Demand Side Platform Market Size, Share & COVID-19 Impact Analysis, By Type (Self Service and Full/Managed Service), By Channel (Display, Mobile, Video, and Native), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

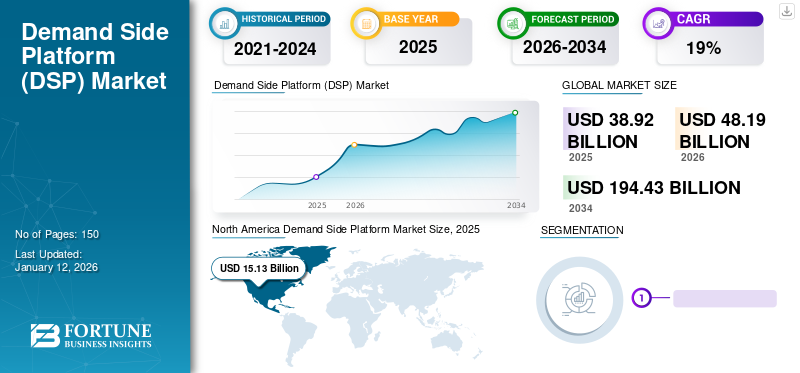

The global demand side platform market size was valued at USD 38.92 billion in 2025 and is projected to grow from USD 48.19 billion in 2026 to USD 194.43 billion by 2034, exhibiting a CAGR of 19% during the forecast period. North America dominated the global market with a share of 38.9% in 2025. Additionally, the U.S. demand side platform market is predicted to grow significantly, reaching an estimated value of USD 46,929.9 million by 2032.

In the scope, we have considered demand side solutions provided by key players such as Amazon.com, Inc., Adobe Inc., the Trade Desk Inc., MediaMath Inc., and SmartyAds, among others.

Demand Side Platform (DSP) is a software that allows advertisers to buy/purchase advertising space for advertising portfolio. Agencies use this platform to buy ad portfolio through an instantaneous bidding system and ad exchange. These platforms are used for advertising inventory over various channels such as display, mobile, video, and native. The rising demand and popularity for programmatic advertising among advertisers is driving the market. Programmatic advertising includes DSPs and Supply-Side Platforms (SSPs).

For instance, in August 2022, Google added three features for advertising on Connected TV (CTV) and to measure the right audience. It added Nielsen Digital Ad Ratings for audience guarantees, advanced programmatic guarantee, and consolidated CTV workflow across YouTube and other CTV apps. These additions aided advertisers in planning, managing, and measuring performance across channels.

Download Free sample to learn more about this report.

DEMAND SIDE PLATFORM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 38.92 billion

- 2026 Market Size: USD 48.19 billion

- 2034 Forecast Market Size: USD 194.43 billion

- CAGR: 19.00% from 2026-2034

- North America represented 38.9% of the global market in 2025.

- The video segment accounted for 38.6% of the market in 2026, driven by the growing adoption of CTV advertising.

- The full/managed service segment represented 53.58% of the market in 2026.

North America

North America represented 38.90% of the global market in 2025.

Europe

Europe accounted for 26.50% of the global market share in 2025.

Asia Pacific

Asia Pacific accounted for 21.40% of the global market in 2025.

U.S.

The U.S. market is expected to reach USD 13.73 billion by 2026.

Japan

The Japan market is projected to reach USD 1.88 billion by 2026.

Read More

COVID-19 IMPACT

Industries Shifting to Digital Solutions and E-commerce Amid Pandemic to Boost Market Opportunity

The pandemic curtailed the movement of goods, services, and people worldwide and significantly impacted economic activity and financial markets. As a result, shifting the workforce to a remote working environment created oversight challenges.

However, in the early 2020s, at the start of the pandemic, demand side platform providers faced slight challenges. Eventually, lockdowns seemed to be an opportunity for greater reach of the audience as people inclined toward online shopping and social media the most for their daily needs. Companies have seen a rise in ad spending by advertisers.

