Fortified Foods Market Size, Share & Industry Analysis, By Product Type (Bakery & Confectionery [Bread & Baked Products, Cakes & Pastries, Cookies & Biscuits, and Confectioneries], Dairy and Dairy Alternatives, Infant Formula, & Others ), By Nutritional Type (Vitamins, Minerals, Protein, Dietary Fibers, Probiotics, & Others), By End-Use (Infants, Children, Adults & Geriatric), By Application (Bone Health, Immunity, Digestive Health, General Health, Cognitive Health, & Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, & Others) and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

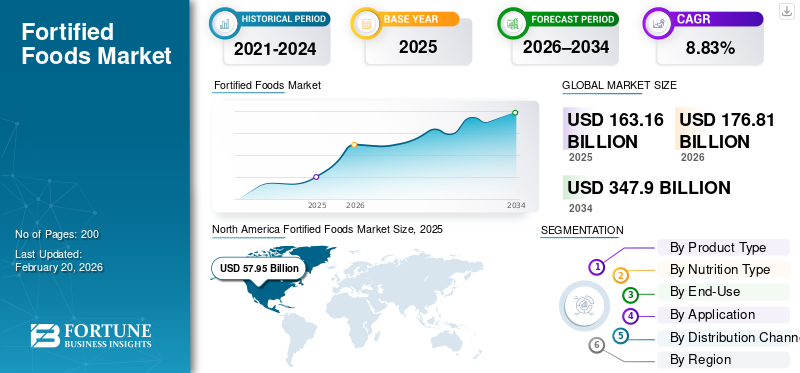

Fortified Foods Market Size and Future Outlook

The global fortified foods market size was valued at USD 163.16 billion in 2025. The market is projected to grow from USD 176.81 billion in 2026 to USD 347.90 billion by 2034, exhibiting a CAGR of 8.83% during the forecast period. North America dominated the fortified foods market with a market share of 35.51% in 2025.

Fortified Foods include naturally derived colors, flavors, sweeteners, starches, flours, malts, and functional ingredients that are minimally processed and free from risks associated with artificial additives. These ingredients are widely used across food & beverages, bakery & confectionery, dairy, snacks & cereals, prepared meals, meat & seafood alternatives, dietary supplements, and animal feed. Dietary habits are shifting toward more plant-forward meals, influenced by environmental and wellness trends worldwide. Therefore, plant-based protein sources such as lentils and quinoa are gaining traction as sustainable alternatives compared to animal proteins in the global market.

The market is dominated by Nestlé S.A., Danone S.A., Kellogg Company, General Mills, Inc., Unilever PLC, and others.

Download Free sample to learn more about this report.

Fortified Foods Market Takeaways

- 2025 Market Size: USD 163.16 billion

- 2026 Market Size: USD 176.81 billion

- 2034 Forecast Market Size: USD 347.90 billion

- CAGR: 8.83% from 2026–2034

- North America dominated the fortified foods market with a 35.51% share in 2025.

- The bakery & confectionery segment led the market with USD 45.72 billion in revenue in 2025.

- The beverages segment is projected to grow at the fastest CAGR of 10.52% during the forecast period.

North America

North America led the global market in 2025, generating USD 57.95 billion and benefiting from strong consumer awareness of nutrition and fortified food products.

Europe

Europe reached USD 45.23 billion in 2025, supported by public health initiatives and widespread adoption of fortified dairy and bakery products.

Asia Pacific

Asia Pacific accounted for USD 35.64 billion in 2025 and is the fastest-growing region, registering a CAGR of 9.73% through 2034.

U.S.

The market was valued at approximately USD 41.81 billion in 2025 and is expected to expand at a CAGR of 8.68% during the forecast period.

Japan

Demand for fortified foods is rising due to an aging population, increasing health awareness, and growing preference for functional and nutrient-enriched food products.

Read More

Fortified Foods Market Trends

Rising Focus on Preventive Nutrition and Micronutrient Sufficiency to Shape Market Growth

The fortified foods market is undergoing structural transformation as governments, health organizations, and food manufacturers increasingly prioritize preventive nutrition to reduce the long-term burden of non-communicable diseases and micronutrient deficiencies. Health conscious consumers are actively seeking foods that deliver functional health benefits beyond basic nutrition, accelerating the adoption of vitamin- and mineral-fortified staples, beverages, and dairy products.

