Earth Observation Market Size, Share & Industry Analysis, By Orbit (LEO, MEO, GEO, Others),By Solution (Imagery Data, Imagery Data Analytical Service, Others), By Imaging Resolution (Very High Resolution, High Resolution, Medium Resolution, Low Resolution), By Application (Urban Development, Mapping & Surveying, Agriculture, Environmental Monitoring, Natural Resource Exploration, Security & Intelligence, Disaster &, Emergency Management, Others) By Technology (Optical Imaging, Radar Imaging, Spectral Imaging, Thermal Imaging, LiDAR) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

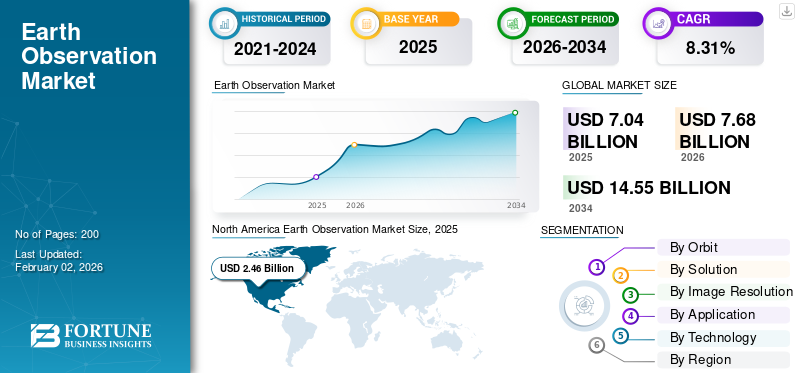

The global earth observation market size was valued at USD 7.04 billion in 2025. The market is projected to grow from USD 7.68 billion in 2026 to USD 14.55 billion by 2034, exhibiting a CAGR of 8.31% during the forecast period. North America dominated the global market with a share of 34.97% in 2025.

The Earth Observation (EO) market revolves around collecting and analyzing information about our planet using satellites, aircraft, drones, and ground-based sensors. It includes imagery data, analytical services, remote sensing, and platforms that convert raw observations into insights for governments, businesses, and researchers. EO supports a wide range of applications from tracking deforestation, monitoring crops, and managing natural disasters to supporting defense intelligence and urban planning. The technology behind it spans optical, radar, hyperspectral, and thermal imaging systems that provide precise, real-time visibility of environmental and human activity. In recent years, demand has surged due to the rise of small satellite constellations, synthetic aperture radar (SAR), cloud-based analytics, and climate-focused initiatives.

Key players include Airbus Defence & Space, Maxar Technologies, Planet Labs, ICEYE, Capella Space, Satellogic, BlackSky, Spire Global, and Thales Alenia Space, along with public programs such as NASA, ESA, ISRO, and JAXA, which continue to shape the global EO ecosystem.

Download Free sample to learn more about this report.

Earth Observation Market Key Takeaways

- 2025 Market Size: USD 7.04 Billion

- 2026 Market Size: USD 7.68 Billion

- 2034 Forecast Market Size: USD 14.55 Billion

- CAGR: 8.31% from 2026–2034

- North America dominated the earth observation market with a 34.97% share in 2025.

- The LEO segment is projected to account for a 42.83% share in 2026.

- The imagery data analytical service segment is projected to hold a 41.11% share in 2026.

Asia Pacific

Asia Pacific generated USD 2.10 billion in 2025 and is projected to reach USD 2.31 billion in 2026.

North America

North America generated USD 2.46 billion in 2025 and is projected to reach USD 2.67 billion in 2026.

Europe

Europe accounted for USD 1.80 billion in 2025 and is expected to reach USD 1.97 billion in 2026.

U.S.

The earth observation market is projected to reach USD 1.84 billion in 2026.

Japan

The earth observation market is projected to reach USD 0.42 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Expanding Role of Satellite Data is a Primary Source for Market Growth

The earth observation market is witnessing rapid growth as satellite-based data becomes essential for managing environmental, economic, and security challenges. Governments and private organizations are investing heavily in EO capabilities to monitor everything from climate patterns and deforestation to urban growth and natural resources. The rise of small satellite constellations and high-resolution imaging technologies, such as radar and hyperspectral systems, has made earth surveillance more affordable and frequent. At the same time, cloud platforms and AI-powered analytics are transforming raw imagery into real-time insights that support smarter decision-making. Global sustainability goals, ESG reporting, and disaster resilience programs are also fueling adoption across agriculture, energy, defense, and infrastructure sectors. Together, these factors are positioning ground observation as a vital digital infrastructure, one that connects data from space with actions on the ground.

