Frozen Snacks Market Size, Share & Industry Analysis, By Type (Veg and Non-veg), By Product Type (Meat-based, Fast Food, Bakery, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, and Online Retail), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

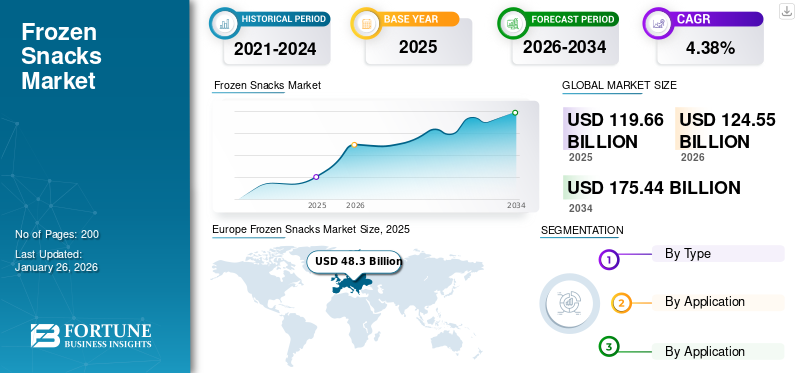

The global frozen snacks market size was valued at USD 119.66 billion in 2025. The market is projected to grow from USD 124.55 billion in 2026 to USD 175.44 billion by 2034, exhibiting a CAGR of 4.38% during the forecast period. Europe dominated the frozen snacks market with a market share of 40.36% in 2025.

Frozen snacks are popularly considered a convenience food. There is a change in the socioeconomic conditions across emerging nations, and the demand for convenient food products, including frozen appetizers and meals, is growing across the globe. Since ready-to-eat food requires less or no preparation time, the RTE format single serve and multi-serve frozen meals, breakfast alternatives, and gluten-free snack products are becoming more popular among youths staying away from home for work, students, and working women.

Furthermore, across emerging economies such as India and China, the number of nuclear families is increasing, and the shift toward packed frozen food products is high among people living in nuclear families. Working couples who do not have enough time to cook and bachelors who are less aware of cooking methods usually prefer frozen food. Key brands in the industry are positioning their products by targeting these consumer groups to strengthen their global market share. Nestle S.A., Tyson Foods, Inc., Conagra Brands, Inc., and others are major players in the global market.

- As per the research published in 2023 by the Institute of Hotel Management, Punjab, India (IHM PUSA) on millennials' consumption patterns of fresh frozen food, more than 34% of working personnel and 21% of students, purchased RTE products, generally 2 to 4 times in a week in Punjab state of India.

Download Free sample to learn more about this report.

Frozen Snacks Market Key Takeaways

- 2025 Market Size: USD 119.66 billion

- 2026 Market Size: USD 124.55 billion

- 2034 Forecast Market Size: USD 175.44 billion

- CAGR: 4.38% from 2026–2034

- Europe dominated the frozen snacks market with a 40.36% share in 2025.

- The veg segment held the largest share of the global frozen snacks market in 2024.

- The bakery segment accounted for the dominant share in 2024.

Europe

Europe reached USD 48.30 billion in 2025 and is projected to grow to USD 49.97 billion in 2026.

Asia Pacific

Asia Pacific generated USD 32.79 billion in 2025 and is expected to reach USD 34.49 billion in 2026.

North America

North America held USD 31.01 billion in 2025 and is projected to reach USD 32.18 billion in 2026.

U.S

The U.S. is expected to grow rapidly over the forecast period.

Japan is expected to witness steady demand for frozen snacks.

Read More

FROZEN SNACKS MARKET TRENDS

Rise in Popularity of Plant-Based Alternatives to Aid Market Growth

Nowadays, health-conscious consumers opt for plant-based foods driving demand for new food formats. This includes dairy-free ice creams, vegetable-based frozen meals and plant-based meat substitutes and cater to the needs of diverse dietary preferences. Moreover, plant-based frozen snacks offer a convenient and sustainable alternative appealing to consumers who prioritize taste and environmental impact. Europe witnessed a growth from USD 48.3 Billion in 2025 to USD 49.97 Billion in 2026.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Convenience Foods to Fuel Market Growth

In the past few years, the demand for frozen food, particularly frozen snacks, has grown exponentially. It is driven by changing consumer preferences with a growing inclination toward convenience and various food products. This inclination was further intensified by the pandemic, which changed the dynamics of the frozen food business and stimulated sales to new heights.

