Hydrogen Processing Equipment Market Size, Share & Industry Analysis, By Hydrogen Type (Grey Hydrogen, Blue Hydrogen, Green Hydrogen, and Others), By Equipment Type (Hydrogen Production Equipment, Hydrogen Storage Equipment, Hydrogen Compression Equipment, Hydrogen Dispensing Equipment, and Others), By Application (Refining, Ammonia Production, Transportation, Power Generation, and Others), and Regional Forecast, 2026-2034

Hydrogen Processing Equipment Market Size and Future Outlook

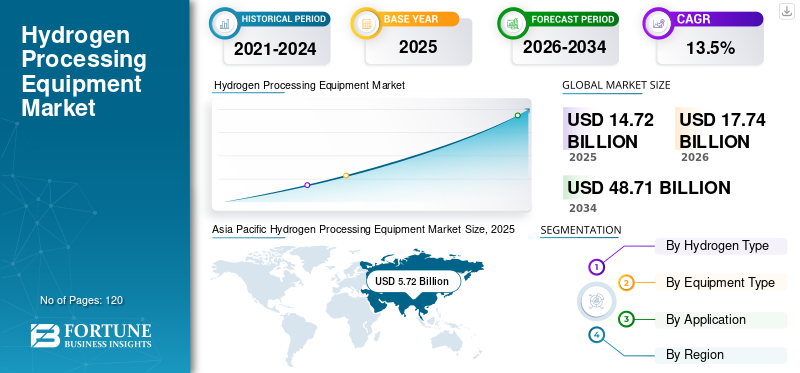

The global hydrogen processing equipment market size was valued at USD 14.72 billion in 2025. The market is projected to grow from USD 17.74 billion in 2026 to USD 48.71 billion by 2034, exhibiting a CAGR of 13.5% during the forecast period. Asia Pacific dominated the hydrogen processing equipment market with a market share of 38.86% in 2025.

Hydrogen processing equipment includes systems used for hydrogen production, storage, compression, purification, and dispensing across industrial and energy applications. These systems play a critical role in enabling hydrogen value chains, supporting decarbonization efforts across refining, ammonia production, transportation, and power generation sectors.

The market is gaining strong momentum due to accelerating investments in green hydrogen projects, expansion of hydrogen refueling infrastructure, and global decarbonization commitments. Governments across North America, Europe, and Asia Pacific are implementing hydrogen roadmaps and funding large-scale electrolysis and hydrogen infrastructure projects. In addition, industrial sectors such as refining and ammonia production are integrating low-carbon hydrogen solutions to meet sustainability targets.

Key players such as Air Liquide, Linde plc, Plug Power Inc., Nel ASA, Siemens Energy, ITM Power, Chart Industries, Cummins Inc., Baker Hughes, and Mitsubishi Heavy Industries are actively expanding hydrogen equipment portfolios.

- For instance, in October 2023, Air Liquide inaugurated a large-scale electrolyzer production facility in Germany to accelerate green hydrogen deployment across Europe.

Download Free sample to learn more about this report.

HYDROGEN PROCESSING EQUIPMENT MARKET TRENDS

Rapid Expansion of Green Hydrogen Infrastructure Pose as a Major Market Trend

A major trend shaping the market is the rapid expansion of green hydrogen projects globally. Electrolyzer capacity additions are accelerating, particularly in Europe and Asia Pacific, to support renewable hydrogen production. Furthermore, investments in hydrogen refueling infrastructure and storage systems are strengthening the hydrogen mobility ecosystem.

- For instance, in 2024, Plug Power commissioned new electrolyzer manufacturing capacity in the U.S. to support large-scale hydrogen generation projects.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Decarbonization Policies Accelerating Hydrogen Infrastructure Investments Drive Market Demand

Global net-zero targets and carbon reduction mandates are primary drivers of hydrogen processing equipment demand. Governments are introducing hydrogen subsidies, tax credits, and funding programs to accelerate infrastructure deployment. Industrial sectors such as refining and ammonia production are increasingly shifting toward low-carbon hydrogen to reduce Scope 1 emissions.

