Glioblastoma Drugs Market Size, Share & Industry Analysis, By Drug (Temozolomide, Bevacizumab, Carmustine, Lomustine, Procarbazine, and Others), By Drug Class (Alkylating Agents, VEGF/Angiogenesis Inhibitors, Nitrosoureas, Platinum Compounds, Topoisomerase Inhibitors, and Others), By Age Group (Pediatric and Adults), By Type (Branded and Generic), By Therapy (Targeted Therapy, Immunotherapy, Chemotherapy, and Others), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, and Others), and Regional Forecast, 2026-2034

Glioblastoma Drugs Market Size and Future Outlook

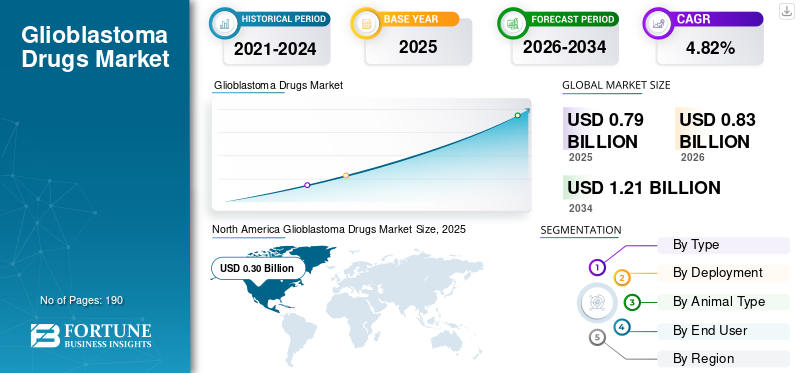

The global glioblastoma drugs market size was valued at USD 0.79 billion in 2025. The market is projected to grow from USD 0.83 billion in 2026 to USD 1.21 billion by 2034, exhibiting a CAGR of 4.82% during the forecast period. North America dominated the glioblastoma drugs market with a market share of 37.97% in 2025.

The global market is expected to witness steady growth driven by the rising prevalence of brain cancers, creating a strong need for better therapeutic options. The continued use of standard chemotherapy supports the market growth, rising research activity in targeted and immune-based therapies, and combination treatment approaches for recurrent and newly diagnosed patients. Key operating companies are investing in developing pipeline candidates to improve efficacy, extend progression-free survival, and address relapse. This continued innovation is expected to support market expansion over the coming years.

- For instance, in March 2026, BioLineRx initiated a Phase 1/2a study of GLIX1 for the treatment of glioblastoma. The GLIX1 is a first-in-class, oral small molecule targeting the DNA damage response in glioblastoma and other solid tumors, developed in collaboration with Hemispherian. Such pipeline advancement is expected to support overall market growth.

Furthermore, leading players in the industry, such as Merck & Co., Inc., Genentech, Inc. (F. Hoffmann-La Roche Ltd), and Teva Pharmaceutical Industries Ltd., are operating in the market to expand their pipeline and address unmet demand.

Download Free sample to learn more about this report.

GLIOBLASTOMA DRUGS MARKET TRENDS

Increasing Development of Immunotherapy-Based Candidates Is Emerging as a Key Market Trend

The prominent global market trend observed is the increasing development of immunotherapy-based candidates. The treatment benefits from currently available drug options in glioblastoma remain limited, especially in recurrent disease. These factors are pushing key companies to invest in cancer vaccines, cell-based immunotherapies, checkpoint-oriented approaches, and other immune-mediated treatments that may offer better disease control and longer survival. As more developers move these candidates into mid-stage and late-stage studies, the market is witnessing a broader shift toward immune-based innovation. This trend is expected to strengthen future product differentiation and expand the commercial potential of the market.

- For instance, in December 2025, Imvax announced positive top-line data from its Phase 2b clinical trial of IGV-001 in newly diagnosed glioblastoma. The IGV-001 is described as a patient-specific, whole tumor cell-derived immunotherapy. Such advancing immunotherapy-based treatment candidates pipeline progress supports the growth potential.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

High Unmet Need for Effective Glioblastoma Therapies is Driving Market Growth

A key factor driving growth in the global glioblastoma drugs market growth is the high unmet need for effective therapies. Currently available treatment options offer limited survival benefits and do not adequately control disease recurrence. These factors are pushing drug developers to invest in new candidates that can improve efficacy, secure regulatory support, and address a patient population with very few therapeutic alternatives. As more companies advance innovative programs in glioblastoma, the market is gaining deeper pipelines and greater commercial interest, further deepening market growth.

