Fiber Optic Components Market Size, Share & Industry Analysis, By Type (Transceivers, Receivers, Cables, Connectors, Amplifiers, and Others), By Application (FTTX, Analytical and Medical Equipment, Distributed Sensing, Data Centers, Lighting, and Others), By Data Rate (Less than 10 G, 40 G, 100 G, and More than 100 G), By End-Use Industry (Telecommunication, BFSI, Industrial, Healthcare, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

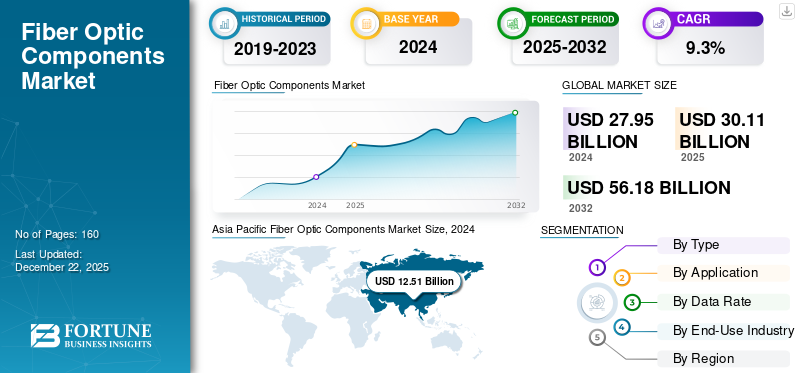

The global fiber optic components market size was valued at USD 30.11 billion in 2025. The market is projected to grow from USD 32.62 billion in 2026 to USD 65.03 billion by 2034, exhibiting a CAGR of 9.01% during the forecast period. The Asia Pacific dominated the global market, accounting for a 45.52% share in 2025.

Fiber optic components are the vital parts that combine and make a fiber optic cable by enabling the data transmission as the light signals. Major players included in this market are Broadcom, Sumitomo Electric, Lumentum, Finisar, Accelink Technologies, Fujitsu Optical Components, EMCORE, Acacia Communications, Furukawa Electric, and Tongding Interconnection Information Co Ltd.

Fiber optic components are witnessing significant market growth mainly due to increasing demand for high-speed internet through consistent connectivity and the rising need for consumer electronics such as smart-home devices, smartphones, and tablets. The industry is heavily changing due to new technological advances such as 5G which is accelerating the market share.

According to PatentPC, the adoption of 5G Internet is growing rapidly, with some industries seeing a 50% YoY increase in subscribers. This widespread hold of upgraded connectivity solutions is driving exceptional demand for fiber optic capabilities across extensive applications which is driving the market growth. These elements are helping in the expansion of market share.

The COVID-19 pandemic has impacted the demand for fiber optic components positively due to the rise in work-from-home, social, and educational demands. Providers had to ensure that connectivity was consistent and that the proper bandwidth to the transmission of data without interruption.

Download Free sample to learn more about this report.

FIBER OPTIC COMPONENTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 30.11 billion

- 2026 Market Size: USD 32.62 billion

- 2034 Forecast Market Size: USD 65.03 billion

- CAGR: 9.01% from 2026–2034

- Asia Pacific dominated the fiber optic components market with a 45.52% share in 2025.

- The FTTX segment accounted for the largest application share of 29.99% in 2026.

- The 40 G segment led the market with a 34.78% share in 2026.

North America

North America generated USD 8.08 billion in 2025 and is experiencing strong growth due to rising fiber broadband penetration, FTTH expansion, and increasing demand for high-speed connectivity.

Europe

Europe accounted for 16.85% of global revenue in 2025 and is projected to witness the second-highest growth rate, driven by smart city initiatives, IoT adoption, and expanding cloud infrastructure.

Asia Pacific

Asia Pacific remained the largest and fastest-growing regional market, supported by rapid 5G deployment, expanding telecom infrastructure, and strong adoption across IT and communications sectors.

U.S.

The market is projected to reach USD 6.48 billion by 2026, supported by growing fiber broadband coverage and continuous investments in next-generation network infrastructure.

