Gas Processing Equipment Market Size, Share & Industry Analysis, By Equipment Type (Separation Equipment, Compression Equipment, Gas Treating Equipment, Cryogenic Processing Equipment, and Others), By Gas Type (Associated Petroleum Gas (APG), Sour Gas, Natural Gas, and Non-associated Gas), By End User (Petrochemical Feedstock Processing, LNG Processing, Gas Processing Plants, Refinery Gas Processing, Field Processing, and Others), and Regional Forecast, 2026-2034

Gas Processing Equipment Market Size and Future Outlook

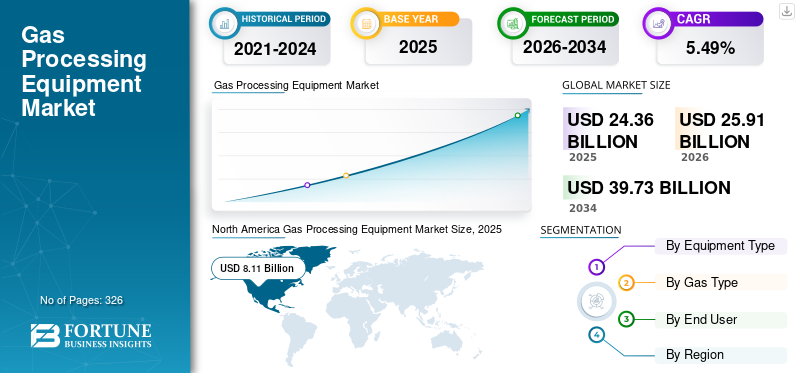

The global gas processing equipment market size was valued at USD 24.36 billion in 2025. The market is projected to grow from USD 25.91 billion in 2026 to USD 39.73 billion by 2034, exhibiting a CAGR of 5.49% during the forecast period. North America dominated the gas processing equipment market with a market share of 33.29% in 2025.

Gas processing equipment refers to the range of machinery and systems used to treat, purify, and separate raw natural gas into marketable products. These equipment systems remove impurities, such as water, carbon dioxide, hydrogen sulfide, and other contaminants, while enabling the extraction of valuable components, such as natural gas liquids (NGLs). Key equipment includes compressors, separators, gas treating units, cryogenic systems, and dehydration units. This equipment is essential across upstream, midstream, and LNG operations to ensure gas meets pipeline specifications and end-use requirements.

Market growth is primarily driven by the increasing global demand for natural gas as a cleaner alternative to coal and oil, particularly in power generation and industrial applications. The expansion of LNG infrastructure and cross-border gas trade is further boosting demand for advanced processing systems, particularly cryogenic and compression equipment. The growing development of unconventional resources, such as shale and tight gas, is increasing the need for advanced processing technologies. Additionally, stringent environmental regulations aimed at reducing flaring and emissions are accelerating investments in gas treating and recovery equipment. The ongoing expansion of gas infrastructure in emerging economies also supports steady market growth.

Leading companies such as Air Products and Chemicals, Inc., Linde plc, Honeywell International Inc. (UOP), Baker Hughes Company, and Chart Industries, Inc. are actively contributing to market development through several common strategic initiatives. These players are heavily investing in advanced and energy-efficient technologies, particularly in cryogenic processing, carbon capture integration, and modular plant solutions. They are also focusing on expanding their LNG and hydrogen-related portfolios to align with the global energy transition. Additionally, these companies are strengthening their market presence through strategic partnerships, EPC contracts, and long-term service agreements with oil & gas operators. Continuous innovation in digital monitoring, automation, and process optimization is further enhancing operational efficiency and driving adoption across global gas processing infrastructure.

Download Free sample to learn more about this report.

Gas Processing Equipment Market Key Takeways

- 2025 Market Size: USD 24.36 billion

- 2026 Market Size: USD 25.91 billion

- 2034 Forecast Market Size: USD 39.73 billion

- CAGR: 5.49% from 2026–2034

- North America dominated the gas processing equipment market with a 33.29% share in 2025.

