Fixed-Wing Turbine Aircraft Market Size, Share & Industry Analysis, By Propulsion Type (Turboprop, Turbojet, and Turbofan), By Aircraft Type (Business Aircraft, Regional Aircraft, Commercial Transport Aircraft, Special Mission Aircraft, Military Fixed-Wing Aircraft, and Trainer Aircraft), By Seating Capacity (Up to 9 seats, 10–19 seats, 20–50 seats, 51–150 seats, and Above 150 seats), By Weight Capacity (Light, Medium, and Heavy), By End User (Commercial airlines, Charter / Business Aviation Operators, Government Agencies, & Others), By Application and Regional Forecast, 2026-2034

Fixed-Wing Turbine Aircraft Market Size and Future Outlook

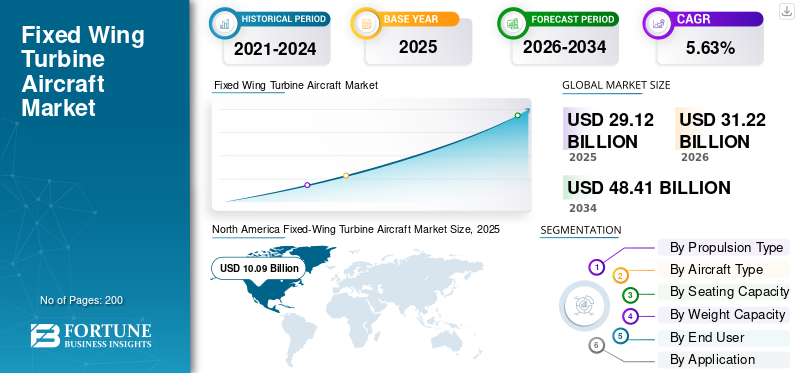

The global fixed- wing turbine aircraft market size was valued at USD 29.12 billion in 2025. The market is projected to grow from USD 31.22 billion in 2026 to USD 48.41 billion by 2034, exhibiting a CAGR of 5.63% during the forecast period. North America dominated the fixed wing turbine aircraft market with a market share of 34.64% in 2025.

Fixed wing turbine aircraft are airplanes for lift, with stationary wings, powered by turbine engines like turbofans, turbojets, or turboprops that deliver high thrust for speed and range. They encompass commercial airliners, regional jets, business jets, military fighters, transports, and cargo planes, used in passenger transport, defense operations, executive travel, and surveillance. Demand for such aircraft surges from rising air travel, military modernization, fuel-efficient designs, and sustainability pushes amid geopolitical tensions.

Leading players include Boeing, Airbus, Embraer, Textron Aviation, and Bombardier. These players have aircraft models such as 737, 777X airliners, A320neo family jets, E-Jets regional aircraft, and among others.

Download Free sample to learn more about this report.

FIXED-WING TURBINE AIRCRAFT MARKET TRENDS

Increased Focus on Sustainability is a Prominent Market Trend

Increased focus on sustainability has emerged as the defining trend in the market. Regulatory pressures from ICAO's net-zero goals and EU mandates compel airlines to adopt cleaner fuels and operations to align with global climate commitments. Passenger expectations for eco-friendly travel intensify the scrutiny on emissions, pushing aircraft manufacturers toward efficient engine designs and lighter materials. Furthermore, current geopolitical uncertainties accelerate to the demand for alternative propulsion amid rising air traffic demands.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Surging Global Air Travel Is Anticipated To Drive Market Growth

Surging global air travel is driving the fixed-wing turbine aircraft market growth as airlines expand fleets to meet rising passenger demand, fueled by economic recovery and expanding middle classes in Asia and other emerging regions. Similarly, leisure and business travel surges is boosting the requirement for international routes that prioritize efficient turbine powered jets and regional aircraft along with greater connectivity demands. Additionally, urbanization and tourism promotion globally is amplifying the route networks, compelling manufacturers to ramp-up the production.

MARKET RESTRAINTS

Stringent Safety And Environmental Regulations to Act as a Restraint in Market Growth

Stringent safety and environmental regulations act as a key market restraint for the product. As by imposing rigorous certification processes can delay new model entries and raise compliance costs for manufacturers. FAA and EASA oversight demands extensive audits, redesigns for enhanced structural integrity, and real-time monitoring systems, diverting resources from production scaling. Environmental rules under ICAO's CORSIA framework require emission tracking and greener technologies, complicating supply chains and fueling retrofits.

MARKET OPPORTUNITIES

Rapid Urbanization In Various Regions Creates New Market Growth Opportunities

Rapid urbanization across Asia, Africa, and Latin America creates fresh market growth opportunities by developing megacities and secondary urban centers that demand expanded regional air links. These population shifts pushes for the development of new travel corridors between growing hubs and spurring airlines to deploy efficient turboprops and jets for shorter routes and business connectivity. Investments in infrastructures in regional airports will enable low-cost carriers to bridge underserved areas, while economic hubs fuel cargo and executive flights.

