Electronic Intelligence (ELINT) Market Size, Share & Industry Analysis, By Platform (Airborne, Naval, Land-based, and Space-based), By System Type (Strategic ELINT, Tactical ELINT, and Integrated / Multi-mission ELINT), By Component (Antennas, Receivers, Signal Processors, Direction Finding Systems, and Others), By Frequency Band (HF, VHF/UHF, and SHF/EHF), By Application (Threat Detection & Early Warning, Surveillance & Reconnaissance, Targeting Support, Electronic Warfare Support, Border and Maritime Monitoring, and Others), By End User, and Regional Forecast, 2026-2034

Electronic Intelligence (ELINT) Market Size and Future Outlook

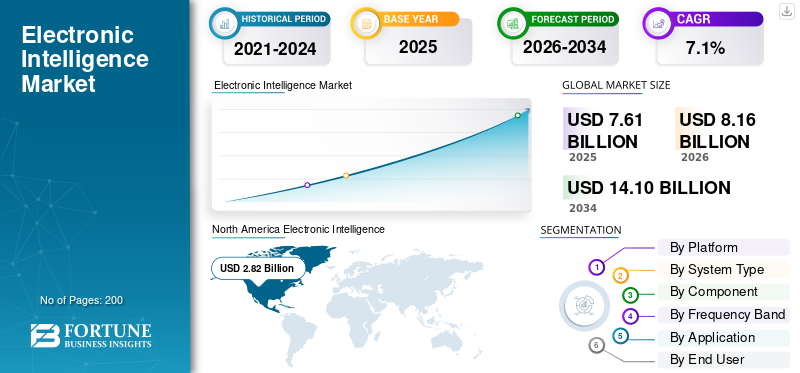

The Electronic Intelligence (ELINT) market size was valued at USD 7.61 billion in 2025. The market is projected to grow from USD 8.16 billion in 2026 to USD 14.10 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the electronic intelligence market with a market share of 37.05% in 2025.

The Electronic Intelligence (ELINT) market includes systems and software designed to detect, intercept, and analyze non-communication electromagnetic signals, such as radar emissions. Growth is primarily driven by increasing defense spending, a stronger focus on Intelligence, Surveillance, and Reconnaissance (ISR) and electronic warfare, and the need to monitor more contested electromagnetic environments.

Key players operating in the market are L3Harris Technologies, Saab AB, Elbit Systems Ltd., Leonardo S.p.A., and BAE Systems plc. They are advancing the market with airborne and naval ELINT systems, integrated sensing suites, and software-led mission upgrades that improve threat detection, surveillance, and operational awareness.

Download Free sample to learn more about this report.

ELECTRONIC INTELLIGENCE (ELINT) MARKET TRENDS

Multi-Platform ELINT Integration is a Prominent Market Trend

A major trend in the market is the shift from standalone collection systems to multi-platform and networked ELINT architectures. Militaries are no longer focused on isolated airborne or naval sensors; they require ELINT data to flow across aircraft, ships, ground stations, and space-linked networks in near real time. ELINT integration speeds up threat monitoring, boosts situational awareness, and enables quicker electronic warfare planning. The market is moving toward ELINT systems that are more connected, flexible, and useful in contested environments.

In December 2025, Saab received an order valued at approximately USD 150 million from a European NATO country. This order is for its Sirius passive sensor system, which is used for signals intelligence and surveillance. Deliveries will continue until 2030.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Defense Modernization and Persistent Threat Monitoring Needs Are Driving Market Growth

One major driving factor in the market is the increasing need to monitor complex radar, air-defense, and electronic activity in real time. Due to increasing geopolitical tensions, military forces encounter more contested airspace, busier electromagnetic environments, and faster threat cycles. ELINT systems are becoming important for surveillance, targeting support, and electronic warfare planning. Moreover, nations are increasingly prioritizing the improvement of Electronic Intelligence (ELINT) capabilities, focusing on detecting enemy emissions, accurately geolocating systems, and reducing the time required to turn data into usable intelligence.

MARKET RESTRAINTS

Complex Platform Integration and Long Development Cycles Are Restraining Market Growth

The difficulty of integrating advanced ELINT systems into modern airborne, naval, land-based, and networked defense platforms is a major market challenge. These systems depend on each other and thus require smooth integration with mission software, sensors, communication links, and electronic warfare suites. This complex approach leads to longer development timelines, higher costs, and more technical challenges. Moreover, delays are due to ongoing issues with software maturity, stringent testing requirements, and long delivery timelines, which are restraining Electronic Intelligence (ELINT) market growth.

