Full Authority Digital Engine Control Market Size, Share & Industry Analysis, By Platform (Commercial Fixed-Wing, Business & General Aviation, Military Fixed-Wing, Rotary-Wing, and Uncrewed Platforms), By Engine Type (Turbofan, Turboprop, Turboshaft, and Small Turbojet / Microturbine), By FADEC Type (Single-channel FADEC and Dual-channel FADEC), By Fit (Line-fit, Retrofit, and Aftermarket), By End User (Civil Aviation, Defense, MRO, and Airframers & Integrators), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

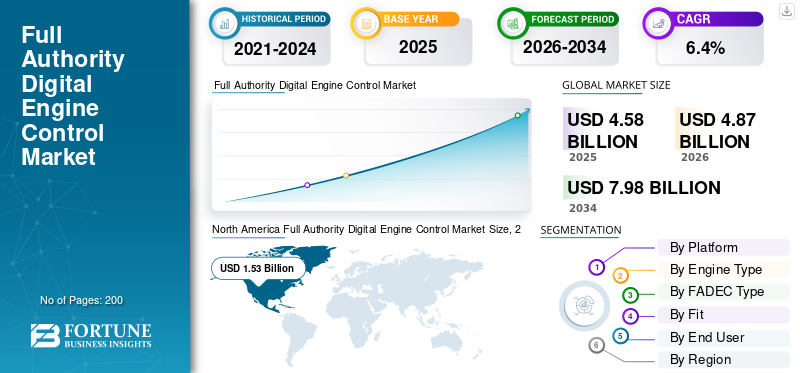

The global full authority digital engine control market size was valued at USD 4.58 billion in 2025. The market is projected to grow from USD 4.87 billion in 2026 to USD 7.98 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the global market with a market share of 33.41% in 2025.

FADEC, or full authority digital engine controller, is the digital engine controller that manages key aspects of an aircraft engine. It continuously monitors key engine parameters, such as fan speed, core speed, compressor pressures, temperatures, and throttle command. Then, it calculates the needed fuel flow and actuator schedules in real time. By handling these decisions automatically, FADEC helps in improving engine performance, protects the engine from exceedances, and maintains consistent operation across various flight conditions. The market is growing mainly because more aircraft are flying more hours. Global passenger demand reached a record in 2024, and Airbus ended 2024 with a significant order backlog that supports this demand.

Competition is focused on few established suppliers win engine programs and then profit from long-term support. Major players include Safran Electronics & Defense/FADEC International (a partnership between Safran and BAE), BAE Systems, Collins Aerospace (RTX), Honeywell, and Woodward. Engine OEMs such as GE Aerospace, Pratt & Whitney, and Rolls-Royce also play a crucial role in shaping which control solutions are used.

Download Free sample to learn more about this report.

FULL AUTHORITY DIGITAL ENGINE CONTROL MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.58 billion

- 2026 Market Size: USD 4.87 billion

- 2034 Forecast Market Size: USD 7.98 billion

- CAGR: 6.4% from 2026–2034

- North America dominated the full authority digital engine control market with a 33.41% share in 2025.

- The commercial fixed-wing segment led the market due to its large installed aircraft fleet.

- The civil aviation segment dominated the market owing to high engine utilization and aftermarket demand.

North America

The market reached USD 1.53 billion in 2025 and is driven by a large commercial aviation fleet, strong MRO network, and increasing FADEC software upgrades.

Europe

The market was valued at USD 1.31 billion in 2025 and is expected to grow steadily, supported by aircraft manufacturing, airline fleet expansion, and long-term engine programs.

Asia Pacific

The market is expected to register the fastest CAGR of 8.3%, driven by rapid aircraft deliveries and expanding aviation fleets across China, India, and Japan.

U.S.

The market is expected to witness strong growth, supported by FAA-driven FADEC upgrades, high aircraft utilization, and advanced aerospace manufacturing.

Japan

The market is expected to grow steadily, supported by increasing aircraft fleet modernization and rising demand for advanced engine control systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Safety requirements for Airworthiness Continue to Push for FADEC Upgrades

FADEC functions as the brain of a turbine engine. When reliability issues arise in service, such as hardware aging, electronics defects, or software edge cases, regulators recommend suggest fixes they also order them. These airworthiness actions lead to real costs, including software updates, control-unit changes, repeated part replacements, shop time, and re-certification paperwork. In short, compliance turns FADEC into a regular upgrade cycle rather than a one-time delivery with the engine. In practice, as modern engines become more driven by software, operators increasingly treat the authority digital engine controller as a lifecycle asset.