One of this market's most important driving forces is today's fast-paced lifestyles, with most individuals not having the energy or time to prepare meals from scratch. To minimize the cooking hassle, most consumers are increasingly relying on frozen snack options as they can be quickly prepared and require minimal heating before consumption.

Rising Urbanization and Growth of Working Population to Aid Market Growth

Rapid urbanization in developing regions has been reshaping food purchasing and consumer behaviors, significantly impacting the global frozen snacks market growth. As more people shift to urban areas, the demand for quality, convenience, and durable food products is rising. These changes fuel the need for food options that can be quickly prepared and stored for longer, making frozen foods an attractive option for consumers. Furthermore, urban residents are increasingly exposed to Western and diverse culinary influences, leading to wide-ranging acceptance of international frozen foods. This influence is particularly seen among millennials and consumers seeking affordable, quick meal options that fit their hectic schedules.

MARKET RESTRAINTS

Lack of Proper Cold Chain Infrastructure to Hamper Market Growth

The lack of proper cold chain infrastructure poses a significant challenge to the frozen snacks industry. Cold chain logistics involves transportation, temperature-controlled distribution, and storage facilities, which are necessary to maintain frozen product safety. However, in many developing countries such as India, South Africa, and others, the underdeveloped or unavailability of components of the supply chain can limit the distribution of frozen food items. Moreover, the low adoption rate of advanced technology can impact broken or underutilized cold chains, leading to losses for manufacturers and operators. Furthermore, the untimely failure of trucks and the unavailability of well-functioning cold storage further act as a barrier in the frozen food business.

MARKET OPPORTUNITIES

Rising Number of Cloud Kitchens Accelerates Usage of Frozen Snacks to Pave Growth Prospects

Cloud kitchens, also known as virtual kitchens, are gaining massive popularity across the globe, which can drive the consumption of frozen snack products. By incorporating frozen items in their operations, these virtual kitchens can optimize their process and curtail the need for huge kitchen space. Also, its use can further improve efficiency, thus allowing ghost kitchens to save time and offer high-quality products. Some famous frozen products in cloud kitchens include frozen gravies, French fries, chicken nuggets, pizza, and others. Thus, such products can be quickly cooked, thawed, and stored, making them suitable for cloud kitchens.

Segmentation Analysis

By Type

Veg Segment Dominated Market Due to Its Wide Availability

Based on type, the global market is divided into veg and non-veg.

The veg segment held the largest global frozen snacks market share in 2024. Consumers are still very uncertain about the quality of frozen processed non-veg food. Hence, they mainly choose vegetarian items when choosing frozen food. Pizza, fries, and nuts are some of the major product categories consumers prefer in the vegetarian food category.

The non-veg segment is expected to grow with the highest CAGR over the forecast period. The inclination of consumers toward non-veg frozen foods is mainly due to the technological innovation that is being adopted in the food industry, which keeps the food quality intact for a longer time and increases the shelf life of the food items.

By Product Type

Bakery Segment Dominated Market Due to Its Popularity among Consumers

Based on product type, the global market is divided into meat-based, fast food, bakery, and others.

The bakery segment held the dominant share in 2024, mainly due to the widespread options available in the frozen bakery products category. Breads, cookies, doughs, pastries, cakes, and rolls are some of consumers' most popular frozen items. The longer shelf life of frozen bakery items is why consumers are inclined toward this category. Hence, this category will dominate the market over the forecast period.

The meat-based category is expected to grow with the highest CAGR over the forecast period, mainly due to the innovation in the meat, beef, seafood, and chicken-based frozen snacks categories. Products such as chicken nuggets, chicken patties, and raw frozen chicken are being launched rapidly by the players to reach a wider consumer base and capture greater market share.

