Coolant Distribution Units Market Size, Share & Industry Analysis, By Type (Liquid-to-Liquid CDUs, Air-to-Liquid CDUs, Direct-to-Chip CDUs, and Immersion Cooling Distribution Units), By Deployment Type (Rack-Level CDU, Row-Level CDU, and Centralized/Facility-Level CDU), By Cooling Capacity (Up to 100kW, 100 - 500 kW, 500 - 1,000 kW, and Above 1,000 kW), By End User (Data Centers, Semiconductor Manufacturing, Industrial Manufacturing, Energy & Power, and Others) and Regional Forecast, 2026 – 2034

Coolant Distribution Units Market Size and Future Outlook

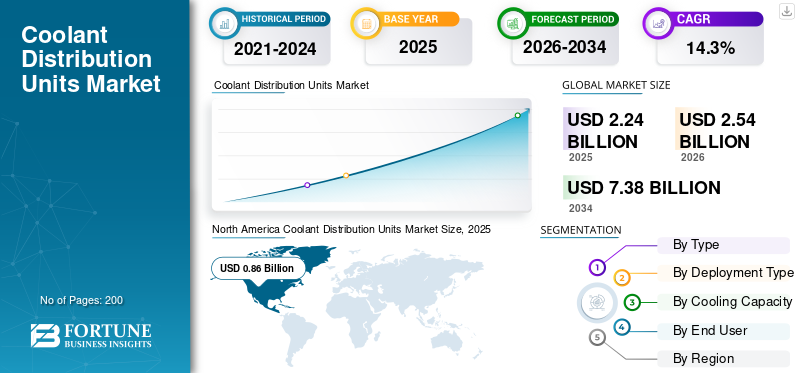

The global coolant distribution units market size was valued at USD 2.24 billion in 2025. The market is projected to grow from USD 2.54 billion in 2026 to USD 7.38 billion by 2034, exhibiting a CAGR of 14.3% during the forecast period. North America dominated the coolant distribution units market with a market share of 38.39% in 2025.

A thermal management system regulating and controlling coolant flow within facilities such as IT server racks, industrial equipment, and semiconductor tools defines the coolant distribution units market. CDUs find their extensive application in data centers, high-performance infrastructure, semiconductor fabrication plants, and other areas. Legacy systems, such as air-cooled data centers and colocation facilities, are adapting to energy-efficient and cost-effective solutions such as liquid cooling. Growing demand for advanced chips, high-density servers, and modular AI pods, government incentives, to further drive market growth.

- For instance, in July 2025, Boyd unveiled its 2.3 MW coolant distribution unit for AI liquid precise cooling applications.

Key players are using key competitive strategies such as product expansion in high-capacity ranges, integrating CDUs with rack systems, prefabricated infrastructures, and developing smart monitoring systems. Some of the key companies include Vertiv, Johnson Controls, and Liquidstack.

Tariffs have impacted the market share due to high component costs, pricing pressures, and supply chain destruction. Heavy dependency on specific geographies for electronics, pumps, and other components has directly impacted the raw material and component costs. However, the market is projected to witness growth during the forecast period owing to heavy demand for AI and high-density computing.

Download Free sample to learn more about this report.

COOLANT DISTRIBUTION UNITS MARKET TRENDS

AI Demand to Drive Prefabricated Cooling Architecture in the Market

Liquid cooling technologies and solutions are largely being designed and deployed for AI-related infrastructure. Hyperscalers are generating heavy demand and stricter deployment timelines, enabling faster time-to-market. Pre-fabricated CDU systems integrate several components such as pumps, controls, and heat exchangers, reducing installation risk and dependency on the workforce. End users get more flexible solutions to add cooling modules depending on their server capacity expansion, providing a more scalable option. Modular cooling makes it easier, faster, and safer to build and expand modern high-density data centers. Although the initial cost may be higher, it reduces the construction complexity, commissioning time, and other related factors.

