Green Aerospace Technology Market Size, Share & Industry Analysis, By Platform (Commercial Fixed-Wing Aircraft, Business and General Aviation, Military Aircraft, Uncrewed Aerial Systems, UAM & eVTOL Platforms, and Space Launch Systems and Spacecraft), By Type (Sustainable Aviation Fuels, Green Propulsion Systems, Aircraft Electrification & Power Systems, Low-Emission Engines, Lightweight Structures & Advanced Materials, & Others), By Level of Integration (Component-Level Technologies, Subsystem-Level Technologies, & Others), By End User, and Regional Forecast, 2026-2034

Green Aerospace Technology Market Size and Future Outlook

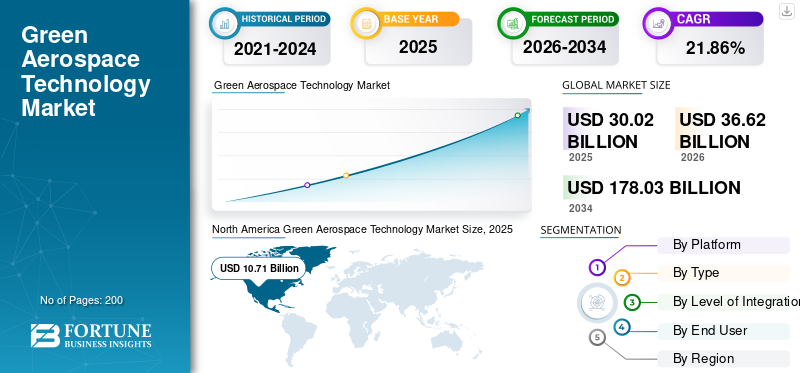

The global green aerospace technology market size was valued at USD 30.02 billion in 2025. The market is projected to grow from USD 36.62 billion in 2026 to USD 178.03 billion by 2034, exhibiting a CAGR of 21.86% during the forecast period. North America dominated the green aerospace technology market with a market share of 35.67% in 2025.

Green aerospace technology encompasses innovations such as sustainable aviation fuels (SAFs), electric/hybrid propulsion, advanced aerodynamics, lightweight materials, and efficient air traffic management to minimize aviation's environmental footprint, including carbon emissions, noise, and fuel use. These are applied in commercial aircraft, helicopters, drones, and operations to enable greener flights worldwide. Key drivers include stringent regulations such as International Civil Aviation Organization (ICAO) emissions standards, net zero targets by 2050, and stakeholder focus for decarbonization.

Major players include Airbus, Boeing, Safran, and Rolls Royce, among others. These companies drive advances in 100% SAF flights and ZEROe hydrogen aircraft, reduced emissions via renewables and supplier alignment, develop hybrid engines, and so on.

Download Free sample to learn more about this report.

GREEN AEROSPACE TECHNOLOGY MARKET TRENDS

Adoption of Sustainable Aviation Fuels is a Market Trend

Adoption of SAFs emerges as a key market trend in green aerospace, driven by regulatory mandates and net zero pledges, yet faces persistent hurdles. High production costs, which far exceed those of conventional jet fuel, deter airlines from adoption. Additionally, limited feedstock availability, competing with other sectors such as road transport, further restricts supply. Furthermore, lengthy certification processes and blend limits create deployment bottlenecks, while policy inconsistencies and financing risks slow scaling despite sufficient long term feedstocks. Airlines prioritize fleet upgrades over SAF amid economic pressures and infrastructure gaps.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Global Regulations is Anticipated to Drive Market Growth

Stringent global regulations serve as a primary market driver for green aviation technology, compelling airlines and manufacturers to adopt low-emission solutions. ICAO's Annex 16 updates establish binding standards for aircraft engine emissions, CO2 efficiency, and noise, mandating fuel-efficient designs and certification compliance for new and modified planes. Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) a global market-based measure by ICAO to stabilize CO₂ emissions offsets international flights, while regional schemes such as EU ETS expand to cover more operations, imposing financial penalties on excess emissions.