MARKET OPPORTUNITIES

Growing Demand for Space-Enabled and Networked Intelligence Systems Creates Growth Opportunities

A major market opportunity is the rising demand for space-enabled and networked intelligence systems. Modern defense procurement strategy has shifted away from procuring standalone airborne or ground-based Electronic Intelligence (ELINT) systems. Agencies are prioritizing “system of systems” architectures that integrate ELINT with broader Electronic Warfare (EW), Intelligence, Surveillance, and Reconnaissance (ISR) platforms. This creates new opportunities for suppliers providing scalable passive sensing, integrated analytics, and multi-platform ELINT systems.

MARKET CHALLENGES

Rapidly Changing Emitter Environments and Complex Spectrums Emerges as a Market Challenge

Tracking, classifying, and interpreting threat emitters in real time has become more difficult. Modern radar systems are agile and often operate in crowded electromagnetic environments. This situation requires ELINT systems to receive continuous software updates, have stronger processing power, and achieve faster data fusion. Legacy systems are unable to function in today's complex environments as their original design does not meet modern, evolving requirements.

Impact of Russia Ukraine War

Russia-Ukraine War Increased the Demand for ELINT by Making Spectrum Awareness a Priority for Military Operations

The Russia-Ukraine war had a positive impact on the market. It pushed electronic surveillance, emitter tracking, and spectrum awareness higher on defense priority lists. The conflict demonstrated that forces need quicker visibility into radar activity, electronic emissions, electronic emissions, threats, and changing battlefield signatures.

As a result, ELINT moved from being a supporting function to a central role in surveillance, threat detection, and electronic warfare planning. The war accelerated procurement and modernization efforts, especially in Europe. According to SIPRI, global military spending reached USD 2.718 trillion in 2024, reflecting a 9.4% increase in real terms. This growth has been especially rapid in Europe and the Middle East.

Segmentation Analysis

By Platform

Need for Long-Range Surveillance and Quick Intelligence Collection Drives the Dominance of Airborne Segment

By platform, the market is categorized into airborne, naval, land-based, and space-based.

The airborne segment holds the largest Electronic Intelligence (ELINT) market share. It provides defense forces a wider surveillance radius, faster threat detection, and better operational flexibility than most other platforms. Airborne ELINT systems can cover large areas, monitor hostile radar activity from stand-off distances, and support missions across border zones, maritime spaces, and contested airspace. Many countries continue to prioritize aircraft-based intelligence platforms for faster and more responsive electronic surveillance capability.

Space-based is the fastest growing segment expected to grow at a CAGR of 15.1% over the forecast period.

By System Type

Tactical ELINT Segment Dominates Due to its Important Role in Real-Time Battlefield Awareness and Mission Support

By system type, the market is classified into strategic ELINT, tactical ELINT, and integrated / multi-mission ELINT.

The tactical ELINT segment leads the market as armed forces require fast, actionable intelligence closer to the point of operation. Tactical ELINT systems detect hostile radar activity, support threat warning, improve situational awareness, and assist in electronic warfare missions across air, land, and naval operations. This makes tactical systems easier to deploy and more frequently purchased than purely strategic systems, especially as militaries focus on responsive intelligence in contested environments.

Integrated / multi-mission ELINT is anticipated to grow at a CAGR of 10.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Receivers Segment Dominates Due to its Central Role in Signal Interception and Emitter Capture

Based on component, the market is segmented into antennas, receivers, signal processors, direction finding systems, and others.

The receivers segment holds the largest market share. The growth of this segment is driven by the central role of receivers in the intelligence chain. An ELINT system first needs to capture the signal accurately and across a wide frequency range before it can classify, locate, or analyze a threat emitter. This makes receivers one of the most important components in airborne, naval, land-based, and integrated ELINT systems. As defense forces seek broader spectrum coverage, faster detection, and improved performance in dense electromagnetic environments, investment increasingly focuses on receiver technologies.

For instance, in March 2024, HENSOLDT integrated SIGINT architectures that use shared antenna and receiver resources for COMINT and ELINT.

Moreover, BAE Systems states that its Eclipse RFTM receivers are installed on over 70% of U.S. ISR platforms.

Signal processors is fastest growing segment in the market expected to grow at a CAGR of 9.7% over the forecast period.

By Frequency Band

VHF/UHF Segment Dominates Due to its Broad Emitter Coverage and Strong Tactical Surveillance Relevance

Based on by frequency band, the market is segmented into HF, VHF/UHF, and SHF/EHF.

