Genomic Data Platforms Market Size, Share & Industry Analysis, By Component (Software and Services {Implementation & Migration Services, Bioinformatics & Workflow Services, Managed Services, Data Curation & Quality Services, Compliance & Security Services and Others}), By Deployment (On-Premise, Cloud-based & Hybrid), By Technology (PCR, Next Generation Sequencing, Microarray, Sanger Sequencing & Others), By Application (Clinical Diagnostics, Drug Discovery, Clinical Trials, Precision Medicine, Population Genomics, Pathogen Genomics & Others), By End User, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

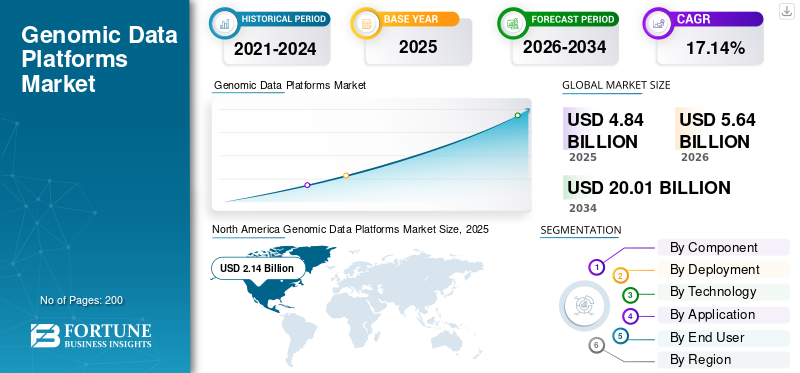

The genomic data platforms market size was valued at USD 4.84 billion in 2025. The market is projected to grow from USD 5.64 billion in 2026 to USD 20.01 billion by 2034, exhibiting a CAGR of 17.14% during the forecast period. North America dominated the global genomic data platforms market with a market share of 44.21% in 2025.

The market is reffered to software platforms that includes managed services what helps organizations ingest, store, govern, compute on, and share genomic as well as multi-omics data at scale. In recent years, this marketspace is witnessing a strong growth driven by factors such as high precision medicine adoption, AI/ML analytics, and regulatory focus on secure data environments.

Moreover, major players such as Illumina Inc., QIAGNEN, Microsoft and others are operating in the market, with emphasis on introducing innovative solutions to meet the growing product demand.

Download Free sample to learn more about this report.

Genomic Data Platforms Market Key Takeaways

- 2025 Market Size: USD 4.84 Billion

- 2026 Market Size: USD 5.64 Billion

- 2034 Forecast Market Size: USD 20.01 Billion

- CAGR: 17.14% from 2026–2034

- North America dominated the genomic data platforms market with a 44.21% share in 2025.

- The services segment is anticipated to grow at a CAGR of 15.27% during the forecast period.

- The hybrid segment is anticipated to grow at a CAGR of 17.11% during the forecast period.

North America

North America led the global market with revenue of USD 2.14 billion in 2025.

Europe

Europe is estimated to grow at a CAGR of 16.82% during the study period.

Asia Pacific

Asia Pacific is projected to reach a market value of USD 1.34 billion in 2026.

U.S.

The market is analytically approximated to reach USD 2.27 billion in 2026.

Japan

The market is estimated at USD 0.19 billion in 2026, accounting for approximately 3.4% of global revenue.

Read More

GENOMIC DATA PLATFORMS MARKET TRENDS

Rising Investments in Cloud Infrastructure is a Significant Trend Observed in Market

In recent years, the market is witnessing a significant increase in investments for cloud infrastructure. Genomics researchers are generating larger datasets especially NGS/multi-omics that are expensive to store, move and analyze on local servers. More capacity provided by cloud infrastructure improves the availability of compliant cloud services such as security, logging and access controls, which reduces barriers for regulated clinical genomics and cross-site collaboration. This pushes buyers toward cloud and hybrid deployments, and increases demand for managed services to run pipelines reliably at scale. These factors are supporting the overall genomic data platforms market growth.