- In October 2025, Vertiv announced its collaboration with NVIDIA to support prefabricated liquid cooling systems for AI-driven infrastructure deployments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Hyperscale AI Expansion and Increasing AI Compute Density to Drive Market Growth

AI-driven compute density is witnessing exponential growth, generating transformational cooling demand in modern data centers. Due to rising computing density, end users are preferring liquid cooling solutions over traditional cooling solutions. Sovereign AI initiatives and hyperscalers are expanding large-scale AI campuses. In high-density AI environments, even minor fluctuations in coolant flow can impact performance or reliability, making advanced CDUs mission-critical infrastructure. Growing rack densities and hyperscale deployment will further bolster the coolant distribution units market growth.

- In March 2024, LiquidStack introduced its Gigamodular CDU platform targeting deployment for hyperscale AI applications.

MARKET RESTRAINTS

Legacy infrastructure and Retrofit Complexity to Limit Market Growth

A large number of legacy facilities require structural provisions, piping infrastructure, and hydraulic layouts for cooling systems. Integrating CDUs into these environments often requires floor modifications, installation of coolant distribution piping, leak detection systems, and upgraded monitoring controls. In some cases, operators must redesign airflow management strategies and reinforce rack structures to handle higher-density deployments. The perceived risk of coolant leakage and potential downtime further increases hesitation among enterprise operators, particularly in mission-critical environments.

MARKET OPPORTUNITIES

Rising Edge AI Deployments are Driving Demand for Compact and Modular CDU Systems

As AI inference workloads move closer to end users, such as in telecom facilities, smart cities, autonomous systems, and regional micro data centers—there is increasing demand for compact, high-density computing at the edge. Unlike hyperscale campuses, edge facilities operate in space-constrained environments with limited mechanical infrastructure, making traditional large cooling systems impractical. As rack densities increase in these smaller sites, liquid cooling becomes necessary to maintain performance and reliability. This creates demand for compact, rack-level, or small modular CDUs that can be deployed quickly with minimal on-site construction.

The distributed nature of edge AI also multiplies the number of deployment sites, expanding the total addressable market volume. As enterprises and telecom operators scale edge AI networks, modular and scalable CDU systems are positioned to become critical enablers of localized high-performance computing.

MARKET CHALLENGES

Standardized Gaps in Liquid Cooling Market will Slowdown Growth

Unlike traditional air-cooling systems, which have decades of established design norms, liquid cooling for data centers is still evolving. One of the key structural challenges in the Coolant Distribution Units (CDU) market is the lack of standardized architecture across the liquid cooling ecosystem. There is currently no universal standard governing rack interfaces, manifold designs, coolant types, pressure tolerances, or quick-disconnect configurations. This creates interoperability challenges between server OEMs, CDU manufacturers, and facility operators. Addressing these gaps through industry collaboration and standardized design frameworks will be critical to accelerating mainstream CDU adoption across global data center markets.

Segmentation Analysis

By Type

Liquid-to-Liquid CDUs Dominate Owing to Demand from Hyperscale and Enterprise Data Centers

Based on type, the market is divided into liquid-to-liquid CDUs, air-to-liquid CDUs, direct-to-chip CDUs, and immersion cooling distribution units.

Liquid-to-Liquid CDUs currently dominate market revenue due to their widespread deployment in hyperscale and enterprise data centers. These systems efficiently transfer heat between the IT coolant loop and facility water systems without fluid mixing, making them highly reliable and scalable. Their strong installed base, compatibility with existing chilled water infrastructure, and suitability for multi-megawatt deployments position them as the primary revenue contributor.

Direct-to-Chip CDUs are expected to witness the highest growth rate, driven by rising AI and high-performance computing workloads. These systems deliver coolant directly to processors via cold plates, enabling efficient thermal management at rack densities exceeding 80–120 kW. As AI infrastructure expands globally, direct-to-chip liquid cooling is becoming increasingly essential, accelerating demand for associated CDU systems.

- In August 2024, LiquidStack launched its CDU compatible with direct-to-chip cooling solutions designed for advanced computing solutions.

By Deployment Type

Large-Scale Hyperscale AI Campus Deployments are Driving Dominance of Centralized/Facility-Level CDUs

Based on deployment type, the market is segmented into rack-level CDU, row-level CDU, and centralized/facility-level CDU.