The VHF/UHF segment leads the market as many military emitters, surveillance systems, and tactical radar signals operate in or pass through these bands. This makes VHF/UHF important for real-time intelligence gathering, battlefield monitoring, and early threat detection in airborne, naval, and ground based missions. Moreover, defense forces rely heavily on this band as it provides a solid mix of coverage, operational relevance, and daily intelligence value in contested environments, resulting in segment dominance.

SHF/EHF is fastest growing segment in the market set to grow at a CAGR of 8.5% during the forecast period.

By Application

Real-time ELINT Enables Threat Monitoring and Operational Readiness, Drives Surveillance & Reconnaissance Segment Growth

Based on application, the market is segmented into threat detection & early warning, surveillance & reconnaissance, targeting support, electronic warfare support, border and maritime monitoring, and others.

The surveillance & reconnaissance segment leads the market, as ELINT is primarily used to generate real-time intelligence across the battlespace before a threat becomes action. Defense forces rely on these systems to monitor radar activity, track emitters, build threat pictures, and support wider intelligence gathering across air, sea, and land domains. Surveillance & reconnaissance remains the most consistent use case as it supports both day-to-day monitoring and high-tempo operational missions.

Electronic warfare support segment is set to record a CAGR of 10.0% during the forecast period.

By End User

Defense Forces Segment Dominates Due to Large-Scale Military Procurement and Operational Deployment Needs

Based on by end user, the market is segmented into defense forces, intelligence agencies, and homeland / border security.

The defense forces segment leads the market as the military is the main buyer and operator of ELINT systems for airborne, naval, land-based, and integrated missions. These systems help detect hostile emitters, support surveillance, improve threat awareness, and boost electronic warfare readiness. The segment dominates as ELINT is primarily viewed as a military capability linked to combat preparation, force protection, and mission planning rather than as a civilian or solely domestic security tool.

Homeland / border security segment is expected to grow at the fastest CAGR of 9.3% over the forecast period.

Electronic Intelligence (ELINT) Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world (Middle East & Africa and Latin America).

North America

North America Electronic Intelligence (ELINT) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market with a 37.04% share in 2025. The regional growth is driven by a strong mix of defense funding, advanced intelligence systems, and steady investment in electronic warfare capabilities across air, naval, ground, and space systems. The U.S. drives this leadership, as it continues to focus on threat detection, intelligence gathering, and readiness for electronic warfare in various areas. Due to which, North America remains at the forefront because it not only purchases ELINT systems but also integrates them into a broader network for surveillance, mission support, and national security. SIPRI highlights that the U.S. was the world’s largest military spender in 2024, representing 37% of global military spending. This further strengthens the region's position in high-end defense electronics demand.

U.S. Electronic Intelligence (ELINT) Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 2.60 billion in 2025, growing at a CAGR of 5.9% over a forecast period.

Europe

Europe held the second largest share of the market in 2025 and is anticipated to grow at the highest CAGR of 8.5% during the forecast period. The region remains a strong ELINT market, with increased emphasis on border surveillance, airborne intelligence, electronic warfare readiness, and defense capabilities following the significant decline in its security situation. Recent spending trends clearly highlight this shift, with SIPRI reporting notably fast growth in military spending in Europe in 2024.

France Electronic Intelligence (ELINT) Market

France market reached approximately USD 0.28 billion in 2025, equivalent to around 13.47% of industry revenues.

Germany Electronic Intelligence (ELINT) Market

The Germany’s market size was estimated at USD 0.28 billion in 2025, representing roughly 13.68% of global revenues.

Asia Pacific

Asia Pacific market is anticipated to be the second fastest growing region, growing at a CAGR of 7.3% during the forecast period. The regional market growth is driven by ongoing defense upgrades, maritime rivalries, and increased investment in ISR and electronic warfare. Additionally, military spending in the region has been rising for years. Countries such as China, Japan, India, South Korea, and Australia are expanding their air, naval, and electronic warfare capabilities.

China Electronic Intelligence (ELINT) Market

China’s market is projected to be one of the largest in Asia Pacific, with 2025 revenues valued at around USD 0.50 billion, representing roughly 29.47% of global sales.

Japan Electronic intelligence (ELINT) Market

The Japanese market in 2025 was valued at USD 0.26 Billion, accounting for roughly 15.43% of global revenues.

Rest of the World

The rest of the world (Middle East & Africa and Latin America) has a comparatively smaller share and is set to grow at a CAGR of 6.2% during the forecast period. This regional growth stems from monitoring missile and air defense systems, securing borders, conducting coastal surveillance, and modernizing targeted ISR capabilities. The Middle East holds more significance in this group due to higher defense spending, whereas Latin America adds to this with surveillance needs related to border, maritime, and internal security.

