Digital Twin in Marine Market Size, Share & Industry Analysis, By Solution (Hardware, Software, & Services), By Vessel Type (Single Vessel Twin, Class-of-Ship Twin, Fleet Twin, & Voyage Twin), By Port Level (Single Berth Twin, Terminal Twin, Port-Wide Twin, & Others), By Marine Subsystem (Hull/Structure, Propulsion System, & Others), By Modeling Type (Physics-Based Twin, Data-Driven Twin, Hybrid Twin, & Others), By Integration Mode (Onboard Only, Shore-Based Only, & Others), By Deployment Mode (Newbuild Embedded & Retrofit Twin), By Application, By End User, and Regional Forecast, 2026-2034

Digital Twin in Marine Market Size & Future Outlook

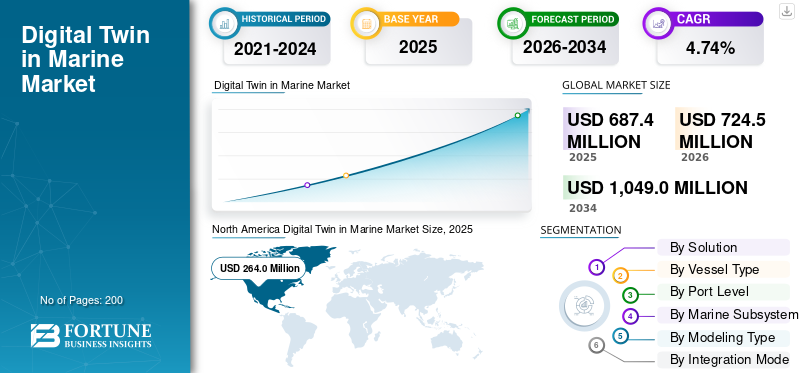

The global digital twin in marine market size was valued at USD 687.4 million in 2025. The market is projected to grow from USD 724.5 million in 2026 to USD 1,049.0 million by 2034, exhibiting a CAGR of 4.74% during the forecast period. North America dominated the digital twin in marine market with a market share of 38.40% in 2025.

The application of digital twin in marine market refers to software, simulation, analytics, and services that create a live virtual representation of a ship, subsystem, shipyard process, or offshore/marine asset by combining engineering models with sensor and operational real-time data in the physical and digital world. It is used across the vessel lifecycle, design, construction, condition monitoring, voyage optimization, maintenance, and class/compliance support. In simple terms, this market is about turning ships and marine assets into continuously monitored, data-driven systems rather than assets managed only through periodic inspection by implementing digital twin technology.

The market is being driven by increasing shipping, which is under growing pressure to cut fuel use and emissions, and the IMO’s 2023 GHG strategy sets explicit 2030 and 2040 reduction checkpoints, which push owners toward tools that improve operational efficiency and support decarburization. Moreover, operators want less unplanned downtime, so digital twins’ technology is being adopted for predictive and preventive maintenance using live sensor data. In addition, shipowners and yards want better lifecycle visibility, linking design data, onboard operations, and shore-based decision-making in one environment drives the global market growth rapidly.

Among the major players, DNV, ABS, Wärtsilä, Kongsberg Maritime, and Siemens stand out. The major entities are focusing on a strategy to strengthen lifecycle digital twinning and industry collaboration, including work on open simulation platforms and twin-based testing. Moreover, the market is pushing growth through verification frameworks, partnerships such as Akselos, and its EagleTwin life-cycle tool, tying digital twins to AI-led fleet optimization and vessel efficiency, an integrated vessel-fleet-shore digital ecosystem, embedding digital twin capability across ship design, ship construction, and shipbuilding digitalization, including collaboration with key players, anticipate the global market growth.

Download Free sample to learn more about this report.

Digital Twin In Marine Market Key Takeaways

- 2025 Market Size: USD 687.4 million

- 2026 Market Size: USD 724.5 million

- 2034 Forecast Market Size: USD 1,049.0 million

- CAGR: 4.74% from 2026–2034

- North America dominated the digital twin in marine market with a 38.40% share in 2025.

- The software segment accounted for the largest market share of 40.95% in 2025.

- The naval/coast guard/government marine segment held the largest share of 40.93% in 2025.

North America

North America led the market with a value of USD 264.0 million in 2025 and is projected to reach USD 276.7 million in 2026.

Europe

Europe is expected to register the fastest regional growth, expanding at a CAGR of 5.17% during the forecast period.