The market witnessed growth throughout the pandemic owing to the exponential rise in e-commerce, online shopping, and the gaming sectors. A report by the Entertainment Software Association (ESA) found that 55% of video game players in the U.S. played more games during the COVID-19 pandemic. This formed a significant opportunity for advertisers.

LATEST TRENDS

Download Free sample to learn more about this report.

Increasing Mobile Gaming and Video Ads to Surge Product Demand

Video medium is the most widespread media type for high-impact display ads. Marketers are implementing automated video ad buying in demand side platforms for distributing digital video commercials. This helps educate the audience, increases engagement on digital and social channels, and enables customer reach with a new medium.

Moreover, home entertainment and mobile gaming in all forms are creating an unprecedented opportunity for demand side platform providers who intend on reaching newly captive audiences. Marketers utilize demand side platforms for gaming ad networks. The mobile gaming landscape has transformed into an opportunity for advertisers to focus on digital ad spending.

For instance, in April 2022, Tyroo, an ad tech platform, launched a gaming vertical, Comet, in Asia Pacific. With Comet, Tyroo can offer advertising opportunities in the vast metaverse while providing customer-centric experiences to the brands. Furthermore, the solution aids brands in shaping their ad campaigns and enhancing their customer experiences.

DRIVING FACTORS

Rising Number of Ad Transactions through Connected TV (CTV) and OTT Platforms to Boost Market Growth

Advertisement inventories implementing new strategies, such as target audience reach and device marketing, platforms, including CTV and OTT, play a vital role in their approach. They aid in better customer reach and target audience. CTV display advertising is on the hype due to the rapid increase in video streaming through OTT platforms such as YouTube TV, Apple TV+, and Netflix. For example, the U.S. streaming revenue increased by 22.8% in 2021.

Demand side platforms facilitate businesses in promoting their brand mentions through such channels and increase avenues alongside complete control of their ad campaigns. Further, video is a highly engaging and personal ad format, which enables advertisers to reach their marketing goals efficiently.

For instance, in May 2022, Google LLC added new features to the Google Marketing Platform, Display & Video 360. To improve CTV advertising, the company expanded its CTV inventory in the Display & Video 360 demand-side platform and extended Google audiences to CTV devices.

RESTRAINING FACTORS

Growing Fraudulent Practices across the Advertising Industry Might Hinder Market Growth

Fraudulent advertising is increasingly emerging as a new risk to consumers shopping online. Consumers are exposed to millions of fraudulent advertisements, directing them to illegal e-commerce websites that defraud and provide counterfeit products and deceitful services. Ad frauds may occur in many forms, including fake ad impressions/clicks by bad bots, piling ads on top of one another, and fake ghost sites that duplicate real websites to get permitted by ad networks. A 2019 China Internet Network Information Center report stated that China's digital ad fraud rate rose as high as 40% over the last few years. China accounted for 30.7% of the total advertising spend, and the U.K. ad fraud accounted for just 2.4% during the same period in the U.K.

Moreover, many fraud adverts are using social media as a platform to practice such deceits. For instance, a report by tracit.org 2020-21 stated facts and use cases related to fraudulent practices.

By using Google's video platform YouTube, fraudsters exploited the popularity of certain popular video games by tricking consumers into downloading risky apps. Also, on YouTube, scammers used COVID-19 to profit through easy-to-find videos advertising overpriced face masks and mock vaccines, costing consumers more than USD 5 million. In April 2019, an advert for fake Tommy Hilfiger apparel was identified on LinkedIn.

SEGMENTATION

By Type Analysis

Complete Control over Ad Campaigns and Ad Buying Process to Increase Self Service DSP Demand

Based on type, the market is bifurcated into self service and full/managed service.

The Full/managed service segment led the market accounting for 53.58% market share in 2026 owing to its diverse advertising solution offerings and growing popularity among advertisers. In full/managed service DSP, a third-party, such as an agency, runs and manages the entire campaign to target an accurate audience with the help of their media strategist's team.

