Generative AI in Life Sciences Market Size, Share & Industry Analysis, By Component (Software/Platforms and Services), By Deployment (Cloud-Based, On-Premise, and Hybrid), By Technology (Large Language Models (LLMs), Natural Language Processing (NLP), Generative Molecular/Protein Models, and Others), By Product Type (Standalone and Integrated), By Application (Drug Discovery & Design, Clinical Trial Design & Operations, and Others), By End User (Pharmaceutical & Biotechnology Companies, CROs, Academic & Research Institutes, and Others) and Regional Forecast, 2026-2034

Generative AI in Life Sciences Market Size and Future Outlook

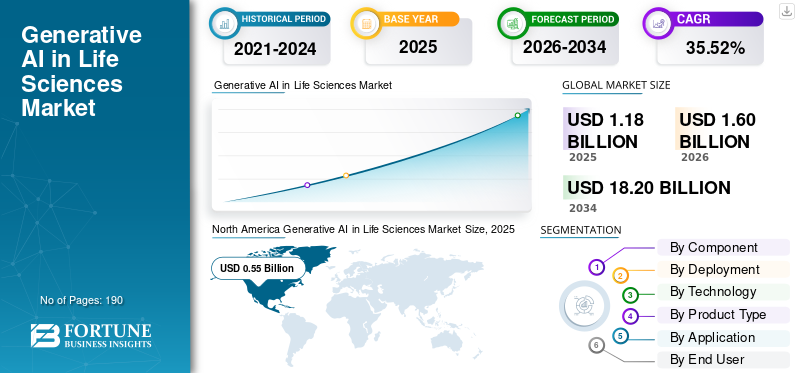

The global generative AI in life sciences market size was valued at USD 1.18 billion in 2025. The market is projected to grow from USD 1.60 billion in 2026 to USD 18.20 billion by 2034, exhibiting a CAGR of 35.52% during the forecast period.

The global market comprises AI-based platforms, models, and software solutions that enhance research, development, and operational workflows. The market is poised for significant growth, as life sciences organizations handle large volumes of genomic, clinical, molecular, imaging, and regulatory data, creating demand for tools that can generate insights, automate documentation, support molecule design, and improve decision-making.

As key companies face rising R&D costs, longer drug development timelines, and growing pressure to improve clinical success rates, the adoption of generative AI across drug discovery, clinical trial design, regulatory writing, medical affairs, and commercial operations is also rising. Key companies are investing in generative AI platforms, strategic partnerships, and AI-enabled life sciences solutions to strengthen their position in this evolving market.

- For instance, in January 2026, NVIDIA Corporation expanded NVIDIA BioNeMo, an open development platform designed to support lab-in-the-loop workflows and accelerate AI-driven biology and drug discovery. The adoption of BioNeMo was aimed at scaling scientific discovery by connecting generative, agentic, and physical AI for drug discovery applications.

Major players, such as NVIDIA Corporation, IQVIA Inc., Oracle Corporation, and Veeva Systems Inc., are streamlining their resources toward technological advancement, investment initiatives, and new product launches to strengthen their market presence.

Download Free sample to learn more about this report.

GENERATIVE AI IN LIFE SCIENCES MARKET TRENDS

Growing Use of AI Copilots is an Emerging Trend Observed

A significant trend emerging in the global generative AI in life sciences market is the growing use of AI copilots. Life sciences companies often work with fragmented data, including lab records, protocols, literature, and study documents, which can slow down decision-making and reduce productivity. AI copilots help address these challenges by allowing scientists and business users to ask questions, summarize information, compare results, and generate insights within existing research platforms. As a result, these tools are shifting from simple productivity assistants to workflow-based scientific copilots that support discovery, experiment planning, documentation, and knowledge management. Key companies are focusing on and investing in new product launches to capitalize on this growing market trend.

- For instance, in October 2025, Benchling, Inc. launched Benchling AI as a command center for scientific AI, bringing agents and predictive models directly into scientists’ existing workflows. Such development highlights how life sciences companies are embedding AI co-pilots into research platforms to reduce the use of disconnected tools and improve access to scientific knowledge.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Volume of Genomic, Clinical, and Molecular Data Across Life Sciences Driving Market Growth

The increasing volume of genomic, clinical, and molecular data is a major driver for the global generative AI in life sciences market. The increased volume of data encourages life sciences companies to adopt faster, smarter ways to manage complex scientific information. Pharmaceutical and biotechnology companies generate large datasets, but traditional analytics tools often struggle to efficiently connect these data sources. Generative AI helps address this challenge by summarizing large datasets, identifying hidden patterns, supporting target discovery, improving clinical trial design, and generating research-ready insights. Adoption of these AI-enabled platforms reduces manual analysis, improves decision-making, and accelerates drug development workflows.