- For instance, in 2024, the U.S. Department of Energy allocated funding under the Hydrogen Hubs program to support hydrogen production and infrastructure development.

MARKET RESTRAINTS

High Capital Costs and Infrastructure Gaps Limiting Adoption

Hydrogen processing equipment requires significant capital investment, particularly for electrolyzers, storage tanks, and compression systems. The cost competitiveness of green hydrogen remains a challenge compared to conventional grey hydrogen. In addition, hydrogen transportation and storage infrastructure remains underdeveloped in several emerging economies.

- For instance, in 2024, industry assessments highlighted cost barriers associated with large-scale hydrogen storage and compression technologies.

MARKET OPPORTUNITIES

Hydrogen Mobility and Power Generation Creating New Growth Avenues

The expansion of hydrogen fuel cell vehicles and hydrogen-based power generation systems presents substantial opportunities for processing equipment providers. Electrolyzer scaling, advanced compression systems, and hydrogen dispensing stations are expected to witness strong demand for hydrogen processing equipment market growth.

- For instance, in 2024, Nel ASA secured contracts for large-scale electrolyzer supply to European renewable hydrogen projects.

Segmentation Analysis

By Hydrogen Type

Grey Hydrogen Dominates Due to Existing Industrial Base

Based on hydrogen type, the market is segmented into grey hydrogen, blue hydrogen, green hydrogen, and others.

The grey hydrogen segment dominates the hydrogen processing equipment market due to its extensive use in refining and ammonia production, which together drive the bulk of global hydrogen demand. Its reliance on cost-effective, well-established technologies such as SMR and existing infrastructure keeps it the largest segment

- For instance, Linde continues to operate large-scale steam methane reforming plants supporting grey hydrogen supply.

The green hydrogen segment is expected to grow with the highest CAGR of 15.6% during the study period, supported by renewable energy integration and electrolyzer capacity expansion.

To know how our report can help streamline your business, Speak to Analyst

By Equipment Type

Hydrogen Production Equipment Leads Due to Electrolyzer Expansion

Based on equipment type, the market is segmented into hydrogen production equipment, hydrogen storage equipment, hydrogen compression equipment, hydrogen dispensing equipment, and others.

The hydrogen production equipment segment holds the highest market share due to the central role of electrolyzers and reformers in hydrogen generation. These systems represent the largest capital investment within the value chain, and their widespread deployment across both conventional and emerging hydrogen projects drives their dominant position in the market.

- For instance, in 2024, Siemens Energy expanded its electrolyzer manufacturing capabilities to support industrial hydrogen production projects.

Hydrogen production equipment is projected to witness strong growth, expanding at a CAGR of 14.7% during the forecast period, driven by accelerating investments in green hydrogen and large-scale project deployments worldwide.

By Application

Refining Sector Leads Owing to Established Hydrogen Demand

Based on application, the market is segmented into refining, ammonia production, transportation, power generation, and others.

The refining segment holds the highest market share, as hydrogen is extensively used in hydrocracking and desulfurization processes to meet fuel quality standards. Its continuous, large-scale demand across global refineries ensures a strong and stable requirement for hydrogen processing equipment.

- For instance, in 2024, Baker Hughes expanded hydrogen compression solutions for refinery applications.

The transportation segment is expected to register the highest CAGR of 16.1% over the forecast period, driven by hydrogen fuel cell vehicle deployment and refueling infrastructure expansion.

HYDROGEN PROCESSING EQUIPMENT MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Hydrogen Processing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest market share and is projected to grow at a CAGR of 15.2% during the forecast period. The region benefits from strong hydrogen roadmaps in China, Japan, and South Korea, along with expanding ammonia and refining industries.

China leads electrolyzer deployment, while Japan focuses on hydrogen mobility and power generation initiatives.

China Hydrogen Processing Equipment Market

China’s market in 2026 is estimated at around USD 3.27 billion, representing approximately 18.4% of global revenues. Government-backed hydrogen industrial clusters and renewable hydrogen investments drive growth.