Moreover, key companies are focusing on regulatory approval and new product launches for their glioblastoma offerings to strengthen their market position.

- For instance, in October 2025, Myosin Therapeutics received Fast Track designation from the U.S. FDA for MT-125 for glioblastoma. The candidate had previously granted Orphan Drug Designation to MT-125 for malignant gliomas, including GBM, highlighting regulatory support for new therapies for this high-need disease area. Such development reflects the need for better glioblastoma treatments, which is encouraging pipeline advancement and supporting market growth.

MARKET RESTRAINTS

High Recurrence and Rapid Treatment Resistance Are Restraining Market Growth

One of the key factors restraining market growth is the rapid development of treatment resistance. This reduces the ability of existing glioblastoma drugs to deliver a durable clinical benefit. When patients relapse quickly after standard treatment, the treatment window becomes shorter, resulting in the value of current marketed therapies being more limited. Additionally, resistance to temozolomide and other treatments makes it more difficult for new drug candidates to demonstrate strong survival improvements in clinical trials. Due to this, recurrence and resistance increase the development risk, erode physician confidence in long-term benefits, and slow the pace of market expansion.

- For instance, in May 2025, Springer Nature Link published an abstract titled ‘Glioblastoma multiforme: an updated overview of temozolomide resistance mechanisms and strategies to overcome resistance.’ The article noted that glioblastoma recurs nearly universally after standard treatment. These findings highlight how current therapies struggle to deliver sustained benefit and remain major restraints on market growth.

MARKET OPPORTUNITIES

Strong and Active Pipeline Development is Creating Market Growth Opportunities

Strong and active pipeline development is creating market growth opportunities as glioblastoma remains a high-unmet-need cancer area where currently available therapies still deliver limited long-term benefit. This is encouraging companies to advance new drug candidates with different mechanisms of action, improved brain-penetration strategies, and more targeted treatment approaches. As more investigational therapies enter clinical studies, the market gains a broader pipeline of future products and greater potential for partnerships, licensing, and commercialization. It also increases the chance that new therapies may address recurrent disease more effectively, where treatment needs remain especially high. Owing to this, a deeper and more active pipeline is opening up long-term expansion opportunities for the market.

- For instance, in August 2025, Lantern Pharma’s subsidiary Starlight Therapeutics announced U.S. FDA clearance of an IND for a Phase Ib/2a glioblastoma multiforme (GBM) trial. The program would evaluate its investigational candidate in GBM, showing how developers are continuing to push new therapies into the clinical pipeline for this disease. This kind of progress highlights why strong pipeline activity is being witnessed as a major market growth opportunity.

MARKET CHALLENGES

Strong Tumor Heterogeneity is Creating a Major Challenge for Market Growth

The global market continues to face significant challenges as glioblastoma is not a uniform disease and exhibits substantial variation across patients, tumor regions, and cellular states. This complexity makes treatment response less predictable and reduces the likelihood that a single drug approach will work broadly across the patient population. As a result, companies developing glioblastoma therapies face higher scientific risk, more difficult trial design, and greater pressure to identify subgroups that may respond better to treatment. This is slowing market expansion and making it more dependent on highly differentiated innovation.

- For instance, a 2025 Nature Genetics study reported that cellular heterogeneity across and within glioblastoma tumors may drive therapeutic resistance, while a 2025 Communications Medicine article described glioblastoma as a highly heterogeneous brain tumor that poses challenges for precision therapies and patient stratification in clinical trials. These published findings directly highlight why tumor heterogeneity remains a major market challenge for glioblastoma drug developers.

Segmentation Analysis

By Drug

Increasing Use of Temozolomide in Treatment Protocol to Lead the Segmental Growth

Based on the drug, the market is categorized into temozolomide, bevacizumab, carmustine, lomustine, procarbazine, irinotecan, and others.

Among these, the temozolomide segment accounted for the largest share in the market. Temozolomide remains one of the core drugs, used in the standard first-line glioblastoma treatment, especially in combination with radiotherapy and later as maintenance therapy. It is deeply embedded in treatment protocols; physicians are more familiar with its dosing, sequencing, and safety profile than with newer investigational options. These factors result in wider clinical use, stronger prescription continuity, and more stable revenue contribution, leading to dominance of the segment.