In April 2025, the U.S. FAA issued a final Airworthiness Directive for GE90-110B1/115B engines. This directive (1) maintains the earlier requirement for regular replacement of a FADEC microprocessor and (2) introduces a new requirement to upgrade EEC/FADEC software to an eligible version to address an unsafe thrust-control issue.

MARKET RESTRAINTS

Cyber security and Software-Assurance Compliance Delay FADEC Rollouts and Increase Upgrade Costs

FADEC systems rely heavily on software and are increasingly linked to connected maintenance systems, including data links, diagnostics, and configuration management. While this approach improves engine performance, but it raises the bar for upgrades. Each upgrade must address security risk management, documentation, audits, and stricter governance over software and configuration baselines. This creates delays, especially for retrofits and smaller suppliers, as compliance work can be just as challenging as the engineering itself.

In October 2022, published in the EU Official Journal in February 2023, the European Commission issued Implementing Regulation (EU) 2023/203 under EASA “Part-IS.” This regulation sets formal requirements for managing information security risks that could affect aviation safety. EASA noted important applicability dates, particularly 16 October 2025 and 22 February 2026, depending on the scope of the organization.

MARKET OPPORTUNITIES

New Engine Certifications and Smart Prop/Engine Digital Control are Creating New Opportunities for Market Players

There is a significant chance with the next wave of newly certified engines, especially in turboprops and other segments where OEMs are implementing more automation and integrated digital control right from the start. When a new engine is launched, the demand for FADEC extends beyond the initial shipment. It generates ongoing value through software updates, configuration management, spare parts, repairs, and upgrade packages. In simpler terms, each new certified engine family turns into a multi-year revenue stream for digital engine control FADEC system.

In February 2025, GE Aerospace announced that it received FAA certification for its Catalyst turboprop (Part 33), allowing production to ramp up toward its entry into service. The certification highlighted that the engine employs Full Authority Digital Engine and Propeller Control (FADEPC), which uses a single-lever digital control method to manage engine and propeller functions.

Full Authority Digital Engine Control MARKET TRENDS

FADEC is Becoming Software-Defined Upgrades and Configuration Management are Now Routine Parts of Engine Maintenance

FADEC was once treated as a sealed box, installed at entry into service and replaced only upon failure. That model is rapidly changing. As control logic becomes more complex and engine fleets remain in service longer, OEMs and regulators are relying more on software upgrades to fix unusual behaviors, reduce safety risks, and regulatory compliance without redesigning hardware. The market impact is clear: more spending is shifting toward software baselines, validation and testing, shop incorporation, and long-term configuration support, rather than purely toward physical line replacement units.

For instance, in September 2025, EASA’s Safety Publications Tool listed AD CF-2025-44, issued by Canada/Transport Canada, for Pratt & Whitney Canada PW150A. This directive requires a FADEC software upgrade to reduce the risk of aircraft jet pipe fire, referencing P&WC Service Bulletin PW150-73-35381, with the initial issue dated 09 June 2025.

MARKET CHALLENGES

Unapproved or Counterfeit Electronics in the Supply Chain Create Significant Problems for FADEC

FADEC hardware contains safety-critical electronics, making component traceability a critical industrial vulnerability. When suspect or unapproved components enter the supply chain, even in small quantities, the operational consequences can be severe. This can lead to urgent inspections, paperwork-heavy removals, additional shop visits, and sometimes, aircraft being taken out of service until their origin is confirmed. This extends beyond quality control and becomes a material operational and availability risk.

In October 2024, Reuters reported that the Aviation Supply Chain Integrity Coalition, which includes OEMs and major airlines, called for clear steps to stop unapproved parts from entering into aircraft supply chains. This came after the AOG Technics case, which involved fake documentation for jet-engine parts. The coalition urged stricter vendor accreditation, digital records, and improved traceability to protect safety-critical systems such as FADEC.

Impact of Russia Ukraine War

The war has affected the FADEC market in two significant ways. First, it has become more harder and in many cases legally impossible, to serve the Russian aviation market. Export controls and sanctions have restricted the flow of aircraft manufacturers parts and avionics, disrupting normal supply lines for spares, repairs, and software support for Russian operators. This has reduced straightforward sales and leads to complications, such as longer lead times, stricter traceability and compliance requirements, and increased pressure on non-Russian supply chains as inventories are adjusted.

