Drone Inspection and Maintenance Market Size, Share & Industry Analysis, By Autonomy Level (Manual, Semi-Autonomous, and Fully Autonomous), By Payload (Camera, Thermal Camera, Laser Scanner, Hyperspectral Imager, and Gas Sensor), By Solution (Platform, Software, Infrastructure, and Service), By Application (Infrastructure Inspection, Energy Inspection, Industrial Inspection, Construction Inspection, and Environmental Monitoring), and Regional Forecast, 2026-2034

Drone Inspection and Maintenance Market Size and Future Outlook

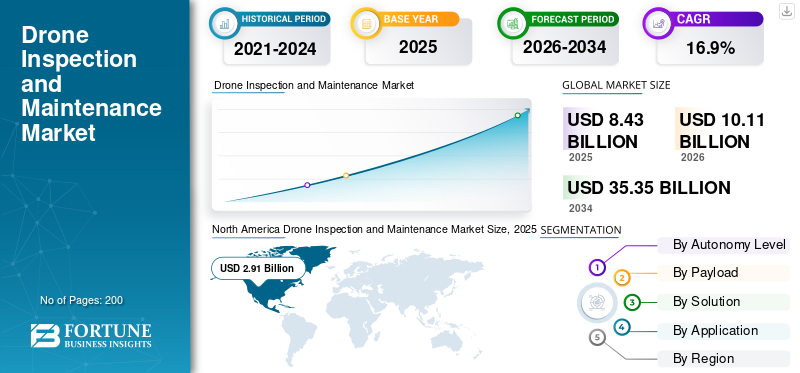

The global drone inspection and maintenance market size was valued at USD 8.43 billion in 2025. The market is projected to grow from USD 10.11 billion in 2026 to USD 35.35 billion by 2034, exhibiting a CAGR of 16.9% during the forecast period. North America dominated the drone inspection and maintenance market with a market share of 34.52% in 2025.

The drone inspection and maintenance market encompasses Unmanned Aerial Vehicles (UAVs) equipped with advanced sensors for non-destructive testing, asset monitoring, and upkeep across industries including energy, infrastructure, oil & gas, and utilities. Autonomous AI-driven drones with thermal imaging, LiDAR, and high-resolution cameras are replacing traditional manual inspections, enabling safer access to hard-to-reach areas such as wind turbines, bridges, and power lines.

Key players include SZ DJI Technology (China), SkySpecs (U.S.), Cyberhawk (U.K.), Raptor Maps (U.S.), Drone Volt (France), PrecisionHawk (U.S.), AeroVironment (U.S.), Percepto (Israel), Delair (France), and Sharper Shape (U.S.), shaping the market by pairing reliable drone platforms with inspection-grade sensors, analytics software, and service delivery.

Download Free sample to learn more about this report.

DRONE INSPECTION AND MAINTENANCE MARKET TRENDS

Rising Adoption of Autonomous AI-Enabled Drones is Shaping Evolution in Market

The market is experiencing a shift toward autonomous operations powered by artificial intelligence and machine learning, enabling real-time defect detection and predictive analytics for assets across industries including energy and infrastructure. Integration with cloud technology and advanced sensors such as thermal imaging and LiDAR is enhancing data accuracy and operational efficiency. Industries are increasingly replacing manual methods with drone solutions for safer access to hazardous areas, driven by improvements in flight stability and software platforms that automate workflows.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Demand for Cost-Effective Safety Solutions Driving Market Growth

The global drone inspection and maintenance market growth is driven by the need for safer inspections in hazardous environments, where drones reduce human risk and eliminate costly scaffolding or crane rentals. Technological advancements in sensors, battery life, and AI analytics enable faster, more precise data collection for real-time decision-making in sectors including utilities and construction. Regulatory adaptations and industry emphasis on operational efficiency further propel adoption as enterprises seek flexible, environmentally conscious alternatives to traditional methods.

MARKET RESTRAINTS

Shortage of Skilled Operators Hinders Market Growth

A major restraint is the scarcity of qualified commercial drone pilots, compounded by complex licensing requirements and the need for specialized skills in data analysis and industry-specific knowledge. This limits widespread deployment despite growing demand in infrastructure and environmental assessments. Stringent training demands deter new entrants, narrowing the pool of capable professionals.

MARKET OPPORTUNITIES

Expansion in Emerging Economies and Predictive Tech to Create Growth Opportunities

Significant growth potential exists in emerging markets investing in infrastructure, smart cities, and energy sectors, where drone services remain untapped for proactive asset management. The integration of predictive analytics and digital maintenance technologies offers new pathways for fleet automation and reliability enhancements, particularly in Asia Pacific regions with rising commercial drone adoption. Service providers can leverage AI-driven solutions to deliver value-added diagnostics, attracting operators focused on minimizing downtime.

MARKET CHALLENGES

Regulatory and Technical Hurdles to Challenge Market Growth

Fragmented global regulations on airspace, BVLOS operations, and data privacy create compliance burdens and operational delays for providers. Technical issues such as limited battery life, payload capacity, and weather sensitivity restrict efficiency in extended missions, while cybersecurity risks in drone-cloud systems add complexity. High initial costs for equipment and software also challenge smaller enterprises.

Segmentation Analysis

By Autonomy Level

Manual Segment to Dominate Due to Easy Approvals and Deployment

Based on autonomy level, the market is segmented into manual, semi-autonomous, and fully autonomous.

The manual segment is anticipated to account for the largest drone inspection and maintenance market share they’re simple to approve, train, and deploy. Many sites need close visual checks and ad-hoc missions where autonomy adds cost without immediate ROI.

The fully autonomous segment is anticipated to rise with a CAGR of 17.8% over the forecast period.

By Payload

Camera Payload Segment Dominated Due to Low-Cost and High-Speed Visual Documentation Needs

Based on payload, the market is segmented into camera, thermal, camera, laser scanner, hyperspectral imager, and gas sensor.

In 2025, the camera segment dominated the global market as it is affordable and the fastest way to document defects and progress. High-resolution imagery supports repeat inspections, digital twins, and reporting without complex processing or specialist calibration.

The hyperspectral imager segment is projected to grow at a CAGR of 20.5% over the forecast period.

By Solution

Service Segment to Dominate as it Standardizes Recurring Inspection Schedules

Based on solution, the market is segmented into platform, software, infrastructure, and service.

The service segment is anticipated to witness a dominating market share over the forecast period as asset owners outsource pilots, compliance, and data processing. Drone-as-a-service reduces capex risk, solves talent gaps, and standardizes recurring inspection schedules across dispersed sites.

The software segment is projected to grow at a high CAGR of 18.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Energy Inspection Segment Leads Due to Grid Expansion, Renewable Buildout, and Stricter Uptime Targets

Based on application, the market is segmented into infrastructure inspection, energy inspection, industrial inspection, construction inspection, and environmental monitoring.

The energy inspection segment dominated as demand remains high due to expanding grids, renewables, and tougher reliability targets. Drones cut outage time, improve safety, and enable frequent checks on towers, substations, pipelines, and solar arrays.

In addition, environmental monitoring are projected to grow at a CAGR of 17.1% during the study period.

Drone Inspection and Maintenance Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Drone Inspection and Maintenance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 2.40 billion, and also maintained the leading share in 2025, with USD 2.91 billion. Demand stays strong as utilities, oil & gas, and transport owners push safer, faster inspections. BVLOS progress and insurance acceptance accelerate routine drone programs, not one-off projects.

U.S. Drone Inspection and Maintenance Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.18 billion in 2026, accounting for roughly 16.7% of global sales. Demand is driven by massive utility inspection cycles, wildfire mitigation, pipeline integrity programs, and industrial safety compliance. BVLOS waivers and enterprise procurement maturity keep budgets recurring and scalable.

Asia Pacific

Asia Pacific is projected to record a growth rate of 17.5% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 2.93 billion by 2026. Demand grows fastest as new grid lines, renewables, ports, and mega-projects expand inspection workload. Large contractor ecosystems and cost pressure favor drones to replace manpower-heavy surveys.

Japan Drone Inspection and Maintenance Market

The Japan market share is estimated at around USD 0.42 billion in 2026, accounting for roughly 16.7% of CAGR during the forecast period. Demand rises from aging bridges, tunnels, coastal assets, and stringent safety culture. Labor shortages push automation; operators adopt drones to maintain inspection frequency while reducing site closures.

China Drone Inspection and Maintenance Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.34 billion. Demand scales with extensive power networks, solar and wind buildouts, and rapid construction activity. Large domestic drone supply and integrated operations drive high utilization, especially for linear assets.

India Drone Inspection and Maintenance Market

The India market is estimated at around USD 0.54 billion in 2026. Demand accelerates as highways, rail corridors, refineries, and expanding power distribution need faster inspections. Government-enabled drone programs and price-sensitive buyers favor service providers and repeatable, high-volume missions.

Europe

Europe is estimated to reach USD 2.58 billion in 2026 and secure the position of third largest region in the market. Demand rises with strict safety rules, decarbonization projects, and aging bridges, rail, and grids. U-space frameworks and standardized operating categories encourage scaled inspections, especially for renewables.

U.K. Drone Inspection and Maintenance Market

The U.K. market growth is estimated at around USD 0.74 billion in 2026, representing roughly 16.6% of global sales. Demand grows as rail, utilities, offshore wind, and local authorities reduce working-at-height exposure. Contractors prefer drone-as-a-service, bundling data capture with analytics to shorten planning and maintenance cycles.

Germany Drone Inspection and Maintenance Market

Germany’s market is projected to reach approximately USD 0.68 billion in 2026. Demand strengthens from grid upgrades, industrial plant reliability programs, and transport infrastructure maintenance. Buyers emphasize documentation quality, repeatability, and compliance, pushing higher-end sensors and standardized workflows.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.75 billion and USD 0.36 billion in 2026. Demand expands from oil & gas corridors, mining, solar farms, and critical infrastructure security. Adoption is uneven, but service-led models grow where skilled pilots and approvals are scarce.

COMPETITIVE LANDSCAPE

Key Industry Players

Notable Players to Increase their Market Share through Novel Product Developments

Key companies operating in the drone inspection and maintenance market are consistently working to strengthen their competitive position through new product development, acquisitions, and geographic expansion. Leading participants are allocating significant resources to research and development to enhance drone performance and create new use cases across inspection and maintenance activities. Market growth is also being supported by the rising adoption of drones among commercial enterprises, government bodies, and end users. The competitive environment is expected to remain intense over the coming years, as major players continue to focus on technological innovation and business expansion.

LIST OF KEY DRONE INSPECTION AND MAINTENANCE COMPANIES PROFILED IN REPORT

- SZ DJI Technology Co., Ltd. (China)

- SkySpecs, Inc. (U.S.)

- Cyberhawk Innovations Limited (U.K.)

- Raptor Maps, Inc. (U.S.)

- Drone Volt SA (France)

- PrecisionHawk, Inc. (U.S.)

- AeroVironment, Inc. (U.S.)

- Percepto Ltd. (Israel)

- Delair SAS (France)

- Sharper Shape Oy (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Danish drone startup Quali Drone worked with RWE and partners to demonstrate autonomous offshore wind turbine blade inspections while blades were rotating.

- August 2025: Vestas partnered with Denmark’s Ministry of Climate, Energy and Utilities and Ministry of Transport to enable autonomous drones for offshore wind inspection and maintenance, targeting lower emissions and operating cost.

- September 2024: RES acquired Sulzer Schmid Laboratories AG, a specialist in autonomous drone inspections and condition monitoring for wind turbine blades, to strengthen RES’ wind O&M offering.

- July 2023: Nearthlab announced it was scaling up its strategic partnership with ONYX Insight beyond North America into Europe and Asia Pacific, combining autonomous drone inspection capability with predictive maintenance

- September 2018: Siemens Gamesa Renewable Energy and SkySpecs signed an agreement for autonomous drone inspections of Siemens Gamesa wind turbine blades, covering both onshore and offshore fleets.

REPORT COVERAGE

This drone inspection and maintenance market research report offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Autonomy Level, By Payload, By Solution, By Application, and Region |

| By Autonomy Level |

|

| By Payload |

|

| By Solution |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.43 billion in 2025 and is projected to reach USD 35.35 billion by 2034.

In 2025, North America’s market value stood at USD 2.91 billion.

The market is expected to exhibit a CAGR of 16.9% during the forecast period of 2026-2034.

By manual segment is expected to dominate the market.

The demand for cost-effective safety solutions to drive the market growth.

SZ DJI Technology Co., Ltd. (China0, SkySpecs, Inc. (U.S.), Cyberhawk Innovations Limited (U.K.), Raptor Maps, Inc. (U.S.), Drone Volt SA (France), PrecisionHawk, Inc. (U.S.) are few major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us