- The compression equipment segment accounted for the largest market share of 29.0% in 2025.

- The gas processing plants segment held the largest share of 41.41% in 2025.

North America

North America led the global market with a value of USD 8.11 billion in 2025, accounting for approximately 33.27% of global revenue.

Europe

Europe reached USD 2.68 billion in 2025, contributing approximately 11.02% of the global market.

Asia Pacific

Asia Pacific was valued at USD 6.08 billion in 2025, representing approximately 24.96% of global revenues.

U.S.

U.S. The market was valued at USD 7.00 billion in 2025 and is projected to reach USD 7.42 billion in 2026.

Japan

Japan The market was valued at USD 0.59 billion in 2025 and is expected to reach USD 0.63 billion in 2026.

Read More

Gas Processing Equipment Market Trends

Increasing Adoption of Modular and Skid-Mounted Processing Systems are Amplifying Market Growth

A significant trend shaping the market is the growing adoption of modular and skid-mounted processing systems. These systems are pre-engineered, factory-assembled units that can be rapidly deployed, reducing project timelines by 20–40% compared to traditional stick-built plants. This trend is particularly prominent in shale gas regions such as the U.S. and emerging markets in Southeast Asia, where operators prioritize flexibility and cost efficiency. Modular systems also enable easier scalability and relocation, making them ideal for remote or smaller gas fields. Companies are increasingly integrating digital monitoring and automation into these systems, enhancing operational efficiency and reducing downtime. The shift toward modularization also aligns with the industry’s push for lower capital expenditure and faster returns on investment, especially in volatile energy markets. As a result, modular solutions are becoming a preferred choice for both new installations and capacity expansions.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global Demand for Natural Gas as a Transition Fuel to Push Market Growth

One of the primary drivers of the gas processing equipment market growth is the increasing global reliance on natural gas as a cleaner transition fuel compared to coal and oil. According to the International Energy Agency (IEA), natural gas accounts for nearly 24% of global energy demand, and its consumption is expected to grow steadily through the decade, particularly in Asia Pacific. Countries such as China and India are actively shifting from coal to gas to reduce emissions, leading to higher demand for processed, pipeline-quality gas. This transition requires extensive deployment of gas processing equipment, including compressors, treating units, and cryogenic systems. Additionally, LNG trade is expected to grow by 3–4% annually, further reinforcing the need for advanced processing infrastructure. As nations aim to balance energy security with decarbonization goals, investments in gas processing facilities are accelerating, directly driving product demand across upstream and midstream operations.

Market Restraints

Volatility in Oil & Gas Prices Affecting Investment Cycles to Limit Market Growth

The market is significantly restrained by the volatility in oil and gas prices, which directly influences capital expenditure decisions in the energy sector. Fluctuations in crude oil prices such as the sharp decline during 2020 when prices briefly fell below USD 20 per barrel, lead to reduced upstream investments and delayed gas infrastructure projects. Since a large share of gas production is associated with oil extraction, lower oil prices often lead to reduced associated gas output and processing requirements. This cyclicality creates uncertainty for equipment manufacturers and EPC contractors, affecting order pipelines and long-term planning. Moreover, investors tend to adopt a cautious approach during periods of price instability, postponing large-scale projects. As a result, demand for gas processing equipment becomes closely tied to broader energy market dynamics, acting as a restraint on consistent market growth.

