Counter-UAS Sensor Fusion Market Size, Share, Russia-Ukraine and Middle East Conflicts, & Industry Analysis, By Component (Software & Analytics, Others), By Sensor Type Integrated, By Fusion Architecture (AI/ML-Enabled Fusion, Edge-Based Fusion, and Others), By Deployment Mode (Fixed-Site, Man-Portable, and Others), By Application (Military Base Protection, Critical Infrastructure, and Others), By Threat Type (Small Commercial Drones, FPV Drones, and Others), By End User (Military & Defense, Critical Infrastructure Operators, and Others), and Regional Forecast, 2026-2034

Counter-UAS Sensor Fusion Market Size and Future Outlook

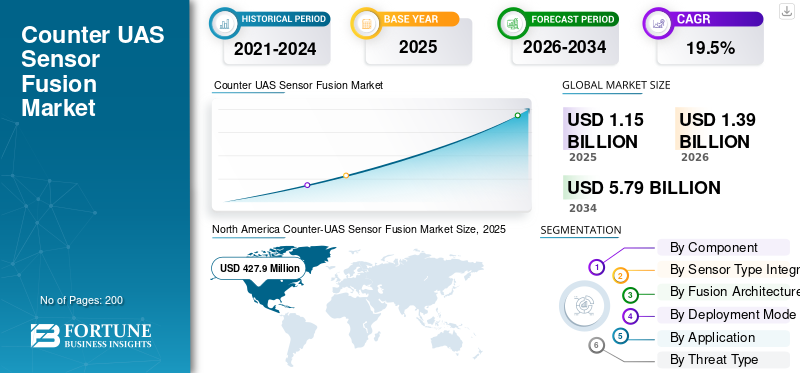

The global counter-UAS sensor fusion market size was valued at USD 1,150.2 million in 2025. The market is projected to grow from USD 1,395.3 million in 2026 to USD 5,790.0 million by 2034, exhibiting a CAGR of 19.5% during the forecast period. North America dominated the counter UAS sensor fusion market with a market share of 37.20% in 2025.

Counter-UAS sensor fusion is the integration of sensor data from radar, rf sensors, EO/IR cameras, acoustic sensors, and command and control systems into one operating picture for drone detection, detection tracking, classification, and response. The market is being driven by rising drone threats from low-cost UAS systems, FPV drones, loitering munitions, and swarm attacks. Further, pushing buyers toward AI driven and machine learning-enabled counter drone system architectures that improve situational awareness in real time.

Key players include Anduril Industries, Dedrone by Axon, DroneShield, Thales, Leonardo, HENSOLDT, Rafael, Elbit Systems, D-Fend Solutions, Sentrycs, MARSS, and QinetiQ. These companies are leading the market through the integration of RF sensors, radar, EO/IR, acoustic sensors, autonomous interceptor drones, and command and control software. This enables them to convert fragmented sensor data into real-time situational awareness and facilitate faster responses against drone threats.

Download Free sample to learn more about this report.

Counter UAS Sensor Fusion Market Key Takeaways

- 2025 Market Size: USD 1,150.2 million

- 2026 Market Size: USD 1,395.3 million

- 2034 Forecast Market Size: USD 5,790.0 million

- CAGR: 19.5% from 2026-2034

- North America dominated the counter-UAS sensor fusion market with a 37.20% share in 2025.

- The middleware & sensor integration segment is projected to grow at a CAGR of 23.3% during the forecast period.

- The radar-based fusion segment is expected to register a CAGR of 19.4% during the forecast period.

North America

North America is anticipated to grow at a CAGR of 16.9% during the forecast period.

Asia Pacific

Asia Pacific is projected to register a CAGR of 20.6% during the forecast period.

Europe

Europe is expected to grow at the fastest regional CAGR of 21.9% during the forecast period.

U.S.

The U.S. market stood at USD 390.5 million in 2025 and is projected to grow at a CAGR of 16.4% during the forecast period.

Japan

Japan is expected to witness steady growth during the forecast period.