- For instance, in March 2025, Laminar Pharma presented positive open-label progression-free survival data for LAM561 in combination with standard-of-care radiotherapy and temozolomide in newly diagnosed glioblastoma patients. This shows that even new therapies are still being developed around temozolomide, reinforcing its role as the leading product in the market.

The others segment is expected to grow at a CAGR of 8.50% over the global glioblastoma drugs market forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Drug Class

Robust Reliance on Alkylating Agents for Glioblastoma to Boost Segmental Growth

Based on drug class, the market is segmented into alkylating agents, VEGF/angiogenesis inhibitors, nitrosoureas, platinum compounds, topoisomerase inhibitors, immune checkpoint inhibitors, and others.

In 2025, the alkylating agents accounted for the largest revenue share among drug classes. The drug class includes temozolomide, which remains the backbone chemotherapy for glioblastoma. Since current treatment standards rely heavily on temozolomide-based regimens, the alkylating class benefits directly from the broadest clinical acceptance and the highest treatment familiarity. These factors increase prescribing confidence and routine use. Additionally, novel product launches by key companies and the regulatory approvals strengthen their market position.

- For instance, in May 2025, Camber Pharmaceuticals launched Temozolomide Capsules, USP, an alkylating drug indicated for newly diagnosed glioblastoma along with radiotherapy and maintenance treatment. This directly supports the continued commercial importance of the alkylating agent class in the market.

The immune checkpoint inhibitors segment is projected to grow at a CAGR of 11.92% during the forecast period.

By Age Group

Large Adult Patient Pool to Reinforce Dominance in the Segment

Based on age group, the market is segmented into pediatric and adult.

In 2025, the adult segment dominated the market. Adults dominated the market as glioblastoma primarily affects adults, naturally creating a larger treated patient base in this segment. Since the disease burden is much higher in adults than in pediatric patients, more drug demand, more clinical trial enrollment, and more commercial focus are concentrated in adult care settings. In addition, most approved and pipeline glioblastoma treatment strategies are developed primarily for adult patients, further strengthening revenue concentration in this age group. Due to this larger incidence pool and stronger treatment activity, the adult segment is likely to remain the leading contributor to the market.

- For instance, in July 2025, Diakonos Oncology announced that the first patient was dosed in its Phase 2 trial of DOC1021 (dubodencel) for glioblastoma. This reflects why adult patients remain the main focus of drug development and market demand.

In addition, the pediatric segment is projected to grow at a CAGR of 7.61% during the study period.

By Type

Greater Affordability and Access Provided by Generics to Fuel the Segment Growth

Based on type, the market is segmented into branded and generic.

Based on type, generics accounted for the largest glioblastoma drugs market share during the forecast period. Glioblastoma treatment still depends heavily on established chemotherapy molecules, especially temozolomide, where generic availability has expanded access and reduced treatment costs. As hospitals and oncology providers are highly cost-conscious in routine cancer treatment, lower-cost generic options are often preferred where clinical outcomes are already well understood. This increases prescription volume for generic products and makes them more widely available than branded therapies in many standard-use settings. In addition, the limited number of breakthrough branded drug alternatives in glioblastoma has allowed generic chemotherapy products to retain strong market relevance.

- For instance, in June 2023, Enzene Biosciences announced the India launch of Bevacizumab.

In addition, the branded segment is projected to grow at a CAGR of 3.10% during the study period.

By Therapy

Increasing Use of Chemotherapy as First-Line Treatment to Lead Segmental Growth

Based on the therapy, the market is segmented into targeted therapy, immunotherapy, chemotherapy, and others.

Among these, chemotherapy is likely to dominate the market as it remains the most established and routinely used drug-based treatment approach in glioblastoma, with temozolomide continuing to serve as the standard chemotherapy backbone. Since immunotherapy and targeted therapy have not yet displaced standard chemoradiation in routine care, chemotherapy continues to account for the largest share of actual treatment use. It also benefits from stronger clinical familiarity, broader treatment eligibility, and longstanding integration into frontline treatment pathways. Moreover, many experimental therapies are still being tested in combination with chemotherapy instead of replacing it. Due to this continued dependence on standard chemoradiation, chemotherapy is likely to remain the dominant therapy segment.