Market Opportunities

Integration of Carbon Capture, Hydrogen, and Low-Carbon Gas Processing to Create New Growth Avenues

A key market opportunity lies in integrating carbon capture, hydrogen production, and low-carbon processing technologies. As global decarbonization efforts intensify, there is increasing demand for equipment that can support carbon capture, utilization, and storage (CCUS) and hydrogen production from natural gas (blue hydrogen). According to the IEA, global CCUS capacity is expected to grow by 5–6 times by 2030, creating substantial demand for advanced gas-treating and separation technologies. Additionally, hydrogen projects, particularly in Europe and the Middle East, are driving the need for specialized processing systems capable of handling gas reforming and purification. Gas processing equipment manufacturers are leveraging this shift by developing solutions that integrate emission reduction technologies with traditional processing systems. This convergence of conventional gas infrastructure with low-carbon technologies presents a significant growth avenue, positioning the market to play a critical role in the global energy transition.

Market Challenges

High Capital Intensity and Project Execution Complexity to Limit Market Growth

A major challenge in the market is the high capital intensity and complexity of project execution. Large-scale gas processing plants, particularly LNG facilities, require significant upfront investments, often exceeding USD 5–10 billion for major projects. These projects involve complex engineering, procurement, and construction (EPC) processes with long lead times that can span several years. Additionally, cost overruns and delays are common due to supply chain disruptions, regulatory approvals, and technical challenges associated with sour or unconventional gas. For instance, several LNG projects globally have experienced delays of 12–24 months, impacting overall project economics. The need for specialized equipment and a skilled workforce further adds to the complexity. This high-risk investment environment can deter smaller players and limit market entry, posing a significant challenge to overall market growth.

Segmentation Analysis

By Equipment Type

Ongoing Pipeline Expansions and Other Developments in Oil & Gas Industry Boosted Compression Equipment Segment Growth

Based on equipment type, the market is segmented into separation equipment, compression equipment, gas treating equipment, cryogenic processing equipment, and others.

The compression equipment segment accounted for 29% of the gas processing equipment market share in 2025. Compression equipment forms the backbone of gas processing infrastructure, accounting for the largest share of the market due to its critical role across upstream, midstream, and LNG operations. These systems are essential for transporting gas through pipelines, maintaining pressure levels, and enabling efficient processing and storage. The segment is characterized by steady demand driven by ongoing pipeline expansions, shale gas development, and aging infrastructure replacement cycles. Technological advancements such as energy-efficient compressors, digital monitoring systems, and predictive maintenance solutions are enhancing operational efficiency and reducing downtime. Additionally, increasing LNG exports and cross-border gas trade are further driving demand for high-capacity compression systems.

The cryogenic processing equipment segment is expected to grow at a CAGR of 6.51% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Gas Type

High Usage of Natural Gas for Power Generation, Industrial Use, and Heating Fuels Segment Growth

Based on gas type, the market is segmented into associated petroleum gas (APG), sour gas, natural gas, and non-associated gas.

The natural gas segment accounts for 69.39% of the market share. Natural gas remains the dominant segment in the market, accounting for the majority of processed gas volumes globally. With global production exceeding 4 trillion cubic meters annually, natural gas is a critical energy source for power generation, industrial use, and heating. The continued shift toward cleaner fuels has reinforced its role, particularly in Asia Pacific, where countries such as China and India are increasing gas consumption to reduce their reliance on coal. Additionally, the expansion of LNG trade, facilitating global gas movement, has significantly increased the need for advanced processing infrastructure, including cryogenic and compression equipment. Shale gas developments, especially in North America, have further contributed to sustained demand for processing systems.

The associated petroleum gas (APG) segment is expected to grow at a CAGR of 6.42% during the forecast period.

By End User

Gas Processing Plants Led Market Due to Their Central Role in Converting Raw Natural Gas into Pipeline-Quality Gas

Based on end user, the market is segmented into petrochemical feedstock processing, LNG processing, gas processing plants, refinery gas processing, field processing, and others.