Asia Pacific

Asia Pacific was the second-largest regional market, valued at USD 183.7 million in 2025.

U.S.

The market reached USD 246.02 million in 2025 and is projected to grow at a CAGR of 3.78% through the forecast period.

Japan

The market was valued at USD 30.77 million in 2025 and is expected to grow at a CAGR of 5.71% during the forecast period.

Read More

Digital Twin in Marine Market Trends

Market is Moving toward AI-Enabled, Cloud-Based, Continuously Updated Twins Rather than Static 3D Models

The clearest market trend is the shift from digital twin as a model to digital twin as a live decision engine. Wartsila’s 2025 material makes this explicit: digital twins are now being linked with AI, sensor streams, auto-logged data, and automated twin creation to support fuel savings, better voyage planning, and lower operating overhead. That means the product direction is moving toward faster model refresh, better prediction accuracy, and easier use by shore teams, not just naval architects or technical specialists. In business terms, the market is trending toward more practical, subscription-like tools that support everyday operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Decarburization, Fuel Efficiency, and Lifecycle Cost Control are Turning Digital Twins into a Core Operating Tool, Driving Market Growth

The shipping industry’s need to run vessels more efficiently under tighter environmental and cost pressure is driving the digital twin in marine market growth. IMO’s approved net-zero measures add direct commercial pressure on shipowners to improve fuel performance, emissions control, and reporting quality, especially for large ocean-going ships. That makes digital twins more valuable, as they connect design, sensor, and operating data into a single model that supports daily technical and commercial decisions. DNV also notes that digital twin systems help reduce costs, improve safety, and manage operational risk, which matters in a market where hidden information costs and unscheduled downtime can materially damage profitability.

For instance, in April 2025, IMO said its new net-zero regulations would include a fuel standard and a global emissions pricing mechanism for ships over 5,000 gross tonnage, sharply increasing the value of digital efficiency and compliance tools.

MARKET RESTRAINTS

Legacy Fleets, Siloed Data, and Weak Digital Foundations Still Slow Large-Scale Adoption, Hampering Market Growth

The market’s biggest restraint is that many vessels and shipyards still lack the clean, connected data environment that a robust digital twin requires. Kongsberg states that while leading owners and newbuild programs are using high-frequency data and advanced analytics, much of the global fleet still depends on digital noon reports and manual processes. DNV makes a similar point in a more structured way: successful maritime digitalization depends on IT integration, connectivity, data sharing, standardization, and internal capability building. In plain business terms, many owners want the outcome of a digital twin before they have built the data backbone required to make the twin reliable.

For instance, in February 2026, Siemens said HD Hyundai selected Siemens Xcelerator to create a single data flow across shipbuilding, as long-standing discontinuities between design and production were still creating inefficiencies and errors.

MARKET OPPORTUNITIES

Market Is Expanding from Ship Monitoring into Offshore Integrity, Digital Shipyards, Ports, and New Service Models

The strongest opportunity is that enabled digital twins are no longer limited to basic vessel performance dashboards. ABS has expanded the concept into offshore structural lifecycle management through EagleTwin, a web-based structural digital twin for FPSO, FLNG, and FSRU assets. At the same time, its AMOG collaboration pushes the model further into moorings, risers, and subsea cables. This broadens the addressable market from ships alone to offshore marine infrastructure, where integrity, class support, inspection planning, and downtime avoidance carry very high economic value. That makes digital twin spending easier to justify, as it can support compliance, maintenance, safety, and asset life extension in a single platform.

For instance, in January 2026, ABS and AMOG signed an MoU to develop an Offshore Mooring Digital Twin, demonstrating how quickly digital twin applications are spreading into higher-value applications in marine integrity and offshore asset management.

MARKET CHALLENGES

Cyber Risk, Model Assurance, and Regulatory Trust Still Limit How Far Operators Will Rely On Digital Twins

As vessels become more connected, digital twins rely on more sensors, interfaces, remote access, and software layers, increasing cyber exposure and raising the consequences of bad data or faulty integration. IMO’s cyber risk guidance and IACS cyber resilience requirements make it clear that cyber resilience is no longer optional; it is becoming part of core ship safety and system assurance. This matters as owners will not allow a digital twin to influence higher-value operational decisions unless they trust the data, the network, and the model itself.

For instance, in March 2025, IMO’s Facilitation Committee approved revised cyber risk management guidance, underscoring that maritime digitalization is advancing only alongside tighter governance and security expectations.

