development to modular, software-defined combat-air systems. CCAs are no longer viewed solely as low-cost wingman aircraft; they are being developed as networked combat nodes capable of integrating mission autonomy, secure datalinks, sensors, electronic warfare payloads, and weapons interfaces within a broader combat-air architecture. This trend is pushing manufacturers and defense agencies to prioritize open systems, software portability, autonomy reference architectures, and modular payload integration.

- For instance, in February 2026, the U.S. Air Force validated its Autonomy Government Reference Architecture across multiple vendor platforms under the Collaborative Combat Aircraft program, supporting a modular and open-systems approach to integrating autonomy across competing CCA air vehicles.

This trend is expected to increase procurement growth as defense forces increasingly require CCA platforms that can be rapidly upgraded to address evolving mission requirements, threat libraries, autonomy models, and payload configurations. As a result, demand is moving beyond aircraft procurement into mission-autonomy software, open mission systems, secure data architecture, digital engineering, and lifecycle software upgrades.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Need to Expand Combat Mass is Propelling Market Growth

The market is being driven by the increasing need to achieve air superiority and high combat capability without relying entirely on expensive crewed fighter fleets. Modern air forces face dense air-defense networks, electronic warfare threats, long-range missiles, and rapidly expanding unmanned systems activity. In this environment, CCAs offer a practical way to extend the reach of crewed fighters, increase sensor and weapons capacity, support electronic attack missions, absorb operational risk, and complicate enemy targeting decisions.

- For instance, in August 2025, the U.S. Air Force announced that the YFQ-42A Collaborative Combat Aircraft, developed by General Atomics, had entered flight testing to evaluate airworthiness, flight autonomy, and mission-system integration.

Therefore, the market is expected to gain momentum as air forces transition from experimental loyal-wingman concepts to operationally relevant CCA fleets. These aircraft are being positioned to support air dominance, ISR extension, electronic warfare, decoy operations, and strike support while reducing pilot exposure during high-risk missions. The shift toward distributed airpower and crewed-uncrewed teaming is increasing demand for air vehicles, mission autonomy, payload integration, secure command links, training systems, and sustainment infrastructure.

MARKET RESTRAINTS

Complexity of Validating Autonomous Behavior for Combat Missions to Limit Market Expansion

A key restraint for the market is the complexity of validating autonomous behavior for combat missions. CCAs must be capable of operating near crewed aircraft, interpreting mission objectives, responding to dynamic threats, and maintaining safe performance under degraded communications, electronic attack, and GPS-challenged environments. This creates a demanding validation burden across software, avionics, propulsion, flight controls, command interfaces, cybersecurity, and human-machine teaming.

The U.S. Department of Defense’s Responsible AI guidance emphasizes that AI-enabled systems should be designed to detect and avoid unintended consequences and should allow disengagement or deactivation if unintended behavior occurs. As a result, procurement timelines may be extended by certification requirements, test-range availability, software assurance, operator training, rules-of-engagement approval, and the need to prove safe teaming with crewed fighters. These factors are expected to limit rapid adoption and hamper the collaborative combat aircraft market growth.

MARKET OPPORTUNITIES

Allied Procurement Programs and Expansion of Multinational Industrial Partnerships Present Several Growth Opportunities in the Market

The market is expected to gain strong opportunities from allied CCA procurement and the expansion of multinational industrial partnerships. Several air forces are moving from concept development toward operational collaborative aircraft, creating opportunities for aircraft OEMs, autonomy providers, sensor manufacturers, electronic warfare companies, datalink suppliers, propulsion firms, and mission-system integrators. The opportunity is especially strong in countries seeking sovereign mission systems on proven or jointly developed uncrewed combat-air platforms.

- For instance, in December 2025, Boeing announced that the Australian Government awarded AUD 754 million to deliver, develop, and support seven MQ-28 Ghost Bat aircraft over a three-year period under the AIR6015 Autonomous Collaborative Platforms Air Program.

Europe is also creating new opportunities through sovereign UCCA and remote-carrier development. For instance, in March 2026, Airbus stated that it was preparing two Kratos Valkyrie aircraft equipped with a European mission system and targeting an operational uncrewed collaborative combat aircraft capability for the German Air Force by 2029.

MARKET CHALLENGES

High Development and Acquisition Costs to Hinder Industry Development

A major challenge for the collaborative combat aircraft market is the extremely high development, testing, and acquisition costs associated with designing crewless aircraft that can operate autonomously alongside manned fighters. Programs such as USAF's Air Combat Evolution (ACE) and Boeing's Loyal Wingman require significant investment in advanced AI, machine learning, secure datalinks, sensor fusion, and autonomous decision-making systems capable of operating in contested electromagnetic environments, which acts as a challenge to market development.