- According to the Food and Agriculture Organization (FAO), over 2 billion people globally suffer from micronutrient deficiencies, particularly iron, iodine, vitamin A, and zinc, reinforcing the importance of large-scale food fortification programs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Government-Led Fortification Programs to Drive Market Growth

Government-backed food fortification initiatives are a primary growth driver for the fortified foods market, particularly in the Asia Pacific, Africa, and Latin America. Mandatory fortification of wheat flour, edible oils, milk, convenience foods, and infant foods has significantly expanded the market for fortified food products.

- According to the Food Fortification Initiative and the World Health Organization, more than 140 countries currently have some form of mandatory fortification for staple foods (such as flour, oil, or salt), with over 90 countries specifically mandating the fortification of wheat flour.

Market Restraints

Higher Production Costs and Nutrient Stability Challenges to Limit Market Expansion

The global fortified foods market growth is due to rising consumer health consciousness and policies aimed at reducing micronutrient deficiencies; nevertheless, higher production costs and essential nutrient stability issues remain significant barriers to deeper market penetration. Fortifying staple foods and processed products with micronutrients (e.g., vitamins and minerals) requires additional inputs and processes, specialized fortificants, tailored equipment for homogeneous nutrient dispersion, and quality control mechanisms, all of which increase manufacturing costs and often raise retail prices. These costs are typically passed on to consumers, making fortified products less affordable, particularly in low- and middle-income regions where purchasing power is limited, and diets prioritize basic calories over enriched products.

Market Opportunities

Rising Demand for Fortified Foods Targeting Maternal and Child Nutrition to Unlock New Growth Avenues

Maternal and child nutrition represents a structurally attractive opportunity segment as governments, NGOs, and healthcare systems prioritize early-life nutrition to improve long-term health outcomes. Fortified foods enriched with iron, folic acid, iodine, calcium, and DHA are increasingly integrated into school feeding programs, prenatal nutrition schemes, and public distribution systems. This creates sustained demand for fortified staples, dairy products, and infant foods, particularly in high-birth-rate regions.

- According to UNICEF and the Food and Agriculture Organization study in 2022, nearly 45 million children under five are wasted globally, reinforcing the urgency of fortified nutrition interventions.

SEGMENTATION ANALYSIS

By Product Type

Bakery & Confectionery Segment Dominates Owing to Widespread Consumption

On the basis of product type, the global market is segmented into bakery & confectionery, dairy & dairy alternatives, infant formula, beverages, processed foods, and others.

The bakery & confectionery segment dominated the market in 2025, valued at USD 45.72 billion, supported by widespread consumption of fortified bread, cereals, cookies, and baked snacks enriched with essential vitamins and minerals. Strong government-mandated enrichment programs and high penetration across retail channels continue to reinforce segment leadership.

Fortified dairy products, such as vitamin-enriched milk and yogurt, play a key role in addressing nutritional gaps in emerging markets.

The beverages segment is projected to grow at the fastest CAGR of 10.52% during 2026 to 2034, fueled by rising demand for functional drinks, fortified juices, sports beverages, and ready-to-drink nutrition products targeting immunity, hydration, and energy enhancement.

To know how our report can help streamline your business, Speak to Analyst

By Nutrition Type

Vitamins Segment Led the Market due to Widespread Fortification Of Staples

Based on nutrition type, the market is segmented into vitamins, minerals, proteins, dietary fibers, probiotics, and others.

The vitamins segment led the global market in 2025, reaching USD 68.33 billion, driven by widespread fortification of staples with vitamin A, D, B-complex, and folic acid to address micronutrient deficiencies.

The protein segment is expected to grow at the fastest CAGR of 11.49%, driven by rising demand for protein-fortified foods among adults, athletes, and aging populations seeking muscle health and metabolic support.

By End-Use

Adult Segment Led due to High Consumption of Functional Foods

By end-use, the market is categorized into infants, children, adults, and geriatric.

The adult segment dominated the fortified foods market in 2025, valued at USD 72.82 billion, reflecting high consumption of fortified staples, beverages, and functional foods aimed at immunity, energy, and lifestyle disease prevention.