By Distribution Channel

Easy Accessibility and Wide Variety of Products to Drive Supermarket/Hypermarkets Segment Growth

Based on distribution channel, the market is classified into supermarkets/hypermarkets, specialty stores, convenience stores, and online retail.

The supermarkets/hypermarkets segment emerged as the leading channel in offering a variety of frozen snacks to consumers. This channel is recognized as a “one-stop shop” which offers premium quality products at a competitive price and with convenience. Other significant benefits include easy accessibility of goods under a roof, which saves buyers a lot of effort and time. Also, the consumers have several options for a particular product, which eases the consumer’s purchasing decision.

The online retail channel is expected to witness the fastest growth in the global market. One of the key advantages of online retail is its extensive global reach to consumers. Unlike any physical store, which is bounded by geographical constraints, an e-commerce channel

allows businesses to connect with consumers in any corner of the world. Also, the online sales of products, mainly frozen foods, spiked during the pandemic due to the restrictions on movement. According to the Food Industry Association and the American Frozen Food Institute, an association, U.S. sales of frozen foods grew by 21% in 2020.

Frozen Snacks Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Frozen Snacks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in Europe reached USD 48.3 billion in 2025, representing 40.36% of total market revenue, and is projected to reach USD 49.97 billion in 2026. Globally, Europe emerged as the leading market for the frozen snack sector, chiefly driven by the growing hectic lifestyles and rising desire for wholesome food that is tasty, easy to cook, and affordable. Manufacturers of frozen food products are increasingly launching new products with innovative flavors and healthy ingredients to cater to the rising demand for frozen food products in the region. Therefore, combining frozen foods with active health benefits has boosted the demand for frozen products in European countries.

- For instance, in March 2024, Mars Inc., an American multinational manufacturer, expanded in the U.K. with the launch of trüfrü, a frozen snack food brand. The brand offers frozen snacks made using 100% natural fruit, dipped in chocolate, and the layer is chilled to lock in all the nutrition and flavor.

North America

In 2025, North America held 25.92% of the global market share, reaching a valuation of USD 31.01 billion, and is projected to grow to USD 32.18 billion in 2026. The increasing demand for frozen snacks in North America can be attributed to various factors, such as changing consumer demand patterns, evolving retail strategies, technological advancements, and many others. Besides, with increasingly hectic schedules, American consumers are seeking convenient meal solutions. These snacks offer a quick and easy way without compromising quality or taste. This, in turn, leads to an amplified product demand in the region.

The U.S. is the leading country in North America, and the market is expected to grow rapidly over the forecast period. Expansion of e-commerce, changing lifestyles, and busy schedules have been the major driving factors in the country.

Asia Pacific

Asia Pacific contributed approximately USD 32.79 billion to the global market in 2025, accounting for 27.40% share, and is expected to reach USD 34.49 billion in 2026. The Asia Pacific market has achieved significant growth owing to several factors, such as rising disposable income, expansion of e-commerce platforms, increasing trade among countries, and many others. Additionally, Asian food manufacturing companies are leveraging innovations in food processing and cold chain logistics to enhance product quality and extend shelf life, thus fostering market growth.

South America

The growing demand for frozen snack products in South America highlights several factors, including rising local manufacturing and innovation in food products, expansion of online sales channels, rapid internet penetration, and many others. Besides, the evolution of the middle class in South America has resulted in greater demand for various food products. Additionally, as internet access expands, more consumers in South America are turning to e-commerce platforms for their grocery shopping. This shift allows for greater convenience and accessibility to a wider variety of frozen snack food products, previously less available in traditional retail settings.

Middle East & Africa

The Middle East & Africa region captured 2.03% of the global market in 2025, generating USD 2.42 billion in revenue, and is projected to reach USD 2.53 billion in 2026. The Middle East & Africa market has experienced steady growth over the years, as the region has strongly emphasized Western food cuisine and increased the reach of food manufacturing companies through both offline and online channels. Furthermore, many tourists seek convenient snack options and various cuisines while traveling. Therefore, frozen foods, particularly ready-to-eat and ready-to-cook options, cater to this growing demand for food convenience in countries such as UAE, South Africa, and others. This preference for convenience and variety is fueling the growth of frozen snack food consumption in tourist destinations across the Middle East & Africa region.