Segmentation Analysis

By Platform Type

Attritable/Reusable Loyal Wingman CCAs Segment to Lead due to Increasing Shift Toward Crewed- Uncrewed Teaming Operations

Based on platform type, the market is divided into attritable/reusable loyal wingman CCAs, high-end survivable CCAs, remote carriers/air-launched collaborative effectors, carrier-capable CCAs, and runway-independent/VTOL CCAs.

These platforms are designed to operate resiliently in electronic warfare target environments, with hardened communications to maintain mission continuity.

The attritable/reusable loyal wingman CCAs segment is expected to hold a leading share of the market as air forces prioritize affordable aircraft that can operate alongside crewed fighters while absorbing higher mission risk. These platforms support distributed sensing, weapons carriage, electronic attack, decoying, and force-multiplication missions without requiring a pilot onboard every combat aircraft. Demand is being supported by the shift from expensive crewed-only force structures to scalable crewed-uncrewed teaming formations.

- For instance, in December 2025, Boeing announced that Australia Government had awarded a USD 537.9 million contract to deliver, develop, and support seven MQ-28 Ghost Bat collaborative combat aircraft over a three-year period under the AIR6015 Autonomous Collaborative Platforms program.

The remote carriers/air-launched collaborative effectors segment is anticipated to rise with a steady growth rate of 15.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By System Offering

Rising Need to Validate Airworthiness to Propel Air Vehicle/Aircraft Platform Segment Growth

By system offering, the market is segmented into air vehicle/aircraft platform, mission autonomy & AI software, mission payload & sensors, command, control & datalink systems, and sustainment, training & MRO.

The air vehicle/aircraft platform segment is expected to dominate the market, as early CCA spending remains concentrated on the physical aircraft, propulsion systems, flight controls, avionics, power systems, and platform integration. As programs move from concept studies to production-representative test vehicles, the aircraft platform continues to represent the largest revenue segment. Demand is further supported by the need to validate airworthiness, endurance, payload carriage, survivability, and safe operation alongside crewed aircraft.

- For instance, in 2025, the U.S. Department of the Air Force began ground testing the YFQ-42A and YFQ-44A production-representative CCA vehicles, with evaluations focused on propulsion systems, avionics, autonomy integration, and ground-control interfaces.

The mission autonomy & AI software segment is expected to register the fastest CAGR of 19.7% over the forecast period.

By Mission Role

Increasing Need for Autonomy Validation and Operational Testing to Propel Training, Test & Tactics Development Segment Growth

On the basis of mission role, the market is segmented into air superiority/fighter escort, ISR, targeting & sensor extension, electronic warfare/SEAD-DEAD support, strike & deep attack, decoy/penetration aid, and training, and test & tactics development.

The training, test & tactics development segment is expected to acquire major collaborative combat aircraft market share during the early stages of CCA adoption, as defense forces require extensive flight testing, autonomy validation, tactics development, and operator training before large-scale deployment. CCAs must be tested for airworthiness, mission-system integration, teaming behavior, command interfaces, and safety procedures before operational fielding. This creates sustained demand for test aircraft, simulation environments, live-virtual-constructive training systems, and mission rehearsal infrastructure.

- For instance, in August 2025, the U.S. Air Force announced that the YFQ-42A Collaborative Combat Aircraft had entered flight testing to evaluate airworthiness, flight autonomy, and mission-system integration for the CCA program.

The air superiority/fighter escort is projected to register the CAGR of 20.2% over the forecast period.

By Autonomy Level

Rising Need to Build Trust in Autonomous Systems to Support Human-in-the-Loop/Human-on-the-Loop Control Segment Expansion

By autonomy level, the market is segmented into supervised/goal-based autonomy, collaborative multi-agent autonomy, human-in-the-loop/human-on-the-loop control, denied-environment autonomy, and swarm autonomy.

The human-in-the-loop/human-on-the-loop control segment is expected to lead the market, as military users continue to require human oversight for mission command, weapons employment, escalation control, and safety assurance. Although CCAs are becoming more autonomous, operational acceptance depends on maintaining clear human authority over sensitive combat decisions. This segment benefits from the need to build trust in autonomous systems while ensuring compliance with military doctrine, airspace safety, and rules-of-engagement requirements.

- For instance, in April 2024, DARPA’s Air Combat Evolution program conducted in-air tests of AI algorithms autonomously flying an F-16 against a human-piloted F-16, supporting the broader objective of building trust in human-machine collaborative combat autonomy.