MARKET CHALLENGES

Supply Chain Disruptions Present a Major Market Challenge to Market Growth

Supply chain disruptions present a major market challenge for fixed-wing turbine aircraft market growth, with prolonged delays in engines, titanium, and composites stemming from geopolitical tensions including Ukraine conflict and skilled labor shortages. Manufacturers face conflicting demands between new builds and legacy fleet maintenance, forcing airlines to retain older, less efficient planes longer, which inflates leasing costs and hampers sustainability goals.

Segmentation Analysis

By Propulsion Type

Optimal Performance Required in Commercial Aviation Boosts the Turbofan Segmental Growth

Based on the propulsion type, the market is segmented into turboprop, turbojet, and turbofan.

The turbofan segment is anticipated to account for the largest market share as turbofans propulsion type are best suited for long-haul, high-altitude flights. Their effectiveness reduces operating expenses and pushes for increased performance required in commercial aviation.

The turboprop propulsion type is anticipated to rise with a CAGR of 5.53% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Aircraft Type

Rise in High Net Worth Individuals (HNWIs) Propels the Dominance of Business Aircraft Segment

Based on aircraft type, the market is segmented into business aircraft, regional aircraft, commercial transport aircraft, special mission aircraft, military fixed-wing aircraft, and trainer aircraft.

In 2025, business aircraft segment dominated the global market. The demand for private jet ownership and charter services is driven by the growing number of HNWIs globally, especially in the Asia Pacific region.

The Special mission aircraft segment is projected to grow at a highest CAGR of 6.28% over the forecast period.

By Seating Capacity

Up to 9 Seats Leads Due to Their Operational Versatility and Accessibility

Based on the seating capacity, the market is segmented into up to 9 seats, 10–19 seats, 20–50 seats, 51–150 seats, and above 150 seats.

The up to 9 seats segment is anticipated to witness a dominating market share over the forecast period. The aircraft equipped with this seating capacity, such as the Beechcraft King Air, Cessna Caravan, and Pilatus PC-12, may fly from small, unpaved, or isolated airstrips that are not feasible for larger jets.

The 51–150 seats segment is projected to grow at a high CAGR of 6.38% over the forecast period.

By Weight Capacity

Optimal Operational Versatility Boosts the Medium Segment Growth

Based on weight capacity, the market is segmented into light, medium, and heavy.

The medium segment dominated due to its ability to connect regional, continental, and transcontinental routes. Medium weight aircraft are the most adaptable. Furthermore, they offer enough payload for efficiency while remaining nimble enough for numerous airports, unlike larger, constrained aircraft.

In addition, heavy are projected to grow at a high CAGR of 6.21% during the study period.

By End User

Fleet Modernization Drives the Leadership of Charter / Business Aviation Operators Segment

Based on end user, the market is segmented into commercial airlines, charter / business aviation operators, government agencies, defense forces, and special mission operators.

The Charter / business aviation operators segment dominated the fixed-wing turbine aircraft market share. The segmental growth i due to are heavy investing by the operators in fleet modernization programs for their aging fleets with newer ones, leading to more fuel-efficient models.

In addition, special mission operators are projected to grow at a high CAGR of 7.38% during the study period.

By Application

Passenger transport Segment Takes the Lead Owing to Surging Global Air Traffic

Based on application, the market is segmented into passenger transport, cargo transport

business aviation, ISR / patrol / surveillance, training, and others.

The passenger transport segment dominated the market. The growth is due to strong recovery witnessed by the global air passenger traffic, driving airlines to expand their fleets to meet demand.

In addition, ISR / patrol / surveillance is projected to grow at a high CAGR of 6.32% during the study period.

Fixed-Wing Turbine Aircraft Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Fixed-Wing Turbine Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 9.39 billion, and also maintained the leading share in 2025, with USD 10.09 billion. North America sustains leadership in the market owing to dense air traffic networks and economic stability.

U.S. Fixed-Wing Turbine Aircraft Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 6.58 billion in 2026, growing at a CAGR of 13.37%. The country powers regional dominance with vast commercial operations and defense spending.

Europe

Europe is projected to record a steady growth rate of 9.07% during the forecast period, which is the second highest among all regions, and anticipates to reach a valuation of USD 6.59 billion by 2026. Europe prioritizes integrated airspace under EASA's 2026 safety plan, emphasizing drone integration and fatigue risk tools for turbine fleets.

U.K. Fixed-Wing Turbine Aircraft Market

The U.K. market in 2026 is estimated around USD 2.23 billion, growing roughly at a CAGR of 9.51% during the study period. The U.K. navigates through its market with renewed emphasis on sovereignty and global reach following Brexit, leveraging strong transatlantic ties and domestic manufacturing.