The conflict has pushed defense spending across Europe, driving increased activity in military aviation support and modernization. This environment supports demand for FADEC retrofits, controller replacements, and software upgrades as part of propulsion-system modernization programs. Additionally, the war has created challenges for upstream electronics inputs, such as neon used in semiconductor manufacturing, quietly raising FADEC controller costs and extending delivery timelines.

- For instance, in February 2022, the U.S. Department of Commerce imposed broad controls on aviation-related items destined for Russia, including a new license requirement for aircraft and aircraft parts.

- In April 2025, SIPRI reported that global military spending reached USD 2.718 trillion (2024), with European spending rising sharply, linked directly to the security issues created by the war. This increase supports a higher focus on modernization and maintenance, including propulsion systems.

Download Free sample to learn more about this report.

Segmentation

By Platform

Commercial Fixed-Wing Segment Leads Due to the Large Installed Base of Narrow-Body

In terms of platform, the market is categorized into commercial fixed-wing, business & general aviation, military fixed-wing, rotary-wing, and un-crewed platforms.

The commercial fixed-wing segment dominates the market demand, driven by the large installed base of narrow-body, wide-body, and regional aircraft fleets. These fleet rely on high-utilization engines that use the digital engine controller FADEC for daily thrust management and accurate fuel flow scheduling. These aircraft create ongoing expenses for spare parts, engine removals, repairs, software updates, and configuration control over many years of heavy use. Additionally, airlines are still managing a significant backlog of aircraft orders. Even if deliveries fluctuate in a single year, the overall pipeline keeps commercial fixed-wing solidly in the lead.

In January 2025, Airbus an aircraft manufacturers announced it delivered 766 commercial aircraft in 2024 and ended the year with a backlog of 8,658 aircraft. This backlog indicates a sustained, multi-year demand for new commercial aircraft, which directly supports the ongoing line-fit FADEC volume and the long-term aftermarket demand.

The uncrewed platforms segment is expected to show fastest grow at a CAGR of 14.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Engine Type

Turbofan Segment Led the Market due to its Ability Create a Strong Demand for Aftermarket Services

On the basis of by engine type, the market is classified into turbofan, turboprop, turboshaft, and small turbojet/microturbine.

The turbofan segment dominated the market in 2025. Most of the world’s total flying hours and engine deliveries are generated by turbofan-powered aircraft, particularly single-aisle and wide body and regional jets. This concentration is important for the FADEC market, as turbofans engines account for the largest drive line-fit volume, with every new engines are shipped with FADEC/EEC. They also create a strong demand for aftermarket services such as spare parts, engine removals, repairs, and continuous software and configuration updates in high-cycle airline operations.

In February 2023, CFM International made a deal with Air India for a record order of over 800 LEAP turbofan engines. These engines will power 210 Airbus A320/A321neo and 190 Boeing 737 MAX aircraft, along with a service package. This order strengthens the demand for turbofan-led FADEC volume and long-term support.

Small Turbojet/Microturbine is expected to show fastest Full Authority Digital Engine Control market growth at a CAGR of 13.5% over the forecast period.

By FADEC Type

Dual-Channel FADEC Segment Dominates the market due to Ability to Address Engine Safety

Based on FADEC type, the market is segmented into single-channel FADEC and dual-channel FADEC.

The dual-channel FADEC segment dominates the market. FADEC is essential for engine safety and reliability in dispatch availability, the industry avoids single points of failure in this area. Dual-channel FADEC architectures address this requirement by incorporating two fully independent control paths with cross-monitoring. This setup keeps the engine controllable even if one path fails. It also makes certification and airline operations much smoother. As fleets become more reliant on software, dual-channel systems help manage upgrades without making every small change a risk to operations.

Single-channel FADEC is the fastest-growing segment in market at a CAGR of 12.3% across the forecast period.

By Fit

Aftermarket segment Leads the market owing to Vast Number of Legacy Aircraft Needing Upgrades

Based on fit, the market is segmented into Line-fit, retrofit, and aftermarket.

Aftermarket segment is holds the largest share of market. The segment dominance is attributed to the vast number of legacy aircraft needing upgrades, the need to extend their service life, and the drive for fuel efficiency/emission compliance on older fleets, creating a huge demand for retrofitting FADEC systems to reduce operational costs and meet new regulations. Moreover, Next-gen FADEC systems with AI, digital twins, and advanced diagnostics are highly desirable for efficiency, driving demand for upgrades.