This creates strong demand for generative AI solutions that can unify diverse data sources and convert them into actionable scientific and clinical intelligence. Underscoring their vast applications, key companies in the market are investing heavily in developing these platforms.

- For instance, in May 2025, Rad AI received a USD 68.0 million Series C investment from Advocate Health, Memorial Hermann Health System, Corewell Health, and Atlantic Health System. These partnerships reflect a shared commitment to transform care delivery for millions of patients nationwide and to scale the use of generative AI across hospitals and clinics.

MARKET RESTRAINTS

Regulatory Uncertainty Around AI-Generated Scientific and Clinical Outputs Hampers Market Growth

One of the key factors restraining the generative AI in life sciences market growth is regulatory uncertainty in the global market. Companies cannot fully rely on AI-generated outputs unless they are explainable, validated, traceable, and acceptable to regulators. Outputs generated by AI may vary depending on data quality, model design, and user prompts. This creates concern for pharmaceutical and biotechnology companies as inaccurate or poorly documented AI-generated information can affect submission quality, clinical decision-making, and compliance. As a result, many companies are adopting generative AI cautiously, mainly for assisted workflows rather than fully automated regulatory or clinical decision-making.

- For instance, in July 2025, in 2025, Applied Clinical Trials published an article titled ‘FDA’s Elsa AI Tool Raises Accuracy and Oversight Concerns,’ noting that the tool had accuracy issues, including false citations and data hallucinations. The report highlighted that although the tool was intended to speed up activities such as protocol reviews and label comparisons, its limitations prevented its use in formal regulatory assessments.

MARKET OPPORTUNITIES

Growing Adoption of Generative AI in Real-World Evidence and Pharmacovigilance to Offer Lucrative Growth Opportunities

The growing use of generative AI in real-world evidence and pharmacovigilance offers a strong growth opportunity for the global generative AI in life sciences market. Pharmaceutical and medical device companies need to monitor large volumes of patient records, safety reports, clinical notes, claims data, literature, and post-market signals to identify treatment outcomes and product safety risks. Generative AI can help companies summarize large, unstructured datasets, detect safety patterns, support adverse event reviews, and generate evidence-based insights more effectively. As regulators and life sciences companies place more focus on post-market safety, real-world outcomes, and faster evidence generation, demand for AI-enabled RWE and pharmacovigilance platforms is expected to increase.

- For instance, in April 2024, ArisGlobal launched LifeSphere NavaX, a generative AI solution designed to streamline pharmacovigilance case intake. The NavaX uses generative AI to support case intake efficiency and forms part of its LifeSphere safety ecosystem. This targets one of the most manual drug safety workflows, case intake, helping safety teams reduce processing effort, improve speed, and manage increasing adverse event data volumes more efficiently.

MARKET CHALLENGES

Integrating Generative AI with Legacy R&D and Clinical Systems Remains a Prominent Challenge

Integrating generative AI with legacy R&D and clinical systems remains a major challenge for the global market. Many pharmaceutical and biotechnology companies still depend on older laboratory information systems, clinical trial platforms, electronic health records, document repositories, and regulatory databases. These systems often store data in different formats and are not always designed to connect smoothly with modern AI models. As a result, companies may face delays in data harmonization, workflow integration, model validation, security review, and user adoption. This slows down large-scale deployment as generative AI cannot deliver strong value unless it can safely access high-quality, structured, and connected data across discovery, clinical, regulatory, and commercial workflows.

- For instance, in 2025, Pharmaphorum published an article titled ‘BIO 2025: As pharma deploys AI across the value chain, data remains a challenge’ and reported that pharma and biotech leaders identified data as a continuing challenge while deploying AI across the drug development value chain. The article noted that high-quality, AI-ready datasets are not consistently available across drug development, which underscores the challenge posed by disconnected systems. Fragmented data sets can slow the practical adoption of generative AI in life sciences.