Japan

The market is projected to reach USD 3.34 billion by 2026, driven by advanced telecommunications networks, increasing data traffic, and ongoing digital transformation initiatives.

Read More

IMPACT OF GENERATIVE AI

Integration of Generative AI with Fiber Optic Components by Enhancing Capabilities to Fuel Market Growth

Generative AI applications or tools demand large data throughput, leading to a significant impact on the production, design, and deployment of fiber optic components. Gen AI is utilized to enhance and optimize the layout of these components, predictive maintenance, and their placement. Gartner forecasts that in 2024, AI-powered fiber management will potentially decrease network downtime by as much as 30% and boost operational efficiency by 40%.

IMPACT OF RECIPROCAL TARIFFS

The effect of reciprocal tariffs has brought considerable difficulties and strategic changes within the fiber optic component industry, mainly for manufacturers and integrators dependent on global supply chains. Furthermore, the players are focusing on reducing risks by managing inventory effectively and spreading their suppliers.

Fiber Optic Components Market Trends

Increased Popularity of Digital Signage Creates a High Data Transfer Demand to Emerge as a Key Market Trend

The increasing adoption of fiber optic components in the digital signage sector can be attributed to their exceptional performance features. In digital signage, the caliber of visual output is crucial for the equipment. Fiber optic technology assures that cable connections do data transfer precisely and without negotiating speed. This feature of transmission is because of the high bandwidth and data transfer rates associated with fiber optics. Thus, it enables the management of large datasets needed for generating complex, high-resolution images.

MARKET DYNAMICS

Market Drivers

Rising Demand for High-Speed Internet and IoT to Aid Market Growth

As the need for high-speed Internet, IoT, and an increasing number of connected devices rises, data transmission has become crucial. Forbes projects that by 2025, the global installed base of Internet of Things (IoT) connected devices will reach around 75 billion, marking a fivefold surge over a decade. These advancements are driving demand for fiber optic network infrastructure that is faster, more reliable, and easily accessible. These factors are set to drive fiber optic components market growth.

Market Restraints

Rise in High Installation and Deployment Costs to Hinder Market Expansion

Installing fiber optic cable and its components necessitates a considerable initial investment for digging trenches, labor costs, and materials. Expanding fiber to remote or less populated regions is frequently not financially feasible, resulting in restricted network coverage.

Market Opportunities

Increasing Adoption of Latest Technological Advancements to Create Lucrative Market Opportunities

The integration of cutting-edge technologies such as silicon photonics, coherent optics, and wavelength division multiplexing (WDM) is improving performance while lowering expenses. Companies that embrace these technologies will be optimally positioned to excel in this rapidly evolving and high-demand industry. For instance, in 2023, an advancement was announced in fiber technology by the Japanese National Institute of Information and Communications Technology (NICT) in collaboration with Sumitomo Electric Industries, Ltd. This fiber features 19 cores, significantly improving data transmission potential in comparison to conventional single-core fibers. Additionally, an increased emphasis on sustainability is driving the need for environmentally friendly, energy-efficient fiber components.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Rising Need for Enhanced Features Provided by Transceivers Boosted Market Demand

Based on type, the market is segmented into transceivers, receivers, cables, connectors, amplifiers, and others.

From the point of view of the share, the transceivers segment dominated the market share 32.91% in 2026. Transceivers play a vital role in enabling efficient and rapid data transmission, which is essential for high-speed data centers and various cloud environments. The growing need for transceivers has been driven by modern communication systems that demand constantly higher data rates.

The connectors segment is expected to register the highest compound annual growth rate (CAGR) throughout the forecast period because of its essential function in meeting the demands of modern networks. They are vital in fiber optic networks, facilitating the seamless connection of optical fibers and ensuring efficient data transmission.

By Application

Increasing Usage of Optical Components in FTTX for Enhanced Data Speed to Aid Segment Growth

Based on application, the market is segmented into FTTX, analytical and medical equipment, distributed sensing, data centers, lighting, and others.

The category of FTTX produced the highest revenue with a share of 29.99% in 2026 due to its heavy requirement and extensive use of fiber optic cables, connectors, transceivers, and other components. The rollout of 5G and increasing consumer demands regarding high speed data transfers is also a major factor for this growth.