The retrofit segment is expected to show fastest market growth at a CAGR of 10.2% during the forecast period.

By End User

Civil Aviation Segment Dominates the Market due to High Daily Cycles

By end user, the market is segmented into Civil Aviation, Defense, MRO, and airframers & integrators.

The civil aviation segment holds the largest full authority digital engine control market share. Dominance of civil aviation represents the most demanding operating environment for aircraft engines, characterized by high daily cycles, long hours, and strict dispatch reliability goals. These operating conditions generate steady FADEC demand throughout the entire engine lifecycle, spanning initial line-fit installation on new aircraft, along with a larger and more reliable flow of spare parts, repairs, bench testing, and software or configuration updates once fleets are operational. Even when new deliveries vary, the installed base ensures that civil aviation remains the main source of need in the market.

The MRO segment is expected to show the fastest growth at a CAGR of 8.3% during the forecast period.

Full Authority Digital Engine Control Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Full Authority Digital Engine Control Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The dominance of North America mainly stems from the U.S., where demand comes from multiple sources. There is a large commercial aviation in constant operation, which means controllers frequently perform repairs, replace parts, and update software. The defense aviation sector is also significant, along with a vast network of OEM-authorized and independent MRO facilities that can carry out upgrades on a large scale. In simple terms, more engines in service, more flight hours, and more required upgrades result in increased FADEC spending year after year.

In April 2025, the U.S. FAA issued a final rule that replacing earlier ADs for GE90-110B1/115B engines. This rule keeps the requirement for repeated replacement of a FADEC (MN4) microprocessor. It also adds a requirement to upgrade EEC/FADEC software to a version that qualifies as a terminating action.

Europe

Europe is expected to witness significant full authority digital engine control market growth in the Full Authority Digital Engine Control Market over the coming years, registering a projected CAGR of 5.8%. The market in Europe is estimated to be USD 1.31 billion in 2025. In this region, both the U.K. and France are expected to reach USD 0.13 billion and USD 0.14 billion, respectively, in 2026. Europe maintains a strong demand for FADEC as it has a unique mix. It has significant aircraft and engine manufacturing activity, which creates line-fit demand. Additionally, a large airline fleet that operates frequently provides a continuous need for FADEC spare parts, repairs, and software and configuration updates. Even though deliveries can vary from quarter to quarter, the long backlog ensures that the line-fit engine control FADEC system process remains steady.

Asia Pacific

Asia Pacific is anticipated to fastest-growing segment in the global Full Authority Digital Engine Control market, growing at a CAGR of 8.3%. China, India, Japan, and Rest of the Asia Pacific, where aircraft deliveries and engine inductions are accelerating rapidly. This leads to a growing installed base that quickly turns into recurring FADEC aftermarket services, including repairs, replacements, and software updates. The scale of fleet expansion in this region strengthens line-fit demand but also creates the largest future pipeline for sustainment. Based on these factors, countries such as China expect to reach a valuation of USD 0.51 billion, and India is set to reach USD 0.26 billion by 2026.

Latin America

Latin America accounted for approximately for 4.17% of the global market in 2025. Latin America's FADEC demand focuses less on new engine programs and more on maintaining the reliability of existing fleets. This is especially true for Brazil and Mexico, which have large commercial aviation bases and busy hubs. As air traffic continue to recover and aircraft usage increases, FADEC spending mostly goes toward repairs, replacements, and shop incorporation work.

Middle East & Africa

The Middle East & Africa region contributed around 5.75% of the market in 2025 and is projected to grow at a CAGR of 7.3%. While MEA represents a smaller full authority digital engine control market share compared to FADEC story focuses on usage. Large hub airports have high aircraft turns and long-haul cycles. This speeds up FADEC removals, shop visits, and configuration updates. With ongoing airport expansion, the regional market is increasingly availability, where maintaining aircraft availability and dispatch reliability remains the primary value driver.

COMPETITIVE LANDSCAPE

Key Industry Players

FADEC Players Focus on Contracts to Gain Competitive Edge

The FADEC market is competitive and program-locked, with a small group of proven suppliers securing long-term positions on engine programs. Once selected, these positions tend to remain stable as FADEC is critical for safety and is deeply integrated into the propulsion systems. This situation benefits established companies with extensive certification histories and mature architectures. Dual-channel FADEC has become the standard in the transport category, raising the bar for any new competitor trying to enter the market.