MARKET RESTRAINTS

High Sustainable Aviation Fuel Premiums is a Market Restraint

High SAF premiums act as a critical market restraint for green aerospace adoption, significantly elevating operational costs for airlines already strained by volatile fuel prices. SAF costs several times more than regular jet fuel as production is still small-scale, turning feedstocks into fuel is complicated, and getting approvals adds extra expenses.

MARKET OPPORTUNITIES

Net Zero Programs Creates New Market Opportunities

Net zero programs create compelling market opportunities by committing airlines and manufacturers to eliminate emissions through SAF adoption, fleet electrification, and hydrogen propulsion innovations. IATA's Fly Net Zero initiative unites carriers worldwide, spurring investments in low carbon alternative fuels, efficient operations, and carbon removal while signaling demand to suppliers. This unlocked partnerships across energy, agriculture, and tech sectors for feedstock scaling and infrastructure upgrades, positioning compliant firms to capture premium ESG investments and regulatory incentives.

MARKET CHALLENGES

Lengthy Certification Processes and Investment Risks Present a Major Market Challenge

Lengthy certification processes and investment risks present a major challenge caused due to development by delaying commercialization of sustainable aviation fuels, hydrogen aircraft, and electric propulsion systems. Rigorous safety validations under ICAO and FAA standards demand extensive testing for novel feedstocks and powertrains, spanning years amid evolving regulations that amplify uncertainty. Furthermore, high capital outlays for first-of-a-kind facilities face payback doubts due to unproven scales and volatile policy support, deterring financiers wary of technological lock-in.

IMPACT OF U.S. TARIFF WAR

U.S. tariffs from the trade war raised costs for imported SAF fuel stocks from Asia and Latin America, disrupting global supply chains critical for green aerospace production. Furthermore, higher expenses on steel, catalysts, and refinery equipment delayed U.S. SAF plant construction and joint ventures with European partners, slowing innovation and scaling amid aviation technologies net zero push. Additionally, many airlines faced pricier blending options, reducing commitments while competitors in the EU advanced via stable trade ties and mandates.

Segmentation Analysis

By Platform

High Fleet Size and Modernization Programs to Boost Commercial Fixed-Wing Aircraft Growth

Based on the platform, the market is segmented into commercial fixed-wing aircraft, business and general aviation, military aircraft, Uncrewed Aerial Systems (UAS), Urban Air Mobility (UAM) & eVTOL platforms, and space launch systems and spacecraft.

The commercial fixed-wing aircraft segment is anticipated to account for the largest green aerospace technology market share. The segmental growth is driven by primarily high fleet renewal demands and planned modernization programs focused on sustainability by various OEMs and Airlines.

The Urban Air Mobility (UAM) & eVTOL platforms segment is anticipated to rise with a highest CAGR of 22.53% over the forecast period.

By Type

Net Zero Programs to Boost Sustainable Aviation Fuels (SAF) Segment Growth

Based on type, the market is segmented into Sustainable Aviation Fuels (SAF), green propulsion systems, aircraft electrification & power systems, low emission engines, lightweight structures & advanced materials, aerodynamic & aircraft efficiency technologies, and digital & software enabled sustainability.

In 2025, the Sustainable Aviation Fuels (SAF) segment dominated the global market. Aiming for carbon neutrality by 2050, net-zero initiatives are propelling the segmental growth. Furthermore, important programs that require or encourage SAF blending, supply scaling, and technology R&D include the IATA Net Zero 2050 roadmap, the U.S. Inflation Reduction Act (IRA) tax incentives, and Brazil's "Fuel of the Future" statute.

The green propulsion systems segment is projected to grow at a high CAGR of 22.53% over the forecast period.

By Level of Integration

Enhanced Operational Efficiency to Boost Component-Level Technologies Segment Growth

Based on the level of integration, the market is segmented into component-level technologies, subsystem-level technologies, system-level architectures, and aircraft-level configurations.

The component-level technologies segment is anticipated to witness a dominating market share over the forecast period. Component-level integrated solutions (such as lightweight materials and AI-enabled flight controls) help operators to minimize fuel consumption and improve routes which further supports the segmental growth.

