Flat Antenna Market Size, Share & Industry Analysis, By Installation Type (Indoor / Window-Mounted, Outdoor Fixed, Vehicular / Mobile, Shipborne, Airborne, & Ruggedized Tactical), By Technology (Electronically Steerable, Passive Fixed, and Integrated Flat-Panel Antenna, Backhaul Systems, & Others), By Frequency Band (Sub-6 GHz, mmWave (24-100 GHz), & Others), By Application (Fixed Wireless Access, mmWave Backhaul, Satellite Land Fixed, Maritime Connectivity, & Others), By End User (Telecom Operators / ISPs, Government & Defense, Commercial Aviation, & Others), and Regional Forecast, 2026-2034

Flat Antenna Market Size & Future Outlook

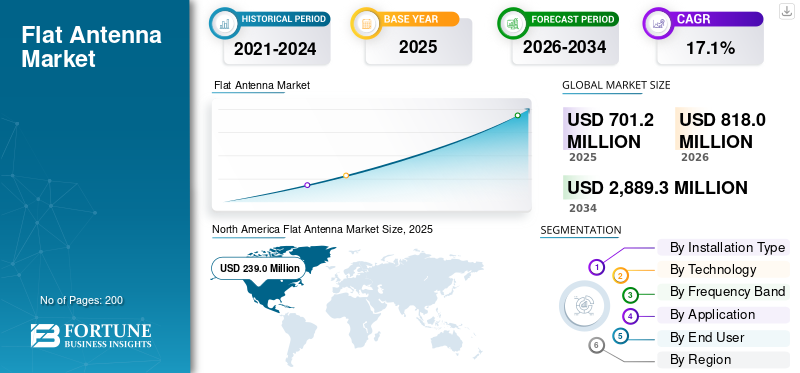

The flat antenna market size was valued at USD 701.2 million in 2025. The market is projected to grow from USD 818.0 million in 2026 to USD 2,889.3 million by 2034, exhibiting a CAGR of 17.1% during the forecast period. North America dominated the flat antenna market with a market share of 34.08% in 2025.

The global flat antenna market includes low-profile, flat-form antenna hardware and integrated terminal systems used in fixed wireless access, backhaul, satellite connectivity, aviation, maritime, and defense applications. The market is growing as operators and end users require higher bandwidth in a smaller, lighter, and easier-to-install format than traditional antenna systems. Demand is rising due to the expansion of 5G fixed wireless and mmWave backhaul, as well as the increasing use of electronically steerable satellite terminals for mobility and remote connectivity.

Key companies are shaping the market by actively expanding the use cases for flat antennas. Intellian and Hughes are enhancing the satellite terminal segment with LEO-focused flat-panel deployments. Kymeta is promoting adoption in defense and mobile connectivity. Meanwhile, companies such as Gapwaves and Ceragon are increasing demand for flat antennas in 5G and transport backhaul, moving the market from niche trials to wider commercial deployment.

Download Free sample to learn more about this report.

Flat Antenna Market Key Takeaways

- 2025 Market Size: USD 701.2 million

- 2026 Market Size: USD 818.0 million

- 2034 Forecast Market Size: USD 2,889.3 million

- CAGR: 17.1% from 2026–2034

- North America dominated the flat antenna market with a 34.08% share in 2025.

- The airborne segment is projected to grow at a 20.3% CAGR during the forecast period.

- The integrated radio & flat-panel backhaul nodes segment is projected to grow at a 19.8% CAGR during the forecast period.

North America

Led the market with a 34.08% share in 2025.

Europe

Held the third-largest market and is projected to grow at a 15.8% CAGR.

Asia Pacific

The second-largest market, projected to grow at a 19.7% CAGR.

U.S

The market was valued at USD 216.0 million in 2025.

Japan

The market was valued at USD 28.2 million in 2025.