The geriatric segment is projected to grow at the fastest CAGR of 9.88%, driven by consumers increasing demand for calcium-, vitamin-D-, fiber-, and probiotic-fortified foods addressing bone health, digestion, and age-related nutrient absorption challenges.

By Application

Bone Health Segment Dominates due to Strong Demand For Calcium- And Vitamin-D-Fortified Foods

On the basis of application, the market is segmented into bone health, immunity, digestive health, general health, cognitive health, weight management, and others.

Bone health accounted for the largest fortified foods market share in 2025, valued at USD 44.84 billion, supported by strong demand for calcium- and vitamin-D-fortified foods across dairy, beverages, and cereals.

Immunity-focused products also gained traction post-pandemic through vitamin C, zinc, and probiotic fortification.

The weight management segment is projected to witness the fastest CAGR of 12.23%, driven by fortified low-calorie foods enriched with fiber, protein, and micronutrients targeting metabolic health and obesity prevention.

By Distribution Channel

Supermarkets/Hypermarkets Segment Dominated, Driven by Wide Product Availability

By distribution channel, the global market is segmented into supermarkets/hypermarkets, convenience stores, online retail, and others.

Supermarkets and hypermarkets dominated the market in 2025, with sales of USD 72.83 billion, owing to wide product availability, strong private-label penetration, and effective in-store nutrition labeling.

Online retail is expected to grow at the fastest CAGR of 9.80%, supported by increasing e-commerce adoption, direct-to-consumer nutrition brands, and subscription-based delivery of fortified foods.

Fortified Foods Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Fortified Foods Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market, accounting for USD 57.95 billion in 2025 and is projected to grow at a CAGR of 8.29% (2026–2034). Growth is supported by strong regulatory frameworks for food fortification, high consumer preference, and widespread adoption of functional and fortified packaged foods.

U.S. Fortified Foods Market

The U.S. fortified foods market was valued at approximately USD 41.81 billion in 2025 and is expected to expand at a CAGR of 8.68% during the forecast period. The U.S. represented the largest share, driven by mandatory enrichment of grains and rising demand for fortified beverages and snacks.

Europe

Europe was valued at USD 45.23 billion in 2025, expanding at a CAGR of 8.73%. The region benefits from strong public health policies, micronutrient deficiency prevention programs, and high penetration of fortified dairy and bakery products.

U.K. Fortified Foods Market

The U.K. accounted for approximately USD 10.99 billion in 2025, driven by folic-acid fortification initiatives and functional food demand.

Asia Pacific

Asia Pacific reached USD 35.64 billion in 2025 and is the fastest-growing region, with a CAGR of 9.73%. Rapid urbanization, rising middle-class income, and growing fortification government initiatives are key drivers.

India Fortified Foods Market

India was valued at USD 7.11 billion in 2025, driven by traditional natural ingredients usage and expanding packaged food markets.

China Fortified Foods Market

China reached USD 12.25 billion in 2025, supported by large-scale vitamin and mineral fortification in staples.

South America and the Middle East & Africa

South America accounted for USD 16.46 billion in 2025, growing at a CAGR of 9.40%. Market expansion is supported by strong agricultural raw material availability and increasing adoption of fortified staples.

The Middle East & Africa market was valued at USD 7.88 billion in 2025, expanding at a CAGR of 7.75%, driven by food security initiatives and international nutrition programs.

South Africa Fortified Foods Market

The South Africa fortified foods market was valued at approximately USD 3.16 billion in 2025 and is projected to grow at a CAGR of 8.20% during 2026-2034, driven by mandatory maize and wheat flour fortification programs.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focused on Innovation to Cater to Evolving Dietary Habits

Key players in the global fortified foods market are focused on portfolio expansion, micronutrient innovation, regulatory compliance, and strategic partnerships. Companies are investing in bioavailable nutrient forms, targeted fortification, and large-scale distribution to address global nutritional gaps. In the global market, innovations blend plant-based protein sources with fortified dairy products to cater to evolving dietary habits while prioritizing clean-label formulations.

Key Players in the Fortified Foods Market

|

Rank |

Company Name |

|

1 |

Nestlé S.A. |

|

2 |

Danone S.A. |

|

3 |

Kellogg Company |

|

4 |

General Mills, Inc. |

|

5 |

Unilever PLC |

List of Key Fortified Foods Companies Profiled

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Unilever plc (U.K.)

