Copper Fungicides Market Size, Share & Industry Analysis, By Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, and Others), By Product Type (Copper Oxychloride, Copper Hydroxide, Cuprous Oxide, Copper Sulfate, and Others), By Formulation (Water-Dispersible Granules, Soluble Granules, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

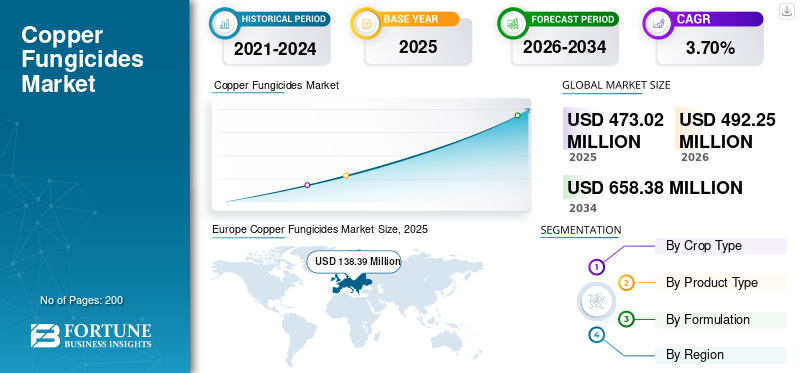

The global copper fungicides market size was valued at USD 473.02 million in 2025. The market is projected to grow from USD 492.25 million in 2026 to USD 658.38 million by 2034, exhibiting a CAGR of 3.70% during the forecast period. Europe dominated the global copper fungicides market with a market share of 29.26% in 2025.

The demand for copper fungicides is driven by the increasing prevalence of fungal diseases in crops, rising demand for sustainable plant protection solutions, and the widespread acceptance of copper-based fungicides in organic and conventional farming. Copper fungicides, widely used to control bacterial and fungal pathogens such as downy mildew, blights, leaf spots, and bacterial canker, remain integral to disease management programs across cereals, fruits, vegetables, and plantation crops.

Further, with rising concerns about crop losses due to climate-induced disease outbreaks, farmers and agricultural production organizations are increasingly relying on copper fungicides due to their broad-spectrum efficacy and long-standing regulatory acceptance. Major agricultural sector companies are expanding their copper-based formulations, active ingredients, improving micronization technologies, and investing in R&D to increase efficiency while reducing environmental impact. UPL Limited, Corteva Agriscience, BASF SE, Bayer AG, and Nufarm Limited dominate the global market growth.

Download Free sample to learn more about this report.

Copper Fungicides Market KEY TAKEAWAYS

- 2025 Market Size: USD 473.02 million

- 2026 Market Size: USD 492.25 million

- 2034 Forecast Market Size: USD 658.38 million

- CAGR: 3.70% from 2026–2034

- Europe dominated the market with a 29.26% share in 2025.

- Cereals & Grains segment was the largest application segment.

- Copper Oxychloride remained the leading product type, growing at a CAGR of 4.04%.

Europe

USD 138.39 million in 2025. Strong demand driven by vineyards and organic farming, despite regulatory limits on copper usage.

Asia Pacific

USD 130.12 million in 2025. Large-scale fruit, vegetable, and cereal production with high disease pressure and expanding organic farming drive strong demand.

North America

USD 71.50 million in 2025. Stable demand supported by vineyards, almonds, berries, citrus, and greenhouse crop protection needs.

U.S.

Strong contributor within North America. Demand driven by vineyards, specialty crops, and greenhouse vegetable production.

Middle East & Africa

USD 19.65 million in 2025. Growth supported by greenhouse farming, irrigated agriculture, and expanding horticulture production across key countries such as South Africa, Egypt, Kenya, Saudi Arabia, and the UAE.

Read More

MARKET DYNAMICS

Market Drivers

Increasing Incidence of Crop Fungal Diseases to Drive Market Growth

The global rise in fungal and bacterial crop diseases, driven by climate variability, high humidity conditions, and the proliferation of pathogens, is significantly increasing copper fungicide adoption. Copper fungicides continue to serve as a first-line defense in integrated pest management (IPM) programs, especially in vineyards, citrus orchards, tomato farms, and potato fields. In horticulture and fruit production, diseases such as downy mildew, anthracnose, black spot, and bacterial blight are becoming more aggressive, prompting increased reliance on copper-based formulations for both preventive and curative control.

- According to the Food and Agriculture Organization (FAO), up to 40% of global crop production is lost annually to pests and diseases, with fungal pathogens accounting for a substantial share.

Market Restraints

Regulatory Restrictions on Copper Usage and Environmental Concerns to Limit Growth

Growing environmental concerns regarding copper accumulation in soils have led to tightening regulatory measures across several markets. Long approval cycles and stringent residue limits also restrict the entry of new copper fungicide formulations in many regions. The need for compliance with updated environmental and toxicological guidelines limits product innovation and raises manufacturing costs.

- The European Union, for instance, has restricted maximum copper application levels to 4 kg/ha/year, posing challenges for farmers with recurring disease pressure.