Read More

FLAT ANTENNA MARKET TRENDS

Shift Toward Electronically Steerable Flat-Panel Antennas is Driving Market Growth

One of the major trends in the market is the shift from bulkier, mechanically steered systems to electronically steerable flat-panel antennas designed for LEO and multi-orbit connectivity. This trend is attributed to operators’ need for lighter, lower-profile antenna systems that provide high speed links across land mobility, maritime, enterprise, and aviation use cases without the complexity of moving parts. This trend is noticeable in commercial product launches and network approvals.

In March 2025, Intellian and Eutelsat Group announced that Intellian’s new Enterprise Flat Panels had become commercially available on Eutelsat’s OneWeb LEO network, covering land fixed, land mobility, and maritime applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth of LEO Satellite Networks and Communication Systems Focused on Mobility Drives Market Growth

The rapid development of LEO satellites and the increasing demand for high speed communication systems in aviation, land mobile, enterprise, and remote connectivity are fueling market growth. Traditional antenna systems are less suitable to this shift, as operators require low-profile hardware that is easier to install, lighter, and more suitable for mobile platforms. As a result, demand for flat panel antennas is growing, as they align better with the new satellite network structure than older mechanically steered models.

In March 2025, United Airlines installed Starlink on its first regional aircraft. They expected to outfit 40+ regional aircraft each month through the end of 2025, highlighting the equipment’s smaller size, lower weight, and faster installation compared with non-Starlink equipment.

MARKET RESTRAINTS

Lengthy Certification and Network-Approval Cycles Restrain the Market Growth

The primary market limitations are that commercialization relies not just on launching a product. Many flat-panel antenna systems, especially those linked to satellite communication systems, require operator validation, network approval, integration testing, and field qualification before commercialization. This process slows down revenue generation, lengthens product timelines, and increases development costs for vendors seeking to enter or grow in the market. In a market where high speed performance, multi-orbit compatibility, and reliability are important, approval cycles can create significant delays, hindering flat antenna market growth.

MARKET OPPORTUNITIES

Expansion of 5G Fixed Wireless Access and mmWave Backhaul is Creating a Strong Commercial Opportunity

A major market opportunity goes beyond satellite alone. As operators expand fixed wireless access and improve communication systems for higher-capacity backhaul, the use case for flat antennas becomes much broader. Low-profile antenna systems are increasingly suitable for outdoor customer equipment, dense urban transport links, and network extension in areas where fiber is limited or costly. This creates a market opportunity for flat antenna vendors, especially as demand shifts toward compact hardware that can support high speed links without the size of traditional antenna systems.

MARKET CHALLENGES

Scaling Production and Building a Stable Supply Chain Remains a Major Challenge

Flat-panel antenna systems, especially electronically steerable designs for high speed communication systems, depend on complex RF architectures, specialized components, and a supply chain that is less developed than that of traditional antenna products. This situation makes it harder to ramp up production, raises cost pressure, and increases the risk that even technically strong companies will struggle to turn product innovation into consistent market growth.

Impact of the Current War

Ongoing Warfare Across Multiple Regions is Increasing Demand for Secure, Mobile, and Resilient Flat Antenna Systems

The impact of current warfare on the market is expected to be broader than the Russia-Ukraine war alone. The market is also influenced by spillover effects from conflicts between the U.S. & Israel vs. Iran, as well as by military demands in the Middle East and other contested areas. In these regions, governments are focusing on faster, more reliable communication systems for land, air, sea, and tactical mobility. This change directly drives the adoption of flat antennas. These systems are compact, easier to set up, and better at ensuring secure satellite network access in changing environments. SIPRI reported that global military spending reached USD 2.718 trillion in 2024, marking the largest annual increase since the end of the Cold War, with particularly rapid growth in Europe and the Middle East. IISS also mentioned that The Military Balance 2025 addresses both Russia’s ongoing invasion of Ukraine and the Houthis’ use of ballistic and cruise missiles. This highlights how various active conflict zones are now affecting defense purchasing and operational planning.