Segmentation Analysis

By Component

Increasing Preference by Pharmaceutical Companies Boosted Software/Platforms Segment Growth

Based on component, the market is categorized into software/platforms and services.

The software/platforms segment dominated the market. Generative AI adoption in life sciences is mainly driven by scalable platforms that support drug discovery, research documentation, scientific data analysis, clinical workflows, and enterprise knowledge management. Pharmaceutical and biotechnology companies prefer software platforms as they can be integrated across multiple departments and reused across discovery, development, regulatory, and commercial functions. These factors result in platform providers experiencing stronger demand as companies seek reusable AI infrastructure. Due to these advantages, key companies also focus on new product launches that segment growth.

- For instance, in October 2025, Benchling launched Benchling AI, described as a command center for scientific AI that integrates agents and predictive models into scientists’ existing workflows, supporting the dominance of software- and platform-based adoption in life sciences.

The services segment is expected to grow at a CAGR of 30.39% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Cloud-based Segment Led due to Its Ability to Allow Faster Collaboration Between Pharma Companies and Research Partners

Based on deployment, the market is segmented into cloud-based, on-premise, and hybrid.

In 2025, the cloud-based segment captured the dominant global generative AI in life sciences market share, as generative AI models require substantial computing capacity, scalable storage, secure data access, and continuous model updates. Cloud-based platforms also allow faster collaboration between pharma companies, AI vendors, CROs, and research partners across geographies. As a result, cloud deployment is becoming the preferred model for generative AI solutions that need speed, flexibility, and enterprise scalability. These factors facilitate smoother collaboration among key operating entities, supporting the overall segment’s growth.

- For instance, in September 2025, Absci collaborated with Oracle Cloud Infrastructure and AMD to accelerate generative AI-driven drug discovery, with Oracle noting that cloud AI infrastructure would help improve performance, scalability, and biologics design cycles.

The hybrid segment is projected to grow at a CAGR of 32.10% during the forecast period.

By Technology

Greater Utilization of Large Language Models (LLMs) Across Medical Writing and Internal Knowledge Management Boosted Segment Growth

Based on technology, the market is segmented into large language models (LLMs), natural language processing (NLP), generative molecular/protein models, machine learning & deep learning, and others.

In 2025, the large language models (LLMs) segment dominated the market as many life sciences workflows depend on understanding, summarizing, generating, and comparing large volumes of text-based scientific and clinical information. LLMs are widely useful across medical writing, regulatory documentation, literature review, support for clinical trial protocols, safety narratives, medical affairs content, and internal knowledge management. Such broad applicability gives LLMs a larger adoption base than more specialized AI models, which are mainly used in narrow discovery or molecular design workflows. As a result, companies are adopting LLMs to improve productivity across both scientific and business functions.

- For instance, in July 2025, Merck & Co., Inc. expanded its internal generative AI solutions, including a platform that significantly reduces the time required to produce critical-path clinical study documents, demonstrating how LLM-based tools are being used to speed life sciences documentation workflows.

The generative molecular/protein models segment is projected to grow at a CAGR of 37.02% during the forecast period.

By Product Type

Standalone Segment Dominated as it Allows Companies to Evaluate Performance Before Deeply Integrating AI

Based on product type, the market is segmented into standalone and integrated.

The standalone segment held a dominant position in the market. Life sciences companies are still in the early-to-mid stage of generative AI adoption and prefer dedicated AI tools that can be tested, validated, and scaled for specific use cases before full enterprise integration. Standalone platforms are easier to deploy for targeted workflows such as molecule generation, scientific literature search, regulatory writing, or research copilots. This lowers implementation risk and allows companies to evaluate performance before deeply integrating AI into existing R&D, clinical, or commercial systems. As a result, standalone solutions have gained stronger initial adoption across pharma and biotech users.

- For instance, in May 2025, Latent Labs announced a multi-year collaboration with AWS to scale generative AI for life sciences and put AI directly in the hands of biologists, pharma, and biotech innovators, supporting the use of dedicated AI platforms for specific scientific workflows.

The integrated segment is projected to grow at a CAGR of 40.86% during the forecast period.

By Application

Drug Discovery & Design Segment Led the Market due to Heavy Investment in AI-enabled Discovery Platforms

Based on application, the market is segmented into drug discovery & design, clinical trial design & operations, regulatory writing & submissions, medical affairs & scientific content, pharmacovigilance, commercial & market access content, and others.