- For instance, in May 2025, Sapience Therapeutics announced an oral presentation at the ASCO 2025 Annual Meeting featuring Phase 2 results for lucicebtide, and noted that an ongoing substudy is evaluating the therapy in combination with radiation and temozolomide in newly diagnosed glioblastoma. This shows that chemotherapy remains central even as newer treatment strategies are being developed.

The immunotherapy segment is projected to grow at a CAGR of 12.72% over the study period.

By Route of Administration

Ease of Oral Medicine Dispense to Favor Growth in the Segment

Based on the route of administration, the market is segmented into oral and parenteral.

By route of administration, the oral drugs dominated the market. Oral dominated the market as temozolomide, the key chemotherapy used in glioblastoma, is widely used in capsule form, making oral administration the most established drug-delivery route in routine treatment. As oral treatment is easier to prescribe, dispense, and continue during maintenance therapy than repeated parenteral administration, it supports greater convenience for both providers and patients. This improves treatment continuity and makes oral therapy more practical within long oncology treatment cycles. In addition, several newer glioblastoma drug candidates are also being designed as oral agents, which supports the continued strength of this route. As a result, oral administration is likely to lead the market by route.

- For instance, in September 2025, NeOnc Technologies announced that it had received FDA authorization to proceed with a Phase II clinical trial of NEO212, a next-generation oral brain cancer therapy. This highlights the continued commercial and development focus on oral treatment approaches in glioblastoma.

The parenteral segment is projected to grow at a CAGR of 5.86% over the study period.

By Distribution Channel

Increasing Demand in Hospital Pharmacies Due to Large Patient Volumes to Lead Growth in the Segment

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

By end user, hospital pharmacies accounted for the largest share. Glioblastoma treatment is highly specialized and usually managed within hospital-based oncology, neurosurgery, and radiation care settings. Since treatment commonly involves surgery, radiotherapy, chemotherapy, supportive medicines, and close monitoring, hospitals remain the primary point of care for drug initiation and ongoing management. This naturally drives higher dispensing through hospital pharmacies than through retail or online channels. In addition, many glioblastoma patients are treated at large cancer centers or specialty hospitals where hospital pharmacy systems are already integrated into the treatment pathway. Due to this care structure, hospital pharmacies are likely to account for the largest share of drug distribution in the market.

- For instance, in August 2025, Novocure announced that patients with newly diagnosed glioblastoma in Spain would be able to access treatment through hospitals and health centers qualified to offer the therapy under the Spanish National Health System. Although this update relates to a broader treatment setting, it clearly reflects how glioblastoma care remains centered in hospital-based channels, which supports the dominance of hospital-linked distribution.

The online pharmacies segment is projected to grow at a CAGR of 7.96% over the study period.

Glioblastoma Drugs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Glioblastoma Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.28 billion and maintained its leading position in 2025 at USD 0.30 billion. The market is growing as the region has a strong neuro-oncology infrastructure, high diagnosis and treatment intensity, and the deepest clinical-trial ecosystem for glioblastoma. It is also benefiting from continued regulatory and pipeline momentum.

U.S. Glioblastoma Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.29 billion in 2026, accounting for roughly 34.34% of the global market.

Europe

Europe is projected to grow at 3.93% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.23 billion by 2026. The market is growing as Europe has well-established cancer registries, broad specialist treatment networks, and increasing access to advanced glioblastoma therapies through both clinical trials and public health systems.

U.K. Glioblastoma Drugs Market

The U.K. market is estimated at around USD 0.05 billion in 2026, representing roughly 5.56% of the global market.

Germany Glioblastoma Drugs Market

Germany's market size is projected to reach approximately USD 0.05 billion in 2026, equivalent to around 6.26% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.19 billion in 2026 and secure the position of the third-largest region in the market. The market is growing as countries in the region are improving advanced cancer care capacity while also increasing local research activity in brain tumors.

Japan Glioblastoma Drugs Market

The Japanese market in 2026 is estimated at around USD 0.04 billion, accounting for approximately 4.82% of the global market.

China Glioblastoma Drugs Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.08 billion, representing approximately 9.22% of global sales.

India Glioblastoma Drugs Market

The Indian market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 2.57% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.06 billion in 2026. The market is growing as access to cancer care is gradually improving, and regional health bodies are pushing harder for greater availability of essential cancer medicines, supplies, and equipment. In the Middle East & Africa, the GCC is set to reach USD 0.02 billion in 2026.