MARKET RESTRAINTS

High Costs and Data Complexity Slow Broader Adoption, Restrain Market Expansion

While the market continues to grow, several challenges still hold it back from reaching its full potential. Launching and maintaining satellite constellations demands significant capital investment, making it difficult for new entrants to compete. Weather conditions and cloud cover limit the consistency of optical imaging, while radar and hyperspectral data require advanced algorithms and skilled analysts to interpret. Differences in international regulations, export controls, and data privacy laws further complicate data sharing across borders. In many regions, especially emerging economies, the lack of technical expertise and infrastructure prevents organizations from fully utilizing EO data. Additionally, fragmented standards between government and commercial datasets reduce interoperability. Although advancements in cloud computing, AI, and low-cost satellite manufacturing are helping bridge these gaps, affordability and accessibility remain major hurdles to truly global adoption of EO technology.

MARKET OPPORTUNITIES

Digital Transformation Unlocks New Value from Space and Offers New Opportunities

The next phase of growth in the market lies in data integration and analytics. As industries embrace digital transformation, EO data is being combined with artificial intelligence, IoT sensors, and digital-twin platforms to deliver predictive insights. These capabilities open new opportunities in precision agriculture, carbon monitoring, infrastructure management, and climate adaptation. The growing focus on sustainability and transparent ESG reporting has made satellite data a critical tool for tracking emissions and protecting ecosystems. Public-private partnerships such as those between NASA, ESA, and private firms such as Planet Labs or Airbus are expanding access to high-quality, near-real-time imagery. Meanwhile, cloud-based subscription platforms allow even small businesses to access EO insights without large upfront costs. As these technologies mature, Earth Surveillance is evolving from an observational science into a core enabler of smarter, data-driven economies worldwide.

EARTH OBSERVATION MARKET TRENDS

Shift Toward Real-Time, AI-Driven Observation Defines Market Trends

The market is undergoing a remarkable transformation, moving from periodic satellite-based earth observation and imaging to continuous, intelligent monitoring of the planet. One of the most prominent trends is the adoption of AI-powered analytics, allowing faster interpretation of imagery for agriculture, defense, and environmental management. Multi-sensor data fusion combining optical, radar, thermal, and hyperspectral inputs is becoming standard practice for richer, more accurate insights. Cloud-based EO marketplaces such as UP42, SkyWatch, and Sentinel Hub are democratizing data access, enabling even small businesses to leverage satellite intelligence. Another key trend is the growing emphasis on sustainability and carbon accountability, with satellites tracking greenhouse gases, deforestation, and climate-related changes in real time. Miniaturized satellites and lower launch costs are also enabling near-daily global coverage. Collectively, these trends reflect a market evolving beyond observation toward predictive, AI-driven planetary awareness.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Managing Data Volume and Technical Complexity Remain Barriers to Hamper Market Growth

One of the biggest challenges facing the Earth Observation industry is the overwhelming volume of data generated by thousands of satellites orbiting the planet. Processing and storing these massive datasets require advanced cloud infrastructure and AI algorithms capable of identifying meaningful patterns quickly. Many organizations still struggle to transform raw imagery into practical insights due to limited technical expertise or a lack of standardized analytical frameworks. Cybersecurity threats, orbital congestion, and the risk of space debris collisions also pose growing operational challenges. Additionally, inconsistent data formats and varying licensing rules hinder interoperability between different EO systems. As the sector expands, balancing data security with open access will remain a delicate issue. Addressing these challenges will be crucial for ensuring that Ground Observation continues to evolve as a reliable, scalable, and sustainable source of global intelligence.

US Tariff Impact

U.S. tariffs on aerospace and electronic components have added cost pressures to the Ground Observation (EO) industry. Many satellites rely on imported sensors, optics, and semiconductors, making production more expensive and occasionally delaying launches. Smaller EO startups are especially affected, as higher component costs narrow profit margins and reduce competitiveness. Retaliatory tariffs have also disrupted international partnerships and supply chains for ground systems and payloads. However, the policy has indirectly encouraged U.S. companies to localize production and invest in domestic suppliers, fostering long-term self-reliance. In the short term, tariffs create friction, but they also drive innovation and supply-chain resilience.