The drug discovery & design dominated the application segment. Drug discovery is a core business application as generative AI delivers the greatest impact by helping reduce discovery time, improve molecule generation, support target identification, and lower early-stage R&D risk. Generative AI supports this need by creating and optimizing new molecules or biologics based on desired properties. As a result, pharma and biotech companies are investing heavily in AI-enabled discovery platforms to improve pipeline productivity.

- For instance, in November 2025, Insilico Medicine announced a research and licensing collaboration with Eli Lilly to combine Insilico’s Pharma.AI platforms with Lilly’s development and disease expertise to discover and advance innovative therapies.

The pharmacovigilance segment is projected to grow at a CAGR of 37.44% over the study period.

By End User

Pharmaceutical and Biotechnology Companies Segment Led due to their Ability to Improve Commercialization Workflows

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs, academic & research institutes, medtech/diagnostics companies, and others.

Pharmaceutical and biotechnology companies held the major market share. These organizations possess the strongest need, financial resources, and data availability to implement generative AI solutions across the life sciences value chain. These companies face high R&D costs, complex pipelines, rising clinical trial expenses, and pressure to improve speed from discovery to commercialization. Generative AI helps them improve target discovery, molecule design, trial planning, documentation, medical affairs, and commercialization workflows. As a result, pharma and biotech companies are leading adoption compared with CROs, academic institutes, and medtech firms.

- For instance, in June 2025, NVIDIA announced a collaboration with Novo Nordisk and Denmark’s DCAI to advance drug discovery using AI factories and generative and agentic AI use cases, demonstrating that major pharmaceutical companies are actively investing in generative AI to accelerate R&D.

The medtech/diagnostics companies segment is projected to grow at a CAGR of 39.19% over the forecast period.

Generative AI in Life Sciences Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Generative AI in Life Sciences Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.42 billion and maintained its leading position in 2025 at USD 0.55 billion. The market is growing in North America due to strong AI adoption by pharmaceutical, biotechnology, and healthcare technology companies. The region has advanced cloud infrastructure, high R&D spending, and early use of generative AI in drug discovery, clinical trials, and regulatory workflows.

U.S. Generative AI in Life Sciences Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is poised to reach around USD 0.69 billion in 2026, accounting for roughly 43.12% of the global market sales.

Europe

Europe is projected to grow at 34.21% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.38 billion in 2026. Europe is witnessing growth as pharmaceutical companies, research institutes, and healthcare organizations increasingly use generative AI to improve scientific research, clinical development, and regulatory efficiency. The region’s focus on data governance and responsible AI is driving demand for secure, compliant AI platforms.

U.K. Generative AI in Life Sciences Market

The U.K.’s market is poised to reach around USD 0.08 billion in 2026, representing roughly 5.26% of the global sales.

Germany Generative AI in Life Sciences Market

Germany's market is projected to reach approximately USD 0.08 billion in 2026, equivalent to around 4.82% of the global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.38 billion in 2026 and secure the position of the third-largest region in the market. Asia Pacific is growing rapidly due to expanding pharmaceutical manufacturing, rising biotech investment, and increasing digital transformation across healthcare and life sciences. The region is investing in AI-enabled drug discovery and clinical research capabilities and creating strong demand for scalable generative AI.

Japan Generative AI in Life Sciences Market

The Japanese market in 2026 is estimated to reach around USD 0.08 billion, accounting for approximately 4.91% of the global revenues.

China Generative AI in Life Sciences Market

China's market is projected to be among the largest worldwide, with 2026 revenues standing at around USD 0.13 billion, accounting for approximately 7.88% of global sales.

India Generative AI in Life Sciences Market

The Indian market in 2026 is estimated to reach around USD 0.05 billion, accounting for roughly 3.25% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is likely to reach a valuation of USD 0.07 billion in 2026. Life sciences companies in the region are adopting digital tools to improve clinical research, patient data analysis, and operational efficiency. In the Middle East & Africa, the GCC is set to reach USD 0.01 billion in 2026.