Read More

Counter-UAS Sensor Fusion MARKET TRENDS

AI-Enabled Multi-Sensor Fusion Drives the Shift Toward Real-Time Counter-UAS Decision Support

A major trend in the global market is the move from standalone drone detection systems toward AI driven, machine learning-enabled sensor fusion platforms that combine radar, RF sensors, EO/IR cameras, acoustic sensors, and command and control software into one operating system. This shift is prompted as modern drone threats are no longer limited to simple commercial drones, buyers now need real time detection tracking, faster classification, lower false alarms, and better situational awareness against FPV drones, loitering munitions, and coordinated UAS systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Small-Drone and FPV Threats Drive Demand for Integrated Counter-UAS Sensor Fusion

A major driver for the global counter-UAS sensor fusion market growth is the rapid operational spread of small commercial drones, FPV drones, loitering munitions, and low-cost UAS systems across battlefields, borders, airports, and critical infrastructure. These drone threats are difficult to manage with one sensor alone as radar can struggle with clutter, RF sensors may miss autonomous or pre-programmed drones, EO/IR needs cueing, and acoustic sensors have range and noise limits. This is pushing buyers toward integrated counter drone system architectures that combine sensor data, drone detection, detection tracking, command and control, machine learning, and AI driven classification into a real time operating picture. Resulting market being pulled by a need of faster situational awareness and lower false alarms before the threat reaches the protected site.

MARKET RESTRAINTS

Regulatory Limits on Drone Mitigation Restrain Wider Civil-Sector Market Growth

Major restraint for the global market is the limited legal authority to move from drone detection to active mitigation, especially in airports, cities, public venues, and critical infrastructure. Many buyers can deploy RF sensors, acoustic sensors, radar, EO/IR, sensor data platforms, and command and control tools for situational awareness, but they sometimes cannot lawfully jam, spoof, intercept, or neutralize UAS systems without government approval. As a result, regulatory uncertainty limits procurement speed, particularly for civil aviation, private infrastructure, and local-security users.

MARKET OPPORTUNITIES

Critical Infrastructure Protection Creates New Growth Opportunities for Sensor-Fusion-Based Counter-UAS Systems

A key opportunity in the market is the expansion of demand beyond military bases into airports, ports, power plants, telecom networks, oil & gas sites, industrial facilities, and public-security environments. These locations need more than basic drone detection as drone threats can appear in busy urban or industrial airspace, where one sensor alone is not reliable enough. This creates room for counter drone system providers that can combine RF sensors, radar, EO/IR, acoustic sensors, sensor data analytics, command and control, and machine learning into a real time situational awareness layer.

MARKET CHALLENGES

Sensor Interoperability and False-Alarm Complexity Challenge Market Adoption

A key challenge in the market is to build a reliable fusion of various sensors, effectors, and command and control layers for operating in cluttered environments. A counter drone system comprises radar, RF sensors, EO/IR cameras, acoustic sensors, machine learning models, and sensor data feeds, however, each of these layers has limitations. Birds, aircraft, weather, terrain, urban noise, electronic interference, and friendly UAS systems can create false alarms or incomplete detection and tracking, challenging the market growth.

Impact of Russia-Ukraine and Middle East Conflicts

Russia-Ukraine War, Middle East Conflicts, and Ongoing Drone Warfare Drive Demand for Sensor-Fusion-Led Counter-UAS Systems

The Russia-Ukraine war, Middle East conflicts, Red Sea-linked security risks, and African conflict zones are accelerating demand for counter-UAS sensor fusion as drone threats are now appearing in higher volume, lower cost, and more complex forms. FPV drones, loitering munitions, one-way attack drones, and swarm-style UAS systems are forcing militaries and security agencies to move beyond standalone drone detection tools. Buyers now need a counter drone system that can fuse sensor data from radar, RF sensors, EO/IR cameras, acoustic sensors, and command and control platforms to deliver real time situational awareness, detection tracking, and faster threat classification. This conflict-driven demand is especially strong around military bases, air-defense sites, borders, airports, ports, oil & gas assets, and critical infrastructure, where delayed detection or false alarms can quickly become operational failures.

- In October 2025, European defense ministers agreed to move forward with a joint “drone wall” project to protect EU airspace after rising drone violations along borders linked to Russia and Ukraine.

- In May 2026, the AP News reported that a drone strike caused a fire at the UAE’s Barakah nuclear power plant perimeter, while two additional drones were intercepted.

- In May 2026, the AP also reported that drones had become the leading cause of conflict-related civilian deaths in Sudan in early 2026, with more than 880 civilian deaths from drone attacks between January and April.

Segmentation Analysis

By Component

Due to Real-Time Threat Classification and Multi-Sensor Correlation, Software & Analytics Dominated the Component Segment

In terms of component, the market is categorized into software & analytics, edge processing hardware, middleware & sensor integration, command & control layer, and services.

Software & analytics held the largest global counter-UAS sensor fusion market share in 2025, as the core value of such sensor fusion is shifting from hardware ownership to how quickly the system can interpret sensor data and support decision-making. Radar, RF sensors, EO/IR cameras, acoustic sensors, and other inputs generate large volumes of fragmented data, but software converts those feeds into drone detection, detection tracking, threat classification, and operator-ready situational awareness.