However, the self service segment is expected to hold the highest CAGR during the forecast period, giving advertisers complete control over their ad campaigns. Marketers can have full control over the ad buying process, selecting inventory, and running campaign management with the help of their marketing team. Self service demand-side platforms are efficient marketing tools that enable advertisers to buy high-quality impressions at scale with minimal friction. This factor is likely to drive the demand side platform market growth.

By Channel Analysis

To know how our report can help streamline your business, Speak to Analyst

Extensive Rise in Number of Smartphone Users and Social Media to Propel Segmental Growth

Based on channel, the market is categorized into display, mobile, video, and native.

The video segment dominated the market accounting for 38.6% market share in 2026, owing to the rising adoption of CTV advertising for mass reach to customers. Advertisers can achieve their target by leveraging video advertising to influence awareness tactics, brand perception, and reach new customers. Further, COVID-19 has shifted viewers from linear to CTV and Over-the-Top (OTT) platforms, with more individuals staying home. This has increased the demand for demand side platforms. According to EMI Research Solutions, in 2020, monthly OTT subscription service users in Latin America rose to 117.2 million.

Mobile advertising is expected to grow at the highest CAGR in the forecast period owing to increasing number of internet and smartphone users. In addition, social media and mobile gaming have gained advertisers' attention for publishing ads. For instance, according to Sensor Tower, mobile gaming revenue accounted for USD 36 billion in 2021.

REGIONAL INSIGHTS

North America Demand Side Platform Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Geographically, the market is divided into five key regions such as North America, South America, Europe, the Middle East & Africa, and Asia Pacific. They are further categorized into countries.

North America

North America accounted for USD 15.13 billion in 2025, representing 38.90% of the global market share, and is projected to reach USD 18.55 billion in 2026. North America is expected to hold the maximum revenue share during the forecast period. The region's market growth is driven by rising programmatic ad spend. According to eMarketer, approximately 85% of expenditure on digital display advertising in the U.S. was done through programmatic technology in 2020. Also, market players are significantly focusing on adopting new technologies in their demand-side platform software. The region is incorporating prominent businesses across all industries and extensively implementing the software. Further, multiple well-established and small regional advertisers are leveraging these platforms for short-term performance campaigns and brand-building campaigns. The U.S. market is projected to reach USD 13.73 billion by 2026.

Asia Pacific

In 2025, Asia Pacific held 21.40% of the global market, reaching a valuation of USD 8.33 billion, and is projected to grow to USD 10.43 billion in 2026. Market players in the region focus on expanding their geographical presence by offering advanced demand side platforms across developing nations. The market is driven by extensive smartphone penetration in the region. Also, the adoption of advertising approaches, such as device marketing and programmatic advertising, is likely to fuel regional growth in the long term. The Japan market is projected to reach USD 1.88 billion by 2026, the China market is projected to reach USD 3.43 billion by 2026, and the India market is projected to reach USD 1.59 billion by 2026.

Europe

The Europe market was valued at USD 10.32 billion in 2025, capturing 26.50% of global revenue, and is estimated to reach USD 12.86 billion in 2026. Europe is expected to hold a prominent demand side platform market share. The growth is owing to the growing popularity of DSP software among advertisers in France, Germany, and the U.K. According to Zenith forecast, Central & Eastern Europe (C&E Europe) is anticipated to showcase significant growth between 2021 and 2024 for programmatic ad spend. The UK market is projected to reach USD 2.96 billion by 2026, while the Germany market is projected to reach USD 2.53 billion by 2026.

Similarly, the rising digitalization and industrialization in South America may drive market growth. The Middle East & Africa region is projected to gain stable growth owing to significant investment in solutions by major players.

To know how our report can help streamline your business, Speak to Analyst

For instance, in 2021, Amazon.com, Inc. launched Amazon DSP in Saudi Arabia to enable advertisers and agencies to reach their target audience. It is a self-service DSP that works for both Amazon-owned and off-Amazon parties. Moreover, it facilitates direct publisher relationships.