The collaborative multi-agent autonomy segment is projected to grow with a steady growth rate of 19.5% over the forecast period.

By End User

Air Force Segment to Lead due to Investment in CCAs to Expand Combat Mass

By end user, the market is segmented into air force, navy/naval aviation, defense R&D/test agencies, marine/expeditionary forces, and joint commands/special mission users.

The air force segment is expected to dominate the Market, as CCA development is primarily driven by air-superiority, fighter escort, ISR extension, electronic warfare, and strike-support requirements. Air forces are investing in CCAs to expand combat mass, reduce pilot exposure, strengthen contested-airspace operations, and improve the operational reach of fifth- and sixth-generation aircraft. The segment is further supported by major government-funded CCA programs in the U.S. and Australia, where these platforms are being integrated into future air-combat force structures.

- For instance, in March 2025, the U.S. Air Force formally designated two aircraft under its CCA program: YFQ-42A from General Atomics and YFQ-44A from Anduril, marking a major step toward the operationalization of air force-led collaborative combat aircraft development.

The navy/naval aviation segment is likely to register a CAGR of 12.7% over the forecast period.

Collaborative Combat Aircraft Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Collaborative Combat Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025, with a valuation of USD 0.59 billion. The regional market is expected to reach USD 0.82 billion by 2026. The region’s leadership is primarily driven by the U.S. Air Force’s formal CCA program, strong defense R&D funding, advanced autonomy suppliers, and the transition from experimental loyal-wingman concepts toward production-representative aircraft. Market growth is further supported by the need to expand combat mass, reduce risk to crewed fighter aircraft, and strengthen air-superiority capabilities in contested environments. The region is also benefiting from the U.S. shift toward modular autonomy, mission-system integration, and open-architecture air-combat ecosystems.

- For instance, in March 2025, the U.S. Air Force formally designated two Collaborative Combat Aircraft as YFQ-42A, developed by General Atomics, and the YFQ-44A, developed by Anduril. These aircraft were identified as the first members of a new generation of uncrewed fighter aircraft designed to support air-superiority through autonomous CCA capabilities and crewed-uncrewed teaming.

U.S. Collaborative Combat Aircraft Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached around USD 0.55 billion in 2025. The U.S. is expected to remain the largest country-level market due to its dedicated CCA budget lines, active prototype development, large fifth-generation fighter fleet, advanced autonomy ecosystem, and clear procurement transition path. Growth is supported by the need to generate affordable combat mass, improve survivability in contested airspace, and deploy uncrewed aircraft capable of operating with F-35, F-22, NGAD-family systems, and future combat-air networks. The country is also focusing on the integration of CCAs with modern weapons systems to enhance force multiplication and improve operational effectiveness.

- For instance, in February 2026, the U.S. Air Force started captive-carry flight tests for Anduril’s YFQ-44A CCA prototype, mounting inert AIM-120 AMRAAM missiles to validate structural integrity and aerodynamic performance.

Europe

Europe is projected to record the fastest growth rate of 15.2% during the forecast period. The region is expected to witness strong growth, supported by FCAS (Future Combat Air System), GCAP (Global Combat Air Programme), UCCA (Uncrewed Collaborative Combat Aircraft), remote-carrier development, and sovereign mission-system initiatives. The region is moving from concept-level future combat-air planning toward more practical collaborative aircraft and remote-carrier experimentation. Growth is driven by the need to strengthen European combat-air autonomy, reduce dependence on non-European mission systems, and improve airpower resilience against advanced air defenses, electronic warfare, and high-intensity conflict scenarios.

- For instance, in July 2025, Airbus announced a partnership with Kratos to equip the XQ-58A Valkyrie with an Airbus-made German mission system, with the objective of making the system combat-ready for the German Air Force by 2029.

U.K. Collaborative Combat Aircraft Market

The U.K.’s market stood at around USD 0.09 billion in 2025, representing roughly 6.8% of global revenues.

Germany Collaborative Combat Aircraft Market

Germany market reached approximately USD 0.05 billion in 2025, equivalent to around 4.1% of global sales.

Asia Pacific

Asia Pacific is projected to witness the fastest growth owing to rising airpower modernization, contested Indo-Pacific security dynamics, island-defense requirements, and the growing need for crewed-uncrewed teaming across Australia, China, India, Japan, South Korea, and other regional defense markets. The region’s near-term demand is anchored by Australia’s MQ-28 Ghost Bat program, while China, India, Japan, and South Korea support the longer-term outlook through unmanned combat-air development, future fighter programs, and autonomous teaming concepts.