SEGMENTATION ANALYSIS

By Solution

Software Segment Led Market as It Scales Analytics, Orchestration, and Decision Support

The global market by solution is divided into hardware, software, and services.

The software segment accounted for the largest digital twin in marine market share of 40.95% in 2025 and is projected to grow at the fastest CAGR of 5.59% in the coming years. This pattern shows that the market is moving beyond basic sensor connectivity into platforms that interpret data, automate decision-making, and enable fleet-wide visibility. In business terms, software captures more value as it is easier to upgrade, easier to replicate across vessels performing and ports, and better aligned with recurring digital service models than hardware-heavy deployments.

The services segment accounted for the second-largest market share in 2025 of 35.17% and is estimated to register a CAGR of 4.57% during the forecast period.

By Vessel Type

Class-of-Ship Twin Segment Dominated as It Standardizes Intelligence Across Similar Vessels

The global market by vessel type is divided into single vessel twin, class-of-ship twin, fleet twin, and voyage twin.

The class-of-ship twin segment accounted for the largest market share of 30.99% and is projected to grow at a CAGR of 5.63% during the forecast period. Major owners can build a single digital framework for a vessel class and reuse it across sister ships, lowering deployment costs and speeding up scaling. This segment also balances detail and efficiency well, as it is more actionable than broad fleet-level analytics and more scalable than one-off single-vessel twin programs.

The fleet twin segment accounted for the second-largest market share in 2025 of 30.70% and is estimated to register a CAGR of 5.14% during the forecast period.

By Port Level

Port-Wide Twin Segment Commanded as It Connects Operations across the Full Terminal Ecosystem

The global market by port level is divided into single berth twin, terminal twin, port-wide twin, and multi-port network twin.

The port-wide twin segment accounted for the largest market share of 30.55% and is projected to grow at a CAGR of 5.15% during the forecast period of 2026-2034. The market sees greater value in optimizing the entire port environment rather than isolated berth-level assets. The reason is practical: when traffic flow, berth scheduling, yard planning, utilities, and marine access are linked in a single twin environment, operators achieve better throughput, better congestion control, and stronger return on digital investment.

The terminal twin segment accounted for the second-largest market share in 2025 of 27.06% and is estimated to rise at a CAGR of 5.06% during the forecast period.

By Marine Subsystem

Automation/Navigation Segment Led Market as It Sits at the Center of Real-Time Vessel Decision-Making

The global market by marine subsystem is divided into hull/structure, propulsion system, electrical/energy, machinery, automation/navigation, cargo/process, safety/environmental, and marine operations.

The automation/navigation segment accounted for the largest market share of 18.40% and is projected to grow at a CAGR of 5.67% during the forecast period of 2026-2034. The growth is driven by bridge systems, route control, navigation support, and automated monitoring, which generate continuous operational data that directly influence vessel safety, efficiency, and compliance. In short, buyers tend to prioritize twin investments where the operational impact is immediate and visible, and that favors automation- and navigation-linked use cases.

The electrical/energy segment accounted for a moderate 15.21% market share in 2025 and is estimated to grow at the fastest CAGR of 6.32% during the forecast period.

By Modeling Type

Hybrid Twin Dominated as It Combines Physics Accuracy with Live Data Adaptability

The global market by modeling type is divided into physics-based twin, data-driven twin, hybrid twin, rule-based twin, reduced-order twin, and real-time simulation twin.

The hybrid twin segment accounted for the largest market share of 27.27% and is projected to grow at the fastest CAGR of 5.93% during the forecast period of 2026-2034. The market increasingly wants models that are accurate enough for engineering decisions but flexible enough for real-world operating conditions. Pure physics models can be slower and heavier, while pure data models may be weaker in causality; hybrid twins sit in the middle and therefore offer the strongest business case for scalable marine deployment.

The data-driven twin segment accounted for a moderate market share of 21.59% in 2025 and is estimated to grow at a CAGR of 4.75% during the forecast period.

By Integration Mode

Hybrid Onboard + Shore Segment Commanded Market as It Links Vessel Execution with Shore-Side Control

The global market by integration mode is divided into onboard only, shore-based only, hybrid onboard + shore, cloud based, and on-premises.

The hybrid onboard + shore segment accounted for the largest market share of 34.15% and is projected to grow at a CAGR of 5.51% during the forecast period of 2026-2034. Its scale advantage is easy to understand: marine operators want local onboard responsiveness, but they also want fleet-level monitoring, benchmarking, and planning from shore. This architecture supports both needs simultaneously, making it more commercially attractive than isolated onboard-only or shore-only approaches.