South Africa Generative AI in Life Sciences Market

The South African market is projected to reach approximately USD 0.004 billion in 2026, accounting for roughly 0.24% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Scientific AI Models to Strengthen Their Market Presence

The global generative AI in life sciences market is moderately fragmented, with the presence of large technology companies, life sciences software providers, AI-native drug discovery firms, and cloud infrastructure players. Key companies such as NVIDIA Corporation, Microsoft Corporation, Oracle Corporation, IQVIA Inc., Veeva Systems Inc., Benchling, Inc., Insilico Medicine, Recursion Pharmaceuticals, Tempus AI, and Certara, Inc. account for a significant share of the market. These companies have a strong presence across drug discovery, clinical development, regulatory writing, medical affairs, real-world evidence, and scientific data management.

- For instance, in January 2026, Oracle launched the Oracle Life Sciences AI Data Platform, a generative AI-enabled platform designed to unify life sciences data and support R&D, clinical trials, post-market safety, and commercialization workflows. The development strengthened Oracle’s position in the market by supporting the use of AI and agentic intelligence across the life sciences value chain.

Other notable participants in the global market include Schrödinger, Inc., Owkin, Inc., TetraScience, Inc., Anthropic PBC, Google Cloud, and Absci Corporation. These companies are expected to focus on product innovation, scientific AI models, enterprise-grade cloud platforms, and domain-specific generative AI solutions to strengthen their market presence during the forecast period. The market remains highly innovation-driven, with competition increasingly shifting toward multimodal AI models, secure data integration, regulatory-grade outputs, and end-to-end AI workflows.

LIST OF KEY GENERATIVE AI IN LIFE SCIENCES COMPANIES PROFILED

- NVIDIA Corporation (U.S.)

- IQVIA Inc. (U.S.)

- Oracle Corporation (U.S.)

- Veeva Systems Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Alphabet Inc. (U.S.)

- Benchling, Inc. (U.S.)

- Insilico Medicine (U.S.)

- Recursion Pharmaceuticals, Inc. (U.S.)

- Tempus AI, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Oracle launched its Oracle Life Sciences AI Data Platform, a generative AI-enabled solution designed to empower pharmaceutical, medical device, research, and life sciences organizations to accelerate outcomes across R&D, clinical trials, post-market safety, and commercialization.

- January 2026: Hippocratic AI acquired Grove AI and entered into a strategic collaboration with Boston Consulting Group (BCG). These developments strengthened the company's capabilities in deploying safe, scalable, and clinically grounded generative AI across the biopharma and medtech value chain, from R&D and clinical trials to commercialization, and improved patient engagement.

- December 2025: Accenture invested in Ryght AI, a platform provider that modernizes the design and execution of clinical research for the life sciences industry. This investment enabled life sciences and clinical research companies to bring new treatments to patients faster by combining agentic AI with enterprise technology solutions.

- October 2025: Owkin, Inc launched K Pro, its co-pilot bringing advanced agentic AI to biomedical research and drug development. K Pro helps pharmaceutical companies and biotechs make smarter decisions across the discovery and development pipeline, increase clinical success rates, and deliver decision-grade, data-driven biological insights fast enough to change program trajectories.

- June 2024: Cognizant launched a set of healthcare large language model (LLM) solutions on Google Cloud's generative AI (genAI) Technology, including the company's Vertex AI platform and Gemini models, aimed at redesigning healthcare administrative processes and improving experiences.

REPORT COVERAGE

The report provides a comprehensive global generative AI in life sciences market. It covers detailed market analysis across component, deployment, technology, product type, application, and end user. It examines the demand for generative AI solutions used in drug discovery and design, clinical trial design and operations, regulatory writing and submissions, medical affairs and scientific content, pharmacovigilance, commercial and market access content, and other life sciences workflows. The study further assesses the role of software/platforms, services, cloud-based deployment, on-premise models, hybrid deployment, large language models, natural language processing, generative molecular/protein models, machine learning and deep learning, standalone products, and integrated solutions in current market adoption. The report also provides regional insights across key geographies, competitive landscape analysis, company profiling, recent developments, and evaluation of the major factors driving, restraining, and shaping future opportunities in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 35.52% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Product Type, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.18 billion in 2025 and is projected to reach USD 18.20 billion by 2034.

In 2025, the market value stood at USD 0.55 billion.

The market is expected to grow at a CAGR of 35.52% over the forecast period.

By component, the software/platforms segment led the market.

The increasing volume of genomic, clinical, and molecular data across life sciences is the key factor driving market growth.

NVIDIA Corporation, IQVIA Inc., Oracle Corporation, and Veeva Systems Inc. are among the major players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us