The aircraft-level configurations segment is projected to grow at a high CAGR of 23.16% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Improved Fuel Efficiency to Boost Commercial Airlines Segment Growth

Based on end user, the market is segmented into commercial airlines, Business jet operators, defense ministries and armed forces (non-combat systems), OEMs and tier-1 aerospace suppliers, and space agencies and launch service providers.

The commercial airlines segment dominated the segmental market share. The growth for green technologies in the commercial aerospace sector is owing to improved fuel efficiency, as new engines and aircraft designs use less fuel. Moreover, advanced composites are used in newer aircraft types, such as the Boeing 737 MAX and Airbus A350, to enhance fuel efficiency and reduce weight.

In addition, space agencies and launch service providers are projected to grow at a high CAGR of 23.60% during the study period.

Green Aerospace Technology Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Green Aerospace Technology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 8.85 billion, and also maintained the leading share in 2025, with USD 10.71 billion. North America dominates the green aerospace industry through federal programs such as NASA's green engine tech demonstrations and the U.S. SAF Grand Challenge, fostering R&D in ultra-efficient nacelles and hybrid propulsion.

U.S. Green Aerospace Technology Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 7.90 billion in 2026, accounting for roughly 22.09% CAGR. The U.S. drives innovation via Department of Energy (DOE's) SAF initiatives and NASA partnerships with Pratt & Whitney for drag-reducing, low-noise engines using advanced composites and laminar flow.

Europe

Europe is projected to record a steady growth rate of 21.13% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 10.39 billion in 2026. Europe regions growth in such technology is owing to the aim to meet net zero targets by 2050. This is further fueled by major investments in SAF, hybrid-electric systems, and lightweight composite materials by various key players and governments.

U.K. Green Aerospace Technology Market

The U.K. market in 2026 is estimated at around USD 2.87 billion, representing roughly 21.16% CAGR during the study period. The U.K. dominates the Europe region due to an increase in investments supporting technologies such as hydrogen gas turbines, electric aircraft parts, and advanced materials, including research into reducing water vapour trails by government and organizations.

Germany Green Aerospace Technology Market

Germany’s market is projected to reach approximately USD 2.25 billion in 2026. Germany's technologies in the green aerospace industry are expanding quickly, motivated by the country's ambition to lead the world in climate-neutral flight and reach net-zero by 2050. Moreover, investments in hydrogen propulsion, sustainable aviation fuels, and hybrid-electric technology, together with a robust research ecosystem also drives the growth.

Asia Pacific

Asia Pacific region is estimated to reach USD 10.49 billion in 2026 and secure the third position during the study period. The market growth across Asia Pacific is fueled by policy-driven SAF programs and the Asia sustainable aviation fuel Association's launch, transforming regional production and markets.

China Green Aerospace Technology Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 2.83 billion. Growth in China's technologies in green aerospace is driven by mass SAF production from waste oils at Junheng Biology, the first private CAAC-approved facility and new airport initiatives.

Japan Green Aerospace Technology Market

The Japan market in 2026 is estimated at around USD 1.93 billion, accounting for roughly 23.05% of compound annual growth rate (CAGR) during the forecast period. Growth in Japan is driven by 10% SAF mandates by 2030, backed by subsidies, taskforces, and India-Japan pacts for green hydrogen and clean ammonia.

India Green Aerospace Technology Market

The India market in 2026 is estimated at around USD 2.28 billion. Growth in India's sector is owing to the Global Biofuel Alliance, HPCL-Boeing SAF collaborations, and bamboo ethanol projects with emerging blending mandates.

Rest of the World

The rest of the world include the Middle East & Africa and Latin America. Growth in Latin America's green aerospace is driven by abundant biofuels potential from sugarcane and biomass. Growth in the Middle East is owing to energy giants' SAF pilots leveraging oil infrastructure for biofuels and synthetics, amid IATA net-zero alignment. Driven by UAE and Saudi Arabia's sustainability visions, initiatives include Emirates' SAF trials and regional blending policies. The Middle East & Africa and Latin America market is set to reach a valuation of USD 1.63 billion and USD 1.04 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships for Securing Supply Chains and De-risking Scale-up to Fuel Market Expansion

The market remains fragmented as established OEMs coexist with specialized biofuel producers and emerging technologies in propulsion, hydrogen systems, and lightweight materials. Key players in the market include Airbus, Boeing, Safran, Rolls-Royce, GE Aerospace, Neste, TotalEnergies, World Energy, Eni, OMV, Shell, BP, SkyNRG, Fulcrum BioEnergy, LanzaJet, and Gevo, among others.