The gas processing plants segment held the largest share of 41.41% in the market in 2025, driven by their central role in converting raw natural gas into pipeline-quality gas and valuable by-products such as NGLs. Globally, with natural gas production exceeding 4 trillion cubic meters annually, a significant portion of this production requires treatment, dehydration, and separation before distribution. These plants are widely deployed across major producing regions, including North America, the Middle East, and Russia, where large-scale midstream infrastructure supports domestic consumption and exports. The segment benefits from both new capacity additions and ongoing debottlenecking/upgradation of existing facilities, particularly as gas compositions become more complex (e.g., higher CO₂ or H₂S content). Additionally, increasing integration with petrochemical value chains (ethane recovery) is enhancing the importance of these plants.

The LNG processing segment is expected to grow with a CAGR of 6.59% over the forecast period.

Gas Processing Equipment Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Gas Processing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is the dominant region globally with a market valued at USD 8.11 billion in 2025, accounting for approximately 33.27% of the global market. North America represents the largest market, primarily driven by the U.S.’ shale gas revolution. The region accounts for nearly 30–35% of global natural gas production, with the U.S. alone producing over 1 trillion cubic meters annually (EIA). This extensive production base requires continuous investment in gas processing plants, compression infrastructure, and LNG facilities. The rapid expansion of LNG export terminals along the U.S. Gulf Coast—such as Sabine Pass and Corpus Christi—has significantly increased demand for cryogenic and compression equipment.

Aging midstream infrastructure is driving replacement and upgrade cycles, particularly for compressors and treating systems. Canada also contributes through unconventional gas developments in the Montney and Duvernay basins. While the market is relatively mature, LNG exports, pipeline expansions, and technological upgrades focused on efficiency and emissions reduction are expected to drive market growth in North America.

U.S. Gas Processing Equipment Market

The U.S. market was valued at USD 7.00 billion in 2025 and is expected to reach USD 7.42 billion in 2026. The U.S. dominates the global market, supported by its position as the largest natural gas producer (~1 trillion cubic meters annually, EIA). The shale gas boom has led to extensive midstream infrastructure, including processing plants and pipelines. Additionally, the U.S. is the world’s leading LNG exporter, with multiple terminals along the Gulf Coast driving demand for cryogenic and compression equipment. Continuous upgrades and debottlenecking of existing infrastructure further sustain market demand.

Europe

Europe accounted for USD 2.68 billion in 2025, representing approximately 11.02% of global revenues. Europe’s market is characterized by moderate growth and structural transition, driven by energy security concerns and decarbonization goals. The region relies heavily on imported gas, with LNG imports increasing significantly in recent years to offset reduced pipeline supplies. For instance, Europe’s LNG imports grew by over 60% between 2021 and 2023 (IEA), leading to the rapid expansion of regasification terminals and associated processing infrastructure. Countries such as Germany and the Netherlands are investing in floating storage and regasification units (FSRUs), thereby boosting demand for cryogenic and gas-handling equipment. Norway remains a key upstream contributor, supplying processed gas to Europe. However, long-term growth is tempered by the region’s shift toward renewable energy and hydrogen. As a result, demand is increasingly focused on efficiency upgrades, retrofits, and integration with low-carbon technologies rather than large-scale greenfield gas-processing projects.

Germany Gas Processing Equipment Market

The market in Germany was valued at USD 0.39 billion in 2025 and is expected to reach USD 0.41 billion in 2026. The market is driven by industrial gas demand and energy transition initiatives. Following the reduced pipeline gas supply, the country has rapidly deployed FSRUs (floating LNG terminals), boosting demand for gas handling and processing equipment. Germany is also investing in hydrogen-ready infrastructure, requiring upgrades to existing gas systems. Despite limited domestic production, infrastructure expansion supports steady demand.

U.K. Gas Processing Equipment Market

The U.K. market was valued at USD 0.32 billion in 2025 and is expected to reach USD 0.34 billion in 2026. The U.K. market is mature, driven by North Sea gas production and LNG imports. While domestic production is declining, infrastructure upgrades and energy security concerns are supporting demand for gas processing equipment. The U.K. has also expanded LNG import capacity to diversify supply, increasing reliance on cryogenic systems. Growth remains moderate due to the country’s strong push toward renewable energy and decarbonization.