South Africa Glioblastoma Drugs Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.64% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global glioblastoma drugs market is highly consolidated, with companies such as Merck & Co., Inc., Genentech, Inc. (F. Hoffmann-La Roche Ltd), Teva Pharmaceutical Industries Ltd., Camber Pharmaceuticals, Inc., and Sun Pharmaceutical Industries Ltd. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in May 2025, Camber Pharmaceuticals, Inc. launched Temozolomide Capsules, USP. The product is indicated for the treatment of newly diagnosed glioblastoma with radiotherapy and maintenance treatment.

Other notable players in the global market include Accord Healthcare, Fresenius Kabi AG, and Zydus Lifesciences Ltd. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the global market forecast period.

LIST OF KEY GLIOBLASTOMA DRUGS COMPANIES PROFILED

- Merck & Co., Inc. (U.S.)

- Genentech, Inc. (F. Hoffmann-La Roche Ltd) (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Accord Healthcare (India)

- Camber Pharmaceuticals, Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Zydus Lifesciences Ltd. (India)

- Amneal Pharmaceuticals, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: GT Medical Technologies enrolled the first patients in the Beginning Radiation Immediately with GammaTile at Glioblastoma Excision versus Standard of Care (BRIDGES) U.S. clinical trial for newly diagnosed glioblastoma (GBM). The BRIDGES trial is an innovative randomized study evaluating whether implanting GammaTile at the time of surgery can improve the survival outcomes for patients with newly diagnosed GBM.

- December 2025: Curasight A/S completed successful and safe dosing of the first patient in the Phase 1 trial using uTREAT in brain cancer (high-grade gliomas). The news marks the initiation of the first clinical trial under the company’s therapeutic platform uTREAT, investigating it as a potential treatment option for glioblastoma.

- November 2025: Vascarta Inc., in collaboration with the City University of New York (CUNY), announces the publication of a preclinical study demonstrating that STO-1, a first-in-class drug candidate, can selectively eliminate glioblastoma (GBM) cancer cells in mice while avoiding harmful autoimmune reactions.

- November 2025: GenomOncology partnered with the Glioblastoma Foundation to transform genomic testing for the nation's most aggressive brain cancer, glioblastoma. The collaboration integrated GenomOncology's advanced Pathology Workbench (PWB) platform into the Foundation's newly opened genomic testing laboratory, dramatically accelerating patients' access to genetic testing.

- July 2025: Actuate Therapeutics, Inc. announced the end of the Phase 1 portion of its clinical study evaluating elraglusib monotherapy or in combination with irinotecan, irinotecan plus temozolomide, or with cyclophosphamide plus topotecan in pediatric patients with refractory malignancies (Actuate-1902). The company sought to advance the clinical development program toward a Phase 2 study in children, adolescents, and adults with relapsed/refractory EWS.

REPORT COVERAGE

The report provides a detailed global glioblastoma drugs market analysis across key segments. It offers in-depth insights into how standard therapies such as temozolomide, bevacizumab, nitrosoureas, and other treatment options are positioned within the current market landscape. The report also evaluates how treatment demand is evolving across adult and pediatric patient groups, while assessing the commercial role of branded and generic drugs in overall market development. Also, the report delivers a comprehensive outlook of the market across major regions. It examines the key factors driving market growth, major restraints and challenges, and emerging opportunities shaping future expansion. The study also covers the competitive landscape by analyzing leading companies, recent product developments, collaborations, partnerships, and pipeline progress specific to glioblastoma therapeutics. Overall, the report is designed to provide strategic insights into current market dynamics, future growth potential, and the competitive positioning of companies operating in the global market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.82% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug, Drug Class, Age Group, Type, Therapy, Route of Administration, Distribution Channel, and Region |

| By Drug |

|

| By Drug Class |

|

| By Age Group |

|

| By Type |

|

| By Therapy |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 0.79 billion in 2025 and is projected to reach USD 1.21 billion by 2034.

In 2025, the market value stood at USD 0.30 billion.

The market is expected to grow at a CAGR of 4.82% over the forecast period.

The temozolomide segment is expected to lead the market by drug.

The high unmet need for effective glioblastoma therapies is driving market growth.

Merck & Co., Inc., Genentech, Inc. (F. Hoffmann-La Roche Ltd), Teva Pharmaceutical Industries Ltd., and Sun Pharmaceutical Industries Ltd. are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us