- For instance, in November 2025, Amazon announced plans to invest an additional USD 15 billion in Northern Indiana to build data center campuses in turn adding 2.4 gigawatts of capacity, directly reflecting the scale-up of cloud infrastructure that supports data-intensive workloads such as genomics.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Growth in Genomic Sequencing Generating Large Volumes of Data is Propelling Market Growth

Rapid growth in genomic sequencing is a major driver for the market growth. This is due to higher-throughput instruments and falling per-sample costs that are pushing labs to run more samples frequently, and across various use cases such as oncology, rare disease, population genomics, pathogen surveillance and others. As genomic sequences volumes rise, data teams also need collaboration features, lineage/audit trails and secure sharing to support multi-site trials and regulated clinical reporting. Thus, sequencing growth directly increases demand for platform capacity and operational help, especially for workflow automation and data management. All these factors cumulatively drive the market growth.

- For instance, in January 2025, Illumina announced updates to the NovaSeq X Series, highlighting it as its most rapidly adopted and utilized high-throughput sequencing platform.

MARKET RESTRAINTS

High Implementation Cost for Integrated Platforms to Limit Market Growth

High implementation cost is a key restraint for the market as integrated genomic data platforms usually require end-to-end change, rather than a software install. Buyers often need to connect the platform with sequencers, LIMS, EHR/clinical systems, identity & access management, and downstream analytics, with migrate legacy pipelines and historical datasets. These costs can delay procurement decisions, limit adoption to larger institutions, or push customers toward phased rollouts. This results in limiting the market growth to certain extent.

- For instance, in November 2025, Genomics England published a contract award notice on for a “Target Cloud Platform Assessment and optional Implementation” engagement awarded to Accenture (U.K.) with a stated total value of USD 1.204 million, explicitly reflecting the real-world cost of assessing, redesigning, and implementing scalable cloud-platform operations.

MARKET OPPORTUNITIES

Increasing Adoption of Precision Medicine and Clinical Genomics to Offer Market Growth Opportunities

Increasing adoption of precision medicine and clinical genomics is a major opportunity for the market growth. As clinical genomics expands, providers need to manage high volumes of sensitive patient genomic and phenotype data with auditability and traceability. This creates demand for platforms that can standardize pipelines, automate QC, speed up interpretation, and support clinical-grade reporting. It also increases the need for secure sharing across hospital networks and with biopharma/CRO partners for evidence generation and trial matching. All these factors would drive the market growth in the coming years.

- For instance, in January 2026, SOPHiA GENETICS and MD Anderson announced a strategic collaboration to accelerate AI-driven precision oncology, aiming to develop tools to analyze and interpret diagnostic results and translate them into clinical practice.

MARKET CHALLENGES

Data Privacy and Cross-Border Data Transfer Restrictions Pose a Significant Challenge to Market Growth

Data privacy and cross-border data transfer restrictions are a major challenge for the market. As genomic datasets are inherently identifiable and often classified as sensitive health data. Many customers need to comply with residency rules and strict access/audit requirements, which complicates centralized global cloud deployments. This can slow purchasing decisions, lengthen sales cycles and push buyers toward hybrid/sovereign cloud options. All the factors cumulatively impact the market growth.

- For instance, in November 2025, Microsoft announced expanded digital sovereignty capabilities for Europe and Switzerland, including expanded services within the EU Data Boundary and enhanced private cloud infrastructure options, directly reflecting how residency and cross-border transfer concerns are shaping cloud platform design.

Segmentation Analysis

By Component

Rising Demand for Software Solutions to Propel Segmental Growth

Based on the component, the market is divided into software and services.

The software segment is anticipated to capture the largest global genomic data platforms market share. This is due to genomic data platforms are primarily monetized through recurring subscriptions/licenses tied to storage, workflow execution, user seats and compute orchestration. Moreover, as sequencing volumes rise, the demand for software also increases. Owing to this, operating players are also focusing on launching new products in the market.

- For instance, in January 2026, Lifebit announced the release of Version 4 of its platform - Agentic Federated Platform.

The services segment is anticipated to rise with a CAGR of 15.27% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Shift Toward Cloud-based Solutions to Enhance Segmental Growth

On the basis of deployment, the market is divided into on-premise, cloud-based and hybrid.

In 2025, the global market was dominated by the cloud-based segment with leading market share. Cloud-based solutions enables labs and biopharma scale storage and compute on-demand as sequencing volumes and workflow complexity rise, without large upfront capex for servers and IT maintenance. Additionally, cloud environments also make it easier to run burst compute for alignment/variant calling and then scale down, improving cost efficiency versus permanently over-provisioned on-premise infrastructure. Furthermore, the segment is set to hold 44.0% share in 2026.