The cloud based segment accounted for a moderate market share in 2025 of 15.68% and is estimated to grow at the fastest-growing CAGR of 5.58% during the forecast period.

By Deployment Mode

Retrofit Twin Segment Dominated as It Matches Size and Urgency of Installed Fleet Base

The global market by deployment mode is divided into newbuild embedded twin and retrofit twin.

The retrofit twin segment accounted for the largest market share of 34.15% and is projected to grow at a CAGR of 5.51% during the forecast period of 2026-2034. This dominance is driven by the reality that most marine assets already exist, and operators need digital gains without waiting for fleet replacement cycles. Retrofit deployment is therefore the most practical route for improving maintenance, fuel performance, and monitoring across a large installed base.

The newbuild embedded twin segment accounted for a moderate market share in 2025 of 45.93% and is estimated to grow at the fastest-growing CAGR of 4.89% during the forecast period.

By Application

Predictive Maintenance Segment Led Market as It Directly Reduces Downtime and Lifecycle Cost

The global market by application is divided into asset health monitoring, condition-based maintenance, predictive maintenance, root-cause analysis, structural integrity monitoring, propulsion optimization, emissions optimization, route/voyage optimization, and others.

The predictive maintenance segment accounted for the largest market share of 20.15% and is projected to grow at the fastest-growing CAGR of 5.86% during the forecast period of 2026-2034. The growth is driven by commercial signals in the dataset as predictive maintenance gives a direct and measurable business return. Operators can justify spending more easily when the twin helps prevent failure, improve spare-parts planning, reduce service disruption, and extend the useful life of critical marine systems.

The structural integrity monitoring segment accounted for a moderate market share in 2025 of 13.49% and is estimated to grow at a CAGR of 5.28% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Naval/Coast Guard/Government Marine Segment Dominated Market as It Operates High-Value, Mission-Critical Fleets

The global market by end user is divided into commercial shipping, offshore energy/offshore marine, ports/harbors/terminals, shipbuilding/repair/conversion, naval/coast guard/government marine, marine OEM/marine equipment, and marine infrastructure/coastal/waterways.

The naval/coast guard/government marine segment accounted for the largest market share of 40.93% and is projected to grow at the fastest CAGR of 5.45% during the forecast period of 2026-2034. This dominance reflects the high complexity, long service life, and mission-readiness requirements of government-operated vessels. In business terms, the digital twins’ model is easier to justify in this segment as the assets are expensive, the performance standards are high, and the value of better availability is much greater than in lower-complexity marine environments.

The shipbuilding/repair/conversion segment accounted for a moderate market share in 2025 of 18.06% and is estimated to grow at a CAGR of 5.63% during the forecast period.

Digital Twin in Marine Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Digital Twin in Marine Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 264.0 million, and is also expected to maintain the leading share in 2026, with USD 276.7 million. The growth is accelerating adoption in shipbuilding, port operations, and offshore energy sectors. Key drivers include the need for predictive maintenance, increased efficiency, and emissions compliance.

U.S. Digital Twin in Marine Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 246.02 million in 2025 and is estimated to have a CAGR of 3.78% during the forecast period.

Europe

Europe is projected to grow at the fastest rate with the highest CAGR of 5.17% during the forecast period. In 2025, the market value stood at USD 164.0 million. The European market is experiencing rapid growth, driven by strict EU decarburization regulations, expansion in offshore wind/aquaculture, and advancements in AI/IoT technologies. The market is driven by the need for predictive maintenance, fuel optimization, and emission reduction to meet mandatory environmental standards.

U.K. Digital Twin in Marine Market

The U.K. market in 2025 was valued at USD 32.57 million and is estimated to grow at a 4.34% CAGR during the forecast period.

Germany Digital Twin in Marine Market

The German market in 2025 was valued at USD 21.17 million and is estimated to grow at a 5.57% CAGR during the forecast period.

Northern Europe Digital Twin in Marine Market

The Northern Europe market in 2025 was valued at USD 21.12 million and is estimated to grow at a 7.05% CAGR during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 183.7 million in 2025 and ranked second-largest. The growth is driven by rapid adoption in shipbuilding, high-volume shipping, and smart port development in China, Japan, and South Korea. The market is experiencing massive growth, supported by IoT integration, AI-based analytics for predictive maintenance, and government-backed decarburization efforts.