The data centers segment is anticipated to register the highest CAGR during the forecast period due to advanced digital services, surging data traffic, and the requirement of high performance network infrastructure.

By Data Rate

40 G Dominated the Market with Its Cost-Effective Capabilities in the Field of Fiber Optic Components

Based on the data rate, the market is categorized into less than 10 G, 40 G, 100 G, and more than 100 G.

In terms of market share 34.78%, in 2026, the 40 G segment dominated the market largely due to a cost-effective strategy and scalable solution for many organizations. This data rate remains important for mid-sized data centers and enterprises, fulfilling a gap between 10 G and 100 G deployments.

The more than 100 G segment is expected to record the highest CAGR during the forecast period. This growth is driven by the increasing demand for high-bandwidth applications and the sudden advancement of data-heavy industries, including telecommunications, data centers, and high-performance computing. As the necessity for quicker data transmission rises, high-speed cloud computing, streaming services, and the processing of large volumes of data rely heavily on these components.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Telecommunication Segment with Increasing Need for High-bandwidth Optical Networks

Based on the end-use industry, the market is categorized into telecommunication, BFSI, industrial, healthcare, aerospace & defense, and others.

In terms of share, the telecommunication segment was the largest in the market share 27.78% in 2026. The increasing use of cloud computing, remote work, and video streaming is driving the demand for high-bandwidth optical networks in telecommunications. Additionally, government initiatives and regulatory backing are contributing to the expansion of the market.

The healthcare segment is expected to record the highest CAGR during the forecast period due to the extensive usage for the application of fiber optics in slightly complex surgeries and radical medical treatments are driving demand within this industry.

FIBER OPTIC COMPONENTS MARKET REGIONAL OUTLOOK

Based on the region, market is studies across North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Asia Pacific

Asia Pacific Fiber Optic Components Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the Asia Pacific market stood at USD 13.71 billion, representing 45.52% of global demand, and is projected to grow to USD 15.08 billion in 2026. and also the fastest-growing market during the forecast period. Technological advancements, widespread adoption in IT and telecommunications, and the development of fiber-integrated infrastructure drives this growth. Furthermore, it is projected that there will be USD 670 million 5G connections (excluding IoT) in the Asia Pacific region by 2025, representing about 60% of the world's total 5G connections, as reported by GSMA.The Japan market is projected to reach USD 3.34 billion by 2026, the China market is projected to reach USD 5.48 billion by 2026, and the India market is projected to reach USD 2.07 billion by 2026.

China remains the leader in the Asia Pacific market, driven by its vast telecommunication sector, rapidly increasing domestic demand, and various government initiatives including “Made in China 2025”.

To know how our report can help streamline your business, Speak to Analyst

South America

The market for fiber optic components in South America is undergoing stable growth due to recent shifts in the local economy and initial government funding for research initiatives.

Europe

Europe contributed approximately USD 5.07 billion to the global market in 2025, accounting for 16.85% share, and is expected to reach USD 5.46 billion in 2026. Europe is estimated to grow at the second-highest rate during the forecast period due to a rise in smart cities and IoT developments. Moreover, the increasing reliance on cloud services and the development of data centers has accelerated the growth of the region in this market.The UK market is projected to reach USD 1.16 billion by 2026, while the Germany market is projected to reach USD 1.06 billion by 2026.

Middle East and Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 2.12 billion in 2025, accounting for 7.04% share, and is expected to reach USD 2.24 billion in 2026. The Middle East and Africa region has a smaller market presence. The expanding smart infrastructure projects and government initiatives have created a positive impact while economic diversification could be a challenging aspect.