Centralized/facility-level CDUs currently dominate market revenue due to their deployment in large hyperscale and multi-megawatt AI data center campuses. These systems are designed to support multiple rows or entire data halls from a centralized mechanical plant, often delivering cooling capacities exceeding 1 MW. Hyperscale operators prefer centralized CDUs in greenfield projects as they enable better hydraulic control, optimized energy efficiency, and simplified facility-level monitoring. Hyperscale operators prefer centralized CDUs in greenfield projects as they enable better hydraulic control, optimized energy efficiency, and simplified facility-level monitoring.

Rack-level solutions are expected to witness the highest growth rate owing to their suitability for AI pods, edge data centers, and retrofit environments where centralized mechanical expansion may be constrained. Their plug-and-play nature reduces deployment timelines and enables faster time-to-market for hyperscale AI infrastructure.

By Cooling Capacity

500-1000kW Leads Owing to its Scalability and Performance

Based on cooling capacity, the market is segmented into up to 100kW, 100 - 500 kW, 500 - 1,000 kW, and above 1,000 kW.

The 500–1,000 kW cooling capacity segment currently dominates market revenue as it represents the optimal balance between scalability, performance, and deployment flexibility. This capacity range is widely adopted in hyperscale pods, large enterprise data centers, and colocation facilities deploying high-density AI clusters. The segment benefits from both greenfield deployments and retrofit upgrades, particularly where operators are expanding liquid cooling zones incrementally.

The above 1,000 kW segment is expected to witness the highest growth rate, driven by hyperscale AI campuses and sovereign compute infrastructure projects. As GPU cluster sizes expand and data halls scale toward multi-megawatt deployments, operators increasingly prefer centralized high-capacity CDUs capable of supporting entire AI halls or multiple rows simultaneously. Hyperscale greenfield projects are embedding multi-megawatt liquid cooling architecture into their baseline design.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rapid AI and Hyperscale Expansion Is Driving Data Centers to Lead CDU Market Growth

Based on end user, the market is segmented into data centers, semiconductor manufacturing, industrial manufacturing, energy & power, and others.

Data centers dominate the revenue and coolant distribution market share over other end users due to the rapid expansion of AI, cloud computing, and hyperscale infrastructure worldwide. Rising rack power densities, particularly in GPU-based AI clusters, are making liquid cooling a necessity rather than an option, directly increasing CDU adoption. As rack densities exceed 80–120 kW in GPU-driven environments, CDUs become a critical component in managing coolant flow, pressure, and thermal stability.

The data center segment’s growth is largely driven by the rapid expansion of AI, cloud computing, and hyperscale infrastructure worldwide. Rising rack power densities, particularly in GPU-based AI clusters, are making liquid cooling a necessity rather than an option, directly increasing CDU adoption.

Coolant Distribution Units Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Coolant Distribution Units Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the CDU market due to its concentration of hyperscale cloud providers and AI infrastructure investments. Rapid deployment of high-density GPU clusters is accelerating liquid cooling adoption across new and retrofit facilities. The region’s advanced data center ecosystem and early integration of direct-to-chip cooling solutions make CDUs a foundational infrastructure component. As AI-driven CAPEX continues to rise, North America remains the largest revenue contributor globally.

U.S. Coolant Distribution Units Market

The U.S. dominates the North American market and is anticipated to garner a revenue of approximately USD 0.75 billion in 2026.

Europe

Europe’s CDU demand is strongly influenced by sustainability regulations and energy efficiency requirements. Operators are increasingly adopting liquid cooling systems to meet stringent environmental standards and reduce energy consumption. Government-backed digital sovereignty initiatives are also driving new AI-ready data center construction. As a result, CDUs are gaining traction as energy-efficient cooling solutions aligned with the region’s regulatory landscape.

U.K. Coolant Distribution Units Market

In 2026 the U.K. market is estimated to reach USD 0.13 billion, representing roughly 5.2% of global market revenues.

Germany Coolant Distribution Units Market

Germany’s market reached USD 0.14 billion in 2026, equivalent to around 5.4% of the global sales.

Asia Pacific

Asia Pacific is witnessing rapid CDU market growth driven by hyperscale data center expansion and semiconductor manufacturing investments. China, Japan, South Korea, and Taiwan have strong fabrication and high-performance computing ecosystems requiring advanced thermal management. Greenfield AI campuses are increasingly designed with liquid cooling infrastructure embedded at the outset. This structural growth positions Asia Pacific as one of the fastest-expanding regional markets.

