Companion Animal Pharmaceuticals Market Size, Share & Industry Analysis, By Product (Veterinary Drugs {Anti-infectives, Anti-inflammatory Parasiticides, and Others}, and Veterinary Vaccines { Inactivated, Live Attenuated, Recombinant, and Others }), By Animal Type (Feline, Canine, Avian, and Others), By Route of Administration (Oral, Parenteral, Topical, Aerosol, and Others), By Distribution Channel (Veterinary Hospitals, Veterinary Clinics, Pharmacies & Drug Stores, and Others), and Regional Forecast, 2026-2034

Companion Animal Pharmaceuticals Market Size and Future Outlook

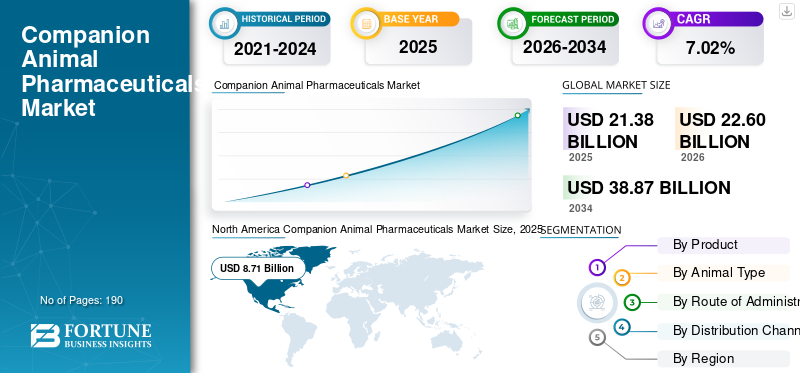

The global companion animal pharmaceuticals market size was valued at USD 21.38 billion in 2025. The market is projected to grow from USD 22.60 billion in 2026 to USD 38.87 billion by 2034, exhibiting a CAGR of 7.02% during the forecast period. North America dominated the companion animal pharmaceuticals market with a market share of 40.73% in 2025.

The global market is growing steadily as pet ownership rises and animals are increasingly treated as part of the family, which is driving higher spending on preventive care, chronic disease treatment, dermatology, pain management, vaccines, and parasite control. As veterinary visits become more frequent and pet owners seek better clinical outcomes, demand for branded and advanced therapies continues to increase. In addition, companies are expanding innovation in areas such as longer-duration protection, improved convenience, and broader-spectrum treatment, which is further supporting market expansion. Rising pet healthcare awareness and continuous product innovation are further expected to boost market growth during the forecast period.

- For instance, in September 2026, Merck Animal Health announced that the U.S. FDA approved BRAVECTO QUANTUM (fluralaner for extended-release injectable suspension) to treat and control Asian longhorned tick and Gulf Coast tick for 12 months in dogs. This type of approval supports the market by expanding treatment options, improving dosing convenience, and reinforcing demand for innovative companion-animal therapeutics.

Leading players in the industry, such as Zoetis Inc., Elanco, Boehringer Ingelheim Animal Health, and Merck Animal Health, are focusing on expanding their offerings in the market to boost their market position.

Download Free sample to learn more about this report.

Companion Animal Pharmaceuticals Market Key Takeaways

- 2025 Market Size: USD 21.38 Billion

- 2026 Market Size: USD 22.60 Billion

- 2034 Forecast Market Size: USD 38.87 Billion

- CAGR: 7.02% from 2026–2034

- North America dominated the companion animal pharmaceuticals market with a 40.73% share in 2025.

- The Canine segment accounted for the largest market share in 2025.

- The Veterinary Vaccines segment is projected to grow at a 9.26% CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 3.99 billion by 2026.

North America

North America held the leading position with a market value of USD 8.71 billion in 2025.

Europe

Europe is projected to reach USD 5.60 billion by 2026.

U.S.

The market is projected to reach USD 8.67 billion by 2026.

Japan

The market is estimated to reach USD 0.70 billion by 2026.

Read More

COMPANION ANIMAL PHARMACEUTICALS MARKET TRENDS

Rising Pet Humanization is Emerging as a Key Market Trend

As pets are increasingly treated like family members, owners are becoming more willing to seek advanced treatment rather than limiting care to only basic or emergency medicines. This is increasing demand for innovative therapies that can improve comfort, convenience, and long-term disease management in companion animals. Due to this shift, companies are focusing more on specialty products such as monoclonal antibodies and long-acting therapies for chronic conditions such as osteoarthritis. The result is stronger commercial momentum for premium companion animal pharmaceuticals and a broader move toward higher-value therapeutic categories across the market.