Market Opportunities

Development of Low-Dose, High-Efficiency Copper Formulations to Unlock Growth Potential

Low-dose, high-efficiency copper fungicide formulations, such as Kocide 3000 and Mastercop, enhance biologically active copper ion release and coverage, enabling effective disease control at reduced application rates compared to traditional compounds such as copper oxychloride. These innovations address environmental concerns by minimizing copper accumulation in soil while maintaining multi-site activity against fungal and bacterial pathogens in crops such as fruits, vegetables, and potatoes.

Copper Fungicides Market Trends

Integration of Copper Fungicides With Biological Crop Protection Solutions To Shape Market

Integration of copper fungicides with biological crop protection solutions enhances Integrated Pest Management (IPM) strategies by combining broad-spectrum chemical efficacy with targeted biocontrol, reducing reliance on synthetic pesticides while addressing disease resistance and supporting sustainable agriculture. Copper fungicides integrate seamlessly into IPM programs alongside biological agents, cultural practices, and resistant varieties, increasing demand for organic farming growth and fungicide resistance to synthetics. The surge in organic farming activities has significantly influenced the global copper fungicides market demand in recent years. Advancements in nano-copper and controlled-release formulations minimize environmental accumulation while boosting efficacy in farmlands and greenhouses.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Crop Type

Large-scale Production and Persistent Fungal Diseases to Lead Cereals & Grains Segment’s Growth

The market is segmented into cereals & grains, fruits & vegetables, oilseeds & pulses, and others.

Cereals & grains continue to dominate copper fungicide consumption, increasing from USD 243.43 million in 2025 to USD 330.97 million by 2034, reflecting a CAGR of 3.43% (2026–2034). This strong position is driven by large-acre cereal production (wheat, rice, barley, and maize) and persistent fungal diseases such as downy mildew and leaf blight. Expanding acreage across Asia and Latin America further sustains copper use for preventive disease control.

The fruits & vegetables segment is expected to grow significantly in the forecast period, with a CAGR of 4.46% in 2026.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Affordability and Compatibility to Lead Copper Oxychloride Segment Growth

The market is segmented into copper oxychloride, copper hydroxide, cuprous oxide, copper sulfate, and others.

Copper oxychloride grows from USD 197.35 million in 2025 to USD 282.91 million by 2034, at a CAGR of 4.04%. It remains the most widely used formulation worldwide, favored for affordability, broad-spectrum activity, and compatibility with multiple crop types.

The copper hydroxide segment is expected to grow significantly at a CAGR of 3.56% during the forecast period.

By Formulation

Handling Benefits and Stability Fuel Water-Dispersible Granules (WG) Segment Market Leadership

The market is segmented into water-dispersible granules (WG), soluble granules (SG), and others.

Water-dispersible granules (WG) formulations dominate the copper fungicides market share and rise from USD 251.08 million in 2025 to USD 346.09 million by 2034, registering a CAGR of 3.59%. WG formulations offer superior stability, dust-free handling, and better leaf coverage, supporting increased uptake across large-scale farms.

The soluble granules segment is anticipated to grow at a CAGR of 4.14% during the global copper fungicides forecast period.

Copper Fungicides Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Copper Fungicides Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

Europe’s copper fungicides market growth is expected to rise from USD 138.39 million in 2025 to USD 181.45 million by 2034, recording a moderate CAGR of 3.01%. Despite stringent regulatory restrictions on annual copper application limits, demand remains stable due to the region's highly disease-sensitive crops, especially in vineyards and potato fields across Italy, Spain, France, and Germany. Copper fungicides continue to be fundamental in organic farming, where synthetic fungicides are restricted. The increasing incidence of downy mildew, blight, and other fungal diseases, exacerbated by climate change, continues to support copper fungicide adoption, particularly in low-residue and organic production systems.

Asia Pacific

Asia Pacific is the largest and fastest-growing regional market for copper fungicides, with the market expanding from USD 130.12 million in 2025 to USD 192.95 million by 2034, reflecting a robust CAGR of 4.43% during 2026–2034. The region’s dominance is driven by extensive fruit, vegetable, and cereal production across China, India, Vietnam, Indonesia, and the Philippines, where humid and monsoon-influenced climates significantly increase fungal and bacterial disease pressure. High dependency on copper fungicides to manage recurring diseases in grapes, citrus, tomatoes, potatoes, and rice supports strong regional consumption. Rising adoption of protected cultivation and organic farming, along with technological advancements in micronized copper formulations, further accelerates market growth in the Asia Pacific.

North America

North America maintains a stable and mature position in the market, increasing from USD 71.50 million in 2025 to USD 98.04 million by 2034, at a steady CAGR of 3.53%. The U.S. dominates regional consumption, largely due to extensive use in vineyards, almonds, potatoes, berries, citrus, and greenhouse vegetables. The ability of copper fungicides to effectively manage fungal diseases is a key factor fueling their demand in the market.