- For instance, in April 2025, AWS announced Elastic Throughput enhancements for AWS HealthOmics dynamic run storage, specifically to improve scaling of storage performance for workflow needs.

The hybrid segment is anticipated to rise with a CAGR of 17.11% over the forecast period.

By Technology

High Volume of Genomic Data Generation Propelled Next Generation Sequencing Segmental Dominance

Based on the technology, the market is divided into PCR, next generation sequencing, microarray, sanger sequencing and others.

In 2025, the next generation sequencing segment led with the largest market share. It generates the largest and fastest-growing volumes of genomic data across research and clinical use cases. Additionally, NGS workflows are also more complex, so labs and biopharma rely on platforms to standardize pipelines, track provenance and ensure reproducibility across sites. Furthermore, the segment is set to hold 75.7% share in 2026.

- For instance, in February 2025, Roche announced a new class of next-generation sequencing based on its Sequencing by Expansion (SBX) technology.

The PCR segment is anticipated to rise with a CAGR of 11.57% over the forecast period.

By Application

High Demand in Diagnostic Applications Supported Clinical Diagnostics Segmental Dominance

Based on the application, the market is divided into clinical diagnostics, drug discovery, clinical trials, precision medicine, population genomics, pathogen genomics and others.

In 2025, the clinical diagnostics segment dominated with the largest market share. The segment growth is boosted by factors including high sample data creation, requirement of fast turnaround time, consistent QC and other. Moreover, diagnostic labs and hospital networks run high-throughput, repeatable testing where every incremental sample creates ongoing demand for secure storage, standardized pipelines and reporting. Furthermore, the segment is set to hold 27.0% share in 2026.

- For instance, in January 2026, QIAGEN stated its 2026 priorities that include expanding AI-enabled software and multilingual automation for clinical reporting, aiming to accelerate precision in clinical decision-making for oncology and hereditary disease diagnostics.

The precision medicine segment is anticipated to rise with a CAGR of 19.03% over the forecast period.

By End User

Increasing Focus on Genomic Research by Pharmaceutical & Biotechnology Companies Supported their Leading Position

On the basis of end user, the market is segmented into pharmaceutical & biotechnology companies, clinical laboratories & diagnostic centers, CROs & CDMOs, and others.

In 2025, the global market was dominated by pharmaceutical & biotechnology companies. These end users run the largest and most continuous genomics workloads across discovery, translational research and clinical development. They also manage multi-site studies and partner ecosystems, and hence need enterprise-grade security, audit trails, and controlled data sharing across internal teams, CROs and collaborators. This results in high demand for genomic data platforms from these companies. Furthermore, the segment is set to hold 34.4% share in 2026.

- For instance, in January 2026, Tempus announced a record Total Contract Value of more than USD 1.1 billion and stated that during 2025 it signed data agreements with more than 70 customers, including large pharmaceutical companies such as AstraZeneca, GlaxoSmithKline. This highlighted the scale of biopharmaceutical demand for genomic/clinical data platform capabilities.

In addition, CROs & CDMOs are projected to grow at a 19.04% CAGR during the forecast period

Genomic Data Platforms Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Genomic Data Platforms Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market size was valued at USD 1.83 billion in 2024 and led the global market. The region also dominated the global market in 2025, with USD 2.14 billion revenue share. Large adoption of genomic platforms, presence of major sequencing hubs and strong cloud provider presence in the region are some of the prominent factors driving the regional market growth.

U.S. Genomic Data Platforms Market

The U.S. market captured a leading share of the North American market and can be analytically approximated at around USD 2.27 billion in 2026, accounting for roughly 40.3% of global market.

Europe

Europe market is estimated to grow at a CAGR of 16.82% during the study period. The region is anticipated to become a second highest among all regions. Europe’s market growth is supported by large national genomics initiatives, coupled with strong regulatory emphasis on data governance.

U.K. Genomic Data Platforms Market

The U.K. market in 2026 is estimated at around USD 0.29 billion, representing roughly 5.2% of global revenues.

Germany Genomic Data Platforms Market

Germany market size is projected to reach approximately USD 0.33 billion in 2026, equivalent to around 5.9% of global sales.