- For instance, in November 2025, Zoetis received marketing authorization from the European Commission for Lenivia (izenivetmab) for the reduction of pain associated with osteoarthritis in dogs. This development reflects the shift toward more advanced, long-acting, quality-of-life therapies that align with rising owner willingness to invest in better pet care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Pet Ownership is Driving Market Growth

As pet ownership increases, the number of animals requiring regular veterinary visits, preventive protection, and disease treatment also rises. This creates a larger, more stable demand base for companion animal pharmaceuticals across both everyday and specialty care categories. As more pet owners seek convenient, broad-coverage, and reliable treatment options, companies are launching and expanding products that address a wider range of companion animal health needs. The result is stronger product uptake, deeper penetration in veterinary clinics, and sustained commercial growth of the market. Moreover, key companies are focusing on regulatory approval and new product launches for their veterinary product offerings to strengthen their market positions.

- For instance, in December 2025, Elanco announced that the U.S. FDA granted conditional approval for Credelio Quattro-CA1 for the treatment of New World screwworm in dogs, calling it the first FDA conditional approval for a companion animal product for that use. The company stated that the product provides 7-in-1 parasite coverage, with updated product labeling expected to be introduced in 2026. This development supports market growth by showing how companies are broadening companion animal treatment options to meet rising demand for multi-purpose medicines in dogs.

MARKET RESTRAINTS

High Cost of Veterinary Care and Medicines is Limiting Treatment Uptake and Restraining Market Growth

As veterinary care becomes more expensive, more pet owners are reconsidering how often they visit clinics and which treatments they are willing to continue. This reduces the use of preventive products, delays diagnosis, and lowers acceptance of higher-value therapies, thereby weakening volume growth for companion animal pharmaceutical companies. The impact is stronger in long-term disease areas where treatment depends on regular monitoring and continued owner spending. As a result, rising treatment costs are becoming an important restraint on market expansion, even when clinical need remains high.

- For instance, in a 2026 AVMA article, veterinarians reported increased pet-owner price sensitivity and fewer visits, while noting that veterinary prices rose faster than inflation in 2025. The report indicated that companion animal practices experienced declining client visits even as pricing increased, highlighting how affordability pressures can reduce care utilization and slow pharmaceutical This trend represents a negative market signal, as fewer veterinary visits can directly translate into fewer prescriptions, delayed treatment starts, and lower continuity of care in companion animals.

MARKET OPPORTUNITIES

Expanding Pet Insurance Coverage to Create New Revenue Opportunities in the Market

The global market is creating new growth opportunities as pet insurance coverage gradually improves, helping reduce the financial burden of veterinary treatment for pet owners. When more owners have insurance support, they become more willing to approve diagnostics, chronic disease treatment, parasite control, dermatology care, and other prescription therapies that may otherwise be delayed or avoided due to cost. This improves treatment continuity, increases acceptance of higher-value medicines, and supports stronger demand for branded and specialty companion animal drugs. As a result, expanding pet insurance coverage is opening a wider commercial opportunity for pharmaceutical companies serving the market.

- For instance, in November 2025, BMO Insurance partnered with Trupanion to expand access to trusted, high-quality pet health coverage for Canadian pet owners. This development supports market growth by improving treatment affordability, encouraging owners to pursue timely care, and improving uptake of companion animal pharmaceuticals across a wider pet population.

MARKET CHALLENGES

Regulatory Requirements and Approval Complexity Slowing Product Commercialization and Market Growth

The global companion animal pharmaceuticals market faces an important challenge, as veterinary drug developers must meet detailed regulatory requirements related to safety, effectiveness, manufacturing quality, labeling, and post-approval compliance before products can reach the market. Since these requirements often involve multiple studies, technical submissions, protocol reviews, and documentation steps, development timelines become longer and product launch costs increase. This creates a greater burden for companies, especially when developing innovative therapies or new indications for companion animals. As a result, regulatory complexity can delay commercialization, slow pipeline expansion, and reduce the number of products that reach the market quickly.

- For instance, as per the March 12, 2026, AVMA article, “FDA animal drug pathways: What veterinarians need to know,” the association highlighted that veterinarians and stakeholders need to understand the distinctions among different FDA animal-drug pathways and remain compliant with the Animal Medicinal Drug Use Clarification Act and related regulations. This published article highlights the challenge by showing that the regulatory environment is complex enough to require additional education and navigation, which can slow adoption, development planning, and commercialization decisions across the market.

Segmentation Analysis

By Product

Veterinary Drug Segment Led due to their Broader Clinical Use

Based on product, the market is categorized into veterinary drugs and veterinary vaccines.

The veterinary drug segment accounted for the largest companion animal pharmaceuticals market share as they are used across a wider range of day-to-day and chronic conditions than vaccines, including pain, dermatology, parasitic infections, cardiac care, anti-infectives, and long-term disease management. This leads to more frequent prescribing and increased repeat treatment demand among companion animals, especially as pets live longer and require ongoing therapy. Due to this broader clinical use, drug revenues tend to grow more steadily than those from vaccines, which are often given on a scheduled or periodic basis. The result is a stronger commercial contribution from veterinary drugs within the market.