Segmentation Analysis

By Installation Type

Outdoor Fixed Segment Dominates the Market Due to Strong Fixed Wireless and Backhaul Demand

In terms of installation type, the market is categorized into indoor / window-mounted, outdoor fixed, vehicular / mobile, shipborne, airborne, and ruggedized tactical.

Outdoor fixed segment leads the market, as it focuses on the biggest commercial applications, especially broadband access, telecom backhaul, and fixed-site communication systems, due to which operators often choose outdoor fixed antenna systems for deployments. They can be installed on walls, poles, rooftops, and building exteriors. This setup provides more stable high-speed performance compared to indoor options, particularly in areas where fiber is limited or expensive.

Airborne segment is expected to grow at a CAGR of 20.3% over the forecast period.

By Technology

Passive Fixed Flat-Panel Antennas Segment Dominates Due to Lower Cost and Wider Fit in Fixed Broadband Deployments

On the basis of technology, the market is classified into electronically steerable flat-panel antennas, passive fixed flat-panel antennas, integrated radio & flat-panel backhaul nodes, integrated terminal & flat-panel antenna systems, and others.

Passive fixed flat-panel antennas segment holds the largest flat antenna market share, as they fit well with the volume side. In fixed wireless access, outdoor broadband links, and site-based communication systems, operators often choose antenna solutions that are simpler, easier to install, and cheaper than electronically steered platforms. Most deployments still happen in fixed locations, rather than in high-end mobility cases. As a result, passive fixed designs continue to dominate the market by offering scale, practicality, and a more favorable cost profile for broadband expansion.

Integrated radio & flat-panel backhaul nodes segment is expected to grow at a CAGR of 19.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Frequency Band

Sub-6 GHz Segment Dominates the Market Due to Wider Network Coverage and Easier Large-Scale Deployment

Based on frequency band, the market is segmented into, Sub-6 GHz, mmWave (24-100 GHz), Ku-band, Ka-band, and Others.

Sub-6 GHz leads the market as it provides a practical balance of coverage, capacity, and cost. In broadband access and fixed-site communication systems, operators need antennas that can cover larger geographic areas and perform well in urban, suburban, and rural settings without the stricter range limits of mmWave. This makes Sub-6 GHz the most popular frequency band apart from Ku-, K- and Ka Band in the market. Additionally, operators are expanding fixed wireless access, outdoor receivers, and standard flat-panel antenna systems rather than focusing solely on premium mobility or high-frequency niche setups, thereby achieving segment dominance.

The mmWave (24-100 GHz) segment is the fastest growing, expected to grow at a CAGR of 20.2% over the forecast period.

By Application

Fixed Wireless Access (FWA) Segment Dominates Due to Wider Expansion of Broadband

Based on application, the market is segmented into Fixed Wireless Access (FWA), mmWave backhaul / transport, satellite land fixed and land mobility, maritime connectivity, airborne connectivity, and others.

Fixed Wireless Access (FWA) segment leads the market, as it is the strongest volume use case for mainstream broadband deployment. Operators are using FWA to deliver high-speed connectivity faster than fiber in many urban, suburban, and rural areas. This keeps the demand high for compact outdoor and fixed flat-panel antenna systems. Additionally, compared to airborne, maritime, or purely tactical applications, FWA has a wider commercial base, more consistent deployment costs, and a bigger role in everyday communication systems.

Airborne connectivity is the fastest growing segment in the market set to grow at a CAGR of 20.9% over the forecast period.

By End User

Telecom Operators / ISPs Segment Dominates Due to Large-Scale Network Rollouts and Recurring Broadband Demand

Based on end user, the market is segmented into telecom operators / ISPs, government & defense, commercial aviation, and others.

Telecom operators/ ISPs hold the largest market share, as they are the main buyers of flat antenna hardware for fixed wireless access, backhaul, and outdoor broadband communication systems. Unlike aviation, maritime, or defense users, operators deploy antenna systems in much larger volumes with more consistent rollout cycles. Additionally, they need to expand high-speed coverage faster than fiber. As a result, this group of end users holds the largest commercial base and maintains a lead over other segments in overall market value.