Middle East & Africa

Middle East & Africa contributed approximately USD 2.97 billion to the global market in 2025, accounting for 7.60% share, and is expected to reach USD 3.69 billion in 2026.

Latin America

The Latin America region captured 5.60% of the global market in 2025, generating USD 2.17 billion in revenue, and is projected to reach USD 2.67 billion in 2026.

KEY INDUSTRY PLAYERS

Strategic Collaborations and Partnerships to Boost Market Expansion of Key Players

Key players are trying to boost their operations and scale sales through partnerships and collaborations. This enables brands to expand their product offerings and customer base.

May 2022: Adform expanded its long-standing partnership with DoubleVerify (DV), a digital media analytics and measurement provider. The partnership enabled advertisers to guard their programmatic campaigns and ensure the media quality in new ways, including connected TV advertising.

March 2022: The Trade Desk integrated with Adobe Real-Time Customer Data Platform, aiding marketers to drive more clarity in their advertising by activating first-party data without depending on third-party cookies. The email-based initiation will be available on all media channels of the Trade Desk, including connected TV (CTV).

List of Key Companies Profiled:

- Alphabet Inc. (U.S.)

- Amazon.com, Inc. (U.S.)

- Adobe Inc. (U.S.)

- The TradeDesk, Inc. (U.S.)

- MediaMath Inc. (U.S.)

- Adform (Denmark)

- Xandr (Microsoft) (U.S.)

- SmartyAds (U.S.)

- Gourmet Ads (Australia)

- Basis Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- January 2023: The Trade Desk introduced Galileo, a novel method for advertiser first-party data activation. The method plays a vital role to secure their customers’ important data safely. Advertisers use this data to enhance mobile and display buys across the globe.

- June 2022: Basis Technologies released Data Canvas, a data visualization solution, to automate reporting in advertising. Data Canvas helps enterprises available in the Basis media automation platform, by decreasing human tasks in constructing and sharing client reports and dashboards.

- July 2022: SmartyAds partnered with SQUID, a news feed company. Through this collaboration, SmartyAds allows advertisers to expand their reach and address audiences, including the tech-savvy youth. SQUID helps SmartyAds in offering news in local languages and broadcasting it through various digital channels.

- April 2022: Xandr launched deal discovery, inventory library, and activation platform for Invest DSP. With this launch, Xandr enabled the easy discovery of premium inventory to buyers, creating a footprint in the programmatic advertising industry. Moreover, buyers can access publishers across multiple Supply-Side Platforms (SSPs).

- May 2022: Adform expanded its long-standing partnership with DoubleVerify (DV), a digital media analytics and measurement provider. The partnership enabled advertisers to guard their programmatic campaigns and ensure media quality in new ways, including connected TV advertising.

- February 2022: The Trade Desk Inc. launched OpenPath to connect advertisers and marketers with premium publishers. OpenPath allows publishers to integrate with their demand side platform directly accessible to premium publishers.

REPORT COVERAGE

The global market research report highlights leading regions across the world to offer a better understanding of the market. Furthermore, the report provides insights into the latest industry and market trends and analyzes technologies deployed at a rapid pace at the global level. It further highlights major growth-stimulating factors and restraints, helping the reader gain an in-depth knowledge about the market.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 19% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Channel, and Region |

|

By Type |

|

|

By Channel |

|

|

By Region |

|

Frequently Asked Questions

The market is projected to reach USD 194.43 billion by 2034.

In 2025, the market stood at USD 38.92 billion.

The market is projected to grow at a CAGR of 19% over the forecast period (2026-2034).

Video segment is likely to lead the market owing to the rising adoption of connected TV advertising for mass reach.

Rising ad transaction through connected TV and OTT platforms is the key factor boosting the market growth.

Alphabet Inc., Amazon.com, Inc., Adobe Inc., The Trade Desk, Inc., MediaMath Inc., Adform, Xandr (Microsoft), SmartyAds, Gourmet Ads, and Basis Technologies are the top players in the market.

North America is expected to hold the highest market share.

Asia Pacific is expected to grow with the highest CAGR.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us