Segmentation Analysis

By Orbit

Proliferation of Small Satellites and Constellation Deployments Accelerate Growth of LEO Segment

On the basis of the segmentation of Orbit, the market is classified into LEO, MEO, GEO, and others.

In 2026, the LEO segment is projected to lead the market with a 42.83% share. The Low Earth Orbit (LEO) segment dominates the market, driven by the increasing deployment of small-satellite constellations for high-frequency imaging and near-real-time monitoring

The GEO segment is expected to grow at the highest CAGR of 9.06% over the forecast period.

By Solution

AI-Powered Insights and Cloud Platforms Drive Growth in Imagery Data Analytical Services Segment

In terms of solution, the market is categorized into imagery data, imagery data analytical service, and others.

The imagery data analytical service segment is projected to dominate the market with a share of 41.11% in 2026. The segment is witnessing strong growth as industries move beyond raw satellite images toward actionable, AI-driven insights.

The imagery data segment is expected to grow at a CAGR of 8.86% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Image Resolution

Growing Demand for Precision Mapping and Urban Monitoring Boosts Very High-Resolution Segment

Based on image resolution, the market is segmented into very high resolution, high resolution, medium resolution, and low resolution.

The very high resolution segment is expected to lead the market, contributing 31.58% globally in 2026. The segment is expanding rapidly due to the increasing need for detailed and high-resolution images in defense, urban planning, and infrastructure monitoring.

The segment of high resolution is set to flourish and is growing at a CAGR of 8.85% growth across the forecast period.

By Application

Rising Geopolitical Tensions and Defense Modernization Programs Fuel Security & Intelligence Segment Growth

Based on application, the market is segmented into urban development, mapping & surveying

agriculture, environmental monitoring, natural resource exploration, security & intelligence, disaster & emergency management, and others.

The security & intelligence segment will account for 19.35% market share in 2026. The Security and Intelligence application segment remains a cornerstone of the market, supported by rising defense budgets and the growing need for geospatial intelligence (GEOINT).

The segment of disaster & emergency management is set to flourish with a growth rate of 9.36% growth across the forecast period.

By Technology

Widespread Use in Environmental and Infrastructure Monitoring Strengthens Optical Imaging Segment

Based on technology, the market is segmented into optical imaging, radar imaging, spectral imaging, thermal imaging, and LiDAR.

The optical imaging segment held the dominating position in 2024. Optical Imaging remains the most established and widely used technology in the market. It delivers high-clarity, color imagery critical for applications in agriculture, disaster management, and urban development.

The segment of radar imaging is set to flourish with a growth rate of 9.53% growth across the forecast period.

Earth Observation Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Earth Observation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 2.46 billion, contributing 34.97% to global market revenue, and is projected to grow to USD 2.67 billion in 2026. North America leads the EO market, driven by strong government programs such as NASA, NOAA, and NGA, alongside commercial players including Maxar and Planet Labs. The region benefits from high defense spending, advanced analytics infrastructure, and early adoption of AI-driven geospatial intelligence. In 2026, the U.S. market is estimated to reach USD 1.84 billion.

Other regions, such as Europe and the Asia Pacific, are anticipated to witness a notable earth observation market growth in the coming years.

Asia Pacific

Asia Pacific recorded a market size of USD 2.1 billion in 2025, capturing 29.83% of the global market share, and is projected to reach USD 2.31 billion in 2026. Asia-Pacific leads in growth rate, fueled by expanding satellite networks in China, India, Japan, and South Korea. Rising investments in agriculture, defense, and disaster management applications are propelling EO adoption across both public and commercial sectors. Backed by these factors, countries including China anticipates to record the valuation of USD 0.8 billion, Japan to record USD 0.42 billion, and India to record USD 0.6 billion in 2026.

Europe

The Europe market accounted for USD 1.8 billion in 2025, representing 25.58% of the global industry, and is expected to reach USD 1.97 billion in 2026. In the region, the U.K. and Germany both are estimated to reach USD 0.66 billion and 0.48 billion each in 2026.

Rest of the World

The Rest of the World market was valued at USD 0.68 billion in 2025, capturing 9.62% of global revenue, and is estimated to reach USD 0.73 billion in 2026. Over the forecast period, the Middle East, Africa, and Latin America regions would witness a moderate growth in this marketspace. The Middle East market in 2025 is set to record USD 0.43 billion as its valuation. Latin America is set to attain the value of USD 0.25 billion by 2025.