Commercial aviation segment is expected to grow at a CAGR of 21.1% during the forecast period.

Flat Antenna Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world (Middle East & Africa, and Latin America).

North America

North America Flat Antenna Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held 34.08% of the market share in 2025, as it combines two of the industry’s biggest revenue engines: large-scale fixed wireless access deployment and the faster adoption of advanced satellite-based communication systems. Additionally, the region has a stronger mix of operator-led broadband expansion, premium enterprise connectivity, aviation upgrades, and early use of flat-panel antenna systems for high-speed applications than most other regions, resulting in region dominance.

U.S. Flat Antenna Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 216.0 million in 2025, growing at a CAGR of 15.2% during the forecast period.

Europe

Europe held the third largest market share in 2025 and is anticipated to grow at a CAGR of 15.8% during the forecast period. The regional growth is propelled by a combination of fixed wireless expansion, satellite-linked enterprise connectivity, aviation upgrades, and defense demand for reliable communication systems. Additionally, on the telecom side, the market continues to benefit from the ongoing 5G rollout, with Europe’s mid-band 5G coverage exceeding 50% of the population by the end of 2024. Meanwhile, the satellite side is gaining importance as flat-panel terminals are increasingly used in land fixed, land mobility, maritime, and government applications. Moreover, Europe also has a stronger focus on security than many other regions. This is important as increased defense spending usually supports low-profile, mobile, and quickly deployable antenna systems.

France Flat Antenna Market

France market reached approximately USD 24.5 million in 2025, equivalent to around 14.93% of industry revenues.

Germany Flat Antenna Market

The Germany’s market reached USD 30.3 million in 2025, representing roughly 18.44% of global revenues.

Asia Pacific

Asia Pacific is the second largest market and is anticipated to grow at a CAGR of 19.7% over the forecast period. The region leads the market in volume growth as it combines extensive telecom infrastructure development with various country-level demand patterns. Japan, South Korea, and Australia are further along in 5G. Others are still working to expand broadband access and improve network quality. This makes the region crucial for flat antennas used in fixed wireless access, backhaul, and new satellite-linked communication systems.

In August 2024, the GSA reported that Asia Pacific made up 35% of 2024 FWA CPE shipments, signaling strong demand for flat-panel and outdoor fixed antennas. Additionally, the GSMA expects 5G to represent 50% of the region’s mobile connections by 2030.

China Flat Antenna Market

China’s market is expected to be one of the largest in the Asia Pacific, with 2025 revenues valued at around USD 64.9 million, representing roughly 33.76% of global sales.

Japan Flat Antenna Market

The Japanese market in 2025 was valued at USD 28.2 million, accounting for roughly 14.68% of global revenues.

Rest of the World

The rest of the world (Middle East & Africa and Latin America) has a comparatively smaller share and is growing at a CAGR of 18.0% during the forecast period. Demand in this region comes from real connectivity gaps, remote operations, aviation, offshore activities, and government-led communication systems. Latin America focuses more on access, emphasizing broadband extension and rural connectivity. In contrast, the Middle East & Africa tend to have a more premium market in some areas due to satellite reliance, mobility needs, aviation, and defense spending. In September 2025, GSA reported that the Middle East & Africa made up 30% of 2024 FWA CPE shipments. This indicates that the market for flat-panel broadband hardware is significant in these regions.

Latin America Flat Antenna Market

The Latin American market was estimated at around USD 43.4 million, accounting for roughly 41.08% of the rest of the world’s revenues, in 2025.

Middle East & Africa Flat Antenna Market

Middle East & Africa Flat market size was estimated at around USD 62.3 million in 2025, and is expected to reach USD 285.1 million in 2034, representing roughly 58.92% of the rest of the world’s sales in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players Are Competing on Deployment Scale, Network Approval, and Product Breadth

The competitive landscape in the flat antenna industry is now defined by more than prototypes. It is increasingly driven by companies that can deploy certified antenna systems in real-world scenarios across the enterprise, maritime, government, and mobility sectors. In March 2025, Intellian from South Korea strengthened its position by offering its Enterprise Flat Panels for sale on Eutelsat’s OneWeb LEO satellite network. Meanwhile, Hughes shipped over 5,000 electronically steerable antenna terminals for OneWeb and received commercial approval for its HL1120W terminal. The market favors vendors that can provide reliable, high-speed flat-panel hardware at a commercial scale rather than merely demonstrating technical ability.