China Digital Twin in Marine Market

The Chinese market in 2025 was valued at USD 58.30 million and is estimated to grow at a rate of 5.17% during the forecast period.

India Digital Twin in Marine Market

The Indian market in 2025 was valued at USD 32.91 million and is estimated to grow at a 7.16% CAGR during the forecast period.

Japan Digital Twin in Marine Market

The Japanese market in 2025 was valued at USD 30.77 million and is estimated to grow at a 5.71% CAGR during the forecast period.

Rest of the World

The Rest of the world, consisting of Latin America and the Middle East & Africa regions, is expected to witness moderate growth in this market space during the forecast period. The Latin America market was valued at USD 17.28 million in 2025. The Middle East & Africa market was valued at USD 58.40 million in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Class-Led Assurance Platforms and OEM-Led Digital Operating Ecosystems to Maintain Their Supremacy

The competitive landscape in the digital twin in marine market is led by DNV, ABS, Siemens, Kongsberg Maritime, and Wärtsilä, but they are not competing in exactly the same way. DNV and ABS are using their class, verification, and compliance strength to move digital twins from a real-time monitoring tool into a trusted lifecycle platform.

At the same time, Siemens, Kongsberg Maritime, and Wärtsilä are pushing the market toward broader digital platforms that connect design, operations, and performance optimization. Siemens is expanding fast through major shipbuilding programs, including HD Hyundai’s integrated digital shipbuilding platform and Navantia’s implementation of digital twin work for naval programs, which shows its strength in end-to-end engineering and industrial metaverse capability.

LIST OF KEY DIGITAL TWIN IN MARINE COMPANIES PROFILED

- Kongsberg Digital AS (Norway)

- Wärtsilä Corporation (Finland)

- Napa Ltd (Finland)

- DNV AS (Norway)

- ABS Wavesight (U.S.)

- Bureau Veritas (France)

- Lloyd’s Register Group Limited (U.K.)

- AVEVA Group Limited (U.K.)

- Siemens Digital Industries Software (U.S.)

- Hexagon AB (publ) (Sweden)

- CADMATIC Oy (Finland)

- BMT Group Ltd (U.K.)

- HD Hyundai Marine Solution Co., Ltd. (South Korea)

- Samsung Heavy Industries Co., Ltd. (South Korea)

- ABB Ltd. (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- November 2025: ABS and Siemens Digital Industries Software signed an MoU to digitalize shipbuilding-classification workflows, covering the use of class rules in 3D design, model-based verification, secure data exchange, and digital twin integration for marine compliance and classification.

- November 2025: Siemens and HD Hyundai signed an MoU to accelerate the digital transformation of U.S. shipbuilding, using Siemens Xcelerator, digital twin, MBSE, and PLM technologies to modernize shipyard operations and vessel production.

- March 2025: The Maritime and Port Authority of Singapore (MPA) signed a three-year MoU with Jurong Port, Singapore Cruise Center, Esri Singapore, Hexagon, Nika, TCOMS, A*STAR IHPC, and NUS C4NGP to apply geospatial tools and support Maritime Digital Twin use cases for port safety, navigation, bunkering, and operational planning.

- February 2025: Siemens and Compute Maritime announced a collaboration to transform ship design by linking Compute Maritime’s NeuralShipper platform with Siemens’ Simcenter STAR-CCM+ for simulation, validation, and faster digital vessel design optimization.

- February 2025: The Japanese Digital Twin Project entered into a new phase as K Line, Kyokuyo Shipyard, Mitsui E&S Shipbuilding, and Sumitomo Heavy Industries Marine & Engineering joined the cross-maritime industry program to build a secure, real-time data-sharing framework for lifecycle digital twins.

REPORT COVERAGE

The global digital twin in marine market growth analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key marine industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.74% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Solution

By Vessel Type

By Port Level

By Marine Subsystem

By Modeling Type

By Integration Mode

By Deployment Mode

By Application

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 687.4 million in 2025 and is projected to reach USD 1,049.0 million by 2034.

In 2025, the European market value stood at USD 164.0 million.

The market is expected to exhibit a CAGR of 4.74% during the forecast period.

The software segment is expected to hold the highest CAGR over the forecast period.

Decarburization, fuel efficiency, and lifecycle cost control are turning digital twins into a core operating tool that drives market growth.

DNV, ABS, Siemens, Kongsberg Maritime, and Wärtsilä are the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us