India Coolant Distribution Units Market

In 2026, Indian is projected to hit USD 0.13 billion, accounting for roughly 5.2% of the global market. Supportive government-led investment and growing AI infrastructure will propel the country’s market growth.

China Coolant Distribution Units Market

China’s market is projected to remain dominant in Asia Pacific in 2026 with revenues reaching USD 0.23 billion, representing roughly 9.2% of global sales.

ASEAN Coolant Distribution Units Market

The ASEAN market will reach USD 0.14 billion, accounting for roughly 5.4% of revenue.

South America

South America’s CDU market is emerging gradually as regional colocation facilities expand and enterprises modernize IT infrastructure. While rack densities remain lower compared to other regions, increasing cloud adoption and AI readiness initiatives are driving selective liquid cooling deployments.

Middle East & Africa

The Middle East & Africa is witnessing growing CDU demand driven by sovereign AI programs and large-scale digital infrastructure projects. The UAE and Saudi Arabia are investing heavily in hyperscale and AI-ready data centers as part of economic diversification strategies. High ambient temperatures further necessitate efficient liquid cooling solutions. Greenfield project development provides strong opportunities for centralized, high-capacity CDU deployments.

GCC Coolant Distribution Units Market

The GCC market reached USD 0.05 billion in 2026, representing roughly 1.9% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Investments and Global Delivery Models Strengthening Cross-Border Service Expansion

Key players in the Coolant Distribution Units (CDU) market are primarily focusing on innovation, scalability, and ecosystem integration to strengthen their competitive positioning. Companies are developing high-capacity, AI-optimized CDUs capable of supporting multi-megawatt deployments to meet rising rack power densities in hyperscale data centers. Modular and prefabricated cooling solutions are gaining importance, enabling faster deployment and reduced on-site complexity. Strategic partnerships with GPU manufacturers and server OEMs are helping vendors align CDU designs with evolving chip-level thermal requirements.

Many players are also expanding regional manufacturing capabilities to mitigate supply chain risks and improve delivery timelines. Integration of smart monitoring systems, leak detection, and predictive maintenance features is becoming a key differentiator.

- For instance, in September 2025, Johnson Controls introduced its Silent-Aire liquid cooling portfolio along with a new CDU platform and wide range of cooling capacities.

LIST OF KEY COOLANT DISTRIBUTION UNITS COMPANIES PROFILED

- Vertiv (U.S.)

- Schneider Electric (France)

- Johnson Controls (U.S.)

- Carrier (U.S.)

- Modine Manufacturing (U.S.)

- LiquidStack (U.S.)

- CooIIT Systems (Canada)

- nVent Electric (U.S.)

- Flex (Singapore)

- Boyd Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Boyd Corporation more than doubled its liquid cooling manufacturing capacity in Mexico to strengthen production capabilities for AI infrastructure, hyperscale, and colocation data centers.

- November 2025: Carrier launched a new family of Coolant Distribution Units under its QuantumLeap™ platform to support large-scale liquid-cooled data center infrastructures.

- October 2025: KSTAR unveiled its next-generation CDU solution as part of its LiquiX liquid cooling portfolio targeting AI data centers.

- October 2025: Boyd Corporation introduced the ROL4000, a 2 MW high-capacity CDU engineered for large-scale AI data center cooling applications.

- September 2025: Johnson Controls expanded its Silent-Aire liquid cooling portfolio with scalable CDU platforms designed for AI-driven data center environments.

REPORT COVERAGE

The global coolant distribution units market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Deployment Type, Cooling Capacity, End User, and Region |

| By Type |

|

| By Deployment Type |

|

| By End User |

|

| By Cooling Capacity |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.24 billion in 2025 and is projected to reach USD 7.38 billion by 2034.

In 2025, North Americas market value stood at USD 0.86 billion.

The market is expected to exhibit a CAGR of 14.3% during the forecast period.

By type, the liquid-to-liquid CDUs dominate the market revenue.

Hyperscale AI expansion and increasing AI compute density drive the market growth.

Vertiv, Boyd Corporation, Modine Manufacturing, are the major players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us