SAF production partnerships drive the green aerospace technology market growth through strategic collaborations securing supply chains and de-risking scale-up. Neste partners with airlines for long-term offtake of waste-based fuels, while Boeing teams with regional energy firms such as HPCL in India to localize feedstocks and blending infrastructure. Airbus secured renewable power purchase agreements with TotalEnergies for European manufacturing sites, enabling greener ZEROe hydrogen aircraft technologies development.

These alliances bridge feedstock gaps, lower entry barriers for new producers, and align with airline net-zero pledges, positioning partners for regulatory compliance and market premium capture amid rising blending mandates.

LIST OF KEY GREEN AEROSPACE TECHNOLOGY COMPANIES PROFILED

- Airbus (France)

- Boeing (U.S.)

- Safran (France)

- Rolls-Royce (U.K.)

- GE Aerospace (U.S.)

- Neste (Finland)

- TotalEnergies (France)

- World Energy (U.S.)

- LanzaJet (U.S.)

- Gevo (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: In order to provide Sustainable Aviation Fuel (SAF) to three additional major airports in the U.S., Neste and United Airlines have extended their current collaboration. United is now the first commercial airline to acquire SAF for use on flights from Dulles International Airport (IAD) in Washington, D.C., George Bush Intercontinental Airport (IAH) in Houston and Newark Liberty International Airport (EWR) in New Jersey.

- June 2025: A collaboration between Airbus and Air France-KLM will allow Airbus employees to reduce the impact of their business travel by promoting the development of environmentally friendly aircraft fuel. A deal that went into effect at the start of 2025 allows Airbus employees to reserve "SAF Bundles" for business air travel tickets that incorporate a voluntary donation to the purchase of SAF right into the ticket.

- April 2024: For its 2024 U.S. operations, Boeing has announced its yearly purchase of 9.4 million gallons of mixed SAF, a 60% increase over 2023. The 30/70 blend, which comes mostly from Neste, will help commercial flights and the ecoDemonstrator program by cutting lifecycle emissions by up to 85%.

- February 2024: Airbus and TotalEnergies have partnered strategically in order to deal with the challenges of decarbonizing aviation using sustainable aviation fuels. In keeping with the goal of becoming aviation net carbon neutral by 2050, this collaboration seeks to lower the industry's CO2 emissions, with SAF playing a major part. When compared to their fossil fuel counterpart, SAF from TotalEnergies can cut CO2 emissions by up to 90% throughout the course of their lifetime.

- February 2023: In order to support its commercial operations in the U.S. through 2023, Boeing has agreements to buy 5.6 million gallons (21.2 million liters) of blended SAF from Neste, the world's largest producer of SAF. The company's SAF procurement from the previous year has more than doubled as a result of these agreements.

REPORT COVERAGE

The global green aerospace technology industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the aerospace and defense springs market for piston engine over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aerospace industries developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 21.86% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform, Type, Level of Integration, End User, and Region |

| By Platform |

|

| By Type |

|

| By Level of Integration |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 30.02 billion in 2025 and is projected to reach USD 178.03 billion by 2034.

In 2025, the market value stood at USD 10.71 billion.

The market is expected to exhibit a CAGR of 21.86% during the forecast period.

By platform, the commercial fixed-wing aircraft segment is expected to dominate the market.

The stringent global regulations is anticipated to drive market growth.

Airbus, Boeing, Safran, Rolls-Royce, GE Aerospace, Neste, TotalEnergies, World Energy, Eni, OMV, Shell, BP, SkyNRG, Fulcrum BioEnergy, LanzaJet, and Gevo, among others are few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us