- For instance, in November 2025, Zoetis received marketing authorization from the European Commission for Portela (relfovetmab) for the alleviation of pain associated with osteoarthritis in cats. This development supports the dominance of veterinary drugs by demonstrating continued innovation in therapeutic medicines for chronic companion animal conditions, thereby expanding treatment demand beyond preventive care alone.

The veterinary vaccines segment is expected to grow at a CAGR of 9.26% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Animal Type

Canine Segment Dominated due to its Broader Use in Parasite Control

Based on animal type, the market is segmented into feline, canine, avian, and others.

In 2025, the canine segment accounted for the largest share of the market. Canines generally account for higher veterinary visit frequency, broader use of parasite control, stronger uptake of pain and allergy treatment, and a larger number of approved therapeutic options than many other companion animal categories. This leads to higher prescription volumes and stronger product penetration in the canine segment. In addition, companies continue to prioritize canine label expansions and product development, further increasing treatment availability and market value for dogs. As a result, canines remain the most commercially important animal type in the market.

Additionally, novel product launches by key companies and the regulatory approvals strengthen their market position.

- For instance, in April 2025, Zoetis received approval from the U.S. FDA for Simparica Trio chewable tablets, making it the first and only canine parasiticide indicated to prevent flea tapeworm infections by killing vector fleas. This supports canine dominance by highlighting how companies continue to expand canine-specific treatment labels, thereby boosting product usage and revenue concentration in dogs.

The feline segment is projected to grow at a CAGR of 8.00% during the forecast period.

By Route of Administration

Oral Segment to Lead due to its Benefits

Based on route of administration, the market is segmented into oral, parenteral, topical, aerosol, and others.

The oral segment is likely to dominate the market during the study period. Oral tablets and chewables offer easier at-home administration, better owner convenience, and stronger treatment acceptance for long-term parasite, dermatology, and chronic care management. Since many pet owners prefer treatments that do not require an in-clinic procedure, oral medications often achieve greater compliance and more consistent use. This makes oral formulations especially attractive for recurring therapies where convenience directly affects continuation rates.

- For instance, in September 2025, MSD Animal Health announced the launch of NUMELVI® (atinvicitinib) tablets for dogs, describing it as a veterinary innovation for fast, effective, and safe targeted itch relief. This supports oral dominance as it shows that innovative companion animal therapies continue to reach the market in tablet form, reinforcing owners' preference for convenient oral treatment.

The aerosol segment is projected to grow at a CAGR of 8.70% over the study period.

By Distribution Channel

Veterinary Hospitals Segment Led, Driven by Early Access to Newly Launched Pharmaceuticals

Based on distribution channel, the market is segmented into veterinary hospitals, veterinary clinics, pharmacies & drug stores, and others.

The veterinary hospitals accounted for the largest share of the market. Veterinary clinics are the primary point of diagnosis, prescribing, follow-up, and treatment recommendation for most companion animal conditions. Pet owners usually depend on clinic-based veterinarians to identify disease, select products, and guide treatment continuation, which gives clinics a stronger role in product flow than general retail channels. In addition, many newly launched companion animal pharmaceuticals are introduced first through veterinary prescribing pathways, further strengthening clinic-level distribution.

- For instance, in January 2025, Elanco launched Credelio Quattro chewable tablets for veterinarians to order, positioning the product directly through the veterinary channel. This supports the dominance of veterinary clinics as it shows that important new companion animal therapies are commercialized through veterinarian-led access and recommendations, keeping clinics central to market distribution.

The pharmacies & drug stores segment is projected to grow at a CAGR of 8.70% over the study period.

Companion Animal Pharmaceuticals Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Companion Animal Pharmaceuticals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 8.13 billion and maintained its leading position in 2025 at USD 8.71 billion. The region is growing strongly as pet ownership and pet-care spending remain high, which keeps demand elevated for chronic care drugs, dermatology products, pain therapies, vaccines, and parasiticides.

U.S. Companion Animal Pharmaceuticals Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 8.67 billion by 2026, accounting for roughly 38.38% of the global market.

Europe

Europe is projected to grow at a CAGR of 6.73% over the coming years, the second-highest among all regions. The region is poised to reach a valuation of USD 5.60 billion by 2026. Europe is growing as companion animal ownership is broad and well established, which supports recurring veterinary visits and steady demand for prescription medicines and preventive care.

U.K. Companion Animal Pharmaceuticals Market

The U.K. market is estimated to reach around USD 1.17 billion by 2026, representing roughly 5.16% of the global market.