Latin America Electronic intelligence (ELINT) Market

The Latin America’s market was estimated at around USD 0.27 billion in 2025, accounting for roughly 26.74% of global revenues.

Middle East & Africa Electronic intelligence (ELINT) Market

Middle East & Africa market size was estimated at around USD 0.75 billion in 2025, and is expected to reach USD 1.31 billion in 2034, representing roughly 73.62% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on Integrated Multi-Domain Sensing, Processing, and Platform Solutions to Gain Market Advantage

The competitive landscape of the global Electronic Intelligence (ELINT) market includes a mix of large defense electronics firms and specialized surveillance companies that excel in ISR, SIGINT, and electronic warfare. L3Harris Technologies, Saab AB, Leonardo S.p.A., Elbit Systems Ltd., and BAE Systems plc. are key players as they operate in airborne, naval, land-based, and integrated sensing systems. L3Harris remains strong with its ISR, passive sensing, and electronic attack offerings. Saab builds its presence through surveillance systems that focus on ESM, ELINT, and COMINT. Leonardo and Elbit are also key players due to their extensive airborne mission systems, defense electronics, and ISTAR/EW capabilities, keeping them linked to ELINT modernization.

These companies provide integrated, upgradeable, and mission-ready solutions. Saab’s 2024 reports indicate ongoing high demand for its products, while L3Harris focuses on ISR, passive sensing, and classified intelligence systems. Leonardo’s defense electronics expertise strengthens its role in mission systems and electronic warfare, and Elbit advances its operational multi-domain sensing and ISTAR/EW solutions. Overall, competition in this market increasingly depends on merging sensing, processing, and platform integration into a single deployable package, rather than simply supplying individual boxes or sensors.

LIST OF KEY ELECTRONIC INTELLIGENCE (ELINT) COMPANIES PROFILED

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX (Raytheon Technologies) (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Thales S.A. (France)

- Israel Aerospace Industries Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- HENSOLDT AG (Germany)

- Rohde Schwarz Gmbh co kg (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Saab announced the launch of Poland’s second SIGINT ship, ORP Henryk Zygalski, in Gdansk, marking another visible step in naval signals-intelligence fleet expansion in Europe.

- December 2025: Saab received an order worth approximately USD 146.98 million from a European NATO country for its Sirius passive sensor system for SIGINT and surveillance, with deliveries scheduled through 2030.

- November 2025: HENSOLDT, Lufthansa Technik Defense, and Bombardier Defense announced that the first PEGASUS aircraft had arrived in Germany, marking the start of integration, testing, and certification work for the Bundeswehr’s next-generation airborne SIGINT platform based on Kalaetron Integral.

- September 2025: NATO stated that Exercise Dynamic Guard sharpened Allied electronic-warfare readiness in the Mediterranean, reflecting continued operational development of contested-spectrum missions closely linked to ELINT and EW demand.

- June 2024: HENSOLDT, Lufthansa Technik Defense, and Bombardier Defense reported significant progress on aircraft modification for Germany’s PEGASUS programme, with the first Global 6000 aircraft rolling out of Bombardier’s modification line for upcoming ground testing and systems integration.

- January 2024: Saab confirmed the keel laying ceremony for Poland’s second SIGINT ship, under the wider Polish naval-intelligence programme that Saab is leading as prime contractor.

- November 2023: HENSOLDT stated that the PEGASUS SIGINT system entered the implementation phase after receiving the green light for the system design, advancing one of Europe’s most important airborne SIGINT/ELINT-related programmes.

- November 2022: Saab signed a contract with the Polish State Treasury Armament Agency for the design, production, and support of two SIGINT ships for Poland, with a total order value of approximately USD 653.17 million.

REPORT COVERAGE

The global Electronic intelligence (ELINT) market analysis provides an in-depth study of market size, company profiling and forecast for all the market segments included in the report. It includes details on the market outlook and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By System Type

|

|

|

By Component

|

|

|

By Frequency Band

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.61 billion in 2025 and is projected to reach USD 14.10 billion by 2034.

In 2025, North Americas market value stood at USD 2.82 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period.

By platform, airborne segment is leading the market.

Rising defense modernization and persistent threat monitoring needs are the key factors driving the market.

Key players in the market include Northrop Grumman, Lockheed Martin, RTX, L3Harris, General Dynamics Corporation, Saab AB, and Thales S.A.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us