Germany Fixed-Wing Turbine Aircraft Market

Germany’s market is projected to reach approximately USD 1.80 billion in 2026. Germany powers its market via engineering excellence and central positioning. For instance, MTU Aero Engines in Munich advances geared turbofan modules that reduce noise footprints for urban-adjacent operations.

Asia Pacific

Asia Pacific region is estimated to reach USD 9.48 billion in 2026 and secure the position of the third-largest region in the market and also to be the fastest growing region during the study period. Asia Pacific surges via its rapidly expanding Pacific routes, infrastructure, and demographics.

Japan Fixed-Wing Turbine Aircraft Market

The Japan market in 2026 is estimated to touch USD 1.72 billion, growing at a 9.10% CAGR during the forecast period. Japan sustains fixed-wing turbine aircraft stability amid demographic headwinds through precision engineering which is focused on efficient maritime and regional platforms.

China Fixed-Wing Turbine Aircraft Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 3.30 billion. China accelerates in self-reliance amid Belt connectivity, scaling domestic jets despite Pacific lags.

India Fixed-Wing Turbine Aircraft Market

The India market in 2026 is estimated at around USD 2.53 billion. India’s market expansion is characterized by atmanirbhar defense push and soaring domestic carriers that bridge the gap between the subcontinent extension projects and strengthen the market growth.

Rest of the World

The rest of the world include Middle East and Africa and Latin America. Latin America, Middle East, Africa sees turbine opportunities via leisure surges, transit hubs, and resource logistics The Middle East & Africa and Latin America market is set to reach a valuation of USD 2.73 billion and USD 1.66 billion, respectively in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Fleet Modernization and Digital Integration By Key Market Players Drives the Competition Edge

The fixed-wing turbine aircraft market displays a consolidating competitive landscape dominated by industry leaders including Boeing, Airbus, Lockheed Martin, Embraer, Textron Aviation, Dassault Aviation, BAE Systems, and COMAC, which collectively shape production pipelines through extensive commercial-defense manufacturing bases and global supply alliances.

These leaders cement their market positions via fleet modernization initiatives paired with digital integration breakthroughs including AI analytics and sensor fusion that mirror edge computing advances. From Washington hubs, Boeing upgrades its 737/777X fleets with real-time data relays for predictive maintenance.

LIST OF KEY FIXED-WING TURBINE AIRCRAFT COMPANIES PROFILED

- Boeing (U.S.)

- Airbus (France)

- Lockheed Martin Corporation (U.S.)

- Embraer (Brazil)

- Textron Aviation (U.S.)

- Dassault Aviation (France)

- BAE Systems (U.K.)

- COMAC (China)

- Bombardier (Canada)

- Gulfstream (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: A USD 1.34 billion contract has been awarded for New Medium Helicopters (NMH) has been announced by the UK Ministry of Defence (MoD). Leonardo will produce and deliver 23 of Yeovil's most recent AW149s as part of the agreement, enhancing the capability of the UK Armed Forces.

- March 2025: Boeing wins a USD 101 million Navy contract to update fleet components for the F/A-18 and EA-18G. This order calls for the manufacturing and delivery of 96 Trailing Edge Flap Retrofit Redesign shipsets, comprising 96 left-hand and right-hand TEFs, to be retrofitted into F/A-18E/F and EA-18G aircraft.

- November 2024: At a ceremony at Bombardier Group's U.S. headquarters in Wichita, Kansas, Bombardier Defense delivered the first Bombardier Global 6500 aircraft in support of the US Army's High Accuracy Detection and Exploitation System (HADES) program.

- March 2024: The Boeing Company was given a USD 1.3 billion contract by the U.S. Navy to buy 17 F/A-18 Super Hornets and provide a technical data package that is essential to the platform's survival.

- March 2023: An Airbus A330 Multi-Role Tanker Transport (MRTT) has been ordered by the NATO Support and Procurement Agency (NSPA), after this contract the total number of the Multinational MRTT Fleet (MMF) is 10 aircrafts.

REPORT COVERAGE

The global fixed-wing turbine aircraft industry analysis includes a comprehensive study table of contents of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aerospace and defense industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.63% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Propulsion Type, Aircraft Type, Seating Capacity, Weight Capacity, End User, Application and Region |

| By Propulsion Type |

|

| By Aircraft Type |

|

| By Seating Capacity |

|

| By Weight Capacity |

|

| By End User |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 29.12 billion in 2025 and is projected to reach USD 48.41 billion by 2034.

In 2025, the market value stood at USD 10.09 billion.

The market is expected to exhibit a CAGR of 5.63% during the forecast period.

By propulsion type, the turbofan segment is expected to dominate the market.

Surging global air travel is anticipated to drive market growth.

Boeing, Airbus, Lockheed Martin, Embraer, Textron Aviation, Dassault Aviation, and BAE Systems are few key players in the market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us