FADEC International (a joint venture between Safran and BAE Systems) focuses on designing, producing, and supporting full-authority digital engine controls for commercial engines. Collins Aerospace (RTX) positions its FADEC electronic engine controllers by adding value through health and diagnostics. Supportability and data-driven maintenance have become part of the product offering. Woodward competes strongly across turbine engine control solutions and broader engine system integration. The competitive landscape is shifting from merely delivering products to three key areas: certification and safety assurance, software and configuration management, and lifecycle responsiveness, which includes repairs, spare parts, and turnaround time. Recent mergers in related flight control and actuation areas, such as Safran and Collins, show that mission-critical control portfolios are blending, increasing pressure on smaller specialists.

LIST OF KEY FULL AUTHORITY DIGITAL ENGINE CONTROL COMPANIES PROFILED:

- Safran Electronics & Defense (France)

- FADEC International (France / U.K.)

- BAE Systems (U.K.)

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Woodward, Inc. (U.S.)

- GE Aerospace (U.S.)

- Pratt & Whitney (U.S.)

- Pratt & Whitney Canada (Canada)

- Rolls-Royce plc. (U.K.)

- Safran Aircraft Engines (France)

- CFM International (France)

KEY INDUSTRY DEVELOPMENTS

- June 2025- Ryanair agreed to buy 30 LEAP-1B spare engines from CFM. This would improve operational resilience and expand the spare engine pool.

- July 2025- SR Technics and Safran Aircraft Engines signed a long-term extension for LEAP-1A complete overhaul and testing. This strengthens the development of new-generation engine maintenance, repair, and overhaul (MRO) capacity, where FADEC testing and configuration are important.

- July 2025- Safran announced it had completed its acquisition of Collins Aerospace’s flight control and actuation activities. This highlights a larger trend of consolidating mission-critical controls related to FADEC ecosystems.

- February 2025- GE Aerospace announced FAA Part 33 certification for its Catalyst turboprop. This marks a significant milestone for modern digital engine control in new turboprops.

- March 2024- CFM finalized agreements with American Airlines. This included a new 20-year LEAP-1B service agreement and spare engines. This clearly signals a "lifecycle annuity" for engine controls and maintenance.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.4% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Platform · Commercial Fixed-Wing · Business & General Aviation · Military Fixed-Wing · Rotary-Wing · Uncrewed Platforms |

|

By Engine Type · Turbofan · Turboprop · Turboshaft · Small Turbojet/Microturbine |

|

|

By FADEC Type · Single-channel FADEC · Dual-channel FADEC |

|

|

By Fit · Line-fit · Retrofit · Aftermarket |

|

|

By End User · Civil Aviation · Defense · MRO · Airframers & Integrators |

|

|

By Region · North America (By Platform, By Engine Type, By FADEC Type, By Fit , By End User, and By Country) o U.S. (By Platform) o Canada (By Platform) · Europe (By Platform, By Engine Type, By FADEC Type, By Fit , By End User, and By Country) o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Spain (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific (By Platform, By Engine Type, By FADEC Type, By Fit , By End User, and By Country) o China (By Platform) o India (By Platform) o Japan (By Platform) o South Korea (By Platform) o Australia (By Platform) o Rest of Asia-Pacific (By Platform) · Latin America (By Platform, By Engine Type, By FADEC Type, By Fit, By End User, and By Country) o Brazil (By Platform) o Mexico (By Platform) o Rest of the Latin America (By Platform) · Middle East & Africa (By Platform, By Engine Type, By FADEC Type, By Fit , By End User, and By Country) o UAE (By Platform) o Saudi Arabia (By Platform) o Egypt (By Platform) · Rest of the Middle East & Africa (By Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.87 billion in 2026 and is projected to reach USD 7.98 billion by 2034.

In 2025, the market value stood at USD 1.53 billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period (2026-2034).

The commercial fixed-wing segment leads the market by platform.

Safety requirements for airworthiness is the key factor driving aftermarket growth.

Safran Electronics & Defense, FADEC International, BAE Systems, Collins Aerospace, Honeywell Aerospace, Woodward, Inc., GE Aerospace, Pratt & Whitney, and among others are the top companies in the market.

North America dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us