North America

The market in North America reached USD 8.08 billion in 2025, representing 26.84% of total market revenue, and is projected to reach USD 8.65 billion in 2026. The North American market for fiber optic components is witnessing substantial growth opportunities. Fiber-optic internet adoption in North America is marked by considerable expansion, especially in the U.S., where fiber broadband now reaches 51.5% of primary residences. According to Broadband Search, in 2023, North America experienced its largest annual growth in fiber-to-the-home (FTTH), with 9 million homes newly connected by network providers. However, the region continues to encounter difficulties related to labor shortages and increasing construction expenses.The U.S. market is projected to reach USD 6.48 billion by 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Market Players to Use Merger & Acquisition, Partnership, and Product Development Strategies to Expand Business Reach

Key players operating in this market are providing fiber optic components to provide users with benefits such as higher bandwidth, faster speeds, greater distances, enhanced security, and resistance to interference. They are focusing on signing acquisition agreements with small and local firms to increase their business operations. Moreover, partnerships, mergers & acquisitions, and key investments will also boost the demand for this technology.

List of Key Fiber Optic Components Companies Studied

- Broadcom (U.S.)

- Sumitomo Electric (Japan)

- Lumentum (U.S.)

- Finisar (U.S.)

- Accelink Technologies (China)

- Fujitsu Optical Components (Japan)

- EMCORE (U.S.)

- Acacia Communications (U.S.)

- Furukawa Electric (Japan)

- Tongding Interconnection Information Co Ltd (China)

- II-VI Incorporated (U.S.)

- O-Net Tech Group (China)

- Mwtechnologies LDA (Portugal)

- Thorlabs, Inc. (U.S.)

- Prysmian Group (Italy)

- MacroOptica Ltd (Russia)

- Fiber Optika Technologies Pvt Ltd (India)

- LEONI Fiber Optics GmbH (Germany)

- Opticonx (U.S.)

- Oclaro (U.S.)

…and more

KEY INDUSTRY DEVELOPMENTS

- April 2025: Nortech Systems, a player in digital connectivity solutions and data management engineering, unveiled its latest innovation of a patent for non-magnetic expanded beam fiber optic cables. This technology platform transforms connectivity to be lighter, quicker, and more sustainable.

- July 2024: STL, a provider of optical and digital solutions, officially introduced high-density, 864F Micro Cables designed and developed to deliver swift and seamless connectivity for dense fiber networks across the U.S.

- April 2024: Broadcom launched its 200G PAM-4 Vertical-Cavity Surface-Emitting Laser (VCSEL) transmitter module aimed at advanced data centers. This module delivers enhanced data rates and superior signal integrity, facilitating quicker and more dependable data transmission across short distances.

- February 2024: Approved Networks, a brand of Legrand, a provider of optical networking technology, introduced its O-band transceiver. This transceiver can transfer data at a high speed and for distances up to 25km.

- March 2023: Lumentum Holdings Inc, a player in optical and photonic technologies for cloud and networking sectors, announced it would highlight its portfolio of full-band optical tunable transceivers in a live product demonstration.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment opportunities in this industry give both growth and value, particularly in its infrastructure development. Investments in fiber-optic infrastructure are classified into three categories initial, mid, and mature markets. According to BroadbandSearch.net,

- Approximately USD 253 billion is needed for initial markets, which encompass areas with less than 30% of households having fiber access.

- Mid markets, defined by a coverage of 30 to 60%, need approximately USD 131 billion to reach the unsatisfied households. In well-grown markets, which have over 60% of households connected to fiber, a USD 39 billion opportunity exists that is aimed at improving rural connectivity and hybrid networks.

- The overall investment needed across 87 countries is projected at roughly USD 420 billion, highlighting the substantial capital needed to achieve widespread fiber connectivity.

Therefore, presenting a huge opportunity for the players operating in this market.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, products/types, and the leading end-use industry of the product. Besides, it offers insights into the fiber optic components market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.01% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Application

By Data Rate

By End-Use Industry

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach a valuation of USD 65.03 billion by 2034.

In 2025, the market was valued at USD 30.11 billion.

The market is projected to record a CAGR of 9.01% during the forecast period.

By type, the transceivers segment led the market in 2025.

Rising demand for high-speed internet and IoT to aid market growth.

Broadcom, Sumitomo Electric, Lumentum, Finisar, Accelink Technologies, Fujitsu Optical Components, EMCORE, Acacia Communications, Furukawa Electric, and Tongding Interconnection Information Co Ltd are the top players in the market.

Asia Pacific held the highest market share in 2025.

By end-use industry, the healthcare segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us