Asia Pacific

Asia Pacific market size is projected to be valued at USD 1.34 billion in 2026 and secure the position of the third-largest region globally. Asia Pacific growth is supported by key factors such as increasing investment in genomics research, developing infrastructure and growing sequencing capacity in Asian countries, especially in China, India and Japan.

Japan Genomic Data Platforms Market

The Japan market in 2026 is estimated at around USD 0.19 billion, accounting for roughly 3.4% of global revenues.

China Genomic Data Platforms Market

China’s market is projected to reach revenues of around USD 0.41 billion in 2026, representing roughly 7.3% of global sales.

India Genomic Data Platforms Market

The India’s market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 2.9% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions would grow at a moderate rate throughout the forecast period. The Latin America market size is set to reach a valuation of USD 0.26 billion in 2026. Factors contributing to the growth in these regions include emerging adoption, increasing number of specialized genomics projects and growing collaborations in these countries. The GCC market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Innovation by Key Entities to Strengthen Market Share

The global market represents a semi-consolidated competitive landscape. Different prominent players are focusing on end-to-end multi-omics enablement, tighter enterprise interoperability, and regulatory-ready security to support clinical genomics and precision medicine programs to maintain their market share. These companies include Illumina Inc., QIAGNEN, DNAnexus, Inc. and Microsoft.

- For instance, in January 2026, Illumina announced the release of Illumina Connected Multiomics, a cloud-based research software platform designed to analyze and visualize multiomic and multimodal data at scale.

Other key players in the competitive landscape include Velsera Inc., SOPHiA GENETICS, Lifebit Biotech Inc., among others. Their strategies typically focus on prevalidated workflows, federated analysis, and AI-assisted interpretation.

LIST OF KEY GENOMIC DATA PLATFORMS COMPANIES PROFILED

- Illumina Inc. (U.S.)

- DNAnexus, Inc. (California)

- Velsera Inc. (U.S.)

- SOPHiA GENETICS. (U.S.)

- Lifebit Biotech Inc. (U.K.)

- QIAGEN (Germany)

- Amazon Web Services, Inc. (U.S.)

- Oxford Nanopore Technologies plc. (U.K.)

- Microsoft (U.S.)

- GeneDx , LLC (Fabric Genomics, Inc.) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: SOPHiA GENETICS and Complete Genomics announced collaboration to launch and co-market MSK-ACCESS/MSK-IMPACT powered with SOPHiA DDM on Complete Genomics’ sequencing platform.

- September 2025: DNAnexus announced a collaboration with Oracle Health to integrate genomic data capabilities into Oracle Health clinical applications, enabling clinicians to access and interpreted genomics alongside medical history.

- May 2025: Illumina Inc. launched DRAGEN v4.4, highlighting clinical oncology apps, multiomics pipeline support and performance/accuracy improvements.

- May 2025: QIAGEN announced the acquisition of Genoox, adding AI-powered interpretation software (Franklin) to strengthen its clinical genomics informatics stack.

- February 2025: Oxford Nanopore announced expanded collaboration with 10x Genomics to enable compatibility for single-cell applications and deeper transcriptomics insights.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.14% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Deployment, Technology, Application, End User, and Region |

|

By Component |

· Software · Services o Implementation & Migration Services o Bioinformatics & Workflow Services o Managed Services o Data Curation & Quality Services o Compliance & Security Services o Others |

|

By Deployment |

· On-Premise · Cloud-based · Hybrid |

|

By Technology |

· PCR · Next Generation Sequencing · Microarray · Sanger Sequencing · Others |

|

By Application |

· Clinical Diagnostics · Drug Discovery · Clinical Trials · Precision Medicine · Population Genomics · Pathogen Genomics · Others |

|

By End User |

· Pharmaceutical & Biotechnology Companies · Clinical Laboratories & Diagnostic Centers · CROs & CDMOs · Others |

|

By Region |

· North America (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o U.S. o Canada · Europe (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.84 billion in 2025 and is projected to reach USD 20.01 billion by 2034.

In 2025, the market value stood at USD 2.14 billion.

The market is expected to exhibit a CAGR of 17.14% during the forecast period of 2026-2034.

By component, the software segment is expected to lead the market.

High data volumes from sequencing, precision medicine adoption, AI/ML analytics, and regulatory focus on secure data environments are primarily driving market expansion.

Illumina Inc., QIAGNEN, DNAnexus, Inc. and Microsoft are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us