Japan Collaborative Combat Aircraft Market

The Japanese market stood at around USD 0.04 billion in 2025, accounting for roughly 3.0% of global revenues.

China Collaborative Combat Aircraft Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 0.13 billion, representing roughly 9.8% of global sales.

India Collaborative Combat Aircraft Market

The Indian market stood at around USD 0.07 billion in 2025, accounting for roughly 5.2% of global revenues.

Latin America and Middle East & Africa

Latin America represents a small but emerging market for CCA. Regional demand remains limited as most countries continue to focus on conventional fleet modernization, surveillance UAVs, border-security aircraft, and broader defense recapitalization rather than dedicated CCA procurement. Brazil is expected to remain the largest Latin American opportunity due to its stronger aerospace-industrial base and larger defense structure, while Mexico and the rest of Latin America are expected to gradually develop during the forecast period. In addition, CCA enhances Marine Corps operations by extending reach, survivability, and ISR capability across maritime and littoral missions. These platforms rely on secure, low-latency datalinks to enable real-time cooperative engagement and shared situational awareness among manned and unmanned platforms.

The Middle East & Africa region is expected to show stronger long-term growth potential than Latin America, primarily due to high defense spending in Gulf markets, advanced airpower modernization, and interest in unmanned combat-air capabilities. Saudi Arabia, the UAE, and Israel are expected to remain the key regional markets.

Saudi Arabia Collaborative Combat Aircraft Market

The Saudi Arabia market stood at around USD 0.02 billion in 2025, accounting for roughly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players Focus on Combining Affordable CCA Airframes into a Single Operational Solution to Boost Product Portfolio

The global market is characterized by competition among air vehicle manufacturers, autonomy software providers, mission-system integrators, defense electronics suppliers, and secure networking companies that are building deployable crewed-uncrewed teaming ecosystems. Competitive leadership is increasingly shaped by companies that can combine affordable CCA airframes, trusted mission autonomy, open architecture, secure datalinks, modular payload integration, and scalable production capacity into a single operational solution. The market is moving beyond prototype aircraft toward production-representative platforms, with the U.S. Air Force having designated the YFQ-42A, developed by General Atomics, and the YFQ-44A, developed by Anduril, under its CCA program. Meanwhile, Boeing’s MQ-28 Ghost Bat is positioned as an uncrewed collaborative combat aircraft designed to operate alongside existing military aircraft, supporting crewed-uncrewed teaming.

LIST OF KEY COLLABORATIVE COMBAT AIRCRAFT COMPANIES PROFILED

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Anduril Industries, Inc. (U.S.)

- The Boeing Company (U.S.)

- Kratos Defense & Security Solutions, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Airbus Defence and Space (Germany)

- BAE Systems plc (U.K.)

- Baykar Technologies (Türkiye)

- Turkish Aerospace Industries/TUSAŞ (Türkiye)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Airbus and Kratos advanced their German Uncrewed Collaborative Combat Aircraft effort by preparing two XQ-58A Valkyries for flight with a sovereign European mission system, targeting an operational UCCA capability for the German Air Force by 2029.

- February 2026: Shield AI was selected as a mission-autonomy provider for the U.S. Air Force Collaborative Combat Aircraft program, with its Hivemind autonomy software planned to fly aboard Anduril’s YFQ-44A Fury.

- February 2026: GE Aerospace and Kratos Defense secured a joint U.S. Air Force contract to design the GEK1500, a 1,500-lb thrust jet engine for small collaborative combat aircraft, leveraging maturation from their successful GEK800 cruise missile

- December 2025: The U.S. Air Force designated Northrop Grumman’s Project Talon prototype as YFQ-48A, establishing its official status as another semi-autonomous prototype aircraft under the CCA development pathway.

- October 2025: Anduril announced that its YFQ-44A CCA began flight testing with the U.S. Air Force, marking a major milestone for the CCA program’s affordable-mass and autonomous airpower roadmap.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform Type, By System Offering, By Mission Role, By Autonomy Level, By End User, and By Region |

| By Platform Type |

|

| By System Offering |

|

| By Mission Role |

|

| By Autonomy Level |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.33 billion in 2025 and is projected to reach USD 6.26 billion by 2034.

In 2025, the market value stood at USD 0.59 billion.

The market is expected to exhibit a CAGR of 16.5% during the forecast period.

By platform type, the attritable/reusable loyal wingman CCAs segment is expected to lead the market.

Rising need to expand combat mass is a key factor driving market expansion.

General Atomics Aeronautical Systems, Inc., Anduril Industries, Inc., The Boeing Company, and Kratos Defense & Security Solutions, Inc., are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us