South America

South America represents one of the fastest-expanding markets, growing from USD 113.35 million in 2025 to USD 161.43 million in 2034, at an impressive CAGR of 3.97%. The region’s tropical and subtropical climate creates persistent disease pressure, driving copper fungicide use in high-value crops such as soybeans, grapes, citrus, bananas, and coffee. Brazil, Chile, and Argentina lead demand due to large-scale fruit and grain export industries that require reliable fungicidal protection. Increasing climatic variability, marked by heavy rainfall and humidity, further elevates the prevalence of fungal and bacterial infections, reinforcing copper fungicides as an essential tool for crop disease management.

Middle East & Africa

The Middle East & Africa market shows steady expansion, rising from USD 19.65 million in 2025 to USD 24.51 million by 2034, with a CAGR of 2.44%. Growth is supported by increasing horticulture production, greenhouse farming, and irrigated agriculture in countries such as South Africa, Morocco, Kenya, Egypt, Saudi Arabia, and the UAE. Copper fungicides are widely used for disease control in citrus, grapes, tomatoes, cucumbers, dates, and specialty crops that thrive in controlled microclimates. Although smaller than other regions, the Middle East & Africa continues to adopt copper fungicides due to cost-effectiveness and the rising need to protect crops from fungal and bacterial pathogens prevalent under irrigation-intensive farming systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong R&D, Product Innovation, and Strategic Acquisitions Drive Competition

The market consists of agricultural chemical manufacturers, crop protection companies, and formulation specialists. Leading players invest heavily in micronized copper technologies, environmentally optimized formulations, and geographic expansion to strengthen market presence.

Key Players in the Copper Fungicides Market

|

Rank |

Company Name |

|

1 |

UPL Limited |

|

2 |

Corteva Agriscience |

|

3 |

BASF SE |

|

4 |

Bayer AG |

|

5 |

Nufarm Limited |

List of Key Copper Fungicides Companies Profiled

- UPL Limited (India)

- Corteva Agriscience (U.S.)

- BASF SE (Germany)

- Nufarm Limited (Australia)

- Syngenta AG (Switzerland)

- ADAMA Agricultural Solutions Ltd. (Israel)

- Albaugh LLC (U.S.)

- FMC Corporation (U.S.)

- Ishihara Sangyo Kaisha, Ltd. (Japan)

- Nordox Industrier AS (Norway)

- CERTIS USA LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2022: Bharat Certis AgriScience Ltd., a Mitsui & Co. group company, launched Kocide 3000, an advanced copper hydroxide fungicide (46.1% w/w WG with 30% metallic copper).

- July 2024: FMC India launched VELZO and COSUIT fungicides to protect fruits and vegetables from fungal diseases early in the crop cycle, targeting crops such as grapes, tomatoes, potatoes, paddy, chilli, and tea.

- July 2024: Albaugh launched its 46% Copper Hydroxide WDG product in China, through Rotam Global AgroSciences Limited. This water-dispersible granule (WDG) fungicide uses HiBio technology to enhance copper ion release, improving efficacy, crop safety, and rain resistance with over 90% suspension and dispersion rates.

- February 2023: Certis Biologicals introduced Kocide 50DF, a high-load copper biofungicide formulation designed for both preventative and curative control of fungal diseases such as blight, anthracnose, canker, phytophthora, and rot in crops such as citrus, vegetables, fruits, tree nuts, and specialty crops.

REPORT COVERAGE

The global copper fungicides industry report analyses the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global copper fungicides market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.70% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Crop Type

|

|

By Product Type · Copper Oxychloride · Copper Hydroxide · Cuprous Oxide · Copper Sulfate · Others |

|

|

By Formulation

|

|

|

By Region · North America (By Crop Type, Product Type, Formulation, and Country) • U.S. (By Crop Type) • Canada (By Crop Type) • Mexico (By Crop Type) · Europe (By Crop Type, Product Type, Formulation, and Country) • Germany (By Crop Type) • Spain (By Crop Type) • Italy (By Crop Type) • France (By Crop Type) • U.K. (By Crop Type) • Rest of Europe (By Crop Type) · Asia Pacific (By Crop Type, Product Type, Formulation, and Country) • China (By Crop Type) • Japan (By Crop Type) • India (By Crop Type) • Australia (By Crop Type) • Rest of Asia Pacific (By Crop Type) · South America (By Crop Type, Product Type, Formulation, and Country) • Brazil (By Crop Type) • Argentina (By Crop Type) • Rest of South America (By Crop Type) · Middle East & Africa (By Crop Type, Product Type, Formulation, and Country) • South Africa (By Crop Type) • UAE (By Crop Type) • Rest of the Middle East & Africa (By Crop Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 473.02 million in 2025 and is anticipated to reach USD 658.38 million by 2034.

At a CAGR of 3.70%, the global market will exhibit steady growth over the forecast period.

By crop type, the cereals & grains segment leads the market.

Europe held the largest market share in 2025.

The increasing incidence of crop fungal diseases drives the market growth.

UPL Limited, Corteva Agriscience, BASF SE, Bayer AG, and Nufarm Limited are the leading companies in the market.

The integration of copper fungicides with biological crop protection solutions is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us