Germany Companion Animal Pharmaceuticals Market

Germany's market is projected to reach approximately USD 1.29 billion by 2026, equivalent to around 5.71% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 3.99 billion by 2026 and secure the position of the third-largest region in the market. Asia Pacific is growing as pet ownership is rising quickly across several markets, and pet parents are spending more on veterinary care, wellness, and preventive treatments.

Japan Companion Animal Pharmaceuticals Market

The Japanese market is estimated to reach around USD 0.70 billion by 2026, accounting for approximately 3.09% of the global market.

China Companion Animal Pharmaceuticals Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimates at around USD 1.32 billion, representing approximately 5.83% of global sales.

India Companion Animal Pharmaceuticals Market

The Indian market is estimated to touch USD 0.53 billion by 2026, accounting for roughly 2.34% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate companion animal pharmaceuticals market growth during the forecast period. The Latin American market is set to reach a valuation of USD 2.37 billion by 2026. Latin America is growing as companion animal care becomes more formalized, while demand for parasite prevention and veterinary treatment is increasing in large pet-owning countries such as Brazil and Mexico.

In the Middle East & Africa, the GCC is set to reach USD 0.38 billion by 2026.

South Africa Companion Animal Pharmaceuticals Market

The South African market is projected to reach approximately USD 0.24 billion by 2026, accounting for roughly 1.05% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on New Product Launches to Boost Their Market Share

The global market is highly consolidated, with companies such as Zoetis Inc., Elanco, Boehringer Ingelheim Animal Health, Inc., Merck Animal Health, Camber Pharmaceuticals, Inc., and Sun Pharmaceutical Industries Ltd. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in February 2026, MSD Animal Health announced that the U.S. FDA approved NUMELVI (atinvicitinib tablets) for dogs to control pruritus associated with allergic dermatitis, and described it as the first and only second-generation JAK inhibitor for this use in dogs. This type of approval supports the companion animal pharmaceutical market by expanding advanced treatment options in dermatology, addressing a common chronic condition in dogs, and increasing the commercial value of innovative pet therapeutics.

Other notable players in the global market include Accord Healthcare, Fresenius Kabi AG, and Zydus Lifesciences Ltd. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the global forecast period.

LIST OF KEY COMPANION ANIMAL PHARMACEUTICALS COMPANIES PROFILED

- Zoetis Inc. (U.S.)

- Elanco (U.S.)

- Boehringer Ingelheim Animal Health (Germany)

- Merck Animal Health (U.S.)

- Virbac (France)

- Vetoquinol S.A. (France)

- Ceva Santé Animale (France)

- Norbrook Laboratories Limited(U.K.)

- Chanelle Pharma (Ireland)

- Bimeda Animal Health Ltd. (Ireland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Mars, Incorporated announced a partnership between its IAMS pet nutrition brand and Strava, the app for active people, to motivate millions of pet parents to move more with their pets.

- February 2026: Zoetis Inc. acquired Neogen’s animal genomics business for USD 160.0 million. The acquisition expanded its capabilities to deliver predictive insights, individualized care, and greater value to customers across major livestock and companion animal species.

- February 2026: MSD Animal Health received approval from the U.S. FDA for NUMELVI (atinvicitinib tablets) for dogs for the control of pruritus associated with allergic dermatitis, and described it as the first and only second-generation JAK inhibitor for this use in dogs.

- May 2025: MSD Animal Health received approval from the U.S. FDA for MOMETAMAX SINGLE (gentamicin, posaconazole, and mometasone furoate otic suspension), a single-dose product for dogs to treat otitis externa.

- February 2025: Boehringer Ingelheim launched SEMINTRA 4 mg/ml oral solution in Europe to manage both chronic kidney disease and hypertension in cats. First approved in 2013 for the reduction of proteinuria associated with chronic kidney disease in cats, SEMINTRA 4 mg/ml Oral Solution is also used to treat systemic hypertension in cats.

REPORT COVERAGE

The report on the global companion animal pharmaceuticals market provides a detailed analysis of the industry across key therapeutic and commercial areas. It covers market size and forecast assessment, major growth drivers, restraints, challenges, and emerging opportunities influencing market growth. The study also examines how rising pet ownership, increasing humanization of pets, growing spending on veterinary care, and continued product innovation are shaping the market landscape. In addition, it reviews recent developments, including product approvals, launches, partnerships, and expansion strategies, that are influencing competition across the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.02% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Animal Type, Route of Administration, Distribution Channel, and Region |

| By Product |

|

| By Animal Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 21.38 billion in 2025 and is projected to reach USD 38.87 billion by 2034.

In 2025, the market value stood at USD 8.71 billion.

The market is expected to grow at a CAGR of 7.02% over the forecast period.

By product, the veterinary drug segment led the market.

Increasing pet ownership is the key factor driving the market.

Zoetis Inc., Elanco., Boehringer Ingelheim Animal Health, Inc., Merck Animal Health, and Virbac are some of the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us