Kymeta Corporation is making a stronger push into land mobile and defense applications with the Goshawk u8. SWISSto12 reinforced its position in advanced satellite hardware by acquiring key assets and intellectual property from Hanwha Phasor, including Ku-band electronically steered technology. This indicates that a small group of key players is shaping the market based on their strengths, focus on mobility and government needs, and others concentrate on the scale of LEO terminals or broader antenna-system integration. As demand for flat panel antennas increases, particularly in North America and other high-value markets, demand is increasingly linked to effective execution, certification, and the ability to manage a scalable supply chain.

LIST OF KEY FLAT ANTENNA COMPANIES PROFILED

- Kymeta Corporation (U.S.)

- Hughes Network Systems, LLC (U.S.)

- ThinKom Solutions, Inc. (U.S.)

- Intellian Technologies, Inc. (South Korea)

- Viasat, Inc. (U.S.)

- Ceragon Networks Ltd. (Israel)

- Gapwaves AB (Sweden)

- SWISSto12 SA (Switzerland)

- SPACE (U.K.)

- Get SAT Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- September 2025: SWISSto12 acquired key assets and intellectual property from Hanwha Phasor, including Ku-band active electronically steered antenna technology. This was an important competitive move as it brought advanced flat-panel capabilities into another active player in satellite communications.

- April 2025: Hughes announced the global commercial availability of its HL1100W single-panel electronically steerable antenna. This expanded its OneWeb user terminal family with a more compact flat-panel option.

- March 2025: United Airlines installed Starlink on its first regional aircraft. The company expects to equip over 40 regional aircraft per month for the rest of 2025. This development is important for the aviation sector as it reflects faster large-scale adoption of low-profile satellite antenna systems in commercial fleets.

- March 2025: Intellian and Eutelsat Group announced that Intellian’s new Enterprise Flat Panels were available on Eutelsat’s OneWeb LEO network.

- August 2024: Hughes shipped over 5,000 HL1120W electronically steerable antenna terminals for the OneWeb LEO network. This milestone indicates that flat-panel satellite terminals are moving beyond limited trials and into real commercial use.

- July 2024: Ceragon Networks announced a multi-million-dollar order from a major American ISP to deliver nearly 1,000 new E-Band links in 2024.

- April 2024: Hughes announced the commercial availability of its HL1120W terminal after receiving Eutelsat OneWeb approval for use on the OneWeb LEO network. This was a big step since it transitioned a flat-panel ESA terminal from product development to approved commercial deployment.

- February 2024: Nokia launched a new 5G mmWave outdoor fixed wireless access receiver. This device aims to improve broadband coverage in urban, suburban, and rural areas. The release is important because it highlights the growing importance of flat-form outdoor antenna systems for broadband access and backhaul.

REPORT COVERAGE

The global flat antenna market analysis provides an in-depth study of market size, Porter’s Five Forces analysis, company profiling and forecast for all the market segments included in the report. It includes details on the market outlook and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.1% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation

|

By Installation Type

|

|

By Technology

|

|

|

By Frequency Band

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 818.0 million in 2026 and is projected to reach USD 2,889.3 million by 2034.

In 2025, the North American market value stood at USD 239.0 million.

The market is expected to exhibit a CAGR of 17.1% during the forecast period of 2026-2034.

Outdoor fixed segment is leading the market by installation type.

Growth of LEO satellite networks and communication systems focused on mobility are the key factors driving the market.

Key players in the market include Kymeta Corporation, Hughes Network Systems, Intellian Technologies, ThinKom Solutions, Viasat, Ceragon Networks, and SWISSto12.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us