Asia Pacific

The Asia Pacific market was valued at USD 6.08 billion in 2025, accounting for approximately 24.96% of global revenues. Asia Pacific is the fastest-growing region in the market, driven by rising energy demand and increasing adoption of natural gas as a cleaner fuel. The region accounts for over 40% of global LNG imports, with countries such as China, Japan, and India leading demand. China’s natural gas consumption has grown significantly, supported by policies aimed at reducing coal use, while India is targeting an increase in the gas share of its energy mix from ~6% to 15% in the coming years. Australia plays a critical role as a major LNG exporter, with large-scale liquefaction facilities driving demand for high-value cryogenic equipment. Southeast Asia is also emerging as a growth hub, with countries such as Indonesia and Vietnam investing in gas infrastructure. The combination of upstream development, LNG trade expansion, and infrastructure build-out makes Asia Pacific a key growth engine for the market.

China Gas Processing Equipment Market

China remains the dominant contributor in Asia Pacific, valued at USD 2.04 billion in 2025 and is expected to reach USD 2.20 billion in 2026. China is one of the fastest-growing markets, with natural gas consumption rising rapidly due to coal-to-gas switching policies. The country is among the largest LNG importers globally, accounting for a significant share of Asia’s demand. Expansion of domestic gas fields and pipeline infrastructure is driving demand for processing equipment. Government targets for cleaner energy further support investments in gas processing systems.

India Gas Processing Equipment Market

India was valued at USD 0.81 billion in 2025 and is expected to reach USD 0.87 billion in 2026. India is an emerging high-growth market, aiming to increase the share of natural gas in its energy mix from ~6% to 15%. Rapid expansion of LNG terminals, pipelines, and city gas distribution networks is driving demand for gas processing equipment. Increasing industrial and power sector gas usage further supports market growth. Government initiatives and infrastructure investments are key growth enablers.

Japan Gas Processing Equipment Market

Japan was valued at USD 0.59 billion in 2025 and is expected to reach USD 0.63 billion in 2026. Japan is one of the world’s largest LNG importers, relying almost entirely on imported gas. The country has well-established LNG regasification infrastructure, driving steady demand for cryogenic and gas handling equipment. While the market is mature, ongoing upgrades and efficiency improvements sustain demand. Energy security concerns continue to reinforce LNG dependence.

Latin America

Latin America accounted for USD 1.76 billion in 2025, or approximately 7.22% of global revenues. Latin America presents a moderately growing market for gas processing equipment, supported by upstream developments and efforts to monetize gas resources. Brazil dominates the region, driven by offshore pre-salt oil and gas fields, where associated gas processing requires significant investment in compression and separation equipment. Argentina is another key market, with the Vaca Muerta shale formation emerging as a major source of unconventional gas. The region’s natural gas production exceeds 200 billion cubic meters annually, creating steady demand for processing infrastructure. Mexico contributes through pipeline expansion and integration with U.S. gas imports, although investment levels have been somewhat inconsistent due to policy changes. Additionally, countries such as Peru and Colombia are gradually expanding their gas processing capabilities. While the market faces challenges related to regulatory uncertainty and investment cycles, ongoing upstream and midstream developments are expected to support stable growth in the coming years.

Middle East & Africa

The Middle East & Africa region was valued at USD 5.73 billion in 2025. The Middle East & Africa region is a high-growth market for gas processing equipment, driven by abundant gas reserves and large-scale development projects. The Middle East, particularly the GCC countries, holds some of the world’s largest natural gas reserves and is investing heavily in processing infrastructure. Qatar’s North Field expansion, one of the largest LNG projects globally, is a key driver of demand for cryogenic and gas-treating equipment. The region is also characterized by a high proportion of sour gas, requiring advanced processing technologies. In Africa, countries such as Mozambique and Nigeria are developing LNG export projects, driving demand for gas processing systems. Africa’s LNG capacity is expected to grow significantly over the next decade, supported by global energy demand. Overall, the region’s combination of upstream expansion, LNG growth, and gas monetization initiatives positions it as a major contributor to future market growth.