- General Mills, Inc. (U.S.)

- Kellogg Company (U.S.)

- Mondelez International, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- DSM-Firmenich AG (Switzerland)

- BASF SE (Germany)

- Archer Daniels Midland Company (ADM) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Millers for Nutrition, powered by TechnoServe, partnered with the Gujarat Roller Flour Millers Association (GRFMA) and Fortify Health to launch seven fortified wheat flour brands in Ahmedabad, Gujarat. The initiative, introduced via a training workshop on wheat flour fortification in late 2024, targets malnutrition and anemia in India.

- June 2025: Jindal Rice Mills launched Nourifyme, a new brand of fortified staples to combat malnutrition in India. Nourifyme offers fortified rice, fortified basmati rice, and fortified wheat atta. These staples target micronutrient deficiencies common in India.

- February 2025: ACI Pure Flour Limited, part of ACI Foods & Commodity Brands in Bangladesh, launched "ACI Pure Power Flour (Fortified Atta)" to tackle nutritional gaps in daily diets. This fortified flour is enriched with 10 essential vitamins and minerals: folic acid, zinc, calcium, iron, vitamin A, vitamin B1 (thiamine), vitamin B2 (riboflavin), vitamin B3 (niacin), vitamin B6, and vitamin B12.

- July 2023: Aashirvaad, ITC's leading atta brand, launched "Namma Chakki" in Bengaluru in June 2023 as a direct-to-consumer (D2C) platform for custom-made flours. The launch leverages ITC's wheat expertise for personalization, a growing lever in India's competitive flour market amid rising millet and fortified product demand.

- March 2021: NuShakti, a brand from DSM India under Project Mandi, launched home food fortification products in Kerala to tackle nutritional deficiencies in the region. The initiative targeted urban and rural consumers by enhancing everyday staples without changing taste or habits.

REPORT COVERAGE

The market industry report analyzes the market in depth and highlights crucial aspects such as global fortified foods market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the research report also provides insights into the global fortified foods market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.83% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Nutrition Type · Vitamins · Minerals · Protein · Dietary Fibers · Probiotics · Others |

|

|

By End-Use · Infants · Children · Adults · Geriatric |

|

|

By Application · Bone Health · Immunity · Digestive Health · General Health · Cognitive Health · Weight Management · Others |

|

|

By Distribution Channel · Supermarkets/hypermarkets · Convenience Stores · Online Retail · Others |

|

|

By Region · North America (By Product Type, Nutrition Type, End-Use, Application, Distribution Channel, and Country) • U.S. (By Distribution Channel) • Canada (By Distribution Channel) • Mexico (By Distribution Channel) · Europe (By Product Type, Nutrition Type, End-Use, Application, Distribution Channel, and Country) • Germany (By Distribution Channel) • Spain (By Distribution Channel) • Italy (By Distribution Channel) • France (By Distribution Channel) • U.K. (By Distribution Channel) • Rest of Europe (By Distribution Channel) · Asia Pacific (By Product Type, Nutrition Type, End-Use, Application, Distribution Channel, and Country) • China (By Distribution Channel) • Japan (By Distribution Channel) • India (By Distribution Channel) • Australia (By Distribution Channel) • Rest of Asia Pacific (By Distribution Channel) · South America (By Product Type, Nutrition Type, End-Use, Application, Distribution Channel, and Country) • Brazil (By Distribution Channel) • Argentina (By Distribution Channel) • Rest of South America (By Distribution Channel) · Middle East & Africa (By Product Type, Nutrition Type, End-Use, Application, Distribution Channel, and Country) • South Africa (By Distribution Channel) • UAE (By Distribution Channel) • Rest of Middle East & Africa (By Distribution Channel) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 163.16 billion in 2025 and is anticipated to reach USD 347.90 billion by 2034.

At a CAGR of 8.83%, the global market will exhibit steady growth over the forecast period.

By product type, the bakery & confectionery segment led the market.

North America held the largest market share in 2025.

Government-led fortification programs and public health policies are driving market growth.

Nestle S.A., Danone S.A., Kellogg Company, General Mills, Inc., Unilever PLC, and others are the leading companies in the market.

Rising focus on preventive nutrition and micronutrient sufficiency is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us