The middleware & sensor integration segment is expected to grow at the highest CAGR of 23.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sensor Type Integrated

Due to Higher Detection Confidence across Complex Drone Threats, Multi-Sensor Fusion Segment Dominated in the Market

On the basis of sensor type integrated, the market is classified into radar-based fusion, RF detection-based fusion, EO/IR-based fusion, acoustic-based fusion, and multi-sensor fusion.

The multi-sensor fusion segment held the largest global market size in 2025, as single sensors are not-reliable enough against today’s drone threats. Radar provides wider-area detection, RF sensors help identify control or telemetry signals, EO/IR supports visual confirmation, and acoustic sensors can add another detection layer in selected environments. The multi-sensors inputs are fused into one counter drone system that improves drone detection, detection tracking, classification, and real time situational awareness. As a result, military, airport, border, and critical-infrastructure users are moving toward systems that combine sensor data from multiple sources rather than depending on radar-only or RF-only architectures.

The radar-based fusion segment is expected to show the second-fastest growth, registering a CAGR of 19.4% over the forecast period.

By Fusion Architecture

Due to Command-Led Military and Critical-Site Protection Needs, Centralized Command-Center Fusion Dominates Segment

The market is further divided by fusion architecture into AI/ML-enabled fusion, edge-based fusion, open-architecture modular fusion, centralized command-center fusion, and rule-based fusion.

Centralized command-center fusion dominated the fusion architecture segment in 2025, as most large counter-UAS deployments still begin with fixed-site military bases, airports, ports, government facilities, oil & gas assets, and national-security sites. While AI driven, edge-based, and machine learning-enabled architectures are growing faster, centralized fusion remains the dominating segment as procurement is still heavily tied to control rooms, base-defense centers, air-defense nodes, and security operations centers that require real time situational awareness and coordinated response against drone threats.

The AI/ML-enabled fusion segment is expected to show the fastest growth, registering a CAGR of 25.8% over the forecast period.

By Deployment Mode

Due to High-Value Site Protection Requirements, Fixed-Site Dominated the Deployment Mode Segment

On the basis of deployment mode, the market is classified into fixed-site, mobile / vehicle-mounted, man-portable, naval / shipborne, and enterprise / regional overlays.

Fixed-site dominated the deployment mode segment in 2025, as most counter-UAS sensor fusion spending is still concentrated around permanent, high-value locations. Such locations include military bases, airports, ports, oil & gas facilities, government sites, nuclear plants, prisons, and critical infrastructure. These sites need continuous drone detection, detection tracking, and real time situational awareness rather than temporary or patrol-based coverage, resulting in segment dominance.

The enterprise / regional overlays segment is expected to witness fastest growth, registering a CAGR of 25.5% over the forecast period.

By Application

Due to High-Value Defense-Site Exposure, Military Base Protection Dominated the Application Segment

The market is further divided by application into military base protection, battlefield / tactical force protection, critical infrastructure, airport & civil aviation security, border & homeland security, and others.

The military base protection segment held the largest market share in 2025, as in military bases counter-UAS sensor fusion becomes operationally necessary and budget-justified. Air bases, forward operating bases, naval facilities, ammunition depots, radar sites, command posts, and logistics hubs face persistent drone threats from small commercial drones, FPV drones, loitering munitions, and hostile UAS systems. These sites need continuous drone detection, detection tracking, real time situational awareness, and command and control workflows that can fuse sensor data from radar, RF sensors, EO/IR cameras, acoustic sensors, and other layers into one counter drone system.

The battlefield / tactical force protection segment is expected to witness fastest market growth, registering a CAGR of 24.0% over the forecast period.

By Threat Type

Due to High Encounter Frequency across Civil and Defense Sites, Small Commercial Drones Dominated in the Market

The market is further divided by threat type into small commercial drones, FPV drones, loitering munitions, and drone swarms.

Small commercial drones dominated the threat type segment in 2025, as they are the most widely encountered drone threats across airports, military bases, prisons, borders, public events, ports, and critical infrastructure. Unlike loitering munitions or drone swarms, small commercial drones are inexpensive, easy to modify, widely available, and difficult to distinguish from legitimate UAS systems in crowded low-altitude airspace. This creates constant demand for drone detection, detection tracking, real time situational awareness, and command and control workflows that can fuse sensor data from radar, RF sensors, EO/IR cameras, and acoustic sensors.