GCC Gas Processing Equipment Market

The GCC market was valued at USD 3.98 billion in 2025 and is expected to reach USD 4.21 billion in 2026. The GCC region is a major hub for gas processing equipment, driven by vast reserves and large-scale projects. Qatar’s North Field expansion and Saudi Arabia’s sour gas developments are key drivers. The region has a high sour gas content, requiring advanced gas-treating technologies. Investments in LNG and gas monetization projects continue to fuel strong demand for processing equipment.

Competitive Landscape

KEY INDUSTRY PLAYERS

Technological Advancements and Global Presence are Booming Market Share for Key Companies

Leading companies such as Air Products and Chemicals, Inc., Linde plc, Honeywell International Inc. (UOP), Baker Hughes Company, and Chart Industries play a critical role in shaping the market through their strong technological capabilities and global project execution. These companies collectively dominate key segments such as cryogenic processing, gas treating, and compression systems, enabling large-scale LNG, hydrogen, and gas monetization projects worldwide. Their market influence is evident in major developments such as LNG export terminals in the U.S. and Qatar’s North Field expansion, where advanced processing technologies are essential. These players are heavily focused on developing energy-efficient, low-emission technologies, including the integration of carbon capture (CCUS) and hydrogen processing solutions. They are also investing in modular and pre-engineered systems to reduce project timelines and costs, addressing industry demand for faster deployment.

List of Key Gas Processing Equipment Companies Profiled

- Air Products and Chemicals, Inc. (U.S.)

- Linde plc (U.K.)

- Air Liquide S.A. (France)

- Honeywell International Inc. (UOP) (U.S.)

- Baker Hughes Company (U.S.)

- SLB (Schlumberger Limited) (U.S.)

- Siemens Energy AG (Germany)

- Atlas Copco AB (Sweden)

- MAN Energy Solutions SE (Germany)

- Ebara Corporation (Japan)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Chart Industries, Inc. (U.S.)

- Technip Energies N.V. (France)

- John Wood Group plc (U.K.)

- Wärtsilä Corporation (Finland)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Baker Hughes secured a contract to supply LNG compression and gas processing equipment for a major global LNG project. The project highlights the growing demand for high-capacity turbomachinery in LNG expansion.

- January 2025: Air Liquide invested in new gas processing and hydrogen production units in Europe. These facilities are designed to support industrial decarbonization and integrate advanced gas purification technologies.

- June 2024: Linde secured a long-term contract to supply industrial gases and processing technologies for a major LNG facility. The project includes advanced gas separation and liquefaction systems, reinforcing Linde’s leadership in cryogenic and large-scale processing solutions.

- April 2024: Honeywell UOP launched upgraded gas-processing and carbon-capture technologies for LNG and refining applications. These solutions focus on improving CO₂ removal efficiency and reducing operational costs for operators.

- March 2024: Air Products expanded its LNG process technology portfolio to support large-scale export terminals. This development focuses on improving energy efficiency and reducing emissions in liquefaction processes, particularly for North America and Middle East projects. It strengthens the company’s position in high-value cryogenic equipment.

REPORT COVERAGE

The gas processing equipment market report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.49% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Equipment Type

|

|

By Gas Type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 24.36 billion in 2025 and is projected to reach USD 39.73 billion by 2034.

In 2025, the market value in North America stood at USD 8.11 billion.

The market is expected to exhibit a CAGR of 5.49% during the forecast period of 2026-2034.

By equipment type, the compression equipment segment led the market.

Rising global demand for natural gas as a transition fuel is driving market expansion.

Air Products and Chemicals, Inc., Linde plc, Honeywell International Inc. (UOP), Baker Hughes Company, and Chart Industries are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us