Latin America

In 2025, Latin America generated USD 5.14 billion, contributing 4.29% to global market revenue, and is projected to grow to USD 5.38 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Partnership Strategies and Introduction of New Products by Key Companies to Strengthen Their Positions in Global Market

The global frozen snacks market is highly competitive, with companies focusing on implementing product launch/portfolio expansion, acquisition, partnership, investment, capacity expansion, and business sustainability strategies to increase their frozen food sales and strengthen their positions in the global market.

- For instance, in October 2023, Tyson Foods Inc. established a joint venturing agreement with Godrej Agrovet Ltd to increase its footprint of frozen vegetarian snacks in the Southeast Asia and Australian markets.

Nestle S.A., Tyson Foods, Inc., Conagra Brands, Inc., and others are major players in the global market. Nestle S.A. is a dominant participant due to its significant worldwide presence, diversified product portfolio, and geographical product reach. Tyson Foods, Inc. exhibited a second-leading global market share in 2024. Its considerable share is attributed to its robust brand image in the U.S. retail market. Conagra Brands, Inc. exhibited a third-leading global market share in 2024. The considerable share can be attributed to its diverse base of partnered restaurants and grocery retailing firms that support the sale of frozen food products worldwide.

LIST OF KEY FROZEN SNACK COMPANIES PROFILED

- FRoSTA AG (Germany)

- Conagra Brands, Inc. (U.S.)

- Kellanova (The Kellogg) (U.S.)

- Nestlé S.A. (Switzerland)

- Lantmännen Unibake International (Denmark)

- The Kraft Heinz Company (U.S.)

- Unilever Plc. (U.K.)

- Tyson Foods, Inc. (U.S.)

- Godrej Industries (India)

- Nomad Foods (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Newman’s Own, Inc., an American company specializing in producing food and beverage products, expanded its product offerings by adding new frozen pizza to its portfolio. The recently launched thick crust, frozen Sourdough Pizzas are made with premium ingredients and available in Uncured Pepperoni Ricotta, Meatball, and Five Cheese flavors.

- April 2024: Baskin Robbins, an American multinational ice cream manufacturer, introduced two new product formats, Doublet Bars and Ice Cream Funwich, in India. The doublet bars are available in Choco Fudge and Raspberry Vanilla variants.

- April 2024: Havmor, a Lotte Wellfood Co Ltd subsidiary, introduced a new range of ice cream products for this summer in India. The new product range includes Indian dessert-inspired ice cream flavors of Shahi Kesar, Rajwadi Kulfi, and others.

- March 2024: BigBasket, an Indian online grocery retailer, launched a new frozen foods brand, Precia. The brand offers three product categories across the country: frozen vegetables, frozen snacks, and frozen sweets.

- December 2023: Genio Della Pizza, an American frozen pizza brand, launched frozen pizzas in four different flavors such as Margherita, The Bianca, Broccoli Rabe, and Marinara.

REPORT COVERAGE

The report analysis provides the global frozen snacks market size & forecast by all the segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the prevalence of frozen snacks in key regions/countries, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. It covers the global market industry analysis, a detailed competitive landscape with information on the market share, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.38% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Product Type

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 124.55 billion in 2026 and is projected to record USD 175.44 billion by 2034.

In 2025, the market value stood at USD 119.66 billion.

The market is expected to exhibit a CAGR of 4.38% during the forecast period of 2026-2034.

The supermarkets/hypermarkets segment led the market by distribution channel.

Rising demand for convenience foods, increasing urbanization, and the growth of the working population are aiding market growth.

Nestle S.A., Tyson Foods, Inc., Conagra Brands, Inc., and others are some prominent players in the global market.

Europe dominated the frozen snacks market with a market share of 40.36% in 2025.

Entry of ethnic and international cuisine-flavored frozen items, innovation in packaging, and an increasing number of food service/quick service restaurants are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us