In September 2025, Le Monde reported that more than 2,000 drone-related incidents are reported annually near sensitive sites in France, and that Paris airport operator Groupe ADP, through Hologarde, had deployed systems integrating optical, radar, radio technologies, and artificial intelligence at major airports such as Roissy-Charles-de-Gaulle and Orly.

Drone swarms segment is expected to show the fastest market growth, registering a CAGR of 27.5% over the forecast period.

By End User

Due to Persistent Base, Air-Defense, and Tactical Protection Needs, Military & Defense Dominates Market

Based on end user, the market is segmented military & defense, homeland security & law enforcement, critical infrastructure operators, and airport & aviation authorities.

Military & defense dominated the end user segment in 2025, as defense forces are the earliest and consistent buyers of counter-UAS sensor fusion. Military users face drone threats around air bases, forward operating bases, naval facilities, ammunition depots, radar sites, command posts, border areas, and deployed formations, where delayed drone detection can create immediate operational risk. The segment leads as defense buyers have clearer authority, larger procurement budgets, and stronger need for detection tracking, threat classification, and coordinated response than most civil end users.

The homeland security & law enforcement segment is expected to witness fastest market growth, registering a CAGR of 22.6% over the forecast period.

Counter-UAS Sensor Fusion Market Regional Outlook

Due to Strong U.S. Defense Procurement and Integrated C-UAS Modernization, North America Dominates the Regional Segment

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Counter-UAS Sensor Fusion Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest market share for counter-UAS sensor fusion solutions in 2025, and is anticipated to grow at a CAGR of 16.9% during the forecast period. The region dominates as the U.S. benefits from the strongest defense budgets, military-base protection needs, homeland-security requirements, border surveillance demand, and advanced counter-UAS technology suppliers. The region is moving quickly from standalone drone detection toward integrated counter drone system architectures that connect radar, RF sensors, EO/IR, acoustic sensors, autonomous interceptor drones, sensor data platforms, and command and control software. This gives North America a clear lead in real time situational awareness, detection tracking, machine learning-enabled classification, and AI driven response coordination against evolving drone threats.

U.S. Counter-UAS Sensor Fusion Market

Based on the strong contribution of North America to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 390.5 million in 2025, growing at a CAGR of 16.4% over the forecast period.

Europe

The European market is anticipated to grow at a fastest pace, registering a CAGR of 21.9% during the forecast period. Europe is becoming one of the most strategically important regions for the market, mainly as the Russia-Ukraine war has pushed drone threats into mainstream defense planning. The region is no longer treating drone detection as a niche border-security tool, it is moving toward networked systems that combine RF sensors, radar, EO/IR, acoustic sensors, sensor data, and command and control layers for real time situational awareness.

France Counter-UAS Sensor Fusion Market

The France market value reached approximately USD 57.1 million in 2025, anticipated to grow at the CAGR of 16.9% during the forecast period.

Germany Counter-UAS Sensor Fusion Market

The Germany market size reached approximately USD 61.3 million in 2025, anticipated to grow at the CAGR of 23.2% during the forecast period.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 20.6% over the forecast period. The Asia Pacific region is growing as drone threats are tied to border tensions, island defense, maritime security, air-base protection, and critical infrastructure security. China, India, Japan, South Korea, and Australia are all strengthening low-altitude surveillance and air-defense readiness, but the region is fragmented in procurement, increasing the need for open sensor-fusion platforms. Japan’s 2025 defense budget included funding for missile defense and a mobile radar system on Okinawa, while Australia purchased a USD 5.00 million laser-based anti-drone system. This shows that regional buyers are moving beyond basic drone detection toward integrated counter drone system capabilities.

China Counter-UAS Sensor Fusion Market

The China market size in 2025 stood at around USD 73.1 million, anticipated to grow at the CAGR of 19.0% during the forecast period.

South Korea Counter-UAS Sensor Fusion Market

The South Korean market value stood at around USD 22.0 million in 2025, accounting for roughly 10.69% of Asia Pacific revenues.

Rest of the World

The Rest of the World region, which includes the Middle East & Africa and Latin America, holds a comparatively smaller market share but is expected to grow at a CAGR of 17.9% during the forecast period. The Middle East & Africa market accounts for most of the demand due to military-base protection, oil & gas assets, ports, airports, border security, and active drone use in conflict zones. Latin America’s demand is more gradual, led by airports, prisons, ports, border agencies, public-security sites, and critical infrastructure operators. The AP News reported that drones caused more than 880 civilian deaths between January and April 2026 and became the leading cause of conflict-related civilian fatalities in Sudan. This type of conflict pressure supports broader adoption of AI driven sensor fusion, acoustic sensors, RF sensors, command and control workflows, and real time situational awareness systems across high-risk security environments.

Latin America Counter-UAS Sensor Fusion Market

The market in Latin America reached around USD 34.7 million in 2025 and is anticipated to grow at a CAGR of 14.5% during the forecast period.

Middle East & Africa Counter-UAS Sensor Fusion Market

The Middle East & Africa market stood at around USD 115.1 million in 2025 and is expected to reach USD 549.0 million in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players Focus on AI-Enabled Sensor Fusion, Integrated C2, and Layered Counter-UAS Architectures

The global counter-UAS sensor fusion market is shifting from standalone drone detection hardware toward integrated platforms built around sensor data, command and control, real time detection tracking, and coordinated response. Key players include Anduril Industries, Dedrone by Axon, DroneShield, Thales, Leonardo, HENSOLDT, Rafael Advanced Defense Systems, Elbit Systems, D-Fend Solutions, Sentrycs, MARSS, QinetiQ, Rheinmetall, and Northrop Grumman.

The strongest players are competing on multi-sensor integration, AI-enabled classification, and open system architecture. Their platforms combine radar, rf sensors, EO/IR, acoustic sensors, electronic warfare, autonomous interceptor drones, and software analytics into a single counter drone system.

LIST OF KEY COUNTER-UAS SENSOR FUSION COMPANIES PROFILED

- Anduril Industries, Inc. (U.S.)

- Axon Enterprise, Inc. (U.S.)

- DroneShield Limited (Australia)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- HENSOLDT AG (Germany)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- D-Fend Solutions Ltd. (Israel)

- Sentrycs Ltd. (Israel)

- MARSS Group (U.K.)

- QinetiQ Group plc (U.K.)

- Rheinmetall AG (Germany)

- Northrop Grumman Corporation (U.S.)

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The U.S. Army signed an USD 87.00 million agreement with Anduril Industries to deploy Lattice as a common counter-drone command-and-control software backbone. The system links sensors, interceptors, and operators for distributed drone detection, tracking, classification, and engagement.

- December 2025: AeroVironment received an USD 874.26 million U.S. Army IDIQ contract for foreign military sales of drone and counter-drone systems, including Titan C-UAS, training, spares, and logistics support for allied and partner forces.

- October 2025: The U.S. Army selected AeroVironment for a USD 96.00 million initial contract to develop the Freedom Eagle-1 next-generation counter-drone missile, strengthening the kinetic interceptor layer of counter-UAS systems.

- August 2025: Australia awarded an initial USD 11.10 million equivalent package under Project LAND 156 to 11 vendors for counter-drone technologies, including threat detectors and drone-defeat systems, and DroneShield received about USD 3.30 million for handheld detection and RF-jamming devices.

- May 2025: AeroVironment completed its acquisition of BlueHalo in an all-stock transaction valued at approximately USD 4.10 billion, adding directed-energy, space, cyber, and counter-UAS technologies to AeroVironment’s portfolio.

- October 2024: The U.S. Department of Defense procured more than 500 Anduril Roadrunner-M interceptors and Pulsar electronic-warfare systems under a nearly USD 250.00 million counter-drone contract.

- January 2024: RTX/Raytheon received a USD 75.00 million U.S. Army contract to produce 600 Coyote 2C interceptors for counter-UAS missions, supporting the Army’s layered defense architecture against small drones.

- March 2022: France awarded the PARADE anti-drone contract to Thales and CS Group/Sopra Steria, valued at around USD 378.00 million over 11 years, with about USD 35.60 million firm at award stage and the system supports modular deployable protection for sensitive sites and major events.

REPORT COVERAGE

The global counter-UAS sensor fusion market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.5% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Component

|

|

By Sensor Type Integrated

|

|

|

By Fusion Architecture

|

|

|

By Deployment Mode

|

|

|

By Application

|

|

|

By Threat Type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1,395.3 million in 2026 and is projected to reach USD 5,790.0 million by 2034.

In 2025, the market value stood at USD 427.9 million.

The market is expected to exhibit a CAGR of 19.5% during the forecast period.

The software & analytics segment led the market by component.

Rising small-drone and FPV threats drive demand for integrated counter-UAS sensor fusion are the key factors driving the market.

Key players in the market include Anduril Industries, Inc., Axon Enterprise, Inc., DroneShield Limited, Thales S.A., Leonardo S.p.A., HENSOLDT AG, Rafael Advanced Defense Systems Ltd., Elbit Systems Ltd., D-Fend Solutions Ltd., Sentrycs Ltd., MARSS Group, QinetiQ Group plc, Rheinmetall AG, and Northrop Grumman Corporation.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us