Japan Hydrogen Processing Equipment Market

Japan’s market in 2026 is estimated at around USD 1.07 billion, representing approximately 6.0% of global revenues. Strong hydrogen fuel cells deployment and national hydrogen strategy support equipment demand.

India Hydrogen Processing Equipment Market

India’s market in 2026 is estimated at around USD 1.08 billion, representing approximately 6.1% of global revenues. The National Green Hydrogen Mission is accelerating infrastructure investments.

North America

North America represents a significant share of the global market, supported by federal hydrogen funding initiatives and expanding industrial decarbonization projects. The U.S. hydrogen hubs program is strengthening domestic hydrogen ecosystems.

U.S. Hydrogen Processing Equipment Market

The U.S. market in 2026 is estimated at around USD 3.11 billion, representing approximately 17.5% of global revenues. Federal incentives and hydrogen infrastructure investments drive growth.

Europe

Europe holds a strong market position driven by aggressive decarbonization goals and the EU Hydrogen Strategy. Electrolyzer deployment and green hydrogen production are expanding rapidly.

U.K. Hydrogen Processing Equipment Market

The U.K. market in 2026 is estimated at around USD 0.76 billion, representing approximately 4.3% of global revenues. Government hydrogen cluster programs drive infrastructure development.

Germany Hydrogen Processing Equipment Market

Germany’s market in 2026 is estimated at around USD 1.08 billion, representing approximately 6.1% of global revenues. Industrial decarbonization programs and hydrogen mobility initiatives support growth.

Middle East & Africa and South America

The Middle East & Africa region is emerging as a major green hydrogen production hub, leveraging abundant renewable resources. Large-scale export-oriented hydrogen projects are strengthening equipment demand.

GCC Hydrogen Processing Equipment Market

The GCC market in 2026 is estimated at around USD 1.18 billion, representing approximately 6.7% of global revenues. Mega-scale green hydrogen projects in Saudi Arabia and UAE support growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Electrolyzer Innovation and Infrastructure Expansion Strengthening Market Position

The hydrogen processing equipment market is characterized by strong competition among industrial gas majors, electrolyzer manufacturers, and engineering firms. Companies are focusing on scaling electrolyzer capacity, advanced compression technologies, and modular hydrogen production systems.

Strategic partnerships and large-scale project deployments remain key competitive differentiators.

LIST OF KEY HYDROGEN PROCESSING EQUIPMENT COMPANIES PROFILED

- Air Liquide (France)

- Linde plc (Ireland)

- Plug Power Inc. (U.S.)

- Nel ASA (Norway)

- Siemens Energy (Germany)

- ITM Power (U.K.)

- Chart Industries (U.S.)

- Cummins Inc. (U.S.)

- Baker Hughes (U.S.)

- Mitsubishi Heavy Industries (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Nel ASA secured a large-scale electrolyzer supply agreement for a European renewable hydrogen project.

- January 2025: Plug Power announced expansion of its electrolyzer manufacturing capacity in New York to support hydrogen hub projects.

- October 2024: Siemens Energy signed agreements to supply electrolyzer systems for Middle East green hydrogen

- August 2024: Air Liquide announced expansion of hydrogen production capacity in North America.

- May 2024: Air Liquide inaugurated a large-scale electrolyzer production facility in Germany.

REPORT COVERAGE

The global report on hydrogen processing equipment market analysis includes a comprehensive study of market size & forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence global market growth over the forecast period. The report also covers technological advancements in digital identity and verification platforms, compliance considerations, and key strategic developments including partnerships and M&A activity, alongside regional insights and competitive landscape analysis. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Hydrogen Type, Equipment Type, Application, and Region |

| By Hydrogen Type |

|

| By Equipment Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 14.72 billion in 2025 and is projected to reach USD 48.71 billion by 2034.

In 2025, the market value stood at USD 5.72 billion.

The market is expected to exhibit a CAGR of 13.5% during the forecast period.

By application, the transportation segment is expected to lead the market.

The global decarbonization policies is the key factor driving the market growth.

Air Liquide, Linde plc, Plug Power Inc., Nel ASA, and Siemens Energy are among the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us