COMPETITIVE LANDSCAPE

Expanding Constellations and Data Partnerships Shape the Competitive Landscape

The global EO market is moderately consolidated, driven by a mix of established aerospace corporations, emerging small-satellite operators, and analytics platform providers. Leading players such as Airbus Defence and Space, Maxar Technologies, Planet Labs, ICEYE, Capella Space, BlackSky, Spire Global, and Satellogic dominate satellite manufacturing, data services, and analytics integration. Government-backed organizations such as NASA, ESA, ISRO, and JAXA continue to play a crucial role through joint missions, open-data programs, and technology co-development. Strategic collaborations between defense agencies, private companies, and cloud providers are accelerating innovation in data processing and AI-powered analytics. Continuous investment in miniaturization, radar imaging, and hyperspectral technologies is enhancing revisit rates and resolution, while partnerships across Europe, North America, and Asia are strengthening interoperability.

LIST OF KEY EARTH OBSERVATION COMPANIES PROFILED

- Airbus Defence and Space (Germany)

- Maxar Technologies (U.S.)

- Planet Labs PBC (U.S.)

- ICEYE (Finland)

- Capella Space (U.S.)

- Satellogic (U.S.)

- BlackSky Technology Inc. (U.S.)

- Spire Global (U.S.)

- Thales Alenia Space (France)

- Pixxel (India)

- Open Cosmos (U.K.)

- Synspective (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Synspective entered low Earth orbit with its seventh StriX satellite as part of a multi-launch agreement with Rocket Lab.

- August 2025: The Indian National Space Promotion and Authorization Centre (IN-SPACe) has chosen a consortium led by Pixxel, a Bengaluru-based space technology company, along with partners Dhruva Space, PierSight, and SatSure, to design, construct, own, and run a national EO constellation under a Public-Private Partnership (PPP) framework. Pixxel is building the highest-resolution hyperspectral satellite constellation in the world.

- April 2025: The European Space Agency (ESA) and Creotech Instruments S.A. have inked a contract worth USD 60.59 million for the CAMILA (Country Awareness Mission in Land Analysis) constellation of satellites. As part of the agreement, Creotech will supply a nationwide constellation of three or more earth observation satellites as well as specialized ground equipment.

- February 2025- A contract for the supply of a high-resolution optical satellite has been signed by Thales Alenia Space, a joint venture between Thales (67%) and Leonardo (33%), with NIBE Space (a division of NIBE Limited). This is the first phase in NIBE's EO constellation project. By 2025, this first contract seeks to make NIBE's first operational EO capabilities available in India.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.31% from 2026-2034 |

| Unit | Value (USD Billion ) |

| Segmentation |

By Orbit · LEO · MEO · GEO · Others By Solution · Imagery Data · Imagery Data Analytical Service · Others By Image Resolution · Very High Resolution · High Resolution · Medium Resolution · Low Resolution By Application · Urban Development · Mapping & Surveying · Agriculture · Environmental Monitoring · Natural Resource Exploration · Security & Intelligence · Disaster & Emergency Management · Others By Technology · Optical Imaging · Radar Imaging · Spectral Imaging · Thermal Imaging · LiDAR By Region · North America (By Orbit, Solution, Image Resolution, Application, Technology, and Country) o U.S. o Canada · Europe (By Orbit, Solution, Image Resolution, Application, Technology, and Country/Sub-region) o U.K. o Germany o France o Russia o Rest of the Europe · Asia Pacific (By Orbit, Solution, Image Resolution, Application, Technology, and Country/Sub-region) o China o Japan o India o South Korea o Rest of the Asia Pacific · Rest of the World (By Orbit, Solution, Image Resolution, Application, Technology, and Country/Sub-region) o Middle East & Africa o Latin America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.68 billion in 2026 and is projected to reach USD 14.55 billion by 2034.

In 2025, the North American market value stood at USD 2.46 billion.

The market is expected to exhibit a CAGR of 8.31% during the forecast period of 2026-2034.

The LEO segment led the market by Orbit.

The growing demand for the expanding role of satellite data in a connected world across verticals is the primary cause for market growth.

Airbus Defence and Space, Maxar Technologies, Planet Labs, ICEYE, Capella Space, BlackSky, and Spire Global are some of the prominent players in the market